Tankless Water Heater Market Size, Share & Industry Analysis, By Energy Source (Gas [Condensing and Non-condensing], [Below 8 Liters/Min, 8-15 Liters/Min, and Above 15 Liters/Min] and Electric [Below 6 KW, 6-12 KW, and Above 12 KW]), By Project Type (New Installation and Replacement/Retrofit), By Smart/Connectivity Feature (Connected/Smart-enabled and Non-connected), By End-User (Residential Settings, Hospitality Settings, Healthcare Facilities, & Educational Institutions), By Distribution Channel (Specialty Stores, Hypermarkets & Supermarkets, & Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

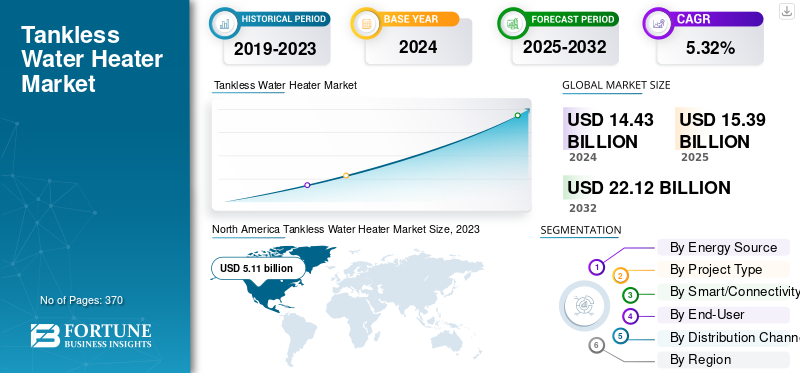

Tankless Water Heater Market Size and Future Outlook

The global tankless water heater market size was valued at USD 15.39 billion in 2025. The market is projected to grow from USD 16.35 billion in 2026 to USD 24.32 billion by 2034, exhibiting a CAGR of 5.09% during the forecast period.

Tankless water heaters are energy-efficient products that provide an endless supply of hot water. Such products have a longer shelf life and exhibit space-saving designs, compared to traditional tank models. The rising demand for energy-efficient and space-saving heating appliances among nuclear and single-person households is primarily driving market growth. In addition, advancements in vent pipe systems and sensor technology-based instant heater models encourage consumers to purchase such products, favoring product sales worldwide. At the 2025 AHR Expo, Rinnai showcased its SENSEI RX gas tankless heater featuring Smart Connect mobile setup/monitoring, Smart-Circ Intelligent Recirculation, and Smart Sense adaptive gas valve technology. This delivers improved diagnostics, easier installation, and optimized combustion.

The global market is characterized by key players, including Paloma Co., Ltd., Rinnai Corporation, Noritz Corporation, KyungDong Navien Co., Ltd., and Robert Bosch GmbH.

Download Free sample to learn more about this report.

Tankless Water Heater Market Key Takeaways

- 2025 Market Size: USD 15.39 billion

- 2026 Market Size: USD 16.35 billion

- 2034 Forecast Market Size: USD 24.32 billion

- CAGR: 5.09% from 2026–2034

- Asia Pacific dominated the tankless water heater market with a 36.23% share in 2025.

- The gas segment is expected to account for 71.74% of the global market in 2026.

- The residential settings segment is projected to hold a 75.35% market share in 2026.

Asia Pacific

Asia Pacific generated USD 5.58 billion in revenue and captured 36.23% of the global market in 2025.

North America

North America accounted for USD 5.57 billion and represented 36.17% of the global market in 2025.

Europe

Europe reached USD 3.48 billion in 2025, contributing 22.60% of global market demand.

U.S.

The market size stood at USD 4.52 billion in 2024, supported by strong demand for energy-efficient water heating systems.

Japan

Growing home renovation activities and replacement demand are supporting market expansion across the country.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Residential and Commercial Infrastructural Settings to Drive Market Growth

The growing number of residential infrastructure facilities and the rising product replacement rate among households are mainly driving the global tankless water heater market growth. Additionally, the expansion of commercial infrastructure facilities, including hospitality settings, healthcare facilities, offices, educational institutions, and others, along with a preference for compact-sized heating appliances, is driving global product demand. The increasing household investments in retrofit and renovation projects positively contributes to market expansion. The International Energy Agency (IEA) Breakthrough Agenda Report, published in 2023, noted that around 80% of new building floor-area growth through 2030 is expected to occur in emerging and developing economies. This implies significant construction activity in regions with a rising demand for stainless steel-based water heating solutions.

MARKET RESTRAINTS:

High Initial Cost and Installation Complexity to Restrain Market Growth

Installing tankless water heaters is complex and costlier than installing conventional storage units. Many tankless systems require an electrical capability, upgraded gas pipelines, and specialized venting, which incur additional installation costs. The high initial cost and installation complexity associated with such models are mainly restraining product demand across many countries. Furthermore, the increasing consumer access to tanked heater products at discounted rates is restraining the global market growth.

MARKET OPPORTUNITIES:

Soaring Popularity of Wi-Fi and App-connected Home Products to Favor Market Growth

The rising adoption of connected home products, including Wi-Fi-enabled and app-integrated instant water heaters featuring real-time monitoring and energy control, is creating new growth opportunities for tankless water heaters. In addition, manufacturers' consistent efforts to embed smart modules into product design to enhance consumers’ experiences are favoring market growth. According to a survey conducted by the government of the U.K., DESNZ Public Attitudes Tracker, in the winter 2024 season, around 25% of U.K.-based households prefer installing a new air-source heat pump in their next product replacement cycle (a connected-ready, app-controllable heating category in many models).

TANKLESS WATER HEATER MARKET TRENDS:

Rising Demand for Energy-Efficient Condensing Tankless Systems to Augment Market Growth

Tight energy-efficiency and emission-related regulations are encouraging manufacturers to produce condensing and high-efficiency gas heaters. Governmental mandates for setting energy efficiency standards for water heaters, along with the provision of tax incentives and rebates, are uplifting product demand across many countries. Additionally, consistent investments by manufacturers in R&D activities for instant heaters are favoring market growth.

MARKET CHALLENGES:

Consumers' Accessibility to Alternative Water Heating Technologies to Hamper Key Players’ Product Revenue Growth

Increasing consumers’ accessibility to alternative water heating technologies, including heat pump water heaters, hybrid storage units, and solar thermal systems, is negatively impacting the sales of instant heaters by global key players. Additionally, the increasing implementation of policies and consumer preference for product alternatives are favoring global business expansion.

Download Free sample to learn more about this report.

Segmentation Analysis

By Energy Source

High Heating Capacity and Better Water Flow Rate of Gas-Powered Systems Led to the Dominance of the Gas Segment

Based on energy source, the market is bifurcated into gas and electric.

The gas segment exhibited a leading tankless water heater market share in 2024. This growth is driven by its higher heating capacity, faster flow rates, and broad suitability for multi-bath residential and commercial applications. Gas tankless systems have traditionally been the backbone of the market in regions such as North America, Europe, and Japan, where gas distribution infrastructure is well-established. They are also widely favored for retrofit and replacement in existing buildings due to easier integration with existing gas lines. The gas segment is expected to lead the market, contributing 71.74% globally in 2026.

Based on technology, the gas segment is further sub-segmented into condensing and non-condensing. The condensing segment held a leading global market share due to the superior energy efficiency and performance of condensing technology-based heaters compared to their counterparts.

Based on capacity, the gas segment is further sub-segmented into below 8 liters/min, 8-15 liters/min, and above 15 liters/min. The 8–15 liter/min segment exhibited a leading share within the gas segment due to its ideal balance between performance, cost, and installation flexibility for most residential applications. This capacity range comfortably supports typical single to two-bath households, which make up the largest share of installations globally.

To know how our report can help streamline your business, Speak to Analyst

The electric segment is projected to excel at a CAGR of 6.39% during the forecast period of 2025-2032. The segment’s fastest growth is attributed to the rising adoption of electrical appliances and ease in product installation, compared to gas-powered products. Additionally, the growing trend of electrification and the implementation of decarbonization policies by governments are expected to increase the demand for electric heaters, thereby favoring the segment’s growth.

Based on power rating, the electric segment is further segregated into below 6 kw, 6-12 kw, and above 12 kw. The 6-12 kw sub segment exhibited a leading market share within the electric segment, as the electric tankless water heaters falling within this power rating range are more energy efficient and require minimal installation costs, compared to products that fall under other power rating ranges. Furthermore, high mid-sized households’ demand for products falling under this power rating, requiring minimal electrical upgrades, is generating considerable revenues from the 6-12 kw segment.

By Project Type

High Number of Customers Replacing their Existing Products with New Ones Drives Replacement/Retrofit Segment Growth

Based on project type, the market is bifurcated into new installations and replacements/retrofits.

The replacement/retrofit segment exhibited a leading global market share in 2024. Its leading share is attributed to the high number of household consumers who prefer replacing existing products with newer technology-based ones. In addition, rising electricity expenses and governmental initiatives aimed at allocating incentives for new product innovation are positively impacting tankless water heater demand among replacement projects, thereby accelerating growth in the replacement/retrofit segment. The replacement/retrofit segment is expected to lead the market, contributing 70.28% globally in 2026.

The new installation segment is projected to grow at the fastest rate of 6.05% between 2025 and 2032. The segment’s fastest growth is attributed to the rapid construction of new housing and the installation of tankless systems by builders and property developers. Furthermore, the expansion of corporate facilities is positively contributing to segmental growth.

By Smart/Connectivity Feature

Better Affordability of Basic Tankless Heaters Models Led the Non-Connected Segment to Hold a Leading Market Share

Based on the smart/connectivity feature, the market is classified into connected/smart-enabled and non-connected.

The non-connected segment captured the leading global market share as non-connected products are more affordable and traditionally accepted by households across many countries. Additionally, the need for low maintenance of non-connected products is driving segmental growth. The non-connected segment will account for 73.39% market share in 2026.

The connected/smart-enabled segment is slated to grow at the fastest rate of 6.69% during the forecast period of 2025-2032. The segment’s fastest growth is attributed to the rising adoption of smart homes and increasing demand for app-connected products, enabling better monitoring and remote control. Additionally, advancements in the development of connected technology-based water heaters, including diagnostic alerts and scheduling features, are creating new growth opportunities for the connected/smart-enabled segment.

By End-User

Significant Household Adoption of Water Heaters Led the Residential Settings Segment to Hold a Leading Market Share

Based on end-user, the market is segmented into residential settings, hospitality settings, healthcare facilities, educational institutions, and others.

The residential settings segment held a leading global market share of 75.35% in 2026. This growth is attributed to the widespread adoption of water heaters among apartment buildings and other residential properties. Increasing housing development and governmental investment in allocating housing facilities to the citizens are positively contributing to the segmental revenue growth in many countries.

The hospitality settings segment is slated to grow at the fastest CAGR of 5.53% during the forecast period of 2025-2032. The segment’s fastest growth is due to the expanding tourism and hospitality infrastructure, which requires the extensive use of tankless heaters across many countries. Furthermore, the growing adoption of connected technology-based electric heaters in hospitality settings, which enables hotel guests to monitor the water flow of the heater remotely, is favoring segmental growth.

By Distribution Channel

High Product Sales from Professional Installers and Contractors Led Wholesale Stores Segment Growth

Based on distribution channel, the market is segmented into specialty stores, hypermarkets & supermarkets, wholesale stores, online channels, and others.

The wholesale stores segment held a leading global market share of 47.70% in 2024. Consumers heavily rely on wholesale heater distributors, plumbers, and HVAC contractors to install branded heating appliances. The largest share of the wholesale stores segment is attributed to high consumer spending on products that are primarily purchased from wholesale distributors. Furthermore, the consistent provision of technical assistance and product-related maintenance guidance by contractors and plumbers enhances users’ loyalty to the services, favoring the segment’s growth.

The online channels segment is slated to grow at the fastest CAGR of 6.67% during the forecast period of 2025-2032. The fastest growth of this segment is due to the rising adoption of e-commerce for the online shopping of home appliances and a greater preference for home delivery options.

Tankless Water Heater Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America Tankless Water Heater Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America contributed approximately USD 5.57 Billion to the global market in 2025, accounting for 36.17% share, and is expected to reach USD 5.87 Billion in 2026. High spending on retrofit projects and rising consumer demand for energy-efficient products are mainly generating considerable product revenues in the region. Additionally, the expansion of urban housing infrastructure and consistent development of tourism facilities increases the demand for tankless water heating products, driving market growth in the U.S. and Canada. In 2024, the U.S. market size reached USD 4.52 billion. The robust infrastructure of gas supplies and the presence of a wider consumer base that prefers energy-efficient products are primarily generating considerable product revenues in the U.S.

Asia Pacific

The Asia Pacific region captured 36.23% of the global market in 2025, generating USD 5.58 Billion in revenue, and is projected to reach USD 6. Billion in 2026. The region exhibited a second leading position in the global market in 2024. Rapid urbanization, growing residential infrastructure construction, and high demand for electric and non-condensing gas models of water heaters are mainly generating product revenues in India, China, Japan, and Southeast Asia. Furthermore, the increasing consumer spending on home renovation/retrofit projects is uplifting the product replacement rate, driving market growth in Japan, Australia, and South Korea.

Europe

In 2025, the Europe market stood at USD 3.48 Billion, representing 22.60% of global demand, and is projected to grow to USD 3.65 Billion in 2026. The European region held a third-leading global market share during the forecast period. Stricter governmental standards related to the sale of less energy-efficient products are primarily supporting the sales of condensing gas and electric systems in the region. Robust smart housing facilities and significant spending on newer products aligning with their lifestyle needs are generating considerable product revenue in the Western European region. The expansion of commercial infrastructure facilities, which necessitate the use of tankless heaters, is driving market growth in Russia and the Eastern European region.

South America and the Middle East & Africa

In 2025, Middle East & Africa generated USD 0.27 Billion, contributing 1.78% to global market revenue, and is projected to grow to USD 0.29 Billion in 2026. Over the forecast period, the market in the South America and the Middle East & Africa regions is expected to witness a moderate growth rate from 2025 to 2032. South America contributed 3.22% to the global market in 2025, with a valuation of USD 0.5 Billion, and is projected to reach USD 0.53 Billion in 2026. The growing number of middle-income households and increasing housing construction in Brazil, Chile, and Colombia are primarily driving market growth in the South American region. The growing hospitality and residential infrastructural facilities in the GCC countries and Southern Africa are mainly driving market growth in the Middle East & Africa region. In the Middle East & African market, South Africa exhibited a market value of USD 0.08 billion by 2025.

COMPETITIVE LANDSCAPE

Key Industry Players:

Geographical Expansion and Product Innovation to Help Key Players Maintain their Market Positions

Key players operating in the global market include Paloma Co., Ltd., Rinnai Corporation, Noritz Corporation, KyungDong Navien Co., Ltd., and Robert Bosch GmbH. These players consistently focus on development smart technology-based products to enhance consumers’ experience of hot water bathing. Furthermore, they establish partnerships with retailers to strengthen their product reach across global markets.

LIST OF KEY TANKLESS WATER HEATER COMPANIES PROFILED:

- Paloma Co., Ltd. (Japan)

- Rinnai Corporation (Japan)

- Noritz Corporation (Japan)

- KyungDong Navien Co., Ltd. (South Korea)

- Robert Bosch GmbH (Germany)

- O. Smith Corporation (U.S.)

- STIEBEL ELTRON GmbH & Co. KG (Germany)

- Ariston Holding N.V. (Italy)

- Vaillant GmbH (Germany)

- Haier Smart Home Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS:

- March 2025: Paloma launched Rheem IKONIC Commercial Tankless Gas Water Heaters, a high-efficiency condensing line designed for restaurants, lodging, and other commercial applications.

- February 2025: Noritz launched the CMK/CRK manifold and rack kits to simplify multi-unit installations, offering flat-packed, easy-to-assemble kits that reduce installation time by up to half.

- September 2024: Racold, a water heating solution provider, launched Omnis Slim Electric Storage Water Heater and the Aures Pro 13 kW Tankless Water Heater products in an Indian market. These products are made of cutting-edge technologies that provide enhanced bathroom comfort to the users.

- March 2024: Paloma’s Rheem brand introduced the Rheem RTGH Series Super High Efficiency Condensing Tankless Gas Water Heaters, featuring built-in diagnostics and optional Wi-Fi (EcoNet) to expedite contractor installations and connected service.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.09% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Energy Source, Project Type, End-User,Smart/Connectivity Feature, Distribution Channel, and Region |

|

By Energy Source |

Gas

Gas

Electric

|

|

By Project Type |

|

|

By Smart/Connectivity Feature |

|

|

By End-User |

|

|

By Distribution Channel |

|

|

By Geography |

North America (By Energy Source, Project Type, End-User, Smart/Connectivity Feature, Distribution Channel, and Country)

Europe (By Energy Source, Project Type, End-User, Smart/Connectivity Feature, Distribution Channel, and Country)

Asia Pacific (By Energy Source, Project Type, End-User, Smart/Connectivity Feature, Distribution Channel, and Country)

South America (By Energy Source, Project Type, End-User, Smart/Connectivity Feature, Distribution Channel, and Country)

Middle East & Africa (By Energy Source, Project Type, End-User, Smart/Connectivity Feature, Distribution Channel, and Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 15.39 billion in 2025 and is projected to reach USD 24.32 billion by 2034.

In 2025, the market value stood at USD 5.57 billion.

The market is expected to exhibit a CAGR of 5.09% during the forecast period of 2026-2034.

The gas segment led the market by energy source in 2025.

The expansion of residential and commercial infrastructure facilities are the key factors driving the market.

Paloma Co., Ltd., Rinnai Corporation, Noritz Corporation, KyungDong Navien Co., Ltd., and Robert Bosch GmbH are some of the prominent players in the market.

North America dominated the market in 2025 with the largest share.

The growing popularity of Wi-Fi and app-connected home products is expected to favor the product adoption rate.

- 2021-2034

- 2025

- 2021-2024

- 370

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us