Underfloor Heating Market Size, Share & Industry Analysis, By Type (Hydronic and Electric), By Installation (New Build and Retrofit), By Component (Heating and Control), By End User (Residential, Industrial, and Commercial), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

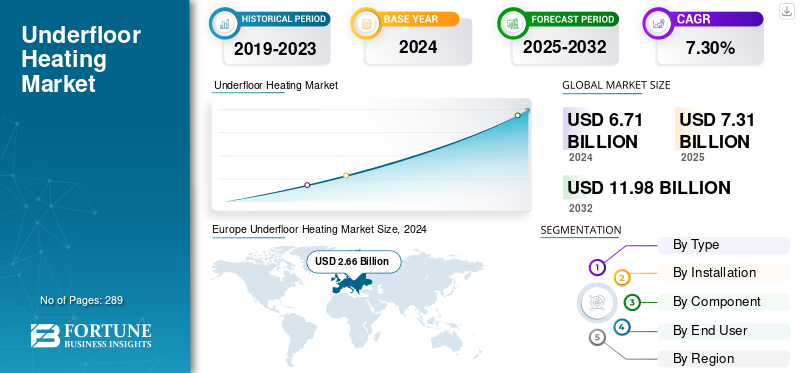

The global underfloor heating market size was valued at USD 7.31 billion in 2025. It is projected to grow from USD 7.94 billion in 2026 to USD 13.57 billion by 2034, exhibiting a CAGR of 6.93% during the forecast period. Europe dominated the underfloor heating market with a market share of 39.36% in 2025.

Underfloor heating is an energy-efficient heating system that uses radiant heat to warm a room from the floor upwards, creating a comfortable and evenly distributed temperature. It eliminates the need for traditional radiators and can be installed using either electric heating cables or water-based (hydronic) systems embedded beneath the floor surface. Electric underfloor heating is typically preferred for smaller spaces or renovations due to its ease of installation, while hydronic systems are more suitable for larger areas or new constructions because of their long-term efficiency and lower operating costs. This technology is widely used in residential, commercial, and industrial applications, offering benefits such as improved indoor air quality, design flexibility, and lower energy consumption compared to conventional heating methods.

Warmup PLC, is one of the key players in the market, which has installed millions of systems in more than 70 countries. Warmup is particularly noted for its efforts to combine high-performance heating technology with sustainability goals. The company’s smart underfloor heating systems, when paired with advanced control algorithms, aim to cut energy waste and reduce CO₂ emissions, with a target of lowering excess annual CO₂ emissions by 170,000 tons by 2025.

Download Free sample to learn more about this report.

Underfloor Heating Market Key Takeaways

- 2025 Market Size: USD 7.31 billion

- 2026 Market Size: USD 7.94 billion

- 2034 Forecast Market Size: USD 13.57 billion

- CAGR: 6.93% from 2026–2034

- Europe dominated the underfloor heating market with a 39.36% share in 2025.

- Hydronic systems accounted for 61.34% market share in 2026.

- New build installation segment held 58.82% market share in 2026.

North America

North America accounted for USD 1.62 billion in 2025, driven by energy-efficient home upgrades and smart heating adoption.

Asia Pacific

Asia Pacific reached USD 1.79 billion in 2025, supported by urbanization and smart building development.

Europe

Europe generated USD 2.88 billion in 2025 and maintained market leadership due to strict energy efficiency regulations.

U.S.

Market is estimated to hold a market size of USD 1.36 billion in 2026.

Japan

Market will represent market size of USD 0.81 billion in 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Energy-Efficient and Sustainable Heating Solutions Drive Market Growth

As global awareness of climate change intensifies, both consumers and governments are prioritizing technologies that reduce energy consumption and carbon emissions. Underfloor heating systems operate through radiant heat, which directly warms objects and occupants rather than just the surrounding air, resulting in more uniform temperature distribution, enhanced comfort, and lower energy wastage compared to traditional heating methods. This efficiency enables users to achieve the same comfort level at lower operating temperatures, typically around 29°C, while traditional systems often require water temperatures of 60–70°C. Consequently, underfloor heating can deliver energy savings of 15–30%, depending on building design and insulation. Moreover, these systems integrate seamlessly with renewable energy technologies such as air and ground-source heat pumps, further enhancing sustainability and lowering operational costs. The growing focus on achieving net-zero energy buildings (NZEBs) and meeting green building certification standards such as LEED and BREEAM has also boosted adoption across residential, commercial, and institutional projects. As a result, energy efficiency and environmental responsibility remain the cornerstone of the industry’s expansion.

Growth in Construction and Renovation Activities Propel Market Expansion

Another significant growth driver for the underfloor heating industry is the steady rise in global construction and renovation activities, particularly in residential and commercial sectors. Rapid urbanization, improved living standards, and a growing emphasis on comfort and aesthetics are pushing developers and homeowners to integrate modern heating systems during new constructions and retrofits. In many European countries, where space optimization and energy efficiency are priorities, underfloor heating is becoming a standard feature. Additionally, renovation projects in older buildings are increasingly incorporating low-profile retrofit systems that can be installed with minimal floor height increase, expanding the addressable market beyond new developments. Commercial spaces such as offices, hotels, hospitals, and educational institutions are also adopting underfloor heating due to its even heat distribution, low maintenance, and silent operation. The post-pandemic trend of home improvement investments has further boosted demand as consumers seek long term comfort and value additions to their properties. Together, these factors make construction and refurbishment activity a leading factor for the rising demand for energy efficient heating.

MARKET RESTRAINTS

High Initial Installation Cost to Constrain Market Growth

One of the major challenges facing the underfloor heating industry is the high initial installation cost, which can act as a deterrent, particularly in price-sensitive markets. Unlike conventional heating systems that rely on radiators or air vents, underfloor heating requires specialized components such as insulation boards, manifolds, thermostats, and either electrical cables or hydronic piping embedded beneath the flooring. This makes installation labor-intensive and technically complex, especially in retrofit projects where existing floors must be modified or replaced. For hydronic systems, the cost of connecting to boilers or heat pumps further adds to the upfront expense. Although these systems offer long-term savings through reduced energy consumption, the payback period can extend over several years, discouraging short-term buyers or developers working on tight budgets. Additionally, the perceived complexity and cost of maintenance in some markets amplify the hesitation to invest. Overcoming this challenge will require increased consumer education, advances in prefabricated or modular installation techniques, and wider availability of cost-effective materials to make underfloor heating more accessible to the mass market.

MARKET OPPORTUNITIES

Supportive Government Regulations and Policies to Offer Lucrative Opportunities for the Market

Supportive government regulations and sustainability initiatives are also playing a crucial role in driving the underfloor heating market growth. Many countries are implementing strict building energy codes and emission standards aimed at reducing fossil fuel dependency and promoting renewable energy integration in the built environment. For instance, the European Union’s Energy Performance of Buildings Directive (EPBD) and various net-zero carbon policies mandate energy-efficient heating solutions, encouraging the use of radiant and low-temperature systems such as underfloor heating. Similarly, government incentives, tax rebates, and subsidies for energy-efficient retrofits and renewable-compatible heating systems have made adoption more financially viable for homeowners and businesses. The compatibility of underfloor heating with renewable sources such as heat pumps, solar thermal systems, and district heating networks aligns perfectly with these policy objectives. As nations move toward carbon neutrality and greener infrastructure, supportive legislation and public awareness campaigns will continue to stimulate strong market growth for underfloor heating solutions worldwide.

MARKET CHALLENGES

Slow Heating Response and System Inertia to Hinder Market Growth

Slow thermal response time often referred to as system inertia is associated with radiant floor heating. Because the system relies on heating large floor surfaces to emit warmth gradually, it can take several hours to reach the desired room temperature, unlike traditional radiators that deliver quicker heat output. This delay can be inconvenient for users seeking rapid temperature adjustments, especially in climates with fluctuating weather or in spaces used intermittently. While modern systems with advanced thermostatic controls and smart sensors help mitigate this issue through preheating algorithms and zonal control, it remains a technical limitation compared to forced-air systems. Additionally, the thermal mass that provides comfort and stability can become a disadvantage when rapid cooling or switching is needed, potentially leading to energy inefficiency if not properly managed. Manufacturers are addressing this challenge by developing low-mass and thin-layer systems, improved insulation materials, and intelligent predictive heating technologies, but widespread awareness and adoption of these solutions are still evolving.

UNDERFLOOR HEATING MARKET TRENDS

Rising Adoption of Smart Home Technologies and Advanced Heating Controls to Lead Market Growth

The integration of smart thermostats, sensors, and Internet of Things (IoT) devices has transformed how underfloor heating systems are managed, making them far more intuitive, responsive, and energy-efficient. Modern systems now feature zonal temperature control, allowing users to adjust heating settings in individual rooms according to occupancy and usage patterns, thereby reducing unnecessary energy consumption. Smart thermostats can also learn user behavior over time and automatically optimize heating schedules for maximum comfort and minimal waste. Many solutions can be controlled remotely via mobile apps or voice assistants such as Amazon Alexa or Google Home, offering convenience and real-time energy monitoring.

Furthermore, the integration of AI and data analytics has enabled predictive maintenance and adaptive heating, where systems can anticipate external factors such as weather changes or open windows and adjust performance accordingly. This technological advancement not only enhances user experience but also significantly lowers operating costs, aligning with global energy conservation goals. As smart homes become more prevalent, the demand for intelligent, connected heating systems is expected to accelerate, positioning underfloor heating as a key component of modern, sustainable living environments.

Download Free sample to learn more about this report.

IMPACT OF TARIFF

Tariffs have a notable impact on the global underfloor heating market by increasing production and installation costs, as many components are imported. Higher tariffs on copper, electronics, and heating cables raise overall system prices, slowing adoption in cost-sensitive regions. They can also disrupt supply chains and limit product availability, affecting international brands. Conversely, countries with low or no tariffs on energy-efficient technologies experience faster market growth. Overall, while tariffs protect local industries, they can reduce affordability and hinder the global expansion of underfloor heating systems.

SEGMENTATION ANALYSIS

By Type

Higher Energy Efficiency and Cost Effectiveness to Lead Hydronic’s Market Share

The market is segmented by type into hydronic and electric. Hydronic systems accounted for 61.34% market share in 2026, driven by their high energy efficiency, cost-effectiveness over long-term use, and suitability for large-scale installations such as residential and commercial buildings. These systems operate by circulating warm water through pipes beneath the floor, offering consistent and comfortable heating with lower operating costs. Their compatibility with renewable energy sources, such as heat pumps and solar thermal systems, further strengthens their global appeal.

Electric underfloor heating systems segment is growing at the fastest rate of 7.81%, favored for their quick installation, compact design, and flexibility in smaller or retrofit projects. Electric systems are often used in bathrooms, kitchens, or offices, where rapid heating and simple control mechanisms are preferred. Although they typically have higher running costs compared to hydronic systems, ongoing advancements in insulation, heating cables, and smart control technologies are improving their efficiency and affordability. Overall, while hydronic systems dominate the global market in large-scale applications, electric systems continue to gain momentum due to their convenience, adaptability, and integration with modern smart home technologies.

By Installation

Easy Installation and Lower Incremental Costs to Boost New Build Segment's Market Growth

Based on installation, the market is divided into new build and retrofit. New build projects held a major market share of 58.82% in 2026 as underfloor heating is increasingly being integrated into the design stage of modern residential, commercial, and industrial constructions. This dominance is driven by the ease of installation during construction, lower incremental costs, and growing emphasis on sustainable building practices and energy-efficient infrastructure. In new builds, underfloor heating systems—both hydronic and electric—can be seamlessly embedded beneath floors with optimized insulation and layout design, ensuring long-term operational efficiency and comfort.

Conversely, retrofit applications are expanding at the fastest rate of 7.73%. The retrofit segment is gaining traction as consumers and building owners seek to enhance comfort, reduce energy bills, and upgrade outdated heating systems without full structural renovations. The development of low-profile and quick-install systems, including electric mats and thin-pipe hydronic solutions, has made retrofitting more feasible and less disruptive. While installation costs remain relatively higher in retrofit projects compared to new builds, technological innovations and modular designs are gradually narrowing this gap. Overall, new build projects continue to dominate due to structural efficiency and policy support, but retrofits represent a rapidly growing opportunity fueled by modernization trends and the global push for energy-efficient building upgrades.

By Component

New Construction Projects and Advancements in Low-Temperature Heating Technologies Boost Heating Systems Growth

The global underfloor heating market is broadly segmented into heating systems and control systems, both of which play integral roles in delivering comfort and energy efficiency. In 2024, heating systems accounted for a major share of 81.97%, as they represent the core hardware responsible for heat generation and distribution. Demand for heating systems is driven by new construction projects, advancements in low-temperature heating technologies, and the integration of underfloor solutions with renewable energy sources. The efficiency, durability, and installation flexibility of these systems continue to be key factors influencing their dominant market position.

Control systems is experiencing fastest growth of 8.57% due to the rising adoption of smart thermostats and digital control technologies. Modern control units enable precise temperature regulation, zonal control, and real-time energy monitoring, significantly enhancing system efficiency and user convenience. The emergence of AI-based and IoT-enabled controls allows users to automate heating schedules, detect occupancy, and integrate underfloor heating with broader smart home ecosystems. Although smaller in overall market share, the control segment’s growth is accelerating rapidly, reflecting the global shift toward intelligent, connected, and energy-optimized heating environments.

By End User

To know how our report can help streamline your business, Speak to Analyst

Rising Disposable Income and Urban Housing Developments to Amplify Residential Segment’s Growth

The market is segmented into residential, commercial, and industrial end users, each contributing differently to overall market demand. The residential sector held the largest underfloor heating market share of 81.49% in 2026, driven by growing consumer preference for energy-efficient, comfortable, and aesthetically appealing heating solutions. Underfloor heating is increasingly being installed in both new homes and renovation projects, offering benefits such as even heat distribution, silent operation, and compatibility with renewable energy systems. Rising disposable incomes, urban housing developments, and awareness of sustainable living practices further support its dominance. The residential segment is expected to lead the market, contributing 50.38% globally in 2026.

The commercial sector is the fastest growing segment at a growth rate of 7.92% with strong demand from office buildings, hotels, hospitals, educational institutions, and retail spaces. These applications prioritize occupant comfort, energy savings, and improved air quality, all of which are enhanced by underfloor heating. Commercial installations often use large-scale hydronic systems, designed for efficient temperature management in high-traffic or multi-room environments.

UNDERFLOOR HEATING MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, and Latin America, and the Middle East & Africa.

Europe Underfloor Heating Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe

The Europe region captured 39.36% of the global market in 2025, generating USD 2.88 Billion in revenue, and is projected to reach USD 3.11 Billion in 2026, driven by strict energy efficiency standards and the widespread integration of renewable energy in building design. For instance, the European Commission’s “Fit for 55” package and the Energy Performance of Buildings Directive (EPBD) have encouraged developers to adopt low-carbon heating solutions. In Germany and the U.K., underfloor heating is now a standard feature in many new homes, with penetration in residential construction exceeding 25%. The region’s preference for hydronic systems is also reinforced by the strong adoption of heat pumps and high awareness of energy conservation among homeowners. In 2026 the U.K., will generate a revenue of USD 0.51 billion, while Germany and France market size will be USD 0.72 billion and USD 0.28 billion respectively.

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 1.79 Billion in 2025, accounting for 24.48% share, and is expected to reach USD 1.96 Billion in 2026. Asia Pacific is emerging as a key growth hub, driven by rapid urbanization, infrastructural development, and an expanding middle-class population seeking enhanced living standards. China, Japan, and South Korea are investing heavily in modern, energy-efficient residential complexes and smart buildings that integrate electric underfloor heating systems. In Japan, radiant floor heating is increasingly incorporated into new urban housing developments, while in China, rising disposable income and a focus on indoor comfort are accelerating installations in premium apartments and villas. China, India, and Japan will represent USD 0.81 billion, USD 0.17 billion, and USD 0.32 billion respectively in 2026.

North America

In 2025, the North America market stood at USD 1.62 Billion, representing 22.18% of global demand, and is projected to grow to USD 1.77 Billion in 2026. In North America, the market is expanding rapidly, supported by rising consumer awareness of indoor comfort and energy savings. The U.S. Department of Energy highlights that radiant floor systems can improve energy efficiency by up to 30% compared to conventional forced-air heating, which has led to their growing installation in residential and commercial buildings. Smart thermostats and connected home technologies are further driving adoption, as consumers increasingly seek comfort systems that can be controlled remotely. Additionally, the growing renovation trend and the focus on sustainable building certifications, such as LEED, are strengthening the market outlook. The U.S. holds a market size of USD 1.36 billion in 2026.

Latin America

In 2025, Latin America represented USD 0.43 Billion, accounting for 5.92% of the worldwide market, and is projected to grow to USD 0.46 Billion in 2026. In Latin America, underfloor heating adoption is still in its early stages but gaining momentum, particularly in Brazil, Chile, and Argentina, where the demand is rising in luxury homes, high-end offices, and hospitality projects. The increasing focus on sustainable building design and growing urban construction activity are expected to strengthen future adoption.

Middle East & Africa

The Middle East & Africa market accounted for USD 0.59 Billion in 2025, representing 8.06% of the global industry, and is expected to reach USD 0.63 Billion in 2026. The Middle East & Africa, though characterized by generally warmer climates, is witnessing growing interest in underfloor heating in specific applications such as luxury villas, hotels, and high-altitude regions where temperature control is important. The UAE and Saudi Arabia are integrating radiant floor heating into premium developments as part of smart and sustainable city initiatives, including NEOM in Saudi Arabia. Overall, each region is advancing at a different pace, but the common trend across all is the increasing alignment of underfloor heating with global goals for energy efficiency, comfort, and sustainable urban development. The Middle East and Africa is estimated to hold a market size of USD 0.59 billion in 2025 while GCC market’s size will be USD 0.27 billion in 2025.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Warmup’ Advancement in Product Solutions to Lead Market Growth

Warmup PLC has established itself as one of the leading players in the global underfloor heating market through a combination of innovation, sustainability-driven initiatives, and customer-centric strategies that have significantly strengthened its market share. The company’s success is largely attributed to its commitment to research and development, which has resulted in continuous product advancements and integration of smart technologies. Warmup invests heavily in developing intelligent heating solutions including its Smart Thermostat 4iE and SmartCare monitoring system that use AI-based algorithms to learn user behavior and optimize energy consumption. These smart systems can reduce energy usage by up to 25–30%, making them attractive to environmentally conscious consumers and aligning with global carbon reduction goals.

List of Key Underfloor Heating Companies Profiled

- Warmup PLC (U.K.)

- Uponor Corporation (Finland)

- Rehau Group (Germany)

- Danfoss A/S (Denmark)

- nVent Electric plc (U.K.)

- Nexans S.A. (France)

- Robert Bosch GmbH (Germany)

- Siemens AG (Germany)

- ThermoSoft International Corporation (U.S.)

- Emerson Electric Co. (U.S.)

- Honeywell International Inc. (U.S.)

- Mitsubishi Electric Corporation (Japan)

- Devi (Danfoss subsidiary) (Denmark)

- Watts Water Technologies, Inc. (U.S.)

- Teplolux (Russia)

KEY INDUSTRY DEVELOPMENTS

- November 2024: Dutch home automation company DomeCtrl launched ControlBox, an all-in-one system that integrates radiant underfloor heating (RFH) with Home Assistant. According to DomeCtrl’s Anton Verburg, ControlBox can manage hydronic RFH systems, including thermal valves, PWM-controlled pumps, and other related components. It supports multiple 1-wire temperature sensors over long distances (over 6 meters) and features 32 LED output channels capable of delivering up to 2kW of power.

- October 2024: Ambiente has introduced JoFloor 28, a high-efficiency underfloor heating system for suspended timber floors. The system uses Alu-Foil in both its base and top panels to boost heat transfer, delivering up to 74 W/m² and ensuring even heat distribution across the floor. It features a 22 mm P5 chipboard base with grooves for AmbiFlex P12 pipes, designed for easy installation and long-term structural stability. Staggered pipe layouts help prevent floor warping and maintain consistent performance.

- September 2024: Jersey Energy Technologies (JET) has partnered with Haydale, a company specializing in graphene materials, to introduce a new type of graphene-based underfloor heating in the island’s social housing sector. Tests by Haydale show that its graphene ink heating system uses about 30% less energy than traditional wired systems connected to the mains. To validate these results, JET will conduct a pilot program during the winter, installing the technology in selected homes to collect real-world performance and energy consumption data.

- January 2024: Independent Builders Merchants Group (IBMG) has introduced its first private-label brand, ProRange, starting with an underfloor heating (UFH) line aimed at professional installers. The ProRange UFH offers a two-year warranty on components like manifolds, pumps, and valves, and a 50-year warranty on pipes. Available across IBMG’s 46 plumbing branches including Total Plumbing Supplies, Grant & Stone, RGB, Sussex Plumbing Suppliers, and DW Burns the range also comes with free design support and a 24-hour quote turnaround service.

- June 2023: At InstallerSHOW 2023, Ambiente introduced three innovations aimed at making underfloor heating installations faster and more efficient. The AmbiDeck Family expands its board range to simplify fitting and reduce on-site preparation, while AmbiFlex offers a smart pipe de-coiler that allows easy reuse of leftover pipe, cutting time and waste. The AmbiEgo actuator uses AI technology to automatically balance and adjust water flow in each room, improving system performance and adapting seamlessly to both new and existing installations.

REPORT COVERAGE

The report delivers a detailed insight into the market and focuses on key aspects, such as leading companies. Besides, it offers insights into the market trends and technologies and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors and challenges that have contributed to the growth and downfall of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.93% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Installation

|

|

|

By Component

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

As per Fortune Business Insights study, the market size in 2025 was USD 7.31 billion.

The market is likely to record a CAGR of 6.93% over the forecast period of 2026-2034.

By end user, the residential segment holds the leading position in the market.

Europes market size stood at USD 2.88 billion in 2025.

Increasing demand for energy-efficient and sustainable heating solutions is the key factor driving the markets growth.

Some of the key players in the market are Warmup PLC, Uponor Corporation, Rehau Group, and Danfoss A/S, and others.

The global market size is expected to reach a valuation of USD 13.57 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 289

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us