Surgical Drill Market Size, Share & Industry Analysis, By Product Type (Instruments {Electric Drills, Pneumatic Drills, and Battery Drills}, and Accessories); By Type (Reusable, and Disposable), By Application (Orthopedic, Dental, Neurology, ENT, and Others), By End User (Hospitals & ASCs, and Specialty Clinics), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

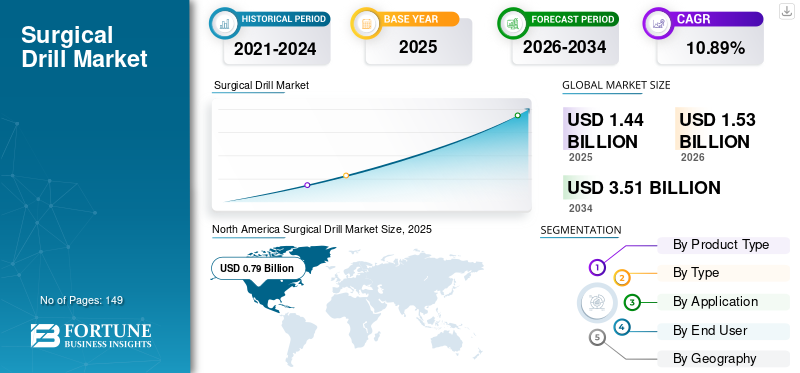

The global surgical drill market size was USD 1.44 billion in 2025 and is projected to grow from USD 1.53 billion in 2026 to USD 3.51 billion by 2034 at a CAGR of 10.89% during the 2026-2034 period. North America dominated the surgical drill market with a market share of 54.79% in 2025.

Surgical powered instruments play a unique role in the operating suite. A surgical drill is a powered instrument used to bore holes in the bone and to cater to a range of applications, from dental to neurological surgeries.

The growing prevalence of chronic disorders requiring surgical intervention coupled with the introduction of technologically advanced instruments by key players is contributing to the growth of the market during the forecast period.

- For instance, according to the study published by the Journal of Neurosurgery (JNS), every year, globally, an estimated 22.6 million patients suffer from neurological disorders or injuries, of whom 13.8 million require surgeries.

The COVID-19 pandemic negatively impacted the surgical drill market. In 2020, the governments of several countries laid instructions for the postponement or cancellation of non-essential surgeries to preserve the healthcare resources for the treatment of COVID-19 patients. This factor resulted in a huge decline in non-emergency procedures worldwide, which further limited the adoption of surgical drills. Disruptions in the supply chain, manufacturing delays, and logistical challenges affected the production and manufacturing of medical devices. However, in 2021, with the easing of the COVID-19 guidelines, the market started to come back to its pre-pandemic stage. With the increase in hospital visits and elective surgical procedures, the sales of surgical drills were improved. Furthermore, the market is stabilized with increasing revenue from the companies in the market, and thus, the market is expected to grow substantially during the forecast period.

Download Free sample to learn more about this report.

SURGICAL DRILL MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.44 billion

- 2026 Market Size: USD 1.53 billion

- 2034 Forecast Market Size: USD 3.51 billion

- CAGR: 10.89% from 2026–2034

- North America dominated the surgical drill market with a market share of 54.79% in 2025.

- The accessories segment is anticipated to account for 59.56% of the market share in 2026.

- The reusable segment is anticipated to account for 91.81% of the market share in 2026.

North America

North America represented USD 0.79 billion, accounting for 54.79% of the worldwide market, and is projected to grow to USD 0.84 billion in 2026.

Europe

. The Europe market generated USD 0.33 billion in 2025, representing 22.91% of the global market landscape, and is expected to reach USD 0.35 billion in 2026.

Asia Pacific

Asia Pacific contributed 15.81% to the global market in 2025, with a valuation of USD 0.23 billion, and is projected to reach USD 0.24 billion in 2026.

U.S.

The U.S. market is projected to reach USD 0.79 billion by 2026.

Japan

The Japan market is projected to reach USD 0.06 billion by 2026.

Read More

Surgical Drill Market Trends

Introduction of Next Generation Drills to Spur Growth of Market

A large number of patients in developed and emerging countries are undergoing surgeries every year. Despite various advancements in surgical devices, drills have their distinct shortcomings. Pricing and shorter-battery life drills, etc., are presenting a huge opportunity for market players to focus on R&D and introduce advanced, next-generation devices in the market.

Various research institutes are already focusing on developing next-generation power tools, including drills such as high-speed drills with robotic systems, non-sterile battery drills, advanced architecture drills, etc.

- For instance, in March 2023, Stryker launched an innovative and patented technology called the CD NXT System for power tools. This technology is empowering surgeons with its rapid, accurate, and consistent digital depth measurement for various surgical procedures.

Additionally, different market players including adeor medical AG and others are focusing on introducing these next-generation drills in the emerging market, which is anticipated to boost the overall market growth in the forthcoming years.

Download Free sample to learn more about this report.

Surgical Drill Market Growth Factors

Growing Number of Surgeries to Augment Demand of Surgical Drill

Globally, the growing number of surgeries owing to the rising prevalence of chronic disorders and increasing road accidents, sports injuries, and trauma is one of the major factors contributing towards the growth of the market.

- According to the data published by the World Health Organization (WHO), in 2019, the estimated mean global surgical rate ranged from 666 to 11,168 surgeries per 100,000 people, with road accidents and trauma being one of the major causes for surgical intervention.

Also, the rapidly increasing geriatric population leads to the rising number of patients with orthopedic disorders, leading toa rise in the number of surgeries such as joint replacement, arthroscopy, organ transplant among elderly patients. This factor drives the demand for new and innovative surgical powered instruments, including surgical drills, in hospitals and other healthcare facilities.

- According to the data published by the American College of Rheumatology in 2023, approximately 790,000 total knee replacement and 450,000 hip replacement surgeries are performed in the U.S. every year. The growing aging population in the U.S. has led to an increase in orthopedic surgical procedures.

The growing demand for surgical powered instruments, including drills, is therefore propelling the market players to invest heavily in R&D and launch of technologically advanced products. . Further, the growing number of technological advancements in the drills for surgeries, is anticipated to spur the surgical drill market growth during the forecast period.

RESTRAINING FACTORS

Inadequate Quality Assurance and Lack of Sterilization Practices May Hamper Market Growth

Surgeons require high-quality surgical instruments to carry out successful procedures. The quality of surgical instruments is heavily relied upon by surgeons to perform procedures to the highest standard. However, the surgeons usually directly use the newly purchased surgical power tools, without undergoing sterilization procedures which results in harmful consequences.

- For instance, according to a research study conducted by National Patient Safety Agency (NPSA) in the U.S., the surgical drills constituted the largest (40%) group of broken and poor quality instruments.

Moreover, failure to properly disinfect or sterilize drills results in transmission of infectious pathogens to the patients. For instance, according to a survey conducted among the dental surgeons in the U.K., 68% of respondents believed they were sterilizing their instruments but did not use appropriate chemical sterilants or exposure times, and 49% of respondents did not challenge autoclaves with biological indicators.

In addition, emergence of advanced minimally invasive surgeries for spine and bone grafting along with comparatively higher cost of powered instruments and lack of reimbursement policies in emerging countries is limiting the adoption of surgical drills and are expected to further hamper the global surgical drill market growth during the forecast period.

- For instance, in October 2023, according to the data published by IRCAD Africa, an estimated 2.0 billion people in Africa were not able to access basic surgeries in the region. Thus, to fulfil the demand for minimally invasive surgeries among the patients of Africa, IRCAD started a research and training center for minimally invasive surgery.

Surgical Drill Market Segmentation Analysis

By Product Type Analysis

Growing Demand of Accessories in Different Surgeries to Lead to Dominant Position in 2023

Based on product type, the global market is segmented into instruments and accessories

The accessories segment is anticipated to account for 59.56% of the market share in 2026. A rising number of surgical interventions, especially orthopedic procedures globally, is leading to rising demand for accessories and consumables such as batteries, electric consoles, pneumatic regulators, and others used for drills.

- For instance, according to a research article published by OrthoSpineNews., approximately 40% of the global population over age 55 suffers from chronic knee pain. Of those, 50.8 million suffer from disabling pain, and about 2.6 million turn to knee replacement surgery each year

On the other hand, the longer shelf life of the instruments and high costs of the these devices limits the frequent buying of new instruments. This factor is primarily responsible for the lower share of the instruments segment during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Type Analysis

Cost Effective Pricing to Hold the Lion’s Share of Reusable Segment in Global Market

Based on type, the global market is segmented into reusable and disposable.

The reusable segment is anticipated to account for 91.81% of the market share in 2026. The dominance of this segment is attributed to the higher preference of surgeons towards reusable instruments owing to their cost advantage, technical superiorities over the disposable surgical drills, and other functional and operational benefits offered by these devices.

On the other hand, the higher purchase price associated with the disposable surgical drills limits their adoption. It is a less popular choice among the surgeons and, therefore has a low growth rate during the forecast period. However, growing concerns about the sterilization of reusable devices and lack of established guidelines and protocols for sterilization in healthcare facilities especially in emerging countries, are shifting the focus towards disposable devices.

By Application Analysis

Growing Number of Orthopedic Surgeries Enabled the Dominance of Segment

Based on indication, the global market is segmented into orthopedic, dental, neurology, ENT, and others.

The orthopedic segment dominated the global surgical drill market with a market share of 61.40% in 2026. The dominance is attributed to the increasing incidence of orthopedic disorders among the global population, resulting in more patients undergoing surgical interventions. For instance, according to the data published by ResearchGate, it was estimated that the global incidence rate of knee arthritis was 203 per 10,000 individuals, and the number of total knee arthroplasty was projected to grow by 85.0% and reach 1.26 million procedures by the end of 2030.

On the other hand, the neurology segment held the second-largest share in the global market in 2023. The segment's growth is lucrative owing to the increasing patient pool suffering from neurological disorders leading to higher demand for surgical procedures as a treatment. Hence, subsequently increasing the demand and uptake of surgical power tools, including drills.

- For instance, according to the data published by the American Society of Clinical Oncology (ASCO), 24,810 adults in the U.S. were diagnosed with brain or spinal cord tumors in 2023, and surgery of the brain is one of the prominent treatment options for the cure of brain tumors. Such rising cases of neurological diseases lead to the increasing adoption of surgical drills in the market.

By End User Analysis

Presence of Insurance Coverage for Surgeries in Hospitals & ASCs Resulted in Highest Market Share of Segment

Based on indication, the global market is segmented into hospitals & ASCs and specialty clinics

The hospitals & ASCs segment held a market value of 1.08 in 2026. The dominance of the segment is attributed to the higher number of surgeries performed in hospitals and ambulatory surgery centers, along with adequate reimbursement policies awarded by hospitals in emerging countries.

Moreover, the presence of skilled healthcare professionals and higher adoption of advanced drills for complicated surgical interventions are some of the major factors driving the patient flow towards these settings in developed and emerging countries.

On the other hand, the specialty clinics segment is growing at a CAGR higher than the hospitals & ASCs segment. An increasing number of specialty clinics, including orthopedic clinics in developed countries, and increasing investments by public and private players to develop healthcare infrastructure and facilities in emerging countries is anticpated to drive the segment's growth.

REGIONAL INSIGHTS

North America Surgical Drill Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America to Hold Largest Market due to Increasing Prevalence of Neurological Disorders

North America

The U.S. market is projected to reach USD 0.79 billion by 2026. The surgical drill market size in North America stood at USD 0.71 billion in 2023. The rising prevalence of neurological disorders, orthopedic disorders, and other chronic conditions, and higher percentage of surgeries is driving the demand for instruments and accessories for surgical power tools. In 2025, North America represented USD 0.79 billion, accounting for 54.79% of the worldwide market, and is projected to grow to USD 0.84 billion in 2026.

Europe

The U.K. market is projected to reach USD 0.05 billion by 2026, while the Germany market is projected to reach USD 0.09 billion by 2026. Europe held the second-largest share in the global market. An increasing number of orthopedic surgeries in countries such as the U.K., Germany, and others and the introduction of advanced drills in the region, are some of the factors driving the growth of this region during the forecast period. The Europe market generated USD 0.33 billion in 2025, representing 22.91% of the global market landscape, and is expected to reach USD 0.35 billion in 2026.

- For instance, according to the data published by the National Joint Registry, it is estimated that around 160,000 total hip and knee replacement procedures are performed in the England and Wales region every year.

Asia Pacific

The Japan market is projected to reach USD 0.06 billion by 2026, the China market is projected to reach USD 0.06 billion by 2026, and the India market is projected to reach USD 0.03 billion by 2026. Meanwhile, the market in Asia Pacific is expected to grow with the highest CAGR. Increasing penetration of market players in developing countries, high volume of surgeries and rise in medical tourism are some of the major factors responsible for the rapid growth of this region. Asia Pacific contributed 15.81% to the global market in 2025, with a valuation of USD 0.23 billion, and is projected to reach USD 0.24 billion in 2026.

Middle East & Africa

The Middle East & Africa market was valued at USD 0.03 billion in 2025, capturing 2.19% of global revenue, and is estimated to reach USD 0.03 billion in 2026.

Latin America

The market in Latin America reached USD 0.06 billion in 2025, representing 4.30% of total market revenue, and is projected to reach USD 0.07 billion in 2026.

List of Key Companies in Surgical Drill Market

Stryker and DePuy Synthes (Johnson & Johnson Services, Inc.) to Acquire Leading Positions in Market

The global market is a consolidated market with players like Stryker, Johnson & Johnson Services, Inc., Zimmer Biomet, Medtronic, and B. Braun Melsungen AG comprising a dominant market share. These major players are constantly focusing on commercializing their products worldwide, launching new battery-powered drills for surgical procedures, and entering into a strategic partnership with other players to expand their product portfolio.

Also, the current market scenario is characterized by an increasing proportion of small manufacturers in emerging and developed countries like De Soutter Medical, AlloTech Co., LTD., NSK/NAKANISHI INC., and others Increasing focus on the development of new products shall enable the players to boost their market share. For instance, in March 2019, NSK launched the S-Max M series, the next phase of the evolution of their globally acclaimed handpieces.

LIST OF KEY COMPANIES PROFILED:

- Medtronic (Ireland)

- Stryker (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- NSK/NAKANISHI INC. (Japan)

- Zimmer Biomet (U.S.)

- B. Braun Melsungen AG (Germany)

- De Soutter Medical (U.K.)

- AlloTech Co., LTD. (South Korea)

KEY INDUSTRY DEVELOPMENTS:

- November 2021- Medical Device Business Services, Inc. (Johnson & Johnson Medtech) launched the UNIUM System to strengthen its power tools portfolio. It is a reliable and efficient system used in trauma settings for small bones, spine, and thorax procedures.

- October 2021- Medtronic introduced the Mazor X System for robotic-guided spine surgery. This platform provides a comprehensive solution for surgical planning, workflow, execution, and confirmation, making it the inaugural robotic-assisted spine surgery platform to be launched in Canada.

- January 2021 –Medtronic received the FDA clearance for its Midas Rex high-speed drills, navigated interbody and disc prep platform using the Mazor robotic guidance system.

- June 2021 - Jiomax, a German-based market leader in technologies and training methods for full-endoscopic and minimally invasive spinal surgery, announced the global launch of its new generation Shrill, the Shaver Drill System.

- July 2020- Smith+Nephew launched the CORI Surgical System, a handheld robotics platform, and the Real Intelligence technology solutions for knee arthroplasty and total knee arthroplasty.

REPORT COVERAGE

An Infographic Representation of Surgical Drill Market

View Full Infographic

View Full InfographicTo get information on various segments, share your queries with us

The global surgical drill market research report provides a detailed analysis of the market. It focuses on key aspects such as leading companies, product type, application, and end-user. Besides this, it offers insights into the key market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

|

|

Base Year |

|

|

Estimated Year |

|

|

Forecast Period |

|

|

Historical Period |

|

|

Growth Rate |

CAGR of 10.89% from 2026 to 2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Product Type

|

|

By Type

|

|

|

By Application

|

|

|

By End User

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 1.44 billion in 2025 and is projected to reach USD 3.51 billion by 2034.

In 2025, the market size in North America was USD 0.79 billion.

The market will exhibit steady growth at a CAGR of 10.89% during the forecast period (2026-2034).

By type, the reusable segment is the leading segment.

The increasing prevalence of chronic disorders requiring surgical intervention and the growing adoption of technologically advanced drills are the key drivers of the market.

Stryker, DePuy Synthes, and Zimmer Biomet are the top players in the market.

- 2021-2034

- 2025

- 2021-2024

- 149

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us