Ultra-Fast EV Batteries Market Size, Share & Industry Analysis, By Vehicle Type (Cars, Vans, Buses, Trucks, and 2 & 3 Wheelers), By Battery Type (Lithium Iron Phosphate, Nickel Manganese Cobalt, Nickel Cobalt Aluminum, and Others), By Charging Capability (Less than 10 minutes charging, 10-20 minutes charging, and 20-30 minutes charging), By Battery Capacity (Less than 50 kWh, 50-100 kWh, and Above 100 kWh), By Component (Cathode Materials, Anode Materials, Electrolytes, Separators, Battery Management Systems, Thermal Management Systems, and Others), and Regional Forecasts, 2026-2034

Ultra-Fast EV Batteries Market Size and Future Outlook

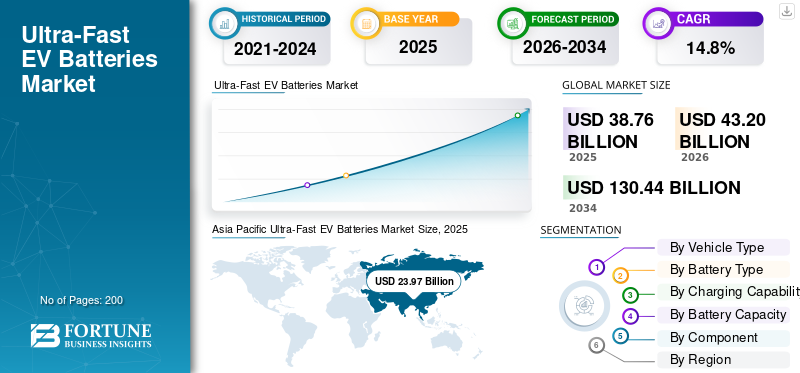

The global ultra-fast EV batteries market size was valued at USD 38.76 billion in 2025. The market is projected to grow from USD 43.20 billion in 2026 to USD 130.44 billion by 2034, exhibiting a CAGR of 14.8% during the forecast period. Asia Pacific dominated the ultra-fast ev batteries market with a market share of 61.84% in 2025.

The global market represents the part of the electric vehicle EV battery industry focused on packs and cells designed for faster charging, high power acceptance, stronger thermal control, and stable performance under repeated rapid charging cycles. In practical terms, this market is tied to vehicles that can use higher-power public chargers and battery systems optimized for short charging windows, better charging capabilities, and safer heat management. Its applications span passenger cars, electric vans, buses, trucks, and selected premium or commercial platforms that depend on reduced downtime and dependable route planning. The market also includes enabling subsystems such as battery management systems, advanced cooling solutions, and chemistry improvements that support repeated high-rate charging.

The industry is evolving through a mix of cost pressure and performance gains. The IEA says global electric car sales exceeded 17 million in 2024, battery demand in the energy sector reached 1 TWh, and LFP now supplies almost half of the global electric car market. That shift matters as improved battery chemistry is making lower-cost solutions viable for high-performance charging, while companies continue to invest in next-generation architectures and solid state batteries for the long term. On the demand side, wider charging infrastructure, stronger policy support, and rising consumer focus on charging speeds are expanding the growth opportunity for ultra-fast charging batteries. Demand is also widening beyond BEVs to some plug-in hybrid electric vehicles PHEVs, although BEVs remain the main value driver. In this market, market share is increasingly shaped by charging readiness, local supply chains, and the pace of battery production ramp-ups compared to the previous year.

Key players such as CATL and BYD are responding by commercializing higher-C-rate cells, localizing factories, and pairing vehicle launches with charging-network expansion. CATL launched its Shenxing 4C LFP battery, while BYD introduced a megawatt-class platform aimed at five-minute range recovery in mass-produced EVs. Those moves show how battery manufacturers are tying product innovation directly to ecosystem control.

Download Free sample to learn more about this report.

ULTRA-FAST EV BATTERIES MARKET TRENDS

Shift Toward Charging-Time-Centric Performance Positioning is a Key Trend

One clear market trend is the shift from talking only about range to talking about minutes-to-charge. Automakers and cell suppliers now market platforms around how quickly drivers can recover practical range, not just how far a battery goes. That trend is pushing investment into cell architecture, cooling, power electronics, and software coordination. It also makes ultra-fast performance easier for consumers to compare across brands, raising competition around real-world charging experience.

- For instance, in March 2025, BYD announced that its latest platform could deliver 400 km of range from 5 minutes of charging, turning charging time itself into a central sales message.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of High-Power Charging Infrastructure Driving Adoption of Ultra-Fast EV Batteries

The strongest ultra-fast EV batteries market growth driver is the spread of high-power charging corridors and urban fast-charging hubs. As more public chargers move into higher-power categories, automakers and suppliers have a clearer reason to deploy batteries engineered for rapid energy intake. This supports faster charging, reduces range anxiety, and improves the commercial case for higher-value packs with stronger thermal controls and smarter software. In simple terms, better infrastructure makes advanced batteries easier to sell and easier to use.

- For instance, in 2025, the IEA reported that the EU had more than 77,000 ultra-fast chargers, while China continued to lead fast-charger deployment, directly supporting batteries built for shorter charging stops.

MARKET RESTRAINTS

Thermal Stress and Degradation Risks Limiting Ultra-Fast Charging Adoption

Ultra-fast charging places heavy stress on cells, pack design, and cooling systems. If a battery cannot manage heat, lithium plating and life-cycle loss become harder to control. That raises costs for materials, pack engineering, and validation, especially in lower-priced EV segments. As a result, not every EV platform can justify ultra-fast readiness, which slows broader market penetration and keeps some vehicle lines on slower or mid-speed charging architectures.

- For instance, in March 2024, Samsung SDI highlighted that reducing charge time requires controlling how lithium ions move quickly through the cell, underscoring the technical limits behind fast-charging performance.

MARKET OPPORTUNITIES

Cost-Effective LFP Advancements Unlocking Wider Market Potential

A major opportunity lies in combining lower-cost LFP chemistry with improving fast-charge performance. That widens adoption beyond premium EVs and creates room for mass-market cars, vans, and fleet vehicles to enter the ultra-fast segment. As cell makers improve energy density and rate capability, LFP can support a broader base of affordable products, giving suppliers a path to higher volume without relying only on nickel-rich premium chemistries.

- For instance, in August 2023, CATL launched Shenxing, describing it as the first 4C superfast-charging LFP battery capable of adding about 400 km of range in 10 minutes.

MARKET CHALLENGES

Supply Chain Concentration and Material Dependency Constraints Creates Market Challenges

The market still faces a supply-side challenge as battery production and critical processing remain concentrated in a few geographies and supplier groups. That concentration can slow localization plans, complicate procurement, and expose manufacturers to price or policy shocks. For ultra-fast products, the challenge is sharper as higher-rate batteries need tighter quality control, specialized materials, and advanced manufacturing consistency.

- For instance, in 2025, the IEA noted that LFP supply chains are more concentrated than nickel-based battery supply chains, highlighting the sourcing and resilience challenge behind rapid scale-up

Segmentation Analysis

By Vehicle Type

Cars Dominate as Passenger EV Volumes Remain Far Ahead of Every Other Vehicle Class

On the basis of vehicle type, the market is segmented into cars, vans, buses, trucks, and 2 & 3 wheelers.

Cars lead this market as passenger EVs account for the largest installed base, the broadest model pipeline, and the fastest charging-network utilization. They also sit at the center of consumer expectations around convenience, making ultra-fast capability more valuable. Commercial vehicles matter for growth, but cars still absorb the largest share of advanced battery value due to scale, model diversity, and infrastructure access.

- For instance, in 2024, the IEA said electric car sales exceeded 17 million globally, confirming that passenger vehicles remain the core volume engine for advanced EV battery demand.

The trucks segment is expected to grow at a CAGR of 23.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Battery Type

Lithium Iron Phosphate Dominates as it Combines Cost Efficiency with Improving Fast-Charge Performance

On the basis of battery type, the market is segmented into lithium iron phosphate, nickel manganese cobalt, nickel cobalt aluminum, and others.

Lithium iron phosphate segment leads globally as it offers a practical balance of price, safety, and improving charge-rate capability. IEA data show it now supplies almost half the global electric car market, supported especially by China. As ultra-fast designs improve, LFP is moving from a value chemistry to a mainstream fast-charge option, making it the strongest global segment by value in broad-market deployment.

- For instance, in 2025, the IEA said LFP batteries supplied almost half of the global electric car market, up sharply from less than 10% in 2020.

Nickel manganese cobalt segment is expected to grow at a CAGR of 14.4% over the forecast period.

By Charging Capability

10-20 Minutes Charging Leads as it Offers the Best Balance Between Performance, Cost, and Pack Durability

On the basis of charging capability, the market is segmented into less than 10 minutes charging, 10-20 minutes charging, and 20-30 minutes charging.

The 10-20 minutes charging range is the most commercially realistic charging band today. It is fast enough to materially improve user convenience, but not so extreme that it forces every program into the cost and engineering burden of sub-10-minute charging. That makes it the strongest near-term value segment for mainstream EV programs, especially where operators want better usability without overdesigning the battery system.

- For instance, in 2025, Samsung SDI highlighted premium EV battery technology capable of charging to 80% in 20 minutes, showing why this band is practical and commercially relevant.

The less than 10 minutes charging segment is expected to grow at a CAGR of 18.5% over the forecast period.

By Battery Capacity

50-100 kWh Dominates as it Fits the Largest Part of the Global Passenger EV Industry

On the basis of battery capacity, the market is segmented into less than 50 kwh, 50-100 kwh, and above 100 kwh.

The 50-100 kWh class matches the needs of mainstream passenger EVs, where demand is highest and charging convenience matters most. Smaller packs have lower value and more limited long-range appeal, while larger packs are concentrated in heavier or premium vehicles. As a result, the middle band captures the best mix of volume, pricing, and charging relevance in the global market.

- For instance, in 2025, the IEA described electric cars as the main driver of battery demand, supporting the outlook that mid-sized passenger-car battery packs remain the core value segment.

The above 100 kWh segment is expected to grow at a CAGR of 17.3% over the forecast period.

By Component

Cathode Materials Dominate as they Remain the Most Value-Intensive Battery Component Group

On the basis of component, the market is segmented into cathode materials, anode materials, electrolytes, separators, battery management systems, thermal management systems, and others.

Cathode materials lead as they carry a large ultra-fast EV batteries market share of cell cost and directly determine energy density, rate capability, and chemistry pathway. Whether the pack uses LFP or nickel-based chemistry, cathode choice heavily shapes performance and economics. In ultra-fast batteries, cathode formulation is especially important as it affects how quickly energy can move while preserving safety and cycle life.

- For instance, in 2024, LG Energy Solution signed long-term agreements for LFP cathode materials as part of supply-chain preparation, showing how central cathodes remain to battery strategy.

Thermal management systems segment is expected to grow at a CAGR of 19.8% over the forecast period.

Ultra-Fast EV Batteries Market Regional Outlook

By region, the global market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Ultra-Fast EV Batteries Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 23.97 billion, and also maintained the leading share in 2024 with USD 18.52 billion. Asia Pacific’s dominance is led by its broad battery manufacturing base, strong chemistry leadership, and faster charger rollout led by China. The region benefits from local scale across cells, packs, materials, and vehicles, which lowers costs and accelerates commercialization. It also leads in buses, trucks, and two- and three-wheelers, giving suppliers wider learning cycles. That makes Asia Pacific the center of both cost-driven LFP expansion and premium fast-charging innovation.

- For instance, in March 2025, BYD launched a platform with 1,000 kW charging power and 400 km of range added in 5 minutes, underlining Asia Pacific’s lead in charging-speed innovation.

China Ultra-Fast EV Batteries Market

China’s market is projected to be one of the largest globally, with 2025 revenues recorded at around USD 17.35 billion, representing roughly 44.8% of the global market.

India Ultra-Fast EV Batteries Market

The Indian market in 2025 was valued at around USD 0.91 billion, accounting for roughly 2.4% of global revenues.

Europe

Europe is estimated to reach USD 9.30 billion in 2026 and secure the position of the second-largest region in the market. Europe should expand through tighter emissions rules, denser public charging, and demand for practical fast-charging passenger EVs. The region remains important for nickel-rich chemistries, but LFP is gaining share as affordability becomes more critical. Europe also benefits from an improving ultra-fast charger base and growing local battery capacity.

Germany Ultra-Fast EV Batteries Market

The German market in 2025 was valued at around USD 2.47 billion, accounting for roughly 6.4% of global revenues.

U.K. Ultra-Fast EV Batteries Market

The U.K. market in 2025 was valued at around USD 1.96 billion, accounting for roughly 5.1% of global revenues.

North America

North America is projected to record a growth rate of 15.1% in the coming years, and reach a valuation of USD 5.31 billion by 2026. The market in North America is expected to grow on the back of corridor charging investment, rising ZEV penetration, and stronger localization of cell supply. The U.S. still has policy uncertainty, but NEVI and related corridor programs support long-distance charging buildout. Canada adds momentum through rising ZEV adoption. In the U.S., the market appears promising in premium and larger-vehicle segments, where pack value is higher and ultra-fast capability is easier to justify.

U.S. Ultra-Fast EV Batteries Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was analytically approximated at around USD 3.51 billion in 2025, representing roughly 11.9% of global market.

Latin America

Latin America is anticipated to grow from a smaller base, supported by import-led EV adoption, improving policy visibility, and rising fleet electrification. Brazil stands out as plug-in sales expanded sharply in 2024, while public and fleet use cases can support fast-charging battery demand in selected corridors and urban markets.

Middle East & Africa

The Middle East & Africa market is estimated to grow through premium EV imports, state-backed charging plans, and fleet modernization. The Gulf has an advantage as charging investment can be coordinated faster, while other markets will grow more gradually. UAE policy support and Saudi fast-charger deployment create the clearest near-term momentum.

COMPETITIVE LANDSCAPE

Key Industry Players

Scale, Chemistry, and Charging Integration Shape Market Competition

Competition in the global ultra-fast EV batteries market is centered on who can combine chemistry, manufacturing scale, vehicle integration, and charging ecosystem access most effectively. CATL, BYD, LG Energy Solution, Panasonic Energy, Samsung SDI, SK On, ACC, Northvolt, Gotion, EVE Energy and others are competing through a mix of plant expansion, OEM partnerships, higher-rate cell design, and localization. The market is not won by cell performance alone. Companies now seek advantage through full-system execution; resilient materials sourcing, regional factory footprints, software-led controls, improved cooling, and coordination with OEM platforms and public charging networks. That is why leadership in battery technology, battery type selection, and production scale matters as much as pure lab performance.

A second competitive theme is chemistry diversification. IEA data show that LFP has become a major global force, while nickel-based chemistries still retain strong positions in the U.S. and Europe. As a result, companies are avoiding one-chemistry dependence. Some are expanding lithium iron phosphate batteries for affordable mass-market vehicles, while others are pushing premium nickel-rich cells or advanced roadmaps in solid state batteries. This is creating a two-track market: high-volume affordability on one side, and high-energy, high-speed premium systems on the other. In both cases, the real differentiator is the ability to maintain safety and life under repeated ultra-fast use.

A third theme is ecosystem control. Winning players are no longer treating the battery as a stand-alone component. They are pairing cells with pack architecture, electronics, software, and charging partnerships. That improves customer retention and gives suppliers more leverage in negotiations with automakers. The competitive edge increasingly comes from being able to deliver cells, modules, pack controls, and compatible charging performance together.

- For instance, in March 2025, BYD said its Super e-Platform reached 1,000 kW charging power and could add 400 km of range in 5 minutes, linking battery design with charging-network strategy.

LIST OF KEY ULTRA-FAST EV BATTERIES COMPANIES PROFILED

- CATL (China)

- BYD (China)

- LG Energy Solution (South Korea)

- Samsung SDI (South Korea)

- SK On (South Korea)

- Panasonic Energy (Japan)

- Gotion High-Tech (China)

- EVE Energy (China)

- Sunwoda (China)

- CALB (China)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Geely introduced a next-generation EV battery capable of charging from 10% to 80% in just over five minutes, setting a new benchmark for ultra-fast charging. The development highlights advancements in high-rate battery technology, significantly reducing charging time and enhancing convenience for next-generation electric vehicles.

- May 2025: LG Energy Solution and GM said they would commercialize lithium manganese-rich prismatic battery cells for future GM electric trucks and full-size SUVs. The announcement pointed to a new chemistry route for larger EVs that need lower cost and practical range.

- December 2024: Stellantis and CATL agreed to invest up to EUR 4.1 billion in a joint venture for a large-scale LFP battery plant in Zaragoza, Spain, with planned production by the end of 2026. The project supports affordable EV programs and strengthens Europe’s LFP footprint.

- December 2024: CATL, CAES, and FAW Hongqi agreed to cooperate on battery swapping. That partnership signaled continued commercial interest in swap-compatible battery strategies for selected vehicle platforms.

- September 2024: Subaru and Panasonic Energy announced plans to supply automotive lithium-ion batteries and jointly establish a new battery factory in Japan. The development added manufacturing depth to Japan’s EV battery ecosystem.

- September 2024: Samsung SDI presented LFP+, all-solid-state, and 46-phi cylindrical batteries for electric commercial vehicles at IAA Transportation. This was significant as it broadened Samsung SDI’s public product mix beyond its traditional premium image.

- April 2024: LG Energy Solution said its USD 5.5 billion Arizona complex was progressing, with 46-series cylindrical batteries planned for EV use. That investment reinforced LGES’s effort to secure future U.S. demand for advanced cylindrical formats.

REPORT COVERAGE

The global ultra-fast EV batteries market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, Battery Type, Charging Capability, Battery Capacity, Component, and Region |

| By Vehicle Type |

|

| By Battery Type |

|

| By Charging Capability |

|

| By Battery Capacity |

|

| By Component |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 38.76 billion in 2025 and is projected to reach USD 130.44 billion by 2034.

In 2025, the market value stood at USD 23.97 billion.

The market is expected to exhibit a CAGR of 14.8% during the forecast period.

The cars segment led the market by vehicle type.

The expansion of high-power charging networks is driving the global market.

CATL, BYD, LG Energy Solution, and Samsung SDI are some of the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us