Electric Vehicle (EV) Market Size, Share & Industry Analysis By Vehicle Type (Passenger Car and Commercial Vehicle), By Propulsion Type (Battery Electric Vehicle (BEV) and Hybrid Electric Vehicle (HEV)), By Drive Type (All Wheel Drive, Front Wheel Drive, and Rear Wheel Drive), By Range (Up to 150 Miles, 151-300 Miles, and Above 300 Miles), By Component (Battery Pack & High Voltage Component, Motor, Brake, Wheel & Suspension, Body & Chassis, and Low Voltage Electric Component), and Regional Forecast, 2026–2034

Global Electric Vehicle Market Analysis & Outlook

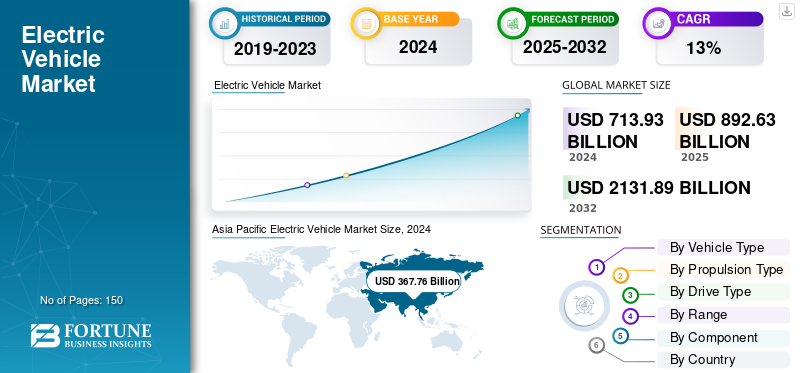

The global electric vehicle market size was valued at USD 927.69 billion in 2025 and is projected to grow from USD 1023.81 billion in 2026 to USD 2190.37 billion by 2034, exhibiting a CAGR of 9.97% during the forecast period. Asia Pacific dominated the electric vehicle market with a market share of 51.78% in 2025.

The environmental impact of conventional gasoline vehicles and the rise in fuel prices have paved the way for alternative fuel vehicles in the market. Buyers are gradually getting inclined to use battery-powered or hybrid automobiles, which is anticipated to drive market expansion. All models use one or more electric motors for propulsion, and electricity serves as the main energy source for EVs. Since they do not have an internal combustion engine installed in them, their overall emissions are significantly lower. The sudden rise in the market’s CAGR can be attributed to the robust demand for alternative fuel vehicles.

Fossil fuel-based vehicles are one of the main causes of air pollution across the world. Therefore, it has forced many governing bodies to impose strict emission regulations on car manufacturers to curb vehicle emissions. In recent years, the demand for BEVs has increased considerably among consumers as these vehicles do not use traditional fuels, such as gasoline or diesel. The maintenance cost of EVs is also considerably less, which gives them an advantage over conventional fuel-based vehicles.

The global electric vehicle (EV) market is dominated by BYD, Tesla, and Volkswagen Group, which together account for a significant share of global EV sales. BYD leads the market with the maximum market share of global EV sales (battery electric vehicle) (BEV) + plug-in hybrid electric vehicle (PHEV), backed by strong vertical integration across batteries, manufacturing, and logistics, enabling cost efficiency and supporting its rapid global expansion.

Early EV market growth was largely incentive-dependent, but electric vehicle market growth now reflects whether manufacturers can lower battery costs, improve platform efficiency, and protect margins amid rising competitive intensity. The industry’s next phase is likely to reward scale discipline rather than volume expansion alone. Vehicle manufacturers capable of reducing battery cost per kilowatt-hour while sustaining pricing flexibility are expected to strengthen electric vehicle market share over the forecast period.

Battery procurement is increasingly shaping competitive positioning across the automotive sector. Manufacturers are shifting from transactional sourcing toward vertically coordinated battery ecosystems, treating localization not solely as supply security but as a profitability mechanism. Exposure to lithium, nickel, graphite, and rare material volatility continues influencing vehicle pricing strategies and investment decisions. At the same time, battery chemistry selection is becoming commercially strategic. Battery Electric Vehicles (BEVs) are strengthening adoption in markets where charging reliability and utilization rates support ownership convenience, whereas Hybrid Electric Vehicles (HEVs) continue serving regions where infrastructure gaps make full electrification economically inconsistent.

The electric vehicle market size expansion is becoming more segmented by use case rather than consumer preference alone. Urban passenger mobility and predictable commercial delivery fleets demonstrate stronger adoption economics because charging downtime remains manageable and the total cost of ownership improves more rapidly. Long-haul freight electrification continues progressing cautiously due to battery weight tradeoffs, route uncertainty, and infrastructure intensity. This divergence increasingly shapes manufacturer investment priorities and product portfolios.

Download Free sample to learn more about this report.

Electric Vehicle (EV) Market KEY TAKEAWAYS

- 2025 Market Size: USD 927.69 billion

- 2026 Market Size: USD 1,023.81 billion

- 2034 Forecast Market Size: USD 2,190.37 billion

- CAGR: 9.97% from 2026–2034

- Asia Pacific dominated the electric vehicle market with a 51.78% share in 2025.

- The Passenger Cars segment is expected to account for 67.02% of the global market share in 2026.

- The Battery Electric Vehicles (BEVs) segment is projected to lead the market with a 75.53% share in 2026.

Asia Pacific

Asia Pacific led the global market in 2025, generating USD 480.38 billion in revenue and accounting for 51.78% of total market share.

Europe

Europe captured 31.11% of the global market in 2025, with revenue reaching USD 288.62 billion.

North America

North America accounted for 15.62% of global demand in 2025, with the market valued at USD 144.89 billion.

U.S.

U.S. The electric vehicle market is projected to reach USD 138.04 billion by 2026, supported by growing EV adoption and charging infrastructure expansion.

Japan

Japan The electric vehicle market is projected to reach USD 3.05 billion by 2026, driven by increasing electrification initiatives and government support.

Read More

Electric Vehicle Market Trends

Rising Investment in EVs to Boost Market Growth

Electric vehicle market growth is anticipated to be fueled by increasing investment in electric mobility. Notable industry players, including Daimler AG, Ford Motor Company, BYD, and Renault Group, are spending their money and production plans to strengthen their EV portfolios. For instance, in March 2025, BYD announced the establishment of its first manufacturing unit in India, with Telangana emerging as the frontrunner.

The Telangana government has proposed three potential sites near Hyderabad for the plant, and BYD representatives are currently assessing these locations before making a final decision. The state government has assured full support, including land allocation, for the project. BYD is also planning to set up a 20-gigawatt battery production plant in India. Over the next five to seven years, it aims to ramp up its production capacity to 600,000 EVs annually.

The electric vehicle market is increasingly transitioning toward platform consolidation, battery localization, and software-defined mobility models. Vehicle manufacturers are moving away from fragmented electric architectures and adopting modular vehicle platforms to improve production scalability, reduce engineering costs, and accelerate model deployment. This shift reflects growing pressure to improve profitability as electric vehicle price competition intensifies across both premium and mass-market categories.

Battery chemistry diversification is becoming a defining electric vehicle market trend. Manufacturers increasingly deploy lithium iron phosphate batteries for cost-sensitive vehicle categories while preserving nickel-rich chemistries for premium models requiring longer range. This dual-chemistry approach reflects a broader industry recognition that battery optimization now depends on use-case economics rather than maximum performance specifications alone.

Charging infrastructure expansion remains important, although utilization efficiency is becoming equally significant. Markets with stronger charger reliability, faster charging cycles, and higher network density demonstrate more resilient electric vehicle market growth. Industry participants increasingly recognize that infrastructure quality matters more than installation volume in sustaining long-term adoption momentum.

Download Free sample to learn more about this report.

EV Market Dynamics

Market Drivers

Favorable Government Subsidies and Policies to Augment Market Growth

Increasing demand for EVs will likely accelerate market growth during the forecast period. Governments across the world are offering attractive incentives and policies to encourage the sales of EVs. These incentives include reduced selling prices, zero or low registration fees, and free access to charging infrastructure at multiple charging stations. Additionally, many countries exclude import, purchase, and road taxes through various subsidy programs.

The production of EVs has increased due to these subsidies for the auto industry. Governments have also made significant infrastructure investments and introduced helpful policies to strengthen the EV system. For instance, over the next five years, the U.S. government intends to spend USD 287 billion on building new highways. In order to support the development of these vehicles, the government will also be putting up EV charging stations all around the U.S. In the future years, it is anticipated that these activities will increase the market share of electric vehicles.

Strict Government Regulations on Vehicle Emissions to Boost Market Growth

Governments of many countries have implemented strict vehicle emission regulations to reduce the amount of greenhouse gas emissions in the atmosphere. For instance, in 2022, the European Union formed a regulation requiring 15% reduction in CO2 emissions from light and medium commercial vehicles before 2025. The Petroleum Ministry of India mandated all automotive manufacturers to start producing BS-VI vehicles after 1 April 2020, a move aimed at reducing air pollution in the country. These stringent steps taken by several regulatory bodies to curb air pollution are expected to boost this industry’s growth in the coming years.

The electric vehicle market growth continues, benefiting from tightening emissions regulations and long-term industrial policy support. Governments increasingly position vehicle electrification as a strategic mechanism for reducing transport emissions, lowering fossil fuel dependency, and strengthening advanced manufacturing competitiveness. These regulatory frameworks continue influencing automaker investment priorities and long-term product roadmaps.

Battery affordability improvements remain another critical growth catalyst. Although raw material volatility persists, battery costs continue declining through chemistry optimization, manufacturing automation, and economies of scale. Vehicle manufacturers increasingly prioritize localized battery production to improve procurement visibility and reduce pricing exposure, strengthening affordability across multiple vehicle categories.

Commercial fleet electrification is emerging as a structurally important growth engine. Logistics providers, urban transport operators, and delivery fleets increasingly evaluate electrified vehicles based on total cost of ownership rather than acquisition price alone. Predictable routes and lower fuel maintenance requirements continue strengthening fleet economics, particularly in urban mobility environments.

Market Restraints

Higher Manufacturing and Battery Costs to Restrain Market Progress

EVs are superior to fossil fuel-based automobiles, but their initial cost remains relatively high. Since electric vehicles have not yet achieved economies of scale, they are not mass-produced. In addition, the absence of EV charging infrastructure has proven to be a negative factor, which has affected the market's growth. Manufacturers also need a lot of investment and assets, which may hamper the market's progress. However, owing to the production of EV batteries in large volumes and technological advancements, the cost of batteries is expected to decrease in the coming years.

Charging infrastructure inconsistency remains one of the most significant barriers to electric vehicle market expansion. Although charger deployment continues accelerating, utilization efficiency, reliability concerns, and uneven geographic distribution continue affecting ownership confidence. Rural markets and long-distance mobility corridors frequently demonstrate slower adoption due to limited charging accessibility and longer waiting times.

Affordability pressures also continue to constrain adoption momentum. Electric vehicles remain comparatively expensive in several regions, particularly where subsidies are declining or battery input costs remain elevated. Vehicle manufacturers increasingly face pressure to balance affordability with profitability, especially amid intensifying price competition and narrowing operating margins.

Raw material concentration risk continues to influence supply chain resilience. Dependence on lithium, nickel, cobalt, and graphite exposes battery manufacturers and automotive companies to geopolitical volatility, export restrictions, and procurement disruptions. Manufacturers increasingly pursue vertical integration and recycling investments to reduce supply insecurity, although implementation remains uneven.

Market Opportunities

Expansion of Charging Infrastructure is the Key Factor for Market Expansion

The expansion of EV charging infrastructure is one of the most critical opportunity factors driving global electric vehicle adoption. A major barrier for consumers has long been range anxiety, but rapid growth in public and private charging networks is easing this concern. Governments are focused on huge investments in electric vehicle charging infrastructure to meet the demand for electric vehicles.

For instance, by 2030, the German government aims to have one million fully accessible and operational charging points for EVs installed nationwide. Several strategic initiatives and funding programs were initiated and directly supported by federal and state governments throughout the past decade. In 2023, around 116,000 (ca. 94,000 AC, 22,000 DC) public charging points with a total of 5.2 gigawatts (GW) of installed charging capacity were available in Germany, up 30% from the year before.

Battery manufacturing localization continues to create significant opportunities across the electric vehicle market. Governments and automakers increasingly invest in regional battery ecosystems to support supply security, strengthen industrial competitiveness, and align with domestic manufacturing objectives. Localized production also helps reduce logistics complexity and supports regional content requirements in several automotive markets.

Commercial mobility represents another important opportunity area. Electrification continues expanding across urban logistics, public transportation, and service fleets, where predictable travel patterns improve charging feasibility. Fleet operators increasingly evaluate electric vehicles through total operating cost considerations, particularly where fuel savings and maintenance reductions support long-term economics.

Battery recycling and second-life battery applications continue gaining attention. Recycling capacity expansion may improve material recovery and reduce dependence on newly mined inputs over time. Energy storage systems using repurposed vehicle batteries are also becoming more common within commercial and grid-support applications.

Market Challenges

Limited Driving Range Significantly Challenges Market Growth

One of the challenging factors for EV adoption is the limitation of driving range compared to conventional ICE vehicles. Most affordable EVs in 2024–25 still deliver around 200–400 km per charge, while a petrol or diesel car typically offers 500–800 km per tank. The factors such as extreme weather, terrain, and accessory usage (such as air conditioning or heating) can further reduce EV range by 20–30%, which heightens consumer concern.

However, the premium electric vehicle offers a range of 600 km per battery charge, their higher price hinders the adoption of EVs. This creates a gap between technological development and consumer accessibility. Thus, the limited driving range of electric vehicles remains a significant factor that may hinder market growth.

EV Market Segmentation

By Vehicle Type

The Passenger Vehicles Segment Holds the Maximum Market Share Due to the Increasing Presence of EV Manufacturers

Based on vehicle type, the market is segmented into passenger and commercial vehicles.

Passenger Car

The passenger vehicle segment holds the maximum market share due to increasing sales in China, India, Norway, and Germany. The adoption rate of EVs in the Asia Pacific is high owing to the presence of EV manufacturers, original equipment manufacturers (OEMs), and other automakers in the region. These factors will help promote the growth of this segment during the forecast period.

The Passenger Cars segment is expected to lead the market, accounting for 67.02% of the global market share in 2026. The segment will hold the largest share of the electric vehicle market, driven by increasing consumer familiarity, expanding model availability, and improving charging infrastructure accessibility. Automakers continue prioritizing passenger vehicle electrification through expanded product portfolios spanning compact vehicles, sport utility vehicles, premium sedans, and crossover categories. Increasing product availability across multiple price segments continues to broaden addressable demand.

Battery Electric Vehicles (BEVs) continue expanding within passenger mobility, particularly in urban and suburban environments where charging access supports routine use. Consumer demand increasingly reflects practical considerations, including driving range, charging convenience, ownership cost, and model availability, rather than environmental preference alone. Premium vehicle categories continue emphasizing performance and software-enabled capabilities, while entry-level offerings increasingly prioritize affordability and operational simplicity.

Passenger electric vehicle adoption tends to be stronger in markets with established charging ecosystems, purchase incentives, and urban density advantages. Consumer behavior also varies according to electricity pricing, fuel costs, and residential charging access. Apartment-dense cities often demonstrate different charging requirements than suburban vehicle markets.

Commercial Vehicle

The electric commercial vehicle segment is estimated to be the fastest-growing in the coming years, owing to the ever-increasing innovations in EV batteries to improve commercial vehicle load capacity.

Commercial vehicles continue to represent a growing segment within the electric vehicle market, although adoption patterns remain more selective than passenger mobility. Electrification is strongest in applications where predictable routes, centralized charging, and controlled fleet operations improve economic viability. Urban logistics, municipal fleets, delivery operations, and public transportation systems continue demonstrating stronger commercialization than long-haul freight segments.

Fleet operators increasingly assess electrification through total operating cost frameworks rather than purchase price alone. Fuel savings, lower maintenance requirements, predictable operating schedules, and regulatory compliance continue influencing adoption decisions. Fixed-route vehicles generally demonstrate stronger feasibility because predictable charging windows reduce operational disruption.

Commercial electrification varies substantially by vehicle class. Light commercial vehicles continue showing stronger adoption than heavy-duty trucks because battery weight, charging downtime, and payload considerations remain more manageable. Public transit agencies increasingly expand electric bus fleets to reduce emissions and comply with urban sustainability requirements.

By Propulsion Type

BEVs Segment to Hold Top Market Position Due to Its Vast Benefits

Based on propulsion type, the market is segmented into Battery Electric Vehicles (BEVs) and Hybrid Electric Vehicles (HEVs).

Battery Electric Vehicle (BEV)

The BEV segment is expected to hold a major market share due to the vast advantages of an electric vehicle. The growth is further supported by the rising production of EVs by OEMs. For instance, in February 2024, BYD announced that the company is set to launch its third electric car, the BYD Seal, in India on March 5. The electric sedan features a sleek design, advanced features, and a range of up to 700 km on a single charge.

In 2026, the Battery Electric Vehicles (BEVs) segment is projected to lead the market with a 75.53% share. The segment is expected to hold an increasing share of the electric vehicle market, driven by the expansion of charging infrastructure and continuous improvements in battery performance. BEVs operate entirely through electricity stored in rechargeable battery systems and do not rely on internal combustion engines during operation. Market adoption continues to strengthen in regions with mature charging ecosystems, supportive policy frameworks, and growing consumer familiarity with electric mobility.

Automakers continue prioritizing BEV production through dedicated electric platforms, expanded model portfolios, and localized battery sourcing strategies. Passenger cars remain the largest deployment category, although commercial applications are gradually increasing where operational routes remain predictable. Improvements in battery range, charging speeds, and thermal management systems continue to support broader market acceptance across both premium and mid-range vehicle categories.

Charging accessibility remains a defining variable influencing BEV adoption. Home charging availability, public fast-charging reliability, and charging network interoperability continue affecting ownership practicality. Urban markets and regions with established charging density generally demonstrate stronger BEV penetration than markets where infrastructure remains uneven. Consumer purchasing decisions increasingly reflect charging convenience alongside vehicle affordability and operating economics.

Hybrid Electric Vehicle (HEV)

The HEV is the second dominant segment, as this vehicle provides the dual option of working on both fuel-based and electric automobiles. This is particularly beneficial in regions with inadequate charging infrastructure. Continued advancements in hybrid electric vehicle (HEV) technology drive the segment’s growth.

Hybrid Electric Vehicles (HEVs) continue to maintain relevance within the electric vehicle market, particularly in regions where charging accessibility remains limited or consumer concerns regarding charging convenience persist. HEVs combine internal combustion engines with electric propulsion systems, improving fuel efficiency without requiring exclusive dependence on charging infrastructure. This operating flexibility continues to support adoption in markets transitioning gradually toward electrification.

Consumer demand for HEVs often reflects practical considerations, including travel range, charging availability, and ownership flexibility. In regions with limited charging density or higher electricity infrastructure constraints, HEVs continue functioning as an intermediate electrification pathway. The segment also remains important among consumers prioritizing fuel efficiency improvements without materially changing driving behavior or charging routines.

Automakers continue to maintain hybrid vehicle portfolios alongside BEV offerings to address varied regional market conditions. Vehicle manufacturers increasingly position hybrids differently according to geography, regulatory requirements, and infrastructure maturity. This diversification strategy reflects uneven electrification readiness across global automotive markets.

By Drive Type

Affordability of Front-wheel Drive Vehicles Encouraged Segment Growth

Based on drive type, the market is divided into All Wheel Drive, Front Wheel Drive, and Rear Wheel Drive.

Front Wheel Drive (FWD)

The front wheel drive (FWD) segment will account for 51.75% market share in 2026. The segment is also expected to register the fastest CAGR during the forecast period, driven by the vehicle's cost efficiency and widespread consumer adoption. Front-wheel drive systems are generally less expensive to manufacture and maintain compared to rear-wheel drive or all-wheel drive systems. This makes Front Wheel Drive vehicles more affordable for customers, thus fueling the segment’s growth.

Front Wheel Drive electric vehicles continue to represent a substantial share of the electric vehicle market due to affordability, manufacturing simplicity, and efficient urban mobility suitability. FWD systems remain common in compact vehicles, city-focused mobility solutions, and cost-sensitive passenger categories where energy efficiency and lower production costs remain important priorities.

Automakers frequently deploy front-wheel drive systems in entry-level and mid-range electric vehicles to optimize battery efficiency and improve pricing competitiveness. Reduced drivetrain complexity often contributes to lower vehicle weight and improved energy consumption performance, strengthening suitability for daily commuting applications.

Urban markets continue demonstrating strong adoption of front-wheel drive electric vehicles because compact form factors and predictable travel patterns align well with battery efficiency priorities. Consumer demand within this segment often reflects affordability considerations and practical ownership requirements rather than performance preferences. FWD systems are therefore expected to remain widely used within mass-market electric vehicle categories.

All Wheel Drive (AWD)

The All Wheel Drive segment accounted for a significant market share in 2026. The growth can be credited to the increasing popularity of all-wheel drive systems in the global automotive industry. The rear-wheel drive segment held a considerable market share in 2024 due to technological advancements in vehicle systems.

All Wheel Drive electric vehicles continue gaining traction across premium passenger mobility and performance-oriented vehicle segments. AWD systems distribute power across all wheels, improving traction, vehicle stability, and performance under challenging road conditions. The segment remains particularly relevant across sport utility vehicles, luxury vehicles, and regions experiencing seasonal weather variability.

Automakers increasingly integrate AWD configurations into premium Battery Electric Vehicle portfolios to improve acceleration, handling precision, and consumer appeal. Dual-motor architectures commonly support electric AWD systems, allowing manufacturers to optimize torque distribution and energy efficiency. This configuration remains especially common in premium electric sport utility vehicles and performance sedans.

By Range

151-300 Segment Dominates the Market Due to Increasing Adoption of Passenger Vehicles

Based on range, the market is divided into up to 150 miles, 151-300 miles, and above 300 miles.

Up to 150 Miles

The up to 150-mile segment holds the second largest due to the adoption of light commercial vehicles and electric vans. The adoption of electric vans is still in its nascent stage. Thus, the growing demand for EVs will drive segmental growth during 2025-2032.

Electric vehicles with a driving range of up to 150 miles continue serving cost-sensitive and urban mobility applications within the electric vehicle market. These vehicles are generally positioned for short-distance commuting, city transportation, shared mobility services, and fleet operations where predictable travel requirements reduce range dependency. Compact vehicle segments and entry-level electric models frequently operate within this category due to affordability considerations and lower battery size requirements.

Consumer adoption within this segment often reflects practical commuting behavior rather than long-distance mobility expectations. Urban drivers with access to home charging infrastructure continue demonstrating stronger suitability for shorter-range electric vehicles. Vehicle affordability remains an important competitive advantage because smaller battery systems generally reduce production costs and overall purchase prices.

151–300 Miles

The 151–300 miles segment is anticipated to hold a dominant market share of 66.16% in 2026. The segment is expected to maintain its leading position in the market, driven by the fact that most passenger electric vehicles are designed to deliver a driving range of 151–300 miles. The rising sales of passenger EVs are expected to augment the segment’s growth.

Electric vehicles offering driving ranges between 151 and 300 miles represent one of the most commercially significant segments within the electric vehicle market. This category balances affordability, operational flexibility, and practical daily usability, making it highly relevant across mainstream passenger mobility. Many mid-range passenger vehicles and sport utility vehicles continue operating within this range bracket.

Consumer demand in this category reflects broader ownership practicality. Vehicles within this range often support both daily commuting and occasional long-distance travel without frequent charging interruptions. As public charging infrastructure expands and fast-charging technology improves, range anxiety concerns continue declining across this segment.

Automakers increasingly prioritize this category because it aligns with broad market demand while maintaining manageable battery costs relative to premium long-range vehicles. Improvements in battery chemistry and energy efficiency continue to support stronger performance within mid-range vehicle categories. This segment is expected to remain central to the electric vehicle market size expansion due to its alignment with mainstream mobility requirements.

Above 300 Miles

Electric vehicles exceeding 300 miles of driving range continue strengthening their position within premium passenger mobility and high-performance categories. Long-range capability remains especially important among consumers prioritizing travel flexibility, reduced charging frequency, and intercity driving convenience. Premium Battery Electric Vehicles frequently compete through range differentiation and charging performance.

Automakers increasingly deploy larger battery systems and advanced thermal management technologies to support longer-range vehicle architectures. Nickel-rich battery chemistries remain more common in this segment because higher energy density supports extended operational performance. However, larger battery systems often contribute to higher production costs and vehicle pricing.

Long-range electric vehicles also remain strategically relevant in regions with less developed charging infrastructure, where extended range improves ownership practicality. Although premium positioning limits mass-market accessibility, this segment continues influencing consumer perception of electric vehicle capability and technological advancement.

To know how our report can help streamline your business, Speak to Analyst

By Component

Battery Pack & High Voltage Component Holds Maximum Market Share Due to Major Cost Contribution

Based on components, the market is divided into battery pack & high voltage component, motor, brake, wheel & suspension, body & chassis, and low voltage electrical component.

Battery Pack & High Voltage Component

The battery pack & high voltage component hold the maximum share due to major cost contribution and their role as a main component for vehicle functioning. Additionally, the price/value of these packs will decrease significantly in the upcoming years. Major manufacturers are focused on developing traction batteries (lithium-ion batteries) and high-voltage components that help enhance performance and reduce cost, which will drive market growth during the forecast period.

Battery pack and high voltage components represent the most critical segment within the electric vehicle market due to their direct influence on vehicle range, charging speed, thermal stability, and overall cost structure. Battery systems continue accounting for a substantial share of vehicle manufacturing costs, making procurement strategy and chemistry selection increasingly important for automakers.

Vehicle manufacturers increasingly invest in localized battery production, long-term mineral sourcing agreements, and battery partnerships to improve supply visibility and reduce logistics complexity. Battery technology improvements continue focusing on energy density, charging efficiency, and durability. High voltage systems also remain essential for supporting power delivery, thermal management, and vehicle performance optimization.

Motor

The motor holds the second-largest share due to its widespread adoption in EVs. Rising EV demand among major countries, coupled with technological advances by OEMs, will augment segment growth. Electric motors remain central to electric vehicle performance, efficiency, and driving dynamics. Unlike conventional internal combustion systems, electric motors provide immediate torque delivery, contributing to smoother acceleration and improved energy efficiency. Automakers increasingly prioritize motor optimization to improve vehicle responsiveness while reducing power consumption.

Permanent magnet and induction motors continue to represent widely used motor categories, although material dependency and efficiency considerations vary across manufacturers. Motor technology decisions increasingly reflect cost management, rare earth material exposure, and performance requirements. Continued investment in lighter and more efficient motor systems remains important as vehicle manufacturers seek improved driving range and manufacturing scalability.

Brake, Wheel & Suspension

Brake, wheel, and suspension systems continue playing an important role in electric vehicle performance, safety, and ride efficiency. Electric vehicles place different operating demands on braking systems because regenerative braking reduces wear on conventional mechanical brakes and contributes to energy recovery. Automakers increasingly optimize brake calibration to balance stopping performance with battery efficiency improvements.

Body & Chassis

Body and chassis systems remain fundamental to electric vehicle market development because structural design directly influences energy efficiency, battery safety, and vehicle weight. Automakers increasingly adopt lightweight materials, including aluminum and high-strength steel, to offset battery weight and improve vehicle range performance. Structural efficiency continues to become a major design priority across passenger and commercial electric vehicles.

Low-Voltage Electric Component

Low-voltage electric components continue supporting essential vehicle operations across the electric vehicle market, including lighting systems, infotainment, climate control, safety electronics, communication modules, and onboard diagnostics. Although smaller in value relative to battery systems, these components remain necessary for overall vehicle functionality and connected mobility performance.

Regional Outlook

Based on region, the market is analyzed across North America, Asia Pacific, Europe, and the Rest of the World.

Asia Pacific Electric Vehicle Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia-Pacific Electric Vehicle Market Analysis

Asia Pacific maintained a strong presence in the global market, reaching USD 480.38 Billion in 2025, accounting for 51.78% share, and is expected to reach USD 532.91 Billion in 2026, driven by the growing demand for passenger cars across developing nations. China accounts for the largest share in terms of passenger cars and other automobiles.

Asia-Pacific accounts for the largest electric vehicle market share due to large-scale manufacturing, battery production leadership, and strong domestic vehicle demand. China, Japan, and South Korea continue playing important roles within supply chains and battery technology development. Regional electric vehicle market growth remains supported by industrial policy, urbanization, and charging infrastructure expansion.

Japan Electric Vehicle Market

The Japan market is projected to reach USD 3.05 billion by 2026. Japan continues contributing to electric vehicle market development through advanced automotive manufacturing, battery technology expertise, and hybrid vehicle leadership. Domestic automakers continue expanding electrified portfolios while strengthening battery supply partnerships. Market adoption remains influenced by infrastructure availability, vehicle affordability, and evolving consumer preferences toward low-emission transportation systems.

China Electric Vehicle Market

The China market is projected to reach USD 513.36 billion by 2026, and the India market is projected to reach USD 4.84 billion by 2026. China leads the global electric vehicle market size through large-scale manufacturing capacity, battery production leadership, and strong domestic demand. Extensive charging infrastructure deployment and vertically integrated supply chains continue supporting market development. Domestic automakers are increasingly expanding electric vehicle portfolios, while battery manufacturing investment continues to strengthen electric vehicle market share and competitiveness.

North America Electric Vehicle Market Analysis

In 2025, the North America market stood at USD 144.89 Billion, representing 15.62% of global demand, and is projected to grow to USD 157.55 Billion in 2026. The regional market’s growth can be attributed to rising initiatives by the Department of Energy (DoE) to build EV charging infrastructure throughout the U.S. to support the growing number of EVs in the region.

North America continues to represent an important electric vehicle market, supported by manufacturing investment, battery localization initiatives, and expanding charging infrastructure. Regulatory measures, corporate fleet electrification, and consumer interest continue to support adoption. Market development remains uneven across regions because charging accessibility, electricity infrastructure, and vehicle affordability continue influencing electric vehicle market growth and ownership patterns.

United States Electric Vehicle Market

The U.S. market is projected to reach USD 138.04 billion by 2026. The United States accounts for the largest regional electric vehicle market size due to expanding vehicle availability, charging infrastructure investment, and battery manufacturing activity. Federal and state-level incentives continue supporting adoption, while automakers increasingly localize production. Commercial fleet electrification and rising consumer familiarity with charging systems continue influencing electric vehicle market growth across multiple segments.

Europe Electric Vehicle Market Analysis

The Europe region captured 31.11% of the global market in 2025, generating USD 288.62 Billion in revenue, and is projected to reach USD 318.73 Billion in 2026. The steps taken by governments to reduce carbon emissions have been driving the market’s growth in the region. The U.K., Germany, and France are important countries contributing to the region's growth. Besides, the rapid adoption of fuel-efficient vehicles will augur well for the European market.

Europe remains a major electric vehicle market, supported by emissions regulations, transport decarbonization goals, and fleet electrification requirements. Electric vehicle market share remains strong in countries with established charging infrastructure and supportive policy frameworks. Battery manufacturing expansion and increasing investment in renewable electricity integration continue to support long-term regional market development.

Germany Electric Vehicle Market

The Germany market is projected to reach USD 97.11 billion by 2026. Germany maintains a strong position within the electric vehicle market due to its established automotive manufacturing capabilities and continued investment in battery production. Domestic automakers continue expanding electric model portfolios while increasing localized supply chain partnerships. Charging network development and industrial policy measures continue to support electric vehicle market growth and broader mobility transition objectives.

United Kingdom Electric Vehicle Market

The UK market is projected to reach USD 49.55 billion by 2026. The United Kingdom electric vehicle market continues to develop through charging infrastructure investment, transport decarbonization policies, and growing model availability. Fleet electrification and urban clean mobility initiatives continue supporting demand. Consumer adoption increasingly reflects charging accessibility, ownership costs, and vehicle availability, while public charging expansion remains important for long-term electric vehicle market growth.

Latin America Electric Vehicle Market Analysis

Latin America continues demonstrating gradual electric vehicle market growth, supported by urban mobility programs, public transportation electrification, and increasing interest in cleaner transport systems. Infrastructure limitations and affordability considerations continue affecting adoption rates. Fleet electrification and policy support remain important factors influencing long-term electric vehicle market development across the region.

Middle East & Africa Electric Vehicle Market Analysis

The Middle East & Africa continue witnessing gradual electric vehicle market expansion through urban sustainability programs, charging investment, and transport diversification efforts. Market growth remains influenced by infrastructure maturity, affordability, and electricity system readiness. Fleet electrification and government mobility initiatives continue supporting regional electric vehicle market development.

Electric Vehicle Industry Competitive Landscape

Key Companies Focus on Developments to Gain Competitive Edge

The market is highly competitive and fragmented, with the presence of key players, such as General Motors Company, Nissan Motors Co. Ltd., Tesla, Inc., Toyota Motor Corporation, BYD Company Ltd., Daimler AG, and Ford Motor Company.

Tesla Inc. is a California-based EV manufacturing company, and its cars are well known for their Autopilot mode and semi-autonomous features. The company is also known for its innovative product design, technological enhancements, and quality assurance. To fulfill the charging station gap in North America, Tesla constructed a network of charging stations across the U.S. and Canada. The company has also built solar power generation plants to provide green energy for these charging stations.

Daimler AG is one of the world's leading manufacturers of commercial vehicles and high-end automobiles. The company has launched a range of passenger cars and commercial vehicles to support the growing EV demand. A few prominent EVs launched by the company include EQC, Smart EQ, GLC F-Cell, and Concept EQV. Moreover, Daimler AG also provides financing, insurance, fleet management, leasing, and innovative electric mobility services.

The electric vehicle market demonstrates an increasingly competitive structure shaped by automotive manufacturers, battery producers, charging infrastructure providers, and software ecosystem participants. Competition is no longer limited to vehicle production alone. Automakers increasingly compete across battery procurement, charging integration, software capability, manufacturing scale, and supply chain resilience. Competitive positioning continues evolving as electrification shifts from early-stage adoption toward cost optimization and operational efficiency.

Established automotive manufacturers continue accelerating investment in dedicated electric vehicle platforms to improve manufacturing efficiency and reduce dependence on internal combustion portfolios. Companies increasingly prioritize modular vehicle architectures that enable multi-model scalability while reducing engineering complexity and production costs. At the same time, several legacy manufacturers continue expanding battery sourcing agreements and regional production facilities to strengthen procurement visibility and align with local manufacturing requirements.

Battery manufacturers remain central to competitive dynamics because battery systems account for a substantial share of electric vehicle production costs. Companies specializing in lithium-ion battery technologies increasingly strengthen long-term supply partnerships with automakers to improve production certainty and secure demand visibility. Localized battery production facilities continue expanding across North America, Europe, and Asia-Pacific to reduce logistics dependence and support regional content requirements.

Charging infrastructure providers are becoming increasingly important participants within the electric vehicle industry. Public charging network operators continue expanding interoperability, charging speed, and network reliability as ownership experience becomes more closely linked to charging accessibility. Automakers increasingly establish partnerships with charging companies to improve convenience and reduce consumer charging concerns.

List of Key Electric Vehicle Companies Profiled

- BMW Group (Germany)

- BYD Company Ltd. (China)

- Daimler AG (Germany)

- Ford Motor Company (U.S.)

- General Motors Company (U.S.)

- Nissan Motor Corporation (Japan)

- Tesla (U.S.)

- Toyota Motor Corporation (Japan)

- Volkswagen AG (Germany)

- Group Renault (France)

Electric Vehicle Industry Key Developments

- March 2025: Japanese automaker Toyota teamed up with oil giant Idemitsu Kosan to construct a large-scale lithium sulfide plant to supply raw materials for Toyota’s all-solid-state EV battery production line. This partnership will provide a reliable supply of raw material to create the EVs of the future.

- March 2025: Hyundai Motor Group commissioned a dedicated electric vehicle manufacturing facility integrating battery module assembly, flexible platform production, and localized supplier networks to enhance cost competitiveness in North America.

- June 2025: Toyota Motor Corporation advanced solid-state battery pilot production targeting higher energy density and faster charging performance, reinforcing long-term electrification strategy beyond hybrid-dominant portfolios.

- January 2024: Tesla expanded its global manufacturing strategy by upgrading battery production capabilities to support next-generation lithium-ion cells, aimed at reducing unit costs and improving energy density across high-volume passenger vehicle platforms.

- April 2024: BYD announced the commercial deployment of advanced blade battery technology across additional export models, strengthening thermal safety performance and extending driving range to support international market expansion.

- September 2024: Volkswagen Group initiated a unified electric vehicle software architecture rollout, consolidating vehicle operating systems to improve over-the-air update capability, feature scalability, and long-term digital revenue generation.

- August 2024: XPeng introduced the Mona M03, a compact (C-segment) battery-electric liftback. It was previewed in June, officially introduced in July, and its first deliveries began on August 30, 2024, with total deliveries reaching 30,000 units by November 2024

- March 2023: Moscow signed a contract with KAMAZ for 1,000 electric buses, with additional plans to purchase another 200 electric buses from GAZ Group. Moscow currently runs 1,055 electric buses on 79 routes. The city also plans to install nearly 200 ultra-fast charging stations for the electric buses, open a second electric bus park in the Mitino district northwest of Moscow, and launch 29 more electric bus routes.

REPORT COVERAGE

The market report provides a detailed analysis and focuses on key aspects, such as leading market players, vehicle type, and leading applications of the product. Besides, the report offers insights into the latest market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market’s growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.97% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type

|

|

By Propulsion Type

|

|

|

By Drive Type

|

|

|

By Range

|

|

|

By Component

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was valued at USD 1023.81 billion in 2026.

The market is likely to register a CAGR of 9.97% during the forecast period (2026-2034).

The Battery Electric Vehicle (BEV) segment is expected to lead the market due to the adoption of pure EVs across the world.

The market size in Asia Pacific stood at USD 480.38 billion in 2025.

BYD, Tesla, and Volkswagen Group are some of the top players in the market.

China dominated the market in terms of sales volume in 2025.

Asia Pacific dominated the electric vehicle market with a market share of 51.78% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us