Superconductors Market Size, Share & Industry Analysis, By Type (NbTi (LTS), Nb3Sn (LTS), and HTS (REBCO/Bi/MgB2)), By Application (MRI & Medical Imaging, Fusion & Particle Accelerators, Research Magnets, Power & Grid, and Others), and Regional Forecast, 2026-2034

Superconductors Market Size and Future Outlook

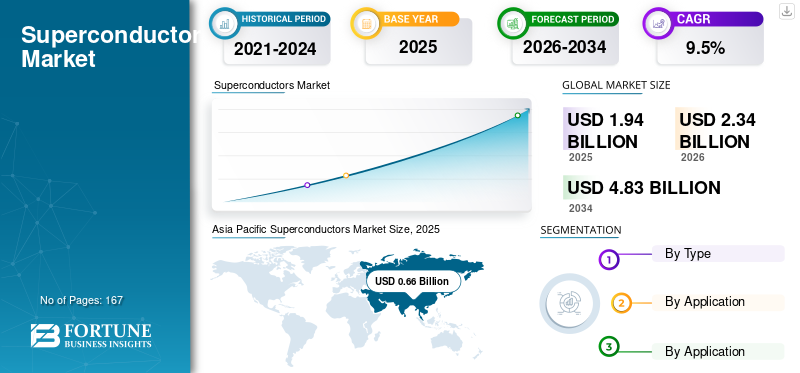

The global superconductors market size was valued at USD 1.94 billion in 2025. The market is projected to grow from USD 2.34 billion in 2026 to USD 4.83 billion by 2034, exhibiting a CAGR of 9.5% during the forecast period. Asia Pacific dominated the superconductors market with a market share of 34.02% in 2025.

Superconductors are materials that exhibit zero Direct Current (DC) electrical resistance below a critical temperature, thereby enabling exceptionally high current density and strong magnetic fields. The commercial demand is primarily driven by superconducting materials rather than bulk materials. These conductors are generally provided in the following forms:

- Multifilament LTS wire and cable (e.g., NbTi, Nb₃Sn) designed for Magnetic Resonance Imaging (MRI) and high-field magnet applications.

- HTS tape, such as REBCO/2G coated conductors, some Bi-based varieties, and MgB₂ used as a conductor class in certain cryogenic applications.

These materials are utilized in MRI magnets, research and NMR magnets, particle accelerators, fusion magnets, and emerging power applications such as High Temperature Superconductor (HTS) cables, fault current limiters, and high-power rotating machinery. A significant driver of demand is the increasing intensity of high-field magnet construction, including fusion devices, accelerators, and high-field research facilities, coupled with the ongoing replacement cycle of existing MRI systems. Additionally, grid constraints and the push toward electrification drive long-term demand for High Temperature Superconductors (HTS) in power devices and cables. The market is further influenced by specialized suppliers and ecosystems, including Low-Temperature Superconductor (LTS) wire producers, HTS tape manufacturers, and system integrators/Original Equipment Manufacturers (OEMs).

Furthermore, the market is dominated by several major players, including Bruker, Sumitomo Electric Industries, Ltd., SuperPower Inc., Fujikura Ltd., and THEVA Dünnschichttechnik GmbH, which are at the forefront of the industry. A broad portfolio, innovative product launches, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

SUPERCONDUCTORS MARKET TRENDS

HTS Adoption Is Shifting Value Pool toward High-Field and Power-Intensive Use Cases

A significant trend is the gradual transition of value from traditional LTS-dominant markets toward HTS-enabled applications. Although the total mass of HTS used remains lower than that of NbTi, HTS commands a considerably higher effective price due to its common valuation in $/kA·m and as thin-coated-conductor tapes have significantly less mass per unit of current capacity than LTS wires. Consequently, the market’s value growth is structurally more influenced by HTS penetration than by volume expansion.

This trend is most pronounced in compact fusion concepts, high-field research magnets, and hybrid magnet systems, where HTS inserts enable magnetic fields exceeding the practical limits of LTS. Concurrently, HTS is progressively regarded as a viable solution for high-capacity power delivery constrained by right-of-way limitations, where the advantages at the system level, such as capacity density and thermal headroom, are of greater significance than the conductor mass.

MARKET DYNAMICS

MARKET DRIVERS

Installed-Base MRI Demand and Program-Scale High-Field Magnet Builds are Accelerating Adoption

Magnetic Resonance Imaging (MRI) continues to account for the largest volume of superconducting conductors. The existing installed base facilitates consistent replacement cycles and the development of new systems, with NbTi remaining the predominant material for conventional MRI field strengths. This establishes a reliable baseline of demand that is less susceptible to volatility compared to project-driven scientific procurement.

Simultaneously, fusion and accelerator projects induce abrupt shifts in demand. Large magnet systems require substantial quantities of Nb₃Sn and NbTi throughout construction, whereas next-generation designs more frequently integrate HTS inserts to reach higher field regions. Consequently, this results in multi-year demand fluctuations that can significantly alter the demand composition, particularly for Nb₃Sn and HTS.

Finally, electrification and grid congestion are driving interest in superconducting power applications, where capacity density and thermal constraints are the predominant factors. Although smaller than current magnets, these deployments disproportionately enhance HTS's value and facilitate long-term market expansion beyond magnet applications. These factors are expected to drive the superconductors market growth.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

HTS Cost, Qualification Burden, and Cryogenic Complexity Can Slow Substitution

High-Temperature Superconductors (HTS) remain costly in terms of $/kA·m across numerous mainstream applications. Many clients are unable to justify the overall system expenses, including conductor, cryogenics, and integration, compared to conventional technologies, unless there is a significant requirement for space or enhanced performance. Consequently, the adoption of HTS is primarily confined to premium applications rather than widespread commodity uses.

Qualification cycles are typically extensive and conformist. Purchases, including MRI systems, high-field magnets, and automotive-grade power modules, require comprehensive validation procedures that encompass thermal cycling, mechanical stress testing, and performance consistency across batches. Consequently, this imposes limitations on rapid transitions and impedes the adoption of new suppliers and innovative chemistries and architectures.

Cryogenic infrastructure also restricts wider adoption. Even when conductor performance is impressive, implementation may be hindered by cryogenic service networks, uptime requirements, safety standards, and limited operational familiarity, especially within industrial sectors.

MARKET OPPORTUNITIES

HTS Manufacturing Scale-Up and Standardization Can Unlock New Demand Pools

The most immediate opportunity lies in the expansion of HTS manufacturing and the enhancement of yield, thereby decreasing the delivered cost and increasing the availability of long-length, high-uniformity tape. Numerous roadmaps emphasize scaling output (frequently measured in km/year) and reducing cost per kiloampere-meter ($/kA·m), which broadens its applicability across magnets, motors, generators, and power devices.

High-value magnet markets constitute a significant opportunity as high-field MRI/NMR, compact fusion, and accelerator upgrades are challenging to replace and are incentivized by proven performance under high field and low temperature conditions. These sectors can justify premium pricing for sophisticated architectures, including graded conductors, HTS inserts, and enhanced joints and splices.

The standardization of formats and quality assurance documentation represents an additional strategic lever. As conductor formats, testing protocols, and qualification packages become increasingly interoperable, it becomes more feasible for Original Equipment Manufacturers (OEMs) to qualify multiple suppliers, enhancing supply resilience and expediting commercialization.

MARKET CHALLENGES

Demand Cyclicality and Manufacturing Yield Management Constrain Scalable Growth

A significant challenge lies in the cyclicality of demand driven by project-based procurement in fusion and accelerator programs. This phenomenon can pose utilization risks between successive project waves, especially for Nb₃Sn and HTS lines that demand substantial capital expenditure and specialized process control.

Manufacturing yield and consistency, particularly concerning HTS tapes, remain ongoing challenges. Even slight reductions in yield can substantially increase the effective cost per kiloampere-meter, thereby limiting supply and hindering adoption.

Scaling also requires the ecosystem to be maturely coordinated. The development of joint technology, cryogenic components, system integration capabilities, and installation and service readiness must progress concurrently with conductor output. When these related aspects fall behind, adoption may be hindered even if conductor prices decrease.

Segmentation Analysis

By Type

Proven Reliability and Cost-Effectiveness Led to NbTi (LTS) Segmental Dominance

Based on type, the market is segmented into NbTi (LTS), Nb3Sn (LTS), and HTS (REBCO/Bi/MgB2).

The NbTi (LTS) segment led the superconductors market share in 2025, driven primarily by MRI’s installed base and steady system demand. NbTi offers strong manufacturability, proven reliability, and cost-effectiveness for mainstream magnet fields.

HTS (REBCO/Bi/MgB2) segment is projected to experience the highest CAGR of 9.9% throughout the forecast period, as it is a premium conductor class with high cost per delivered current capability in many use cases. HTS demand is primarily driven by compact fusion concepts, high-field research magnets, and emerging power-grid demonstrations.

By Application

To know how our report can help streamline your business, Speak to Analyst

Power & Grid Segment to Dominate Owing to Need for High-Performance Insulation and Reliability Under Electrical Stress

By application, the market is segmented into MRI & medical imaging, fusion & particle accelerators, research magnets, power & grid, and others.

The power & grid segment is anticipated to experience the fastest growth rate, driven by applications such as HTS cables, fault current limiters, and pilot power devices, which are heavily reliant on High-Temperature Superconductors (HTS) and are frequently evaluated in terms of dollars per kiloampere-meter ($/kA·m). These applications necessitate high-performance insulation, thermal stability, and reliability under electrical stress. Consequently, a relatively modest conductor mass can result in significant material value critical to the system, particularly as grid congestion and high-capacity corridors increase interest in demonstration projects and early deployments.

The fusion & particle accelerators sector is experiencing significant growth. High-field requirements attract Nb₃Sn (for higher-field LTS magnets) and increasingly HTS inserts to enhance performance beyond practical LTS limits. Demand tends to come in program-scale procurement waves tied to multi-year build schedules. Consequently, even if volumes are lower than those for MRI in certain years, the higher-performance conductor mix disproportionately increases both the average price and the market value. Furthermore, this segment is projected to expand at a CAGR of 10.8% over the specified study period.

Superconductors Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

Asia Pacific

Asia Pacific Superconductors Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2024, valued at USD 0.53 billion, and also led in 2025, with USD 0.66 billion. Asia Pacific is the largest demand center in this estimate, supported by the scale of electronics manufacturing, high-field research activity, and increasing visibility of HTS manufacturing and deployment initiatives. China, Japan, and India contribute materially, with China showing the strongest growth tilt in fusion-adjacent and grid-facing HTS adoption.

China Superconductors Market

In 2026, the China market is estimated to reach USD 0.36 billion. The demand is primarily driven by medical imaging, including MRI installations and ongoing procurement efforts. This demand predominantly favors NbTi (LTS) volumes, owing to their maturity, established qualification history, and cost-effectiveness. Concurrently, China’s advanced high-field research infrastructure and fusion-related initiatives enhance the significance of Nb₃Sn and HTS technologies within the market, thereby contributing to value growth.

To know how our report can help streamline your business, Speak to Analyst

Japan Superconductors Market

Japan’s market is estimated to be around USD 0.13 billion in 2026, accounting for roughly 5.6% of the global revenues.

India Superconductors Market

India’s market is estimated at around USD 0.13 billion in 2026, accounting for roughly 5.6% of global revenues.

North America

The market in North America is estimated to reach USD 0.64 billion in 2026 and secure the position of the second-largest region in the market. North America is anchored by MRI demand, national labs and high-field research and development, and a strong emerging fusion ecosystem that can amplify HTS pull. The region benefits from deep technical infrastructure and early adoption in premium use cases, although qualification conservatism can extend adoption timelines.

U.S. Superconductors Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market can be estimated at around USD 0.61 billion in 2026, accounting for roughly 26.0% of global sales.

Europe

Europe is expected to grow significantly in the coming years. During the forecast period, the European region is projected to grow at 8.2% and reach a valuation of USD 0.65 billion in 2026. Europe is characterized by robust research infrastructure, accelerator ecosystems, and high engineering standards for magnet systems. Demand is supported by MRI and scientific programs, with increasing attention to energy efficiency and power conversion applications that could support HTS adoption through pilots.

U.K. Superconductors Market

The U.K. market is estimated at around USD 0.08 billion in 2026, accounting for roughly 3.5% of global revenues.

Germany Superconductors Market

Germany’s market is estimated at around USD 0.16 billion in 2026, accounting for roughly 6.8% of global revenues.

Latin America and Middle East & Africa

Over the forecast period, the Latin America and Middle East & Africa regions are anticipated to experience moderate growth within this market. The Latin America market is projected to reach USD 0.12 billion by 2026. Both Latin America and the Middle East & Africa continue to exhibit smaller current demand levels. Growth is primarily driven by the expansion of medical imaging technologies and targeted grid modernization and energy infrastructure projects. Demand in these regions tends to be more price-sensitive and significantly reliant on imported supplies and the preparedness of integrators.

GCC Superconductors Market

The GCC market is estimated to be around USD 0.07 billion in 2026, accounting for approximately 1.6% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Firms Gain Edge via Specialization and Long-Length Uniformity

The market is characterized by specialization and technological complexity. Competitive advantage is derived from manufacturing yield and defect control, particularly in HTS coated conductors, uniformity, and reliability over extended lengths, which are essential for MRI systems and high-field magnet applications. Support and thorough documentation for qualification processes are vital, along with capacity in program execution to ensure delivery reliability for large-scale magnet construction. Large suppliers often compete by offering comprehensive application engineering and fostering partnerships through qualification processes, whereas regional specialists tend to compete based on localized production capabilities and specialized performance grades. Bruker, Sumitomo Electric Industries, Ltd., SuperPower Inc., Fujikura Ltd., and THEVA Dünnschichttechnik GmbH are key players in the market.

LIST OF KEY SUPERCONDUCTORS COMPANIES PROFILED IN REPORT

- Bruker (Germany)

- Sumitomo Electric Industries, Ltd. (Japan)

- SuperPower Inc. (U.S.)

- Fujikura Ltd. (Japan)

- THEVA Dünnschichttechnik GmbH (Germany)

- SuNAM Co., Ltd. (South Korea)

- Shanghai Superconductor Technology Co., Ltd. (China)

- Western Superconducting Technologies Co., Ltd. (China)

- Kiswire Advanced Technology (South Korea)

- Supercon, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Bruker announced approximately USD 500 million in multi-year orders, including two expanded supply agreements, for the delivery of high-performance superconductors intended for next-generation MRI magnets.

- July 2025: During MT29, Shanghai Superconductor Technology announced the initiation of a new phase of production expansion for REBCO tape in response to increasing demand from compact fusion applications. The company also reported an annual supply of 2,000 km/12 mm at the end of 2023, with an expansion of approximately 4000 km/12 mm in 2025.

- January 2025: Western Superconducting Technologies had recently developed a high-Jc Nb₃Sn superconducting wire (RRP distributed-barrier layout) designed to meet the demands of high-field tokamak coils, demonstrating ongoing product development for next-generation fusion magnets.

REPORT COVERAGE

The global superconductors market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.5% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 1.94 billion in 2025 and is projected to reach USD 4.83 billion by 2034.

Recording a CAGR of 9.5%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The power & grid is the leading application segment in the market.

Asia Pacific held the highest market share in 2025.

Compact fusion concepts and hybrid high-field magnets are accelerating the demand for superconductors.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us