Super High Frequency Communication Market Size, Share, Industry Analysis and Industry Analysis, By Technology (5G sub-6.0 GHz, 5G mm-Wave, LEO SATCOM, Radar, and Others), By Frequency (3 - 10 GHz, 10 - 20 GHz, 20 - 30 GHz, 30 - 40 GHz, and Above 40 GHz), By Radome Type (Sandwich, Solid Laminate, Multi-layer System, Tensioned Fabric, and Other), By End User (Space & Strategic Command, Military Aviation & UAVs, Naval combatants & maritime security, Land Forces & Tactical Networks, and Aerospace OEMs & MRO), and Regional Forecast, 2026-2034

SUPER HIGH FREQUENCY COMMUNICATION MARKET SIZE AND FUTURE OUTLOOK

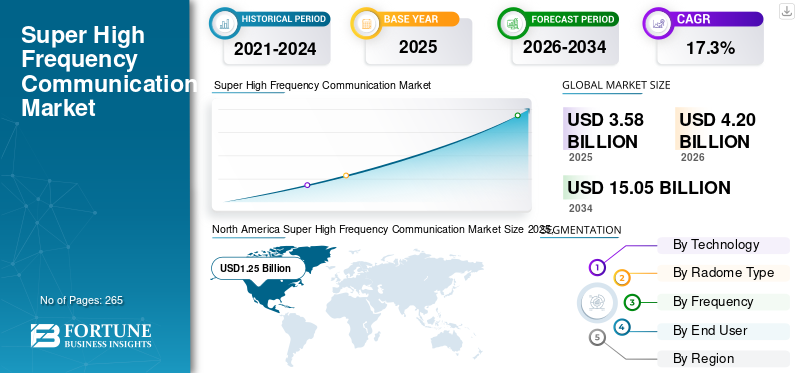

The global super high frequency communication market size was valued at USD 3.58 billion in 2025. The market is projected to grow from USD 4.20 billion in 2026 to USD 15.05 billion by 2034, exhibiting a CAGR of 17.3% during the forecast period. North America dominated the super high frequency communication market with a market share of 34.92% in 2025.

The market share is entering a robust growth phase, propelled by advances in wireless communication, 5G networks, and satellite-based connectivity. SHF technology operates within the 3 GHz–30 GHz spectrum, providing large bandwidth and high data rates essential for critical applications in military, defense, telecommunications, and aerospace sectors. The rapid proliferation of IoT devices, smart city projects, and advanced low-Earth orbit satellites is escalating demand for networks that can support ultra-fast data transmission and secure communication. SHF communication also enables advanced radar systems and broadband connectivity in remote regions, making it indispensable for government, commercial, and industrial players seeking resilient, high-performance solutions. Besides 5G and satellite, defense agencies rely on SHF for secure satellite links, electronic warfare, and high-resolution radar imaging, further solidifying market momentum.

The super high frequency (SHF) communication market is driven by a mix of prime defense contractors, RF specialists, and materials experts. L3Harris Technologies, Inc. and Northrop Grumman lead with advanced SHF radios, data links, and satellite payloads for complex defense and space networks. General Dynamics Corporation adds secure SHF communication systems for tactical and strategic users. Cobham Limited, Astronics Corporation, Hensoldt, and JENOPTIK AG contribute high-performance RF, EW, and test solutions that enable reliable operation in dense electromagnetic environments.

Download Free sample to learn more about this report.

Super High Frequency Communication Market Key Takeaways

- 2025 Market Size: USD 3.58 billion

- 2026 Market Size: USD 4.20 billion

- 2034 Forecast Market Size: USD 15.05 billion

- CAGR: 17.3% from 2026–2034

- North America dominated the super high frequency communication market with a 34.92% share in 2025.

- LEO SATCOM is expected to account for 34.67% of the market in 2026.

- Military aviation & UAVs is projected to hold a 28.66% share in 2026.

North America

North America reached USD 1.25 billion in 2025 and is projected to maintain its leadership in 2026.

Europe

Europe is expected to reach USD 1.23 billion in 2026, growing at a CAGR of 30.7%.

Asia Pacific

Asia Pacific is projected to attain a market value of USD 1.32 billion in 2026.

U.S.

The market is estimated to reach USD 1.26 billion by 2026.

Japan

The market is expected to witness steady growth supported by expanding satellite communication investments.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Growth in Data-Centric Networks and Defense Requirements are Boosting Market Growth

The primary driver for SHF communication adoption is the relentless need for data-centric networks that offer high-speed, low-latency, and resilient transmission pathways. Next-generation wireless systems, principally 5G and satellite communications, rely heavily on SHF bands to ensure mass connectivity for urban populations, supporting millions of IoT devices concurrently. The defense sector additionally propels market growth, leveraging SHF for advanced electronic warfare, secure satellite backhaul, and high-resolution radar imaging. Investments by governments and private firms in expanding radar, secure communication, and 5G infrastructure underpins the agility, security, and scalability vital to digital modernization in critical industries. The combination of resilient, high-speed networks and mission-critical defense requirements keeps SHF communication at the forefront of technological evolution.

MARKET RESTRAINTS

Spectrum Regulation and Capital Expenditure to Hamper Market Growth

The SHF communication market faces considerable restraints, notably in spectrum allocation, regulation, and high upfront investment. As the demand for high-frequency band grows, obtaining regulatory clearance and accessing unencumbered spectrum can hinder rapid deployment, especially in regions with stringent spectrum management policies. The cost required to develop, install, and operate SHF infrastructure such as mmWave towers, advanced radios, and high throughput satellites presents challenges for smaller firms and emerging economies. Technological obsolescence and rapidly changing standards require continual investments, while frequency interference and signal attenuation at higher bands sometimes limit practical range and reliability. Taken together, regulatory hurdles and economic burdens can slow market penetration and the scaling of new solutions.

SUPER HIGH FREQUENCY COMMUNICATION MARKET TRENDS

Ascendance of 5G mmWave and Satellite Networks Driving Rapid Expansion

A dominant trend in the super high frequency communication market growth is the expansion of 5G mmWave technology in urban and rural connectivity, as well as the increasing installation of LEO and Ka-band satellites. Telecom giants such as AT&T, Verizon, and China Telecom are aggressively deploying mmWave infrastructure in the 24–30 GHz band, targeting ultra-fast mobile internet and high-bandwidth applications for IoT, smart cities, and industrial automation. The use of advanced radar systems in military and civil aviation is also accelerating in the 10–20 GHz segment. The pursuit of digital transformation, high-speed data, and reliable connectivity is pushing manufacturers and solution providers to focus on product launches centered around interoperability and scalability. These trends combine to drive aggressive network upgrades and wider adoption of SHF technology in both established and emerging markets.

Download Free sample to learn more about this report.

MARKET OPPORTUNITIES

IoT Ecosystem and Next-Generation Satellite Communication to Accentuate Market Growth

The most promising opportunity in the SHF market revolves around the exponential growth of IoT devices and next-generation satellite communication. As more industries such as logistics, healthcare, energy, and urban management integrate IoT sensors and controls, the need for robust, low-latency SHF networks intensifies. The ongoing evolution of LEO and Ka-band satellites, capable of supporting broadband internet and secure communication over vast distances, is fueling demand in remote and underserved regions. Innovations in smart antenna design, spectrum management, and high-capacity data transfer further expand market opportunities for vendors and service providers seeking to deliver cutting-edge connectivity solutions. The proliferation of 5G-enabled IoT modules and connected devices ensures sustained market expansion as enterprises invest in more reliable, ultra-fast communication platforms.

MARKET CHALLENGES

Interoperability, Environmental Factors, and Technology Lifecycle Are Major Market Challenges

Critical challenges in the SHF communication market center on achieving seamless interoperability across devices and networks, managing environmental effects, and addressing the fast-paced technol

The most promising opportunity in the SHF market revolves around the exponential growth of IoT devices and next-generation satellite communication. As more industries such as logistics, healthcare, energy, and urban management integrate IoT sensors and controls, the need for robust, low-latency SHF networks intensifies. The ongoing evolution of LEO and Ka-band satellites, capable of supporting broadband internet and secure communication over vast distances, is fueling demand in remote and underserved regions. Innovations in smart antenna design, spectrum management, and high-capacity data transfer further expand market opportunities for vendors and service providers seeking to deliver cutting-edge connectivity solutions. The proliferation of 5G-enabled IoT modules and connected devices ensures sustained market expansion as enterprises invest in more reliable, ultra-fast communication platforms.

ogy lifecycle. Ensuring smooth integration between legacy systems and new high-frequency platforms is both a technical and commercial hurdle. SHF signals are highly susceptible to environmental factors such as rain fade, atmospheric absorption, and physical obstructions, which can degrade performance, particularly at higher frequencies. Ongoing technological advancements demand frequent upgrades and retraining, making long-term investment riskier for stakeholders. As the industry continues to innovate, balancing speed, reliability, scalability, and cost-efficiency comprises a persistent market challenge.

SEGMENTATION ANALYSIS

By Technology

LEO SATCOM Demand Climbs as Latency, Coverage, and Pricing Unlock New Use-Cases

By technology, the market is segmented into 5G sub-6.0 Ghz, 5G mm-wave, LEO SATCOM, radar, and others.

The LEO SATCOM segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 34.67% share. Sub-50 ms round-trip latency enables real-time apps where fiber is absent or fragile. Multi-constellation roaming, falling terminal costs, and flexible bandwidth plans de-risk adoption for aviation, maritime, and remote enterprise. Governments value path diversity for resilience, converting pilots into multi-year contracts across mobility and edge-cloud workloads.

The 5G mm-wave segment is expected to grow at a CAGR of 17.7% over the forecast period.

By Radome Type

Sandwich Radomes Demand Grows as Strength-To-Weight Meets Broadband Transparency

The radome type segment is classified into sandwich, solid laminate, multi-layer system, tensioned fabric, and other.

The sandwich segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 45.90% share. Honeycomb/foam cores deliver high stiffness and low RF loss, crucial for Ku/K terminals on aircraft and ships. They tolerate harsh environments, simplify certification, and support multi-band apertures. Retrofit waves and line-fit standardization make sandwich the default choice as operators push higher throughput without aerodynamic or thermal penalties.The multi-layer system segment is expected to grow at a CAGR of 18.3% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Frequency

10–20 GHz Band Demand Expands Due to its Capacity Reliability Sweet Spot

The frequency segment is classified into 3 - 10 GHz, 10 - 20 GHz, 20 - 30 GHz, 30 - 40 GHz, and above 40 GHz.

The 10 - 20 GHz segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 28.40% share. This slice balances rain-fade resilience with ample bandwidth, covering much licensed microwave and Ku satcom. Carriers lean on it for 5G backhaul where fiber lags; mobility operators value stability across climates. Mature components, available spectrum, and proven planning tools reduce rollout risk, permitting faster, cheaper network extensions.

The 20 - 30 GHz segment is expected to grow at a CAGR of 18.1% over the forecast period.

By End User

Military Aviation & UAVs Demand Surges as Missions need Low-latency BLOS

The end user segment is classified into space & strategic command, military aviation & UAVs, naval combatants & maritime security, land forces & tactical networks, and aerospace OEMs & MRO.

The military aviation & UAVs segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 28.66% share. Fighter, transport, and MALE/HALE UAV fleets rely on SHF (X/Ku/10–20 GHz) for beyond-line-of-sight C2, ISR offload, and secure AEW/ELINT links. Higher sensor data rates, multi-domain ops, and SATCOM-on-the-move drive upgrades to multi-band terminals with sandwich radomes, anti-jam waveforms, and multi-orbit resilience to keep links up under contested EM conditions.

The space & strategic command segment is expected to grow at a CAGR of 17.7% over the forecast period.

SUPER HIGH FREQUENCY COMMUNICATION MARKET REGIONAL OUTLOOK

In terms of region, the market is divided into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America held the dominant super high frequency communication market share in 2024 valuing at USD 1.07 billion and also took the leading share in 2025 with USD 1.25 billion. North America demand rises as mobility, defense, and rural gaps need resilient links. Airlines upgrading in-flight connectivity, offshore energy and Arctic shipping, and FirstNet-style public-safety networks keep SHF spend elevated. Defense programs prioritize anti-jam X/Ku paths and multi-orbit resilience. Rural broadband subsidies and microwave backhaul bridge fiber deserts. Buyers want certified sandwich radomes, GaN front-ends, and service contracts that cap opex.

North America Super High Frequency Communication Market Size 2025,(USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2026, the U.S. market is estimated to reach USD 1.26 billion. The country’s demand accelerates as scale, budgets, and regulation align. Large airline retrofits, DoD’s resilient satcom push, and USDA/BEAD-backed rural programs sustain spend. Utilities and telcos use licensed SHF backhaul to harden grids and extend coverage. Certification regimes drive adoption of proven sandwich radomes, while competitive service offerings and spectrum clarity compress deployment timelines and total cost.

Europe

During the forecast period, the European region is projected to record a growth rate of 30.7% and touch a valuation of USD 1.23 billion in 2026. Europe demand grows as sovereignty and spectrum discipline shape long-horizon buys. IRIS² and national GOVSATCOM signal sustained procurement, while North Sea/Baltic lanes require reliable Ku links. Rail corridors and cross-border logistics use licensed microwaves where fiber is slow. Cybersecurity and export controls push interoperable, assured-access terminals. Environmental regulations favor low-loss radomes and energy-efficient gateways to meet climate targets.

Asia Pacific

The market in Asia Pacific is estimated to reach USD 1.32 billion in 2026. Asia Pacific demand surges as fleets expand across vast, under-fibered geographies. Rapid civil aviation growth, archipelagic logistics, and offshore energy drive Ku/K adoption. Carriers densify 4G/5G with SHF microwave backhaul across mountains and islands. Disaster-prone regions prioritize always-on links. Rugged sandwich radomes and affordable terminals win, while multi-constellation roaming reduces downtime for mining, fisheries, and remote enterprise sites.

Rest of the World

The rest of the World market in 2026 is set to record USD 0.19 billion as its valuation. Rest of world demand holds as critical industries operate far from fiber. Latin America and the Middle East & Africa rely on SHF for pipelines, mining, and remote health/education. Government continuity and disaster response need quick-deploy terminals and microwave hops. Further, maritime fisheries demand dependable coverage. Budget constraints favor managed services, shared gateways, and phased ground upgrades that extend life of existing infrastructure.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Demand Concentrates with Integrators of Protected Links and Certified Hardware

Astronics Corporation advances aircraft power/IFC integration that eases fleet retrofits. Cobham Limited supplies maritime/aviation terminals and NGSO-ready ground stations. Raycap protects sites with surge/EMC solutions. General Dynamics Corporation and L3Harris Technologies, Inc. deliver secure defense satcom. Hensoldt and JENOPTIK AG provide RF sensors/subsystems; Northrop Grumman leads protected payloads. Saint-Gobain and The NORDAM Group LLC furnish low-loss, certified radome materials and structures critical to multi-band performance, environmental durability, and compliance anchoring reliability from airframes and ships to fixed gateways.

LIST OF KEY SUPER HIGH FREQUENCY COMMUNICATION COMPANIES PROFILED

- Astronics Corporation (U.S.)

- Cobham Limited (U.K.)

- Raycap (U.S.)

- General Dynamics Corporation (U.S.)

- Hensoldt (Germany)

- JENOPTIK AG (Germany)

- L3Harris Technologies, Inc. (U.S.)

- Northrop Grumman (U.S.)

- Saint-Gobain (France)

- The NORDAM Group LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- August 2024 - China launched what is believed to be the first geosynchronous-orbit SAR satellite. Its L-band sensor enables 24/7, all-weather imaging over China and nearby regions to strengthen disaster response.

- July 2024 - SpaceX’s Falcon Heavy deployed Maxar’s Jupiter-3, billed as the largest commercial comsat to date. The craft joins the Hughes Jupiter constellation to expand broadband service across the Americas.

- May 2023 - Thuraya and SAT Global completed an over-the-air demo of direct-to-satellite IoT texting, delivering low-latency, low-power messages via the Thuraya-2 (T2) network.

- April 2024 - Quectel introduced the BG95-S5 satellite module for 3GPP Release 17 IoT-NTN, operating on S and L bands. It’s multi-mode, adding LTE Cat M1, Cat NB2, GPRS, and integrated GNSS.

- February 2023 - Thales won a deal to equip the French Navy with Syracuse IV naval stations, upgrading communications with dual-band X/Ka capability.

REPORT COVERAGE

This report delivers a tight, deep dive into the SHF communication ecosystem profiling top infrastructure developers and operators, the core radome-related components (pads, charging, control systems, and passenger processing), and the main use cases from urban air mobility to regional corridors. It charts policy milestones, pilot trials, and live build-outs now in motion, and pinpoints the shifts setting up the next deployment wave. Together, these threads explain the recent surge and what will propel the market’s next stage of growth.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

| Attributes | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 17.3% from 2026-2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Technology

|

|

By Radome Type

|

|

|

By Frequency

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 3.58 billion in 2025 and is estimated to reach USD 15.05 billion by 2034.

The market is growing at a CAGR of 17.3% during the projection period.

The LEO SATCOM segment is estimated to be the leading segment in this market during the forecast period.

The 10 - 20 GHz segment is estimated to be the leading segment in this market during the forecast period.

Astronics Corporation, Cobham Limited, Raycap, General Dynamics Corporation, Hensoldt, and JENOPTIK AG are some of the leading players in the market.

North America is projected to be the largest shareholder in the market.

- 2021-2034

- 2025

- 2021-2024

- 265

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us