Talc Market Size, Share & Industry Analysis, By Deposit Type (Talc-Carbonate, Talc-Serpentine, Talc-Chlorite, and Others), By End Use (Plastics, Ceramics, Paints & Coatings, Pulp & Paper, Rubber, Personal Care & Cosmetics, and Others), and Regional Forecast, 2026-2034

Talc Market Size and Future Outlook

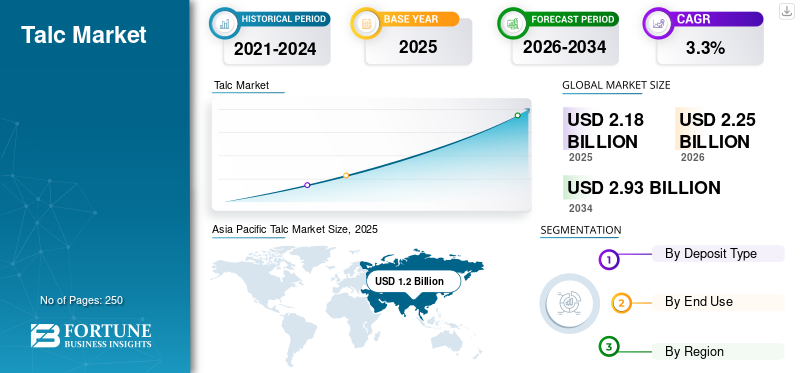

The global talc market size was valued at USD 2.18 billion in 2025. The market is projected to grow from USD 2.25 billion in 2026 to USD 2.93 billion by 2034, exhibiting a CAGR of 3.3% during the forecast period. Asia Pacific dominated the global talc market with a market share of 55.04% in 2025.

Talc refers to a versatile industrial mineral composed primarily of hydrated magnesium silicate, valued for its softness, lamellar structure, chemical inertness, hydrophobicity, and excellent barrier and reinforcement properties. As the world’s softest mineral, it is widely used across plastics, ceramics, paints & coatings, pulp & paper, rubber, personal care, and several niche industrial applications. In plastics, it improves stiffness, dimensional stability, heat resistance, and recyclability, making it essential for polypropylene (PP) compounds used in automotive components, appliances, and packaging. Its role in coatings includes improving matting, opacity, rheology, and anticorrosion performance, while in paper, it aids pitch control and surface smoothness. High-purity grades are further used in cosmetics and pharmaceuticals due to their superior whiteness and strict regulatory compliance. The rising demand for lightweight plastics, expanding ceramics production in Asia, and sustained use in coatings and industrial fillers are expected to drive product demand.

Furthermore, the global talc industry is shaped by several leading producers, including Imerys, Golcha Group, IMI Fabi, Mondo Minerals, Nippon Talc, and Liaoning Aihai. Their portfolios encompass carbonate, serpentine, and chlorite talc deposits, which are processed into various grades tailored for different industrial and specialty applications. Continuous investments in mineral beneficiation, ultra-fine milling technologies, asbestos-free certification, and high-purity cosmetic-grade production help reinforce their competitive positioning.

Download Free sample to learn more about this report.

TALC MARKET KEY TAKEAWAYS

Market Size & Forecast

Market Size & Forecast

- 2025 Market Size: USD 2.18 Billion

- 2026 Market Size: USD 2.25 Billion

- 2034 Forecast Market Size: USD 2.93 Billion

- CAGR: 3.3% from 2026–2034

Market Share

Market Share

- Asia Pacific dominated the global talc market with a market share of 55.04% in 2025.

- Plastics emerged as the leading end-use segment, driven by growing demand for lightweight composites.

- Ceramics represented another major application area, supported by increasing demand for tiles.

Key Regional Highlights

Key Regional Highlights

North America

North America represented a mature market, supported by demand from plastics, coatings, personal care products, and automotive lightweighting applications.

Europe

Europe maintained a significant market position, driven by advanced manufacturing capabilities, strict quality standards, sustainable sourcing initiatives, and strong demand for premium talc grades.

Asia Pacific

Asia Pacific held the largest market share in 2025, valued at USD 1.21 billion, and is expected to lead in 2026.

India

The market continues to witness strong growth due to expanding plastics processing, ceramics production, infrastructure development, and increasing investments in advanced mineral processing technologies.

China

The market reached USD 0.74 billion in 2025, driven by its position as the world's largest producer and consumer of talc, supported by extensive industrial and manufacturing activities.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Increasing Demand for Plastics Reinforcements and Lightweight Composites Drive Market Growth

The global shift toward lightweight materials, driven by automotive efficiency targets, sustainability mandates, and the growing use of plastics in consumer and industrial applications, is significantly boosting the product demand as a reinforcement mineral. Mineral’s lamellar structure enhances stiffness, dimensional stability, thermal resistance, and impact strength in polypropylene (PP) and other engineering plastics, making it a critical additive across several applications. As OEMs and Tier-1 suppliers continue to substitute metals with polymer composites, talc-filled PP compounds are becoming increasingly essential due to their cost-effectiveness and superior mechanical performance. Additionally, it is gaining traction in recycled plastics, where it restores the mechanical properties lost during repeated processing cycles, supporting circular economy goals. Growth in packaging, electrical components, and lightweight consumer goods is set to drive the global talc market growth in the foreseeable period.

MARKET RESTRAINTS:

Substitution Risk from Calcium Carbonate, Kaolin, and Other Industrial Minerals May Restrain Market Growth

Although talc offers unique benefits across various industrial applications, the market faces notable substitution risks from alternative minerals, including calcium carbonate, kaolin, mica, and barite. These substitutes are often more cost-competitive, especially in low- to mid-performance applications, and can partially replicate their functional properties such as reinforcement, matting, and rheological control. In paints and coatings, kaolin and calcium carbonate are frequently used as extenders due to their lower price points and strong availability in major manufacturing regions. The pulp and paper industry, a historically significant consumer, is increasingly shifting toward alternative fillers as digitalization reduces paper demand and producers seek lower-cost formulations. In plastics, calcium carbonate continues to penetrate cost-sensitive packaging and commodity applications. Furthermore, evolving environmental regulations, concerns about impurities at the mine level, and scrutiny over cosmetic-grade talc may accelerate the adoption of substitutes. These factors collectively act as a restraint on product demand, particularly in developed markets where industrial users prioritize cost optimization.

MARKET OPPORTUNITIES:

Increasing Demand for Advanced Grades in Engineering Plastics and other Applications Offer Growth Prospects

Advanced grades characterized by ultra-fine particle sizes, high purity, controlled morphology, and engineered surface treatments are opening new growth avenues across engineering plastics, coatings, pharmaceuticals, and high-performance ceramics. In automotive lightweighting, advanced talc-filled PP compounds help manufacturers achieve superior stiffness-to-weight ratios, dimensional stability, and heat resistance, enabling the replacement of metal components and supporting EV platform development. Surface-modified talc enhances compatibility with polymer matrices, allowing for improved impact resistance and dispersion in advanced polyolefins and engineering resins. Beyond plastics, high-purity grades are gaining adoption in premium cosmetics, food and pharma excipients, and specialty ceramics where strict regulatory, aesthetic, and functional requirements apply. The rise of recycled plastics is also creating opportunities for high-performance mineral formulations that restore material integrity in reprocessed PP and PE streams. With global manufacturers focusing on product differentiation, compliance, and performance-driven formulations, the demand for advanced grades is poised to create lucrative opportunities for producers.

TALC MARKET TRENDS:

Growing Emphasis on Sustainable and Traceable Mineral Sourcing Shape Market Dynamics

Sustainability and supply chain transparency are becoming central themes across the global industrial minerals market, and talc is no exception. Manufacturers, particularly in the cosmetics, pharmaceuticals, food-contact applications, and premium polymer compounds sectors, are increasingly demanding fully traceable, responsibly mined, and asbestos-free products. Stricter regulatory frameworks in the U.S., Europe, and Japan, along with growing consumer scrutiny, are pushing producers to adopt robust ESG practices. Practices such as responsible mining certifications, minimizing environmental impact, community engagement, and transparent geological verification are poised to become new norms in the industry.

Additionally, large downstream users are incorporating sustainability criteria into supplier selection, preferring partners that provide life-cycle assessments, carbon footprint reporting, and clean processing technologies. As producers invest in dust-free operations, water recycling, energy-efficient grinding, and safe tailings management, sustainability becomes both a compliance requirement and a competitive differentiator. Sustainability, therefore, is poised to become a defining factor shaping the long-term dynamics of the global market.

Download Free sample to learn more about this report.

Segmentation Analysis

By Deposit Type

Talc-carbonate Dominates With its Superior Properties Due to its Use in Numerous Applications

Based on deposit type, the market is classified into talc-carbonate, talc-serpentine, talc-chlorite, and others.

The talc-carbonate deposit type dominated the global talc market share in 2025 due to its high purity, brightness, and superior lamellar structure, making it a preferred choice for applications in plastics, coatings, ceramics, and cosmetics. These deposits yield consistent mineralogy and low impurity levels, enabling excellent reinforcement performance in polypropylene compounds and improved thermal properties in engineering plastics. With the growing adoption of automotive lightweighting, advanced ceramics, and high-performance coatings, this type represents the largest deposit type.

Talc-serpentine deposits exhibit a mixed mineralogy derived from serpentinite host rocks, offering good thermal stability and moderate brightness, making them ideal for use in ceramics, refractories, rubber, and as industrial fillers. In 2025, this type continued to maintain strong demand in Asia, where large building materials and tile manufacturing hubs rely on its cost-effectiveness and functional performance. Though not as pure as carbonate grades, its favorable balance of strength, thermal resistance, and chemical inertness supports applications requiring durability over whiteness. With the ongoing expansion of the construction, industrial ceramics, and rubber goods markets, serpentine talc is expected to experience moderate demand, particularly in India, China, and Southeast Asia.

Talc-chlorite ores comprise talc interlayered with chlorite and associated silicates, producing grades known for high lamellarity, improved stiffness, and enhanced barrier performance. In 2025, this type gained traction in paints, paper, engineered fillers, and technical ceramics, which require controlled rheology and abrasion resistance. While these deposits typically exhibit narrower availability, as observed in Finland, Japan, and select European regions, they offer specialized performance advantages that are not easily matched by bulk industrial grades. Their ability to improve coating matting, paper smoothness, and polymer dimensional stability positions it as an important niche category serving value-added and specialty industrial markets.

The others category encompasses mixed talc ores, including dolomitic, magnesitic, and ophiolite-associated deposits, which supply lower-purity but cost-competitive industrial grades. These materials serve large-volume applications in agriculture, construction fillers, foundry compounds, and certain ceramic and coating formulations where purity or brightness requirements are moderate. This segment remained essential for price-sensitive markets in Latin America, Africa, and parts of Asia, where industrial demand is driven by construction and basic manufacturing. While not suitable for cosmetics or high-end plastics, mixed-ore provides functional performance at economical cost, ensuring its steady demand in diverse downstream industries.

By End Use

Plastic Holds Leading Share as it Benefits End Use Applications in Cost-Effectiveness

Based on end use, the market is segmented into plastics, ceramics, paints & coatings, pulp & paper, rubber, personal care & cosmetics, and others.

To know how our report can help streamline your business, Speak to Analyst

Plastics remained the largest end-use segment in 2025, driven by the product’s critical role in reinforcing polypropylene, producing lightweight composites, and manufacturing automotive components. Mineral’s lamellar structure enhances stiffness, heat resistance, dimensional stability, and impact strength, supporting applications across bumpers, dashboards, appliance housings, and packaging. As OEMs continue to shift from metal-based systems to polymer-based ones, talc-filled PP compounds have gained broader acceptance due to their cost-effectiveness and mechanical performance. The growing demand for recycled plastics has further accelerated the usage, as it restores lost properties and improves processing efficiency across the mobility, packaging, and consumer goods industries.

Ceramics is another high-volume application, driven by strong demand from tiles, sanitaryware, refractories, and technical ceramics. The product enhances firing behavior, thermal shock resistance, and dimensional stability, while providing smoother surfaces and reduced warpage. Rapid urbanization in the Asia Pacific, the Middle East, and Latin America has strengthened demand for ceramic tiles and bathroom fixtures, supporting steady mineral consumption. As a result, this segment remains a stable and essential driver for the market's growth.

The product plays a vital role in architectural and industrial coatings due to its ability to control rheology, provide matting, enhance barrier properties, and offer anti-corrosion protection. In 2025, demand was supported by expanding construction activity, growth in protective coatings, and rising use of matte finishes in decorative paints. Talc’s plate-like morphology improves opacity, scrub resistance, weatherability, and film durability, making it a preferred extender in high-performance coatings. Industrial users value the product’s ability to reduce permeability and improve coating uniformity, which will support demand for the product in the forecast period.

The others category includes usage in adhesives, sealants, agriculture, foundry compounds, and electrical insulators, where cost-effective functional performance is prioritized. Fertilizer producers use the product as an anti-caking and flow-improving agent, while foundries benefit from its heat tolerance and mold-release qualities. In construction applications, it improves workability and durability in sealants and joint compounds. Although fragmented, this segment provides a consistent baseline demand across diverse industrial and manufacturing environments.

Talc Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Talc Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the largest market share in 2025, valued at USD 1.21 billion, and is expected to lead in 2026. Asia Pacific is identified as the largest and fastest-growing market globally, driven by robust manufacturing activity in plastics, ceramics, paints, and rubber. The region benefits from abundant mineral reserves, competitive processing costs, and the presence of large tile, sanitaryware, automotive, and polymer industries. China and India dominate both production and consumption, while Japan and South Korea rely on high-purity imports for specialty applications. Rapid urbanization, construction expansion, and increasing plastics processing capacity drive demand across various industrial grades. With increasing investments in ultra-fine grinding and engineered talc products, the Asia Pacific continues to shape global supply chains and downstream consumption trends.

In 2025, China reached USD 0.74 billion as it is the world’s single-largest producer and consumer of the product, supported by extensive reserves and a highly diversified industrial base. Ceramics, plastics, and rubber dominate consumption, while significant volumes are also used in coatings, agriculture, and polymer masterbatches. Although pricing remains lower than in Western markets, China is progressively upgrading its quality to supply higher-purity grades, which will shape the country’s market dynamics in the long-term forecast period.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe maintains a well-diversified market, supported by advanced manufacturing, high-quality standards, and stringent environmental regulations. Major consuming sectors include plastics, coatings, engineering ceramics, and specialty papers. Countries such as Germany, France, Italy, and Finland play key roles in both production and high-value consumption. The region favors premium, asbestos-free talc grades due to strict regulatory requirements and consumer preferences for high-quality products. While construction and industrial coatings provide steady demand, structural declines in printing paper offset some growth. Continuous product innovation, sustainable sourcing, and ultra-fine milling technologies are central to Europe’s competitive positioning in both industrial and specialty applications.

North America

North America represents a mature market characterized by stable industrial demand, strong regulatory oversight, and a concentrated producer base. The U.S. accounts for the majority of regional consumption, driven primarily by plastics, paints & coatings, and personal care applications. Automotive lightweighting and engineered plastics continue to support long-term usage, although growth remains moderate due to high material substitution pressure and a declining paper industry. The demand for high-purity grades in the cosmetics and pharmaceutical industries remains resilient, driven by stringent product quality standards. With limited domestic mining expansion, North America heavily relies on imports for specialty and cosmetic-grade minerals.

Latin America and the Middle East & Africa

Over the forecast period, the Latin America and Middle East & Africa regions would witness a moderate growth in this market. Latin America’s market is primarily driven by Brazil and Mexico, with support from strong demand for ceramics, construction materials, and plastics. The region’s expanding tile and sanitaryware production base makes ceramics the dominant consumer, while industrial coatings, adhesives, and rubber compounds provide a steady baseline demand. Growth remains moderate yet stable, closely tied to urbanization, housing activity, and manufacturing trends.

The Middle East & Africa is characterized by expanding demand for construction, ceramics, and industrial coatings, particularly within the GCC and North African regions. The consumption of the product is driven by large-scale tile manufacturing, infrastructure development, and the growth of the polymer processing industry. While deposits exist in Egypt, Morocco, and Afghanistan, much of the high-purity and specialty-grade is imported from Asia and Europe. As industrial capacity expands, especially in the UAE, Saudi Arabia, and South Africa, the region remains a steadily growing consumer of both industrial and specialty talc grades.

COMPETITIVE LANDSCAPE

Key Industry Players:

Companies Maintain their Dominant Position by Integrating Advanced Technologies in Manufacturing Process

The global talc market is moderately consolidated, with competition shaped by ore quality, beneficiation capabilities, product purity, and regional distribution strength. Leading players, including Imerys, Golcha Group, IMI Fabi, Sibelco, Mondo Minerals, Nippon Talc, and Liaoning Aihai, control a significant share of high-quality deposits worldwide, particularly carbonate-rich and low-impurity reserves. These companies differentiate themselves through advanced milling technologies, ultra-fine and surface-treated grades, and stringent quality assurance, enabling them to meet the demanding applications in plastics, coatings, ceramics, and personal care. The premium cosmetics and pharmaceutical sectors remain dominated by suppliers with proven asbestos-free certification and fully traceable sourcing. With global customers increasingly prioritizing certified and ethically sourced talc, sustainability, environmental compliance, and responsible mining practices are becoming major competitive levers in mature markets.

LIST OF KEY TALC COMPANIES PROFILED:

- Golcha Group (India)

- Imerys S.A. (France)

- IMI Fabi S.p.A. (Italy)

- Liaoning Aihai Talc Co., Ltd. (China)

- Liaoning Xinda Talc Group (China)

- Mondo Minerals B.V. (Netherlands)

- Nippon Talc Co., Ltd. (Japan)

- Sibelco N.V. (Belgium)

- Sudarshan Mineral (likely Sudarshan Chemical Industries Ltd.) (India)

- Vasundhara Micro Mineral Infinite Pvt Ltd (India)

KEY INDUSTRY DEVELOPMENTS:

- May 2025: IMI Fabi acquired Elementis's industrial talc business for a total enterprise value of USD 121 million. This transaction includes all of the talc business's assets, sites, and employees, which IMI Fabi will integrate under its existing brands, such as Mondo Minerals. Elementis stated this divestment was a strategic move to become a more focused "pure-play" specialty chemicals company.

- October 2023: Imerys Company established a new talc processing plant in Wuhu, China, which will supply mineral solutions to the Chinese automotive market, specifically to support the transition toward Electric Vehicles (EVs) through products used for lightweighting plastics. The plant's strategic location and high-quality talc products are intended to meet the growing demand for sustainable and high-performance materials in China's rapidly expanding EV sector.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.3% from 2026-2034 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Segmentation | By Deposit Type, End Use, and Region |

| By Deposit Type |

|

| By End Use |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.18 billion in 2025 and is projected to reach USD 2.93 billion by 2034.

In 2025, Asia Pacific’s market value stood at USD 1.21 billion.

The market is expected to exhibit a CAGR of 3.3% during the forecast period.

The talc-carbonate segment led the market by deposit type.

The key factors driving the market are the increasing use of talc as a plastic reinforcement, lightweight composites, and as a high-performance filler in polypropylene and other polymers.

Imerys, Golcha Group, IMI Fabi, Sibelco, Mondo Minerals, Nippon Talc, and Liaoning Aihai are some of the prominent players in the market.

In terms of market share, Asia Pacific dominated the market in 2025.

Growing emphasis on sustainable and traceable mineral sourcing will favor the adoption of greener talc products.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us