Thin Client Market Size, Share & Industry Analysis, By Component (Hardware, Software, and Services), By Enterprise Type (Large Enterprises and Small and Medium Enterprises (SMEs)), By End-user (IT and Telecom, BFSI, Healthcare, Industrial, Government, Education, Retail, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

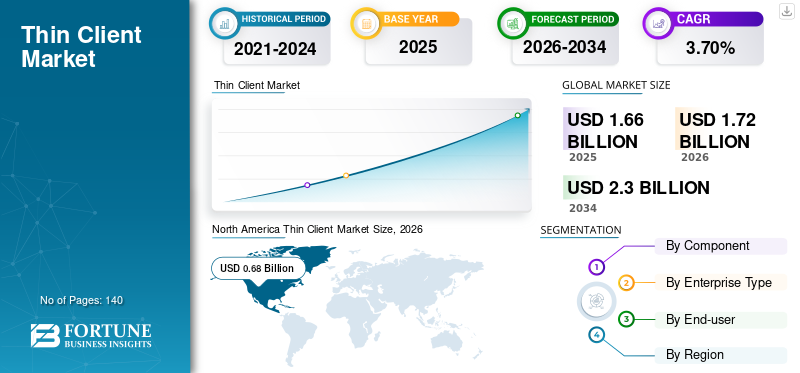

The global thin client market size was estimated at USD 1.66 billion in 2025 and is projected to reach USD 1.72 billion in 2026 to USD 2.30 billion by 2034, growing at a CAGR of 3.70% from 2026 to 2034. North America dominated the thin client market with a market share of 41.08% in 2025.

A thin client refers to a lightweight computing device relying on a central server for most processing and storage functions. The market encompasses the industry focused on devices and solutions operating under a centralized computing model. Typically employing client-server architecture, these devices allow users to access applications and data stored on the server, simplifying maintenance and updates for IT administrators. This market involves the development, manufacturing, and implementation of these devices and associated software, catering to diverse sectors such as IT and telecom, BFSI, healthcare, industrial, government, education, retail, and others. The evolving landscape of remote and flexible work arrangements is driving the demand for these solutions.

Download Free sample to learn more about this report.

Thin Client Market MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.66 billion

- 2026 Market Size: USD 1.72 billion

- 2034 Forecast Market Size: USD 2.30 billion

- CAGR: 3.70% from 2026–2034

- North America dominated the thin client market with a 41.08% share in 2025.

- The hardware segment held the largest market share in 2025.

- The IT & telecom segment is projected to account for 20.0% of the market in 2026.

North American

Valued at USD 0.68 billion in 2025 and projected to reach USD 0.71 billion in 2026.

Europe

Demonstrated steady growth, supported by secure computing adoption and cloud integration.

Asia Pacific

Expected to witness the fastest growth, driven by increasing adoption of cloud solutions.

U.S.

Growth is driven by rising demand for secure remote access and centralized IT infrastructure.

Japan

Increasing digital transformation and cloud adoption are supporting market growth.

Read More

Thin Client Market TRENDS

Incorporation of Edge Computing into Thin Client Solutions to Fuel Market Growth

The trend of integrating edge computing capabilities into these solutions is fueling the market's growth. This strategic evolution arises from the growing demand for swift, decentralized data processing in various business environments. Traditionally reliant on centralized servers, these solutions are adapting by incorporating computing functionalities to meet businesses' real-time analytical needs. This shift enhances the solutions' versatility, expanding their application across various use cases.

Download Free sample to learn more about this report.

For instance, in manufacturing, thin clients with embedded edge capabilities streamline decision-making by processing data from production line sensors, reducing operational delays. Similarly, in healthcare, these solutions enable real-time analysis of patient data at the point of care, facilitating faster and more informed medical decisions.

This trend ensures that these solutions remain crucial for efficient, localized processing while benefiting from centralized management. As businesses increasingly prioritize rapid, real-time insights, the incorporation of edge computing serves as a strategic move, driving the thin client market share by addressing the evolving needs of modern enterprises.

THIN CLIENT MARKET GROWTH FACTORS

Increasing Need to Manage IT Budgets without Compromising Performance to Drive Market Growth

Traditional PCs involve higher upfront expenses due to the need for robust local processing power and storage capacity. In contrast, thin-clients rely on a centralized server for computing tasks, allowing them to have minimal hardware requirements, which results in lower initial costs. For instance, a company planning to upgrade its computer infrastructure might find that deploying these tools requires a lesser upfront investment compared to purchasing traditional PCs. This is particularly beneficial for businesses with a large workforce, where the aggregate savings on hardware costs can be higher. Lower upfront costs also make the solution an appealing option for budget-conscious organizations, especially in sectors including education and healthcare, where large deployments are typical.

As businesses seek to optimize their IT budgets without compromising performance, the cost advantage becomes a significant driver, fueling their adoption and driving the thin client market growth.

RESTRAINING FACTORS

Concerns related to Latency or Interruptions in Accessing Data Hamper Market Growth

Thin-clients rely heavily on a stable and robust network connection to access centralized servers for computing tasks. In scenarios where network connectivity is inconsistent or disrupted, the performance can be adversely affected, leading to operational challenges and potential downtime. For instance, in environments with unreliable internet connections, such as remote or rural areas, the solutions may experience latency issues or disruptions in accessing essential applications and data. This dependency on network reliability can pose a constraint, particularly for businesses operating in regions with inconsistent or limited network infrastructure.

Addressing this restraint involves investing in robust network solutions and considering backup measures to ensure continuous connectivity. Despite advancements in network technologies, the dependence on a reliable network remains a consideration for organizations contemplating the adoption in their computing environments.

SEGMENTATION Analysis

By Component Analysis

Rising Virtualization Advancements to Boost Hardware Segment Growth

Based on component, the market is segmented into hardware, software, and services.

The hardware segment holds the maximum share due to the centralized nature of computing. In its setup, the server assumes the bulk of the computing responsibilities, necessitating robust and powerful hardware to manage multiple simultaneous connections from thin-client terminals effectively. This central server hardware is a critical component that holds a substantial share of the overall hardware costs in the ecosystem.

The software segment is expected to grow at the highest CAGR over the study period. This can be credited to advancements in virtualization technologies that play a crucial role in optimizing resource utilization on centralized servers and enhancing overall performance. The integration of cloud computing and the demand for customization and flexibility in configuration environments further drive the expansion of the software segment.

By Enterprise Type Analysis

Enhanced Operational Efficiency and Centralized Management Capabilities to Increase the Deployment in Large Enterprises

Based on enterprise type, the thin client market is bifurcated into large enterprises and small and medium enterprises (SMEs).

The large enterprises segment holds the maximum share driven by the alignment of the product with centralized management strategies, cost efficiency, enhanced security features, and the ability to support a geographically dispersed workforce. This makes these products a practical and strategic choice for organizations with extensive and complex operational requirements.

The SMEs segment is projected to grow at the highest rate over the study period as they may experience rapid growth or fluctuations in workforce size. The solutions allow for easier and more cost-effective scalability compared to traditional PC setups. This adaptability is essential for SMEs seeking flexible solutions that can evolve with their business requirements.

By End-user Analysis

To know how our report can help streamline your business, Speak to Analyst

Rising Demand for Financial Security and Stability to Boost BFSI Segment Growth

Based on end-users, the market is subdivided into IT and telecom, BFSI, healthcare, industrial, government, education, retail, and others.

The IT and Telecom segment dominated the market accounting for 20.0% market share in 2026. The BFSI segment holds the maximum share owing to the critical emphasis on security, centralized management, and scalability requirements in managing substantial volumes of financial data and transactions. With their resilience on centralized servers, they offer scalability and performance benefits, making them suitable for data-intensive operations of financial services.

The healthcare segment is expected to grow at the highest CAGR over the analysis period. This is driven by the industry’s unique requirements for security, compliance, digitization, flexibility, and cost-effective IT solutions, positioning these solutions as a strategic choice for modernizing healthcare IT infrastructure.

REGIONAL Analysis

By geography, the market has been analyzed across five regions, including North America, South America, Europe, the Middle East & Africa, and Asia Pacific. These regions are further categorized into leading countries.

North America Thin Client Market Size, 2026 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America dominated the market with a valuation of USD 0.68 billion in 2025 and is projected to reach USD 0.71 billion in 2026. North America holds the maximum share, driven by the presence of a majority of key players providing secure and cost-effective computing solutions. The thin client market has responded to the evolving landscape of remote work, with businesses leveraging solutions for secure access to centralized applications and data. Technology partnerships, innovations in virtualization, and a focus on cloud integration characterize the competitive landscape. As the region continues to navigate the changing work dynamics and digital transformation, the market remains a dynamic and influential component of IT infrastructure strategies.

Asia Pacific

Asia Pacific is expected to grow at the highest growth rate due to the region’s increasing adoption of cloud solutions. The market has witnessed robust expansion across diverse industries, including finance, healthcare, and education, driven by a demand for efficient, secure, and cost-effective IT infrastructure. As businesses in the region embrace digital transformation, thin clients offer a compelling solution for centralized management and streamlined operations. Furthermore, a growing emphasis on data security, compliance, and technological advancements is expected to fuel the market expansion during the projected period.

Europe

Europe has demonstrated steady growth in 2022, influenced by the region’s focus on implementing advanced and secure computing solutions. The market players responded to the evolving demands of flexible work arrangements, facilitating secure remote access to centralized applications and data. European businesses are also exploring the integration with cloud computing for extra scalability and operational efficiency.

South America and the Middle East & Africa

The South America and the Middle East & Africa markets are at their nascent stages, where cybersecurity and regulatory concerns are paramount. Thin-clients are gaining traction for their ability to centralize computing, enhance data security, and facilitate compliance adherence.

KEY INDUSTRY PLAYERS

Key Players Launch New Products to Strengthen Market Positioning

Players in this market are actively creating advanced solutions to cater to customer demands. They also focus on enhancing their existing product portfolio to deliver flexible solutions with unique attributes. Furthermore, these major players proactively pursue collaborations, acquisitions, and partnerships to bolster their product offerings and strengthen market positioning.

List of Key Companies Profiled in Thin Client Market:

- HP Development Company, L.P. (U.S.)

- Dell Inc. (U.S.)

- Samsung Electronics (South Korea)

- LG Electronics (South Korea)

- Fujitsu (Japan)

- Centerm (China)

- IGEL Technology (Germany)

- Lenovo (China)

- 10ZiG Technology Inc. (U.S.)

- Praim Srl (U.K.)

KEY INDUSTRY DEVELOPMENTS:

- August 2023 - LG Business Solutions USA launched the 2023 CQ series of clients, emphasizing extended product life, advanced security, robust performance, seamless connectivity, and notable power savings. These clients aim to enhance efficiency and productivity while simplifying expansion for users.

- May 2023 - Altos India revealed a range of advanced workstations in response to the growing demand for high-performance computing solutions in the country. The launch event, attended by Altos India executives, IT professionals, partners, and industry experts, emphasized the company's commitment to providing comprehensive solutions encompassing commercial hardware and integrated software development. Altos India specifically concentrates on Artificial Intelligence (AI), cloud computing, and high-performance computing to address the evolving industry requirements.

- August 2022 - OnLogic introduced the TM120 and TM710 compact fanless PCs equipped with ThinManager software for centralized thin-client and remote server management. In this setup, thin clients would connect to a centralized server to access applications, memory, and data, which would then be delivered to its device.

- July 2022 - Amulet Hotkey unveiled its newest ultra-thin clients, the DX1300 and DX1600, as part of the DX series. The latest DX series additions address the growing need for businesses to facilitate remote work. These enhancements contribute to their Agile Work Environments solutions, empowering workforces to maintain productivity from any location.

- February 2022 - LG Business Solutions USA unveiled a comprehensive range of LG Gram Mobile Thin Client laptops. These laptops, available in 15.6-inch Full HD and 14-inch WXUGA configurations, weighed 2.5 pounds and 2.2 pounds, respectively. Designed for easy deployment and management, the highly protected LG gram Mobile Thin Clients were tailored to accompany a dynamic workforce.

REPORT COVERAGE

The thin client market report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product/service types, and leading product components. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.70% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component

By Enterprise Type

By End-user

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the market is projected to reach USD 2.3 billion by 2034.

In 2025, the market was valued at USD 1.66 billion.

The market is projected to grow at a CAGR of 3.70% during the forecast period.

On the basis of end-user, the BFSI industry is the leading segment in the market.

The increasing need to manage IT budgets without compromising on performance is a key factor driving market growth.

HP Development Company, L.P., Dell Inc., Samsung Electronics, LG Electronics, Fujitsu, Centerm, IGEL Technology, Lenovo, 10ZiG Technology Inc., and Praim Srl are the top players in the market.

North America accounts for the highest share of the global market.

By enterprise type, the SMEs segment is expected to grow at the highest rate during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us