Pet Care Market Size, Share & Industry Analysis, By Product (Pet Food Products {Dry, Wet, and Treats}, Veterinary Care, and Others), By Pet Type (Dog, Cat, and Others), By Distribution Channel (Online and Offline), and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

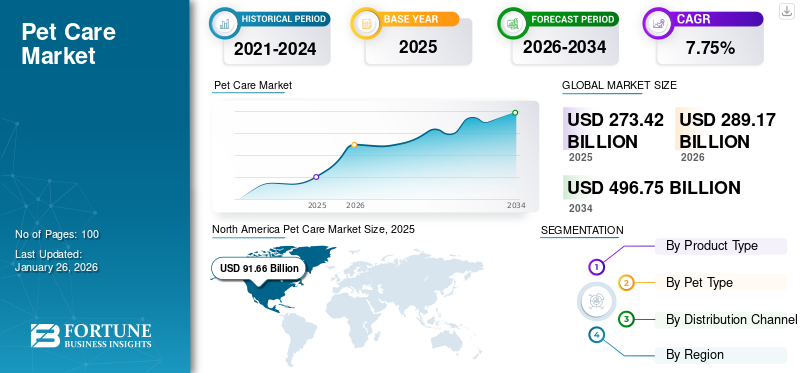

Pet Care Market Size and Future Outlook

The global pet care market size was valued at USD 273.42 billion in 2025. The market is projected to grow from USD 289.17 billion in 2026 to USD 499.06 billion by 2034, exhibiting a CAGR of 7.06% during the forecast period. North America dominated the pet care market with a market share of 33.51% in 2025.

The global pet care industry includes a range of items, including treats, toys, nutritional supplements, grooming products, and leashes. These products are developed to maintain the safety and health of various pets. The growing knowledge regarding the overall well-being of domesticated animals using various products, through online blogs and social media, triggers global market growth. The key companies in the global market include Central Garden & Pet, Spectrum Brands, KONG Company, and The Orvis Company, Inc.

Download Free sample to learn more about this report.

PET CARE MARKET TRENDS

Increasing Interest in Smart Pet Care Products & Customization to Trigger Market Expansion

Tech-savvy consumers worldwide are highly interested in technologically advanced products, including smart pet care items such as automatic litter boxes, pet health monitors, GPS pet trackers, and smart feeders. These products assist in efficient pet management, which boosts their adoption. Furthermore, rising consumer preference for customized products such as engraved collars, personalized bowls, and custom-fitted harnesses is a key global pet care market trend. Increasing income level is resulting in owners spending more on these personalized products.

MARKET DYNAMICS

MARKET DRIVERS

Rising Pet Humanization & Pet Parenting to Increase Product Demand

Consciousness regarding animal welfare and the mental health advantages of pets is increasing the number of individuals throughout countries adopting pets. For instance, according to the American Pet Products Association (APPA), a U.S.-based trade association, households owning at least one pet increased from 82 million in 2023 to 94 million in 2025. A rising affectionate bond with pets results in owners spending on various products for their pet’s comfort, driving global market expansion.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Growing Prevalence of Animal-Borne Diseases to Hamper Market Growth

Increasing cases of animal-borne diseases, including parasitic infections, rabies, and toxoplasmosis, hamper the global pet care market growth. These health problems can be spread to humans through close contact with pets. This factor can discourage individuals from adopting pets, decreasing product demand. Families with elderly individuals or kids are especially more conscious about these infections and diseases, which can limit the pet adoption rate in the near term.

MARKET OPPORTUNITIES

Growing Interest in Sustainable Products to Provide Growth Opportunities

Recent years have witnessed a rising consumer inclination toward sustainable and eco-friendly products, notably among youth, owing to heightened environmental knowledge. This factor also fuels demand for organic pet food items, chemical-free pet grooming sprays, natural rubber pet toys, bamboo-based pet mats, and leashes featuring recycled plastics. Industry participants can prioritize developing these products to escalate sales among eco-conscious end users.

MARKET CHALLENGES

High Cost of Luxury Pet Care Products to Limit Product Sales

The high cost of luxury pet care products, including designer collars, high-end pet jewelry, premium pet travel crates, and limited-edition toy hampers, drives sales among middle-income pet owners with limited budgets. In addition, unorganized players provide low-grade pet care products at low prices owing to lower overhead costs. This factor triggers price competition for organized companies and limits their growth.

Segmentation Analysis

By Product

Essential Nature of the Product & Focus on Nutrition to Trigger Pet Food Products Sales

By product, the market is segmented into pet food products (dry, wet, and treats), veterinary care, and others.

The pet food products (dry, wet, and treats) segment is projected to dominate the market with a share of 52.60% in 2025. The segment is projected to grow at a CAGR of 7.00% from 2026 to 2034. This includes various kinds of food items, such as dry food with a long shelf life, wet food that is easy to digest, and pet treats, including dental chews and snacks. These are essential items required multiple times daily, unlike their counterparts. Moreover, rising knowledge about pet nutrition is driving spending on branded food items, favoring segmental growth.

The other segment is the fastest growing at a rate of 7.68% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Pet Type

High Pet Dog Adoption & Greater Food Consumption to Support Segmental Growth

By pet type, the market is divided into dogs, cats, and others.

The dog segment is projected to dominate the market with a share of 48.09% in 2025. The segment is projected to grow at a CAGR of 7.57% from 2026 to 2034. Higher adoption of dogs as pets than their counterparts, owing to their trainability and loyalty, favors segmental expansion. Furthermore, large breeds of dogs require more food compared to smaller pets, which fuels spending on them.

The others segment is projected to grow at the second-fastest CAGR of 6.85% from 2026 to 2034.

By Distribution Channel

Strong Presence of Numerous Veterinary Clinics and Pet Stores Boosts the Offline Segment’s Expansion

Based on the distribution channel, the market is bifurcated into online and offline.

The offline segment is projected to dominate the market with a share of 73.00% in 2025. The presence of numerous veterinary clinics and pet stores across countries offering a variety of services and items for pet management contributes to the segment’s growth. Moreover, these retailers meet the immediate requirement for products that are frequently needed, such as hygiene and food items.

The online segment is projected to grow at the second-fastest CAGR of 3.71% from 2026 to 2034.

Pet Care Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Pet Care Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The market in North America reached USD 91.66 billion in 2025, representing 33.52% of total market revenue, and is projected to reach USD 96.67 billion in 2026. A sizable number of households owning cats or dogs in countries such as Canada and the U.S, which escalates product sales. Advanced veterinary services across the region further drive market growth. In addition, omnichannel expansion is expected to accelerate online sales in the forthcoming years.

U.S. Pet Care Market

The U.S. market size reached USD 75.55 billion in 2025. The U.S. market accounted for around 27.63% of the global market sales. Numerous individuals throughout the country with high disposable income trigger spending on pet care products from premium brands, supporting the U.S market expansion. In addition, several technologically advanced and modern end users prefer smart pet care products in the country.

Europe

Europe contributed approximately USD 77.83 billion to the global market in 2025, accounting for 28.47% share, and is expected to reach USD 82.94 billion in 2026. Sustainability consciousness is rapidly growing throughout European nations, which is increasing the adoption of products including biodegradable cat litter, organic pet shampoos, recycled material toys, and plant-based harnesses. In addition, a well-established retail ecosystem, including numerous supermarkets and pet shops, ensures product availability.

U.K Pet Care Market

The U.K. market in 2025 reached around USD 21.91 billion, representing approximately 7.32% of global market revenues.

Germany Pet Care Market

Germany’s market was valued at USD 20.01 billion in 2025, equivalent to around 8.01% of global sales.

Asia Pacific

The Asia Pacific market is projected to grow at a CAGR of 7.24% from 2026 to 2034. The region exhibited a global market share of 20.67%, with a market size valued at USD 56.51 billion in 2025. The rising trend of pet insurance in Asian countries is resulting in owners opting for better veterinary services in the region. Furthermore, the increasing disposable income in countries such as Indonesia, Vietnam, and India is expected to fuel the purchase of branded pet products in the coming years.

China Pet Care Market

The Chinese market in 2025 held at USD 22.15 billion, accounting for roughly 8.10% of global market revenues.

India Pet Care Market

India’s market is projected to be one of the largest worldwide, with revenues accounting for USD 14.80 billion in 2025, representing roughly 5.41% of the global market.

Japan Pet Care Market

The Japanese market in 2025 accounted for USD 10.74 billion, roughly 3.93% of global market revenues.

South America and the Middle East & Africa

Middle East & Africa maintained a strong presence in the global market, reaching USD 17 billion in 2025, accounting for 6.22% share, and is expected to reach USD 17.7 billion in 2026. The South America market in 2025 was valued at USD 30.41 billion. Younger generations in the region are increasingly adopting cats and dogs owing to social media influence and the companionship benefits. In the Middle East & African market, South Africa reached a market value of USD 4.98 billion in 2025. Urban security issues have led to several households in the country adopting dogs for home safety purposes, which escalates demand for pet products and services.

UAE Pet Care Market

The UAE market was valued at USD 2.20 billion in 2025, accounting for roughly 0.80% of the global market revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Expanding Product Portfolio & Offering Products Online to Strengthen Market Positioning

The key players operating in the global market include Central Garden & Pet, Spectrum Brands, KONG Company, and The Orvis Company, Inc. Manufacturers develop a varied product portfolio encompassing food items, accessories, and supplements to fulfill the requirements of several consumers. Collaborating with established e-commerce businesses can further help them boost sales. Furthermore, prioritizing research and development can help manufacturers in developing innovative pet care products.

LIST OF KEY PET CARE COMPANIES PROFILED

- Central Garden & Pet (U.S.)

- The Orvis Company, Inc. (U.S.)

- Spectrum Brands (U.S.)

- KONG Company (U.S)

- Canada Pooch (Canada)

- Moshiqa (U.S.)

- Jolly Pets (U.S.)

- Coastal Pet Products (U.S.)

- Doskocil Manufacturing Company, Inc. (Petmate) (U.S.)

- Radio Systems Corporation (PetSafe Brands) (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2025: Doskocil Manufacturing Company, Inc. (Petmate), a U.S.-based pet products company, celebrated its 65th anniversary at the Global Pet Expo, an annual trade show, by displaying its products.

- May 2024: Dogtopia, a U.S.-based dog wellness company, collaborated with KONG Company, a U.S.-based pet supplies company, for an initiative to promote pet wellness.

- March 2024: Radio Systems Corporation, a U.S.-based pet care products company, rebranded to PetSafe Brands. The name change reflects its emphasis on innovative pet supplies.

- March 2024: Coastal Pet Products, a U.S.-based pet care company, unveiled its new website incorporating user-friendly features.

- August 2023: Spectrum Brands, a U.S.-based consumer products company, unveiled its new product Meowee! Cat treats. The new product is free from artificial colors.

REPORT COVERAGE

The global pet care market analysis provides an in-depth study of market insights, size, and forecast by distribution channel, as well as all other market segments included in the report. In addition, the report outlooks market dynamics and market trends expected to drive the market in the forecast period. The report on the market includes information on the technological advancements, new launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.06% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Pet Type, Distribution Channel, and Region |

| By Product |

|

| By Pet Type |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 273.42 billion in 2025 and is projected to reach USD 499.06 billion by 2034.

In 2025, the North American market value stood at USD 91.65 billion.

At a CAGR of 7.06%, the global market is forecasted to grow during the forecast period.

By product, the pet food products segment is projected to hold the leading global market share throughout the forecast period.

Rising pet humanization & pet parenting to increase product demand.

Central Garden & Pet, Spectrum Brands, KONG Company, and The Orvis Company, Inc. are among the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 277

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us