Surgical Retractors Market Size, Share & Industry Analysis, By Type (Handheld and Self-retaining), By Usage (Reusable and Single Use), By Application (General Surgery, Abdominal Surgery, Orthopedic Surgery, Cardiothoracic Surgery, and Others), By End User (Hospitals & ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

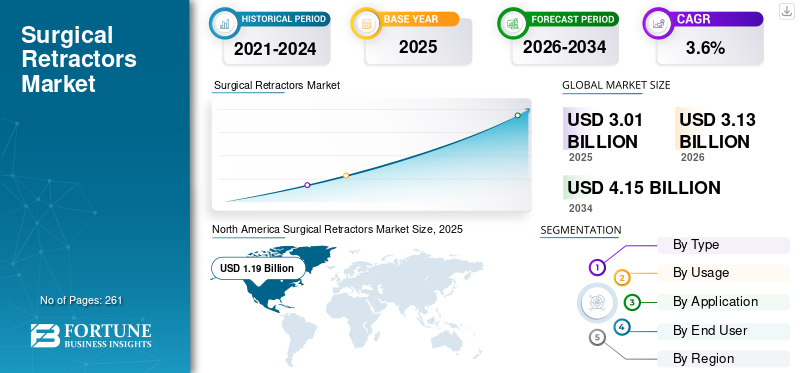

The global surgical retractors market size was valued at USD 3.01 billion in 2025 and is projected to grow from USD 3.13 billion in 2026 to USD 4.15 billion by 2034, exhibiting a CAGR of 3.6% during the forecast period. North America dominated the global surgical retractors market with a market share of 39.53% in 2025.

Surgical retractors are medical devices used to hold back organs, tissues, or incision edges during surgical procedures to provide surgeons with visibility and access to the surgical site, which improves precision and minimizes trauma among patients. The increasing prevalence of chronic conditions, rising surgical procedure volumes, and the expansion of healthcare infrastructure are resulting in an increasing adoption rate of these products in the market. The increasing geriatric population is further increasing the demand for surgical procedures among patients, thereby boosting the adoption rate of surgical retractors in the market.

- For instance, according to the 2020 data published by the National Center for Biotechnology Information (NCBI), about 310 million major surgical procedures are performed every year worldwide.

Furthermore, the rising integration of technological advancements in these products among the major players, such as Medtronic, Johnson & Johnson Services, Inc., among others, is further contributing to the demand for these devices in the market.

Download Free sample to learn more about this report.

SURGICAL RETRACTORS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 3.01 billion

- 2026 Market Size: USD 3.13 billion

- 2034 Forecast Market Size: USD 4.15 billion

- CAGR: 3.60% from 2026–2034

- North America dominated the global surgical retractors market with a market share of 39.53% in 2025.

- The self-retaining segment is expected to grow at a CAGR of 3.8% over the forecast period.

- By application, the general surgery segment held the share of 31.7% in 2025.

North America

The North America market held the dominant share in 2024, valued at USD 1.15 billion, and also took the leading share in 2025 with USD 1.19 billion.

Europe

Europe is projected to record a growth rate of 2.9% in the coming years, which is the second highest among all regions, and reach a valuation of USD 1.00 billion by 2026.

Asia Pacific

Asia Pacific is estimated to reach USD 0.65 billion in 2026 and secure the position of the third-largest region in the market.

U.S.

The U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.18 billion in 2026, accounting for roughly 37.6% of global surgical retractors sales.

Japan

The Japan surgical retractors market in 2026 is estimated at around USD 0.14 billion, accounting for roughly 4.5% of global revenues.

Read More

Surgical Retractors Market Trends

Integration of Technological Advancements in these Surgical Retractors to Fuel the Demand

There is an increasing focus on the integration of technological advancements in these surgical retractors, which improves the surgical efficiency and patient safety. The prominent companies are focusing on technologically advanced self-retaining devices that enhance the precision and intraoperative visibility.

Additionally, the adoption of advanced materials, including coated stainless steel, high-performance polymers, illumination systems, and others, has further enhanced the efficiency of surgical procedures. There is ongoing research for new designs for robotic-assisted and minimally invasive procedures, which reflects the wider adoption of these products in healthcare settings.

- In April 2023, Orthofix Medical Inc., a global spine and orthopedic company, launched two access retractor systems: The Lattus Lateral Access System and the Fathom Pedicle-Based Retractor System, to aid surgeons during minimally invasive spine (MIS) procedures.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Growing Volume of Surgical Procedures Among the Patient Population to Fuel Market Growth

The increasing prevalence of chronic conditions, such as cardiovascular disorders and urological disorders, is leading to a rise in surgical procedures among the patient population, thereby driving the demand for surgical retractors to hold tissue and organs in place, and enhancing visibility in the market.

- For instance, according to 2024 data published by the Center for Disease Control & Prevention (CDC), it was reported that about 1 in 20 adults has coronary artery disease in the U.S.

This, along with a shift towards procedures in outpatient settings and expansion of ambulatory surgical centers, is further augmenting the adoption rate of these products in the market. Therefore, the factors above, along with the rising focus of prominent players on introducing R&D activities to launch novel products, are expected to boost the adoption rate of these products, thereby supporting the global surgical retractors market size.

Market Restraints

Surgical Site Infections Risk Associated with Reusable Retractors to Hamper the Market Growth

There is an increasing demand for innovative surgical procedures. However, the risk of surgical site infections associated with reusable retractors hampers the adoption rate for these products, particularly in emerging countries, including India, Mexico, and others.

Additionally, reusable retractors require thorough reprocessing between surgeries, and any lapses in reprocessing methods can result in microbial contamination. The complex designs with grooves, joints, or modular components also increase the chances of incomplete sterilization, further raising concerns among clinical providers and infection control organizations globally.

- For instance, according to the 2024 statistics published by the Centers for Disease Control & Prevention (CDC), about one in 31 hospital patients has at least one healthcare-associated infection on any given day.

Market Opportunities

Growth of Ambulatory Surgical Centers (ASCs)

There is a rapid expansion of healthcare systems in emerging countries, including Brazil, Mexico, and others. The growing surgical volumes, expansion of hospital infrastructure, growing number of ambulatory surgical centers are consequently increasing the adoption of surgical retractors in the healthcare settings. The preference for ambulatory surgical centers has increased for elective and minimally invasive surgical procedures owing to their benefits, such as shorter patient stays, lower procedural costs, faster turnover times, and reduced risk of hospital-acquired infections.

- According to 2025 data published by Definitive Healthcare, there are about 10,000 active ambulatory surgical centers in the U.S.

Market Challenges

Limited Healthcare Access in Emerging Countries to Hinder the Market Growth

There is an increasing demand for robot-assisted and minimally invasive surgeries among the patient population. However, shortage of technologically advanced devices, limited healthcare spending, along with insufficient reimbursement policies, particularly in developing nations, are resulting in limited access to clinical facilities among the patient population.

Moreover, a limited number of healthcare facilities and limited specialist surgeons, among others, are some of the vital factors, resulting in the delayed surgical procedures among the patient population, especially in emerging nations, such as India, Brazil, among others.

- For instance, according to 2023 statistics published by The World Bank Group (WBG), about 4.5 billion people lack full access to essential health services globally.

Other Prominent Challenges

- High capital and instrument reprocessing costs will hamper the market growth

SEGMENTATION ANALYSIS

By Type

Increasing Number of Surgical Procedures Led to the Handheld Segment Dominance

Based on the type, the market is classified into handheld and self-retaining.

To know how our report can help streamline your business, Speak to Analyst

The handheld segment held the largest revenue share in 2025. The growth is due to the increasing prevalence of chronic disorders among patients, resulting in a rising number of surgical procedures worldwide. This, coupled with the growing focus of key players on launching novel products, is further expected to contribute to the global surgical retractors market growth.

- For instance, according to 2024 statistics published by Science Direct, more than 1 million cardiac surgical procedures are estimated to occur yearly worldwide.

The self-retaining segment is expected to grow at a CAGR of 3.8% over the forecast period.

By Usage

Increasing Prevalence of Hospital-Acquired Infections Led to the Dominance of the Single Use Segment

Based on usage, the market is bifurcated into reusable and single-use.

The single-use segment dominated the global market in 2025. By usage, the single-use segment held the share of 93.6% in 2025. The growth is due to the increasing prevalence of hospital-acquired infections, resulting in a growing demand for single-use products, thereby supporting the adoption rate of these devices in the market.

- For instance, in September 2024, Spartan Medical expanded its single-use, sterile portfolio of surgical procedure kits, including surgical retractors, to address orthopedic and trauma procedures in the U.S.

The segment of reusable is set to flourish with a growth rate of 2.4% across the forecast period.

By Application

Growing Number of General Surgery Procedures has led to the Dominance of the Segment

Based on application, the market is segmented into general surgery, abdominal surgery, orthopedic surgery, cardiothoracic surgery, and others.

The general surgery segment dominated the global market in 2025. By application, the general surgery segment held the share of 31.7% in 2025. The growth is due to the growing prevalence of chronic disorders such as cardiovascular diseases and urological diseases, among others, resulting in an increasing number of surgical procedures worldwide, thereby contributing to the adoption rate of these devices in the market.

- For instance, according to the 2020 statistics published by the National Center for Biotechnology Information, it was reported that approximately 18.3% procedures were for general surgery in 9,284 surgical procedures performed in 88,273 people in India.

The segment of abdominal surgery is set to flourish with a growth rate of 4.3% across the forecast period.

By End-user

Increasing Number of Hospitals & ASCs Led to the Segmental Dominance

Based on end user, the market is divided into hospitals & ASCs, specialty clinics, and others.

The hospitals & ASCs segment dominated the market in 2025. The increasing prevalence of chronic conditions, rising number of surgical procedures in hospitals, growing number of hospitals, among others, are some of the crucial factors supporting the growth of the segment in the market. Furthermore, the segment is set to hold an 81.5% share in 2026.

- For instance, according to 2025 statistics published by Statistisches Bundesamt, it was reported that there are about 1,874 hospitals in Germany.

In addition, specialty clinics’ end users are projected to grow at a 4.4% CAGR during the forecast period.

Surgical Retractors Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Surgical Retractors Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valued at USD 1.15 billion, and also took the leading share in 2025 with USD 1.19 billion. The growing prevalence of chronic conditions, high surgical volumes, advanced hospital infrastructure, and strong replacement demand for premium retractors, among others, are some of the factors supporting the growth of the segment in the market.

- For instance, according to 2024 statistics published by the Center for Disease Control & Prevention (CDC), the prevalence of inflammatory bowel disease (IBD) is estimated between 2.4 and 3.1 million among patients in the U.S.

U.S. Surgical Retractors Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.18 billion in 2026, accounting for roughly 37.6% of global surgical retractors sales.

Europe

Europe is projected to record a growth rate of 2.9% in the coming years, which is the second highest among all regions, and reach a valuation of USD 1.00 billion by 2026. The mature surgical markets, with an emphasis on ergonomics, surgeon safety, and reusable device standards, are likely to support market growth.

U.K Surgical Retractors Market

The U.K. surgical retractors market in 2026 is estimated to be around USD 0.16 billion, representing roughly 5.2% of the global surgical retractors market revenues.

Germany Surgical Retractors Market

Germany’s surgical retractors market is projected to reach approximately USD 0.23 billion in 2026, equivalent to around 7.3% of global surgical retractors sales.

Asia Pacific

Asia Pacific is estimated to reach USD 0.65 billion in 2026 and secure the position of the third-largest region in the market. The fastest growth in surgical procedures, driven by population size, expanding hospital capacity, and increased healthcare access, is likely to support the growth of the market. In the region, India and China are both estimated to reach USD 0.11 billion and USD 0.17 billion, respectively, in 2026.

Japan Surgical Retractors Market

The Japan surgical retractors market in 2026 is estimated at around USD 0.14 billion, accounting for roughly 4.5% of global revenues. Japan has historically reported a relatively high prevalence of chronic diseases, with a large number of surgical volumes.

China Surgical Retractors Market

China’s surgical retractors market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.17 billion, representing roughly 5.4% of global sales.

India Surgical Retractors Market

The India surgical retractors market size in 2026 is estimated at around USD 0.11 billion, accounting for roughly 3.6% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.14 billion in 2026. The growth is due to the gradual growth tied to public healthcare investment and medical tourism hubs in these regions. In the Middle East & Africa, the GCC is set to reach a value of USD 0.04 billion in 2026.

South Africa Surgical Retractors Market

The South Africa surgical retractors market is projected to reach around USD 0.03 billion in 2026, representing roughly 0.8% of global revenues.

Competitive Landscape

Key Industry Players

Increasing Number of Reprocessed Medical Devices to Support Their Dominance

A significant product portfolio, coupled with a strong focus on inorganic growth strategies worldwide, is one of the prominent factors supporting the dominance of these players in the market. Medtronic and Johnson & Johnson Services, Inc., are major companies in the market in 2025. Moreover, the growing focus of key companies on the expansion of robotics hubs for surgical procedures is likely to strengthen their presence and support the global surgical retractors market share.

- For instance, in September 2025, Medtronic expanded an artificial intelligence robotics hub for bladder lesion removal surgery in the U.K.

Other key players, including BD and others, are also growing in the market, primarily due to their increasing focus on acquisitions and collaborations among other players to strengthen their presence in the market.

List of Key Surgical Retractors Companies Profiled

- Medtronic (U.S.)

- BD (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Stryker (U.S.)

- CooperSurgical, Inc. (U.S.)

- Teleflex Incorporated (U.S.)

- Braun SE (Germany)

- Integra LifeSciences Corporation (U.S.)

- Medline Industries L.P. (U.S)

- Globus Medical (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2025 – June Medical collaborated with Aspen Surgical to distribute the Galaxy II retractor system across the U.S. market.

- September 2024 – The TITAN CSR surgical retractor was honored with the prestigious Best Equipment Award at the 2024 American Association for the Surgery of Trauma (AAST) Annual Meeting and Clinical Congress of Acute Care Surgery. This helped the company in strengthening its presence.

- September 2023 – Livac USA, Inc. launched its LiVac Retractor in the U.S. for use as a solid organ retractor. This helped the company in strengthening its product portfolio.

- October 2022 – Livac USA, Inc. has been awarded a national group purchasing agreement for a New Technology Breakthrough with Premier, Inc. for the LiVac Retractor System.

- June 2019 – obp launches cordless surgical retractor with multi-LED light source, ONETRAC LX, with an aim to strengthen its product portfolio.

REPORT COVERAGE

The global surgical retractors market report provides a detailed analysis and focuses on key aspects such as leading companies and market segmentation, including type, usage, application, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.6% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, Usage, Application, End User, and Region |

|

By Type |

· Handheld · Self-retaining |

|

By Usage |

· Reusable · Single Use |

|

By Application |

· General Surgery · Abdominal Surgery · Orthopedic Surgery · Cardiothoracic Surgery · Others |

|

By End User |

· Hospitals & ASCs · Specialty Clinics · Others |

|

By Region |

· North America (By Type, By Usage, By Application, By End User, and by Country) o U.S. (By Type) o Canada (By Type) · Europe (By Type, By Usage, By Application, By End User, and by Country/Sub-region) o U.K. (By Type) o Germany (By Type) o France (By Type) o Italy (By Type) o Spain (By Type) o Scandinavia (By Type) o Rest of Europe (By Type) · Asia Pacific (By Type, By Usage, By Application, By End User, and by Country/Sub-region) o China (By Type) o Japan (By Type) o India (By Type) o Australia (By Type) o Southeast Asia (By Type) o Rest of Asia Pacific (By Type) · Latin America (By Type, By Usage, By Application, By End User, and by Country/Sub-region) o Brazil (By Type) o Mexico (By Type) o Rest of Latin America (By Type) · Middle East & Africa (By Type, By Usage, By Application, By End User, and by Country/Sub-region) o GCC (By Type) o South Africa (By Type) o Rest of the Middle East & Africa (By Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 3.01 billion in 2025 and is projected to reach USD 4.15 billion by 2034.

In 2025, the North America regional market value stood at USD 1.19 billion.

Growing at a CAGR of 3.6%, the market will exhibit steady growth over the forecast period (2026-2034).

By type, the handheld segment is the leading segment in this market.

The introduction of novel surgical retractors is one of the major factors driving the market's growth.

Medtonic and Johnson & Johnson Services, Inc., are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of chronic conditions, the increasing number of surgical procedures, among others, are some of the vital factors expected to boost the adoption of these products worldwide.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us