Submarine Cable System Market Size, Share & Industry Analysis, By Component (Wet Plant and Dry Plant), By Cable Type (Subsea Communication Cables and Subsea Power Cables), By Voltage (Medium Voltage (≤66 kV), High Voltage AC (≈110–245 kV), High Voltage DC – Standard Range (±320-525 kV), and Others), By Deployment (New-Build Systems, Upgrades & Extensions, Replacement & Re-Routing, and Others), By Application (Spaceport & Launch Range Connectivity, Missile Test & Weapons Proving Ranges, Integrated Air & Missile Defence (IAMD) Networks, & Others), By End User, and Regional Forecast, 2026-2034

Submarine Cable System Market Size and Future Outlook

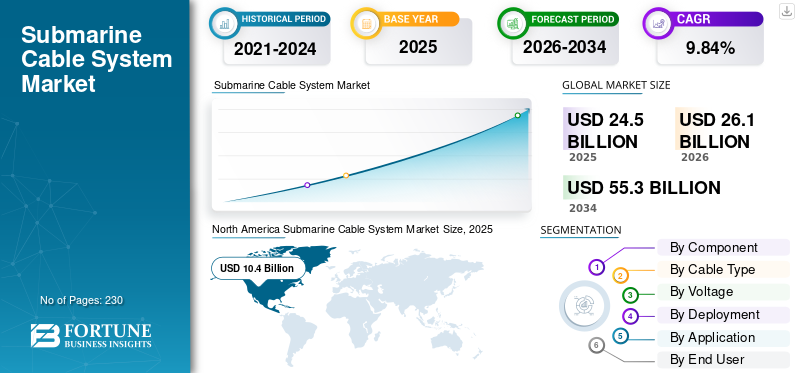

The global submarine cable system market size was valued at USD 24.5 billion in 2025. The market is projected to grow from USD 26.1 billion in 2026 to USD 55.3 billion by 2034, exhibiting a CAGR of 9.84% during the forecast period. North America dominated the global submarine cable system market with a market share of 42.44% in 2025.

The submarine cable system market involves underwater cables used primarily for data transmission and power supply across oceans and seas. These cables connect continents and countries for internet, telecom, and offshore energy projects. Common cables include fiber optic cables for communications and high-voltage power cables for energy transfer. Submarine cable systems are crucial infrastructure for safe, high-capacity communication and data transfer across continents and oceans in the aerospace and defense industry vertical. These cables facilitate strategic data interchange, real-time military communications, and remote control of aeronautical assets such as satellites and drones.

Major players in the market include SubCom, Alcatel Submarine Networks, Prysmian Group, Nexans, and NEC Corporation, who focus on innovation, expansion, and deployment of advanced fiber-optic and power transmission cables globally to meet rising internet connectivity and renewable energy demands.

Download Free sample to learn more about this report.

Submarine Cable System Market Key Takeaways

- 2025 Market Size: USD 24.5 Billion

- 2026 Market Size: USD 26.1 Billion

- 2034 Forecast Market Size: USD 55.3 Billion

- CAGR: 9.84% from 2026–2034

- North America dominated the submarine cable system market with a 42.44% share in 2025.

- The wet plant segment accounted for the largest market share in 2025.

- The subsea communication cables segment captured the largest market share in 2025.

North America

North America led the global market with a 42.44% share and a market size of USD 10.4 billion in 2025.

Asia Pacific

Asia Pacific is projected to record the highest regional CAGR of 10.34% during the forecast period.

Europe

Europe is projected to reach a market size of USD 5.6 billion in 2026.

U.S.

The submarine cable system market is projected to reach USD 6.8 billion in 2026.

Japan

The submarine cable system market is projected to reach USD 1.4 billion in 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

High-Bandwidth and Low-Latency Connectivity is a Market Driver

High-bandwidth, low-latency connectivity from submarine cable systems drives rapid growth by enabling real time control of unmanned aerial vehicles (UAVs), satellite ground stations, and global aerospace coordination networks. These cables provide resilient, secure data links that complement space based systems, supporting mission critical operations including remote sensing and airborne internet access for flight planning and air to air communications. Moreover, the interdependencies with satellite infrastructure amplify demand, as cables offer backup amid vulnerabilities, ensuring uninterrupted high speed data rate transfers essential for modern aerospace platforms. Additionally, the advancements in fiber optics further enhance their role in transporting RF signals for avionics.

MARKET RESTRAINTS

High Installation and Maintenance Costs Restraint Market Growth

High installation and maintenance costs significantly restrain submarine cable system deployment, as specialized cable placing ships, deep sea equipment, and precise route planning demand substantial capital expenditures. Furthermore, life cycle costs encompass construction, repairs, and risk mitigation in challenging ocean terrains further limits the scalability. Such economic barriers necessitate cost-effective path planning and redundancy strategies to optimize infrastructure viability.

MARKET OPPORTUNITIES

Expanding Undersea Sensor Networks Offer Market Opportunity

Undersea sensor networks are composed of multiple underwater sensors and autonomous vehicles. These are increasingly used for extensive ocean monitoring and environmental data collection. Such systems enhance aerospace operations by providing early warning for maritime navigation, flight safety, and environmental monitoring crucial to aerospace situational awareness. The networks also support real-time communication in harsh underwater environments, enabling military reconnaissance, disaster response, and remote asset monitoring. Furthermore, the integration of mobile and static nodes reduces costs and improves coverage, offering a growing opportunity for aerospace applications reliant on accurate oceanic and atmospheric data for operational efficiency and security.

SUBMARINE CABLE SYSTEM MARKET TRENDS:

Integration of Satellite Networks for Hybrid Resilient Communications Is Latest Trend in Market

Integration of satellite networks with submarine cables forms the latest trend in hybrid resilient communications, combining the high capacity, low-latency backbone of undersea fiber optics with the global reach of Low Earth Orbit (LEO) satellites. This collaboration addresses and reduces satellite vulnerabilities such as jamming and further supports international data traffic, ensuring redundancy for mission-critical applications. Additionally, hybrid systems enhance connectivity for remote areas, disaster recovery, and secure data relay, with LEO inter-satellite lasers supplementing cable infrastructure. Such configurations provide scalable, robust networks vital for global digital resilience and operational continuity.

MARKET CHALLENGES:

Cybersecurity Threats Pose a Significant Challenge in Submarine Cable System Networks

Submarine cable systems face growing cybersecurity threats, particularly from state-sponsored actors targeting critical communication infrastructure for espionage, sabotage, and traffic manipulation. Advanced persistent attacks take advantage of flaws in cable landing stations, such as firmware backdoors, malware implants, and hijacking of the Border Gateway Protocol (BGP) to intercept or reroute traffic. These hacks have the potential to compromise mission-critical activities by interfering with defense and aerospace communications that depend on underwater cables.

Russia Ukraine War Impact:

The Russia Ukraine war has considerably impacted submarine cable systems, with Russia suspected of conducting covert sabotage and hybrid warfare operations targeting critical undersea communication infrastructure supporting Ukraine and its allies. Since the war began, multiple undersea cables and power lines in the Baltic Sea and surrounding regions have been damaged. These actions aim to disrupt Western communications, weaken surveillance and impose hybrid conflict beyond traditional battlefields.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component

Rising Ultra High-Capacity Routes Drive Wet Plant Segment Growth

On the basis of the market segmentation of component, the market is bifurcated into wet plant and dry plant.

The wet plant segment accounts for the dominant submarine cable system market share in 2025. The growth in this segment is owing to continuous deployment by major defense and armed forces of new high capacity cables on strategic routes, which support most of the project capex.

Dry Plant segment is expected to grow at a highest CAGR of 10.12% over the forecast period.

By Cable Type

Rise in Secured International Connectivity is Anticipated to Drive Subsea Communication Cables Segment

Based on cable type, the market is bifurcated into subsea communication cables and subsea power cables.

Subsea communication cables segment captured the largest share of the market in 2025. The growth in this segment is owing to rising requirements for secured, low latency connectivity between North America and allied regions for commercial, governmental and defense traffic.

Subsea power cables segment is expected to grow at a highest CAGR of 10.05% over the forecast period.

By Voltage

Efficiency and Cost Effectiveness is Anticipated to Boost High Voltage DC – Standard Range (±320–525 kV) Segment Growth

Based on voltage, the market is segmented into medium voltage (≤66 kV), high voltage AC (≈110–245 kV), high voltage DC – standard range (±320–525 kV), and others.

The High Voltage DC – Standard Range (±320–525 kV) segment held the dominating position in 2025. The growth in this segment as the ±320–525 kV range achieves superior transmission efficiency with minimal energy losses over long distances. This balance drives widespread adoption in various submarine communication cable projects which boosts the segment for dominant market expansion.

The segment of High Voltage AC (≈110–245 kV) is set to flourish and is growing at a highest CAGR of 10.04% growth across the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Rise in Strategic Diversification Initiatives to Boost New-Build Systems Segments

Based on deployment, the market is classified into new-build systems, upgrades & extensions, replacement & re-routing, and others.

New-Build Systems segment held the dominating position in 2025. The growth in this segment is owing to initiatives to open additional corridors that reduce reliance on existing chokepoints and provide alternative landings for critical networks by major countries and allied regions.

Upgrades & Extensions segment will witness a highest growth rate of 10.32% growth across the projected period.

By Application

Expanding Surveillance Requirements Supporting Maritime Tests Segment Growth

Based on application, the market is classified into spaceport & launch range connectivity, missile test & weapons proving ranges, integrated air & missile defense (IAMD) networks, maritime tests, unmanned systems & multi-domain test corridors, space surveillance & deep, space science data transport, and others.

The maritime tests segment held the leading position in 2025. The growth in this segment is owing to rise in broader monitoring and surveillance tests of key sea lanes, major routes using seabed infrastructure cables.

The segment of Unmanned Systems & Multi-Domain Test Corridors will witness a highest growth rate of 10.55% growth across the forecast period.

By End User

Network Modernization Programs Supports Defense & Armed Forces Segment Growth

Based on end user, the market is classified into defense & armed forces, space agencies, homeland security agencies, alliance structures, and others.

The defense & armed forces segment held the leading position in 2025. The growth in this segment is owing to network modernization initiatives by governments. These initiatives upgrade cable systems to support real time data sharing, UAV control, and satellite integration, driving demand for resilient undersea infrastructure.

Homeland security agencies segment will witness a highest growth rate of 10.50% growth across the forecast period.

Submarine Cable System Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and Rest of the World.

NORTH AMERICA

North America Submarine Cable System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the leading share in 2024 valuing at USD 9.9 billion and also took the dominating share in 2025 with USD 10.4 billion. The market for submarine cable systems in North America is expanding owing to the government focus on secure digital infrastructure, rise in substantial private investment, and strong demand from data intensive services. Moreover, rise in government programs along with partnerships with major tech firms such as Google, Meta due to increased international data traffic, are the main drivers of growth in the US. In 2026, U.S. market is projected to reach USD 6.8 billion.

EUROPE and ASIA PACIFIC

Regions such as Europe and Asia Pacific are expected to witness a notable submarine cable system market growth during the projected years. During the projected period, Asia Pacific submarine cable systems market is projected to record 10.34% CAGR during the forecast period, which is the greatest among all the areas. The Asia Pacific market is expanding owing to the need for improved connection brought about by digital transformation, including cloud services and 5G networks, which boost data traffic. Supported by these elements, countries including China anticipates to record the evaluation of USD 2.1 billion, Japan to record USD 1.4 billion, and India to record USD 1.7 billion in 2026. After Asia Pacific, the market in Europe is valued to touch USD 5.6 billion in 2026. European regions strategic location, vast digital and energy infrastructure requirements, and thriving telecom industry are the main drivers of the continent's submarine cable system expansion. In regions, the U.K. and Germany both are projected to reach USD 1.6 billion and 1.2 billion each in 2026.

REST OF THE WORLD

Over the projected period, Rest of the World includes Middle East and Africa and Latin America regions which would witness a moderate growth in this market space. Middle East and Africa market in 2026 is set to record USD 1.2 billion as its valuation. Latin America is projected to reach the value of USD 0.7 billion 2026. The growth is driven by the strategic significance of a high-capacity, secure communication infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Rise in Mergers and Acquisitions along with Infrastructure Innovations Define Submarine Cable System Market Landscape

The submarine cable system market features dominant players including Alcatel Submarine Networks, SubCom, NEC Corporation, Prysmian Group, and Nexans. These key players are focusing on high-capacity fiber and resilient wet plant solutions to gain competitive edge in the market. Recent strategic partnerships and acquisitions enhanced global deployment capabilities and technological integration. Furthermore, expansion of secure defense networks alongside offshore renewable interconnectors bolsters infrastructure reliability. Additionally, industry leaders prioritize HVDC advancements and secure supply chains, with strong momentum in Asia Pacific and Europe driven by investments in offshore wind power cable projects, defense infrastructure and regulatory frameworks.

LIST OF KEY SUBMARINE CABLE SYSTEMS COMPANIES PROFILED:

- SubCom (U.S.)

- Alcatel Submarine Networks (France)

- NEC Corporation (Japan)

- HMN Technologies (China)

- Prysmian Group (Italy)

- Nexans (France)

- NKT A/S (Denmark)

- Hengtong Group (China)

- ZTT Submarine Cable & System (China)

- Global Marine Group (U.K.)

KEY INDUSTRY DEVELOPMENTS:

- February 2025: Space Norway and SubCom have signed a contract for the Arctic Way Cable System's whole system supply, which includes design, production, installation, and survey scheduled to start operating in 2028.

- February 2025: A European Memorandum of Understanding (MoU) has been signed by six European parties, including Cinia Oy, NORDUnet A/S, Tusass A/S, the Dutch Subsea Cable Coalition, GlobalConnect AB, and Tampnet AS. The parties have acknowledged the strategic importance of building a Pan Arctic Cable System (PACS) between Europe and Asia via the Arctic and North America.

- March 2025: LIBERTY NETWORKS, GOLD DATA, SPARKLE formed a partnership named “The MANTA” have announced that SubCom has been given the contract to design, manufacture, and install the MANTA system, and the agreement has come into effect (CIF). By connecting major data hubs in Mexico City, Queretaro, Bogota, and Panama City with the U.S. Via new landing access points in Veracruz, Mexico, and San Blas, Florida, MANTA seeks to enhance traffic flow in the area.

- May 2025: Dr. Bernd Drapp, Innovation Director at AP Sensing, received the Best Newcomer Award at the Undersea Defence Technology (UDT) 2025 conference in Oslo for his presentation on how Distributed Acoustic Sensing (DAS) improves the security of vital subsea infrastructure.

- December 2024: Telecom Italia and Italy's Fincantieri agreed to create systems for monitoring and safeguarding underwater communications cables. According to a joint statement from the corporations, the agreement intends to guarantee the operational stability of infrastructure, which is thought to be crucial for Italy's connectivity and technological sector growth.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key Submarine Cable System industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.84% from 2026-2034 |

| Unit | Value (USD Billion ) |

| Segmentation | By Component, Solution, Cable Type, Voltage, Deployment, Application, End User and Region |

| By Component |

|

| By Cable Type |

|

| By Voltage |

|

| By Deployment |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 24.5 billion in 2025 and is projected to reach USD 55.3 billion by 2034.

In 2025, the market value stood at USD 10.4 billion.

The market is expected to exhibit a CAGR of 9.84% during the forecast period of 2026-2034.

New-Build systems segment dominated the market by deployment.

High-Bandwidth and low-latency connectivity is an market driver.

Alcatel Submarine Networks, SubCom, NEC Corporation, Prysmian Group, Nexans are some of the key players in the market.

North America dominated the Submarine Cable System market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 230

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us