Thin Metals and Foils Market Size, Share & Industry Analysis, By Material Type (Aluminum Foil, Copper Foil, Stainless Steel Foil, Nickel Foil and Others), By Application (Packaging, Electronics & Energy Storage, Automotive & Transportation, Building & Infrastructure and Others), and Regional Forecast, 2025-2032

KEY MARKET INSIGHTS

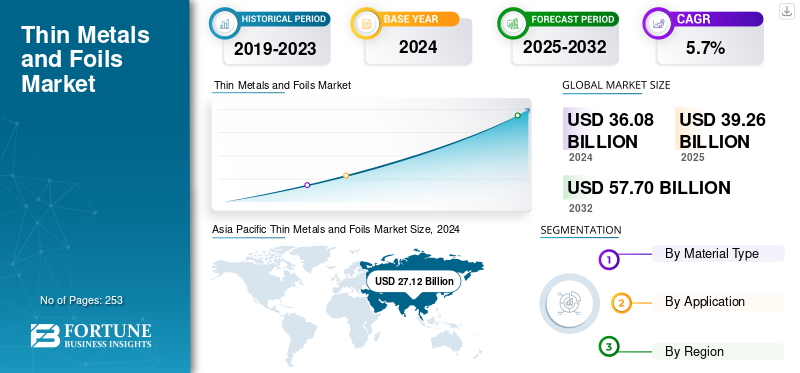

The global thin metals and foils market size was valued at USD 36.08 billion in 2024. The market is projected to grow from USD 39.26 billion in 2025 to USD 57.70 billion by 2032, exhibiting a CAGR of 5.7% during the forecast period. Asia Pacific dominated the global market with a market share of 75.16% in 2024.

Thin metals and foils constitute flat-rolled metallic products supplied as foil, thin strip, or thin sheet. Typically manufactured to very low thicknesses, often ranging from tens of microns to sub-millimeter levels, they are delivered in coils or rolls, slit strips or cut sheets. These materials are employed as functional layers or formed components where properties such as barrier performance, electrical and thermal conductivity, corrosion resistance, formability and lightweight characteristics are essential. The market scope encompasses thin foil and strip products made from various materials, including aluminum, copper, stainless steel, nickel and others, and monitors their consumption across sectors such as packaging, electronics and energy storage, automotive and transportation, building and infrastructure, among other end-use applications. Packaging continues to be a fundamental driver, particularly for aluminum foil, due to its capacity to serve as a robust barrier against moisture, oxygen, light, and aroma when integrated as a layer within multi-material laminates. The expansion of processed foods, ready-to-eat formats, pharmaceutical packaging, and premium personal care products sustains a steady demand for foil, as these industries prioritize shelf-life extension and product protection.

The market is comprised of several major players, including Novelis, UACJ Foil Corporation, Constellium SE, and LOTTE Aluminium Co., Ltd., which are key players at the forefront. A broad portfolio, innovative product launches, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

Thin Metals and Foils Market Key Takeaways

- 2025 Market Size: USD 36.08 billion

- 2026 Market Size: USD 39.26 billion

- 2034 Forecast Market Size: USD 57.70 billion

- CAGR: 5.70% from 2025–2032

- Asia Pacific dominated the market with a 75.16% share in 2024.

- Aluminum Foil dominated the market in 2024.

- Packaging is expected to dominate the market, while Electronics & Energy Storage is projected to account for a 32.0% share in 2025.

North America

Projected to reach USD 3.05 billion in 2025, driven by battery supply chain localization.

Asia Pacific

Valued at USD 27.12 billion in 2024, driven by strong battery and electronics manufacturing.

Europe

Expected to reach USD 5.15 billion in 2025, supported by automotive and battery ecosystem growth.

U.S.

The U.S. market is projected to reach USD 2.17 billion by 2025.

Japan

The Japan market is projected to reach USD 1.95 billion by 2025.

Read More

THIN METALS AND FOILS MARKET TRENDS

Rapid Growth in Battery-Grade Foils and Tighter Performance Specifications is a Prominent Market Trend

The demand for thin metals and foils is progressively driven by electronics and energy storage applications, whereby the consumption of copper foil (serving as the anode current collector) and aluminum foil (serving as the cathode current collector) increases concomitantly with the expansion of Electric Vehicles (EVs) and stationary storage solutions. This development is prompting a shift in the market composition toward higher-specification, defect-sensitive foils, thereby emphasizing the significance of attributes such as thickness uniformity, surface treatment, cleanliness, and mechanical stability, capabilities that underpin premium pricing in contrast to commodity packaging foils.

Consequently, producers are focusing on capacity expansion and technological enhancements that facilitate the production of thinner gauges and ensure more uniform quality at scale. Simultaneously, customers are increasingly emphasizing qualification, traceability, and dependable delivery. Over time, it is anticipated that this trend will accentuate the gap between commoditized foil segments and high-performance foil segments, with suppliers capable of consistently satisfying demanding specifications gaining greater value.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Electrification and Energy-storage Expansion is Key Growth Driver

The primary structural factor driving demand for thin metals and foils is the ongoing expansion of lithium-ion batteries across various sectors, including electric vehicles, stationary energy storage, consumer electronics and power tools. Battery cell architectures irreversibly depend on copper foil and aluminum foil, rendering each additional gigawatt-hour of cell capacity associated with increased foil consumption. This correlation closely links the market to the rate of electric vehicle adoption and grid storage deployment.

Beyond the fundamental growth in demand, electrification enhances the quality and specification requirements for foil products. Battery and electronics foils must adhere to stringent thickness tolerances, surface cleanliness standards and defect control, including the prevention of pinholes, as well as consistent mechanical properties suitable for high-speed coating and winding processes.

Furthermore, the geographic distribution of the product demand is significant. Battery supply chains are expanding most rapidly in the Asia Pacific region, with increasing growth in North America and Europe driven by localization and supply-security initiatives. Such developments foster regional investments in copper and aluminum foil capacities, adherence to qualification cycles with cell manufacturers and the establishment of long-term supply agreements. These factors typically enhance demand visibility and elevate the strategic importance of thin foils within the broader metals value chain. These factors are expected to drive the thin metals and foils market growth.

MARKET RESTRAINTS

Volatility in Metal Input Costs and Margin Pressure across Value Chain May Hamper Market Growth

Thin metals and foils are inherently vulnerable to fluctuations in the prices of primary metals such as aluminum, copper and nickel, as well as to regional premiums and energy costs. Considering that raw metal constitutes a significant component of delivered foil pricing, sudden changes in LME or benchmark prices, along with regional premiums, can lead to temporal mismatches between procurement activities and customer pricing, especially when contracts include delayed pass-through clauses. This discrepancy can reduce margins for rolling mills and converters and increase caution among end customers regarding inventory management.

The energy further exacerbates the constraint and process-intensive nature of manufacturing high-quality foils. Processes such as rolling, annealing, surface treatment and rigorous quality control demand substantial energy consumption and involve sophisticated equipment as during the elevated energy costs or supply disruptions, operating costs can escalate rapidly. For high-specification foils, including those used in batteries and electronics, scrap rates due to defects can incur high costs, thereby necessitating stable operations and meticulous process control to maintain profitability.

MARKET OPPORTUNITIES

Localization, Premiumization and Specification-driven Value Growth is Lucrative Market Opportunity

A significant opportunity exists in the ongoing localization of supply chains for electronics and energy storage, particularly across North America and Europe. As Original Equipment Manufacturers (OEMs) and battery producers prioritize regional sourcing, foil producers and converters that meet qualification standards can secure long-term contracts, foster closer customer relationships and potentially enhance pricing power. Localization often favors suppliers who provide reliability, traceability, and technical support.

Another aspect of opportunity is premiumization, which involves shifting toward higher-value foils. Applications in batteries, electronics, shielding and specialized industrial uses increasingly demand ultra-thin gauges, improved surface qualities, higher purity, tighter tolerances and advanced coatings or treatments. Suppliers investing in process capabilities, such as precision rolling, surface treatments, defect inspection and cleanliness, can capture higher value share, even without dominating overall volume.

Additionally, opportunities exist in functional integration, whereby foils become components of engineered systems rather than simple commodities. Examples include foil-based thermal management laminates, EMI shielding structures and next-generation packaging designs that enhance barrier performance through downgauging or hybrid constructions. In these sectors, innovation and application engineering can differentiate products, diminish price-based competition and enable entry into related high-performance markets within the same thin metals and foils ecosystem.

MARKET CHALLENGES

Margin Pressure From Volatility in Base Metals, Energy Costs and Oversupply Cycles to Hamper Market Growth

The market remains structurally vulnerable to fluctuations in the prices of aluminum, copper, and nickel, as well as regional premiums and energy costs. This volatility results in frequent fluctuations in delivered prices and conversion spreads. Rapid movements in benchmark metals can lead to timing mismatches for producers and converters in pass-through mechanisms. Similarly, buyers may seek to postpone purchases or de-stock, thereby compressing realized margins despite stable shipment volumes.

Meanwhile, aggressive capacity expansions, particularly in copper foil, may occasionally surpass short-term demand growth, leading to price competition and reduced utilization until demand aligns. This cyclicality is intensified in high-spec segments where qualification procedures are lengthy. Consequently, new lines cannot operate at optimal yields immediately, resulting in increased unit costs and heightened margin pressures during periods of demand slowdown. These factors collectively hamper the market growth.

Segmentation Analysis

By Material Type

Aluminum Foil Dominated Market Due to Growing Demand from End-use Industries

Based on material type, the market is segmented into aluminum foil, copper foil, stainless steel foil, nickel foil, and others.

Aluminum foil segment accounted for the largest thin metals and foils market share in 2024. Demand for aluminum foil is driven by packaging and insulation-facing laminates, where barrier performance, lightweighting and cost competitiveness support large-volume consumption. This growth is further reinforced by downgauging and high-barrier flexible formats, while battery cathode current-collector foil constitutes a faster-growing, higher-spec subcategory.

In the copper foil segment, the primary drivers for the growth are electronics and energy storage, particularly lithium-ion batteries, where copper foil serves as a fundamental layer for current collection. Specifications are becoming increasingly stringent, including thinner gauges and improved control over defects. The demand for PCB and flexible circuits remains a steady contributor. Meanwhile, technological advancements and qualification requirements sustain higher pricing levels compared to commodity foils.

Stainless steel foil is primarily used in applications that require corrosion resistance and durability at thin gauges. Such applications include engineered sealing, industrial components, shielding, and specialized uses in buildings or industries. The segment is predominantly influenced by industrial cycles and engineered applications rather than mass packaging. The growing demand is due to favor suppliers capable of providing precision rolling and consistent metallurgical quality.

By Application

To know how our report can help streamline your business, Speak to Analyst

Electronics & Energy Storage Segment to Dominate Due to Higher Adoption

Based on application, the market is classified into packaging, electronics & energy storage, automotive & transportation, building & infrastructure, and others.

The packaging segment is expected to dominate the market. Packaging continues to serve as a fundamental component of volume, primarily influenced by the demand for food and pharmaceutical hygiene, the extension of shelf life, and ongoing adoption of flexible formats that utilize foil as a barrier layer. The growth trajectory is more stable yet increasingly sensitive to price variations, shaped by downgrading, sustainability-driven redesign of structures, and performance requirements set forth by brand owners. Furthermore, it is projected that this segment will grow at a CAGR of 3.2% throughout the specified study period.

Electronics and energy storage constitute the most rapidly expanding sector, driven by the scaling of Electric Vehicles (EVs) and stationary storage systems, alongside increasing electronics content. This directly elevates the demand for copper and aluminum current-collector foil. The growth is further intensified by more stringent specifications, including thinner gauges, surface treatments and reduced defects, which support premium pricing and necessitate capacity investments. Furthermore, the electronics & energy storage segment is anticipated to account for a 32.0% market share by 2025.

Thin Metals and Foils Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Thin Metals and Foils Market Size, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Country and sub-region dynamics across the Asia Pacific are diverse. Asia Pacific held the dominant share in 2023 valuing at USD 26.11 billion and also took the leading share in 2024, with USD 27.12 billion. Asia Pacific continues to serve as the focal point of global growth, given its concentration of battery manufacturing and electronics production. This drives substantial consumption of copper and aluminum foil, alongside swift technological advancements Although large-scale capacity expansions and fierce competition may induce periods of price pressure, the region maintains the most robust volume momentum.

China Thin Metals and Foils Market

In 2025, the China market is estimated to reach USD 22.90 billion. China serves as the global hub for battery and electronics manufacturing, positioning copper foil and battery-grade aluminum foil as primary growth sectors through aggressive capacity expansions. Intense competition drives rapid advancements in gauge reduction, surface treatment, and defect inspection to meet high-volume qualification standards. Pricing and profit margins may experience cyclical fluctuations, as capacity expansions occasionally surpass demand. However, medium-term volume prospects remain robust. Vertical integration and strategic proximity to cathode, anode and cell manufacturers often influence supplier selection, supporting long-term market share gains.

To know how our report can help streamline your business, Speak to Analyst

Japan Thin Metals and Foils Market

In 2025, the Japan market is estimated to reach USD 1.95 billion. Japan represents a mature market characterized by a significant focus on high-specification electronics and advanced materials. This supports premium foils and enforces rigorous process controls. While volume growth is steady, the density of value remains elevated due to engineered applications and stringent quality standards.

India Thin Metals and Foils Market

In 2025, the Japan market is estimated to reach USD 2.01 billion. India's current demand is predominantly oriented toward the packaging and construction sectors, bolstered by increasing consumer expenditure and expanding converting capacities. Concurrently, demand within the electronics and battery sectors is accelerating from a smaller initial base. Strategies such as import substitution and new manufacturing incentives are expected to enhance local sourcing of foil stock and converter-ready materials gradually.

North America

The market in North America is estimated to reach USD 3.05 billion in 2025 and secure the position of the third-largest region in the market. In North America, growth is increasingly influenced by the localization of the battery supply chain and the qualification of higher-specification foils, thereby supporting premium market segments alongside consistent demand for packaging and insulation. Tariffs and policy dynamics, along with regional premiums, further incentivize nearshoring and supply diversification across the U.S., Canada, and Mexico.

U.S. Thin Metals and Foils Market

The U.S. dominates the region and is estimated to reach USD 2.17 billion in 2025. In the U.S., the most significant influence stems from the localization of battery and electronics manufacturing, coupled with an extensive packaging conversion base, which sustains a qualification-led growth trajectory for copper and battery-grade aluminum foils.

Europe

During the forecast period, Europe is projected to record a growth rate of 3.7% and reach a valuation of USD 5.15 billion by 2025. At the country level, Germany stands out as the largest and most influential market within Europe. Germany exhibits a pronounced inclination toward automotive and engineered industrial demand, thereby supporting stainless steel and higher-specification foils as well as packaging applications. The expansion of battery ecosystem enhances demand for qualified copper and aluminum foils. However, the rate of ramp-up is contingent upon gigafactory utilization levels and existing supply agreements.

U.K. Thin Metals and Foils Market

In 2025, the U.K. market is estimated to reach USD 0.63 billion. The U.K. market is increasingly focused on packaging and specialized converting, with comparatively lower direct exposure to large-scale battery foil demand than Germany. Factors such as import pricing, logistics and converter-led purchasing cycles contribute to near-term volatility, especially in the specialty foil segment. Sustainability-driven redesign initiatives in packaging may lead to a shift toward optimized structures that maintain essential barrier performance standards.

France Thin Metals and Foils Market

In 2025, the France market is estimated to reach USD 0.94 billion. France exhibits a comprehensive packaging industry, encompassing regulated formats, and is also expanding its connection to energy-transition sectors. This collaboration fosters a gradual increase in the demand for copper and aluminum foil. Customers are increasingly prioritizing compliance, traceability, and sustainability reporting, thereby favoring suppliers who can provide transparent documentation of their ecological footprint and sourcing practices.

South America and Middle East & Africa

In South America, demand is primarily driven by consumer packaging and construction-related applications. The region's exposure to advanced electronics is comparatively limited relative to North America, and the European Union. Currency volatility and dependence on imports for specialty foils are critical factors influencing pricing stability and supply consistency for converters and end users. Brazil stands as the largest regional market, characterized by a substantial packaging conversion base and significant demand linked to building activities for insulation and barrier facings.

The growth of the Middle East & Africa region is primarily driven by developments in building and infrastructure, including insulation facings and reflective barriers, as well as an increasing demand for packaged foods that supports the use of foil laminates. Trade flows, logistics costs, and the development of local converting capabilities influence the delivered pricing and the acceleration towards regional self-sufficiency. In the Middle East & Africa, the GCC demonstrates a significant inclination toward construction and infrastructure activities, characterized by substantial utilization of insulation facings, reflective barriers, and foil laminates associated with HVAC systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships, Coupled with the Capacity Expansion of Key Companies Support their Leading Position

Technological advancements in ultra-thin rolling and deposition processes, combined with enhanced quality assurance measures and increasingly regionalized supply networks, are shaping competitive advantages within the global market for thin metals and foils. The industry landscape remains moderately fragmented, characterized by a mix of large, diversified flat-rolled metal companies, particularly those specializing in aluminum foil and foilstock, and specialized foil manufacturers, notably in copper foil and precision foils.

Novelis Inc., UACJ Foil Corporation, Constellium SE, LOTTE Aluminium Co., Ltd., and SK Nexilis are some of the dominating players in the market. Across various regions, firms are enhancing their competitive standing by expanding capacity near key demand centers, upgrading inspection and surface treatment facilities, and forming strategic partnerships along the battery and packaging value chains to secure long-term supply agreements. These efforts aim to enhance resilience against trade disruptions and logistical challenges.

LIST OF KEY THIN METALS AND FOILS COMPANIES PROFILED

- Novelis Inc. (U.S.)

- UACJ Foil Corporation (Japan)

- Constellium SE (France)

- LOTTE Aluminium Co. Ltd. (South Korea)

- SK Nexilis (South Korea)

- LOTTE ENERGY MATERIALS Corporation (South Korea)

- Mitsui Mining & Smelting (Japan)

- JX Advanced Metals (Japan)

- Guangdong Jiayuan Technology (China)

- Nippon Steel Chemical & Material (Japan)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Constellium inaugurates a new finishing line at the Singen plant. This milestone marks the completion of a USD 35 million investment in partnership with Lotte Infracell to produce high-quality aluminium foil stock for battery applications in Europe. The new lines enhance the capacity to supply foil used in EV battery markets and other high-performance segments, featuring advanced edge trimming and packing capabilities, as well as sustainability enhancements such as onsite solar-generated power.

- April 2025: Novelis opened a new Ulsan Aluminum Recycling Center in South Korea, with an annual capacity of 100,000 tons of low-carbon aluminum, thereby enhancing the recycled aluminum feedstock. While the facility primarily targets beverage, automotive, and specialty products, the increased availability of recycled aluminum supports Novelis’s ability to supply high-recycled-content thin foil and sheet products globally.

- September 2023: Lotte Energy Materials Corp. has announced its plans to build a copper foil plant in the US to fulfill North America's growing demand for battery components from electric vehicle makers. The South Korean battery materials manufacturer has applied to the Delaware state government to establish its U.S. subsidiary, and the application review is expected to be processed within weeks. After approval, Lotte will start building the copper foil plant, with potential locations in Kentucky, Michigan, Tennessee, and Georgia. The move aims to expand Lotte's operations and meet the growing demand for electric vehicles in the U.S.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 5.7% from 2025-2032 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Material Type, Application, and Region |

|

By Material Type |

· Aluminum Foil · Copper Foil · Stainless Steel Foil · Nickel Foil · Others |

|

By Application |

· Packaging · Electronics & Energy Storage · Automotive & Transportation · Building & Infrastructure · Others |

|

By Region |

· North America (By Material Type, Application, and Country) o U.S. (By Application) o Canada (By Application) o Mexico (By Application) · Europe (By Material Type, Application, and Country) o Germany (By Application) o U.K. (By Application) o France (By Application) o Russia (By Application) o Rest of Europe (By Application) · Asia Pacific (By Material Type, Application, and Country) o China (By Application) o India (By Application) o Japan (By Application) o South Korea (By Application) o Southeast Asia (By Application) o Rest of Asia Pacific (By Application) · South America (By Material Type, Application, and Country) o Brazil (By Application) o Argentina (By Application) o Rest of South America (By Application) · Middle East & Africa (By Material Type, Application, and Country) o GCC (By Application) o South Africa (By Application) o Rest of Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 36.08 billion in 2024 and is projected to reach USD 57.70 billion by 2032.

In 2024, the market value stood at USD 27.12 billion.

The market is expected to exhibit a CAGR of 5.7% during the forecast period of 2025-2032.

The Aluminum Foil segment led the market by Material Type.

The increasing demand from packaging applications is driving the market.

Novelis Inc., UACJ Foil Corporation, Constellium SE, LOTTE Aluminium Co., Ltd., and SK Nexilis are some of the prominent players in the market.

Asia Pacific dominated the market in 2024.

Higher-barrier packaging and hygiene-led consumption of foil structures are expected to favor the product adoption.

- 2019-2032

- 2024

- 2019-2023

- 253

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us