Underwater Warfare Market Size, Share & Industry Analysis, By Platform (Submarines, Surface Ships, and Naval Helicopters), By Systems (Communications, Electronic Warfare, Weapons, Unmanned, and Sonar), By End User (Commercial and Naval), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

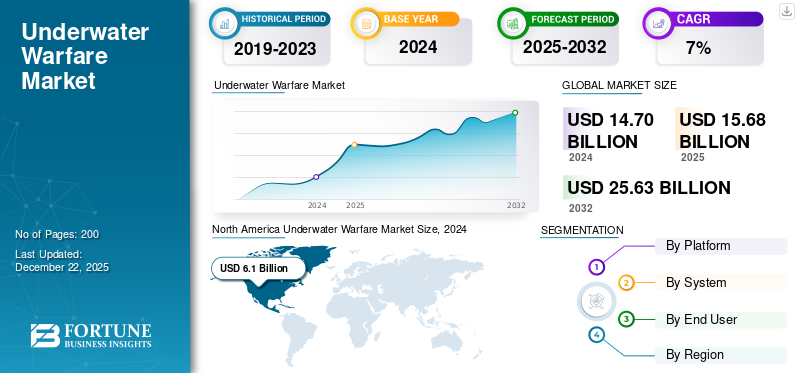

The global underwater warfare market size was valued at USD 15.69 billion in 2025 and is projected to grow from USD 17.06 billion in 2026 to USD 28.78 billion by 2034, exhibiting a CAGR of 6.80% during the forecast period. North America dominated the underwater warfare market with a market share of 41.05% in 2025.

The underwater warfare market is a critical segment of the global defense industry, focusing on technologies and systems designed for operations beneath the ocean's surface. This market includes submarines, Autonomous Underwater Vehicles (AUVs), Unmanned Underwater Vehicles (UUVs), sonar systems, torpedoes, and other advanced weaponry. Geopolitical tensions, naval modernization programs, and technological advancements are driving significant growth in this sector.

Undersea warfare systems consist of a range of technologies and gear utilized for military activities beneath the ocean’s surface. These systems comprise submarines, underwater sensors, torpedoes, mines, and anti-submarine warfare (ASW) gear. They are employed for several purposes, such as detecting, tracking, and neutralizing underwater hazards, safeguarding maritime borders, and protecting crucial underwater infrastructure. Developments in automation, artificial intelligence, and underwater robotics are expanding the future potential of undersea warfare systems, enhancing capabilities for both offensive and defensive operations. This progression is motivated by increasing geopolitical conflicts and the demand for enhanced maritime security, both of which continue to influence and drive innovation in the sector.

The COVID-19 pandemic had a mixed impact on market growth, affecting different aspects in various ways. The pandemic caused significant disruptions in production and supply chains, leading to delays in the delivery of critical components and affecting the timely completion of naval projects. Economic downturns resulting from the pandemic led to budgetary constraints, potentially slowing down investments in underwater warfare technology. The pandemic increased the demand for maritime security, particularly for Anti-Submarine Warfare (ASW) Unmanned Underwater Vehicles (UUVs), as countries sought to protect their borders with reduced human involvement.

Download Free sample to learn more about this report.

Underwater Warfare Market Key Takeaways

- 2025 Market Size: USD 15.69 billion

- 2026 Market Size: USD 17.06 billion

- 2034 Forecast Market Size: USD 28.78 billion

- CAGR: 6.80% from 2026–2034

- North America dominated the underwater warfare market with a market share of 41.05% in 2025.

- The submarines segment is projected to dominate the market with a share of 46.58% in 2026.

- The SOR segment is expected to account for 45.00% of the market share in 2026.

North America

North America contributed 41.05% to the global market in 2025, with a valuation of USD 6.44 billion, and is projected to reach USD 6.93 billion in 2026.

Europe

Europe accounted for USD 5.29 billion in 2025, representing 33.75% of the global market share, and is projected to reach USD 5.77 billion in 2026.

Asia Pacific

The Asia Pacific market was valued at USD 2.76 billion in 2025, capturing 17.57% of global revenue, and is estimated to reach USD 3.02 billion in 2026.

U.S.

The U.S. market is projected to reach USD 5.76 billion by 2026.

Japan

The Japan market is projected to reach USD 0.89 billion by 2026.

Read More

Russia-Ukraine War Impact

Ongoing Conflict among Russia-Ukraine to Boost Investments in Unmanned Underwater Vehicles and Advanced Undersea Warfare Technologies

The Russia-Ukraine war has significantly impacted the underwater warfare market growth, particularly in the areas of Unmanned Underwater Vehicles (UUVs) and undersea warfare systems. The conflict has heightened the need for advanced underwater weapons, particularly smart and unmanned systems. Russia has increased its focus on smart underwater weapons to gain strategic advantages, while countries supporting Ukraine have expanded their weapon portfolios to counteract Russian aggression.

Unmanned Maritime Vehicles (UMVs) such as Ukraine's Magura V5 have played a pivotal role in naval warfare, damaging Russian ships and forcing the retreat of its Black Sea Fleet. This success highlights the growing importance of UMVs in modern naval conflicts.

Emerging trends include advancements in sonar and sensor technologies, artificial intelligence integration, enhanced stealth capabilities, and multi-domain operations. These innovations are being accelerated by the geopolitical tensions stemming from the war.

The war has underscored the strategic importance of controlling maritime zones through underwater systems. Russia’s blockade of Ukrainian ports and restricted access to critical seas such as the Black Sea has emphasized the need for robust undersea warfare systems for border security and naval defense. Ukraine's use of long-range artillery and UMVs to target Russian naval assets demonstrates how undersea warfare systems can shift military dynamics in contested waters.

The war has disrupted maritime commerce, increasing costs such as war-risk premiums for vessels operating near conflict zones. This has indirectly affected investments in maritime technologies, including underwater systems. Sanctions against Russia have restricted its ability to invest in naval technologies, which may slow its production of advanced undersea systems but could also drive innovation as it seeks alternatives.

UNDERWATER WARFARE MARKET TRENDS

Technological Improvements in Underwater Defense Systems to Drive Market Expansion

One of the primary factors driving the CAGR of the market is the rising technological advancements in underwater defense systems. Likewise, nations are recognizing the strategic importance of safeguarding their marine borders and interests. Consequently, new technology specifically crafted for underwater defense is being developed and implemented at an escalating pace. Underwater surveillance and reconnaissance abilities are enhanced through the deployment of Autonomous Underwater Vehicles (AUVs) and Unmanned Underwater Vehicles (UUVs), which are equipped with advanced sensors and communication technologies.

As sonar technologies have progressed, the monitoring of submarine activities can now be conducted more efficiently, resulting in improved detection and tracking abilities. Furthermore, extensive underwater data processing has been refined through the integration of artificial intelligence and machine learning algorithms, facilitating faster and more accurate decision-making. The advancement of stealth technology, including advanced coatings and materials, has also contributed to making underwater assets more elusive and harder to detect.

In the future, heightened tensions among various nations due to escalating wars and conflicts are expected to propel market growth. A war is defined as a violent conflict between nations or states. Armed forces commonly utilize underwater warfare technology to address underwater threats in order to maintain and manage conflict situations and ensure national security.

- North America witnessed underwater warfare market growth from USD 5.71 Billion in 2023 to USD 6.1 Billion in 2024.

For example, in July 2022, Ukrainian forces were utilizing long-range artillery across the Dnipro River to strike at bridges. The U.K. Ministry of Defence reported two attacks on the Antonivskiy Bridge in Kherson in their update regarding the Russia-Ukraine War. Therefore, the market is growing due to the increased tensions among different countries caused by a rise in wars and conflicts. Thus, the market is expanding due to the surge in underwater threats. This factor is driving the revenue of the market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Advancements in Underwater Robotics to Stimulate Market Expansion

Rising developments in underwater robotics are anticipated to enhance the undersea warfare systems market by boosting capabilities and operational efficiency. Recent progress in underwater robotics, including enhanced Autonomous Underwater Vehicles (AUVs) and Remotely Operated Vehicles (ROVs), is expanding the range of undersea missions such as surveillance, reconnaissance, and mine detection. For example, in August 2024, the U.S. Navy’s Naval Sea Systems Command revealed the deployment of a new fleet of sophisticated AUVs equipped with state-of-the-art sensors and AI for better underwater operations, signaling a notable rise in the market’s potential.

Moreover, these advancements align with global defense strategies focused on maintaining maritime security and enhancing response capabilities. In September 2024, the European Union sanctioned funding for the creation of next-generation underwater drones to aid naval operations and anti-submarine warfare. This focus on technological innovation is in line with a wider trend in the defense sector, where investment in robotic systems is predicted to stimulate growth and advancement in the subsea warfare systems market.

MARKET RESTRAINTS

Increasing Technological Complexity to Hinder Market Expansion

Increasing intricacy in the undersea warfare systems market may hinder growth by elevating development and operational expenses. As systems progress, their design, integration, and maintenance require specialized expertise and advanced technology. This intricacy raises the initial investment and also demands continual research and development to stay aligned with technological progress. Consequently, these elements may constrain market participation to a selected few major players with substantial financial resources, potentially diminishing competition and innovation.

Moreover, swift technological advancements can render existing systems outdated, leading to a cycle of incessant upgrades. This ongoing requirement for technological improvement and adjustment can strain budgets and resources, complicating the market’s growth path. Organizations might encounter challenges in managing these complexities, leading to deployment delays and possible operational inefficiencies.

MARKET OPPORTUNITIES

Changing Defense Needs and Advancements in Technology in Underwater Warfare Sector Drives Market Growth

The underwater warfare sector presents considerable opportunities driven by changing defense needs and technological advancements. The increasing demand for sophisticated naval defense systems, such as Autonomous Underwater Vehicles (AUVs), Unmanned Underwater Vehicles (UUVs), and next-generation sonar technologies, is generating significant prospects for manufacturers and technology providers.

Geopolitical tensions and the heightened necessity for maritime security are encouraging nations to invest in the modernization of their naval fleets and the enhancement of underwater defense capabilities. Additionally, the incorporation of Artificial Intelligence (AI), machine learning, and automation into underwater warfare technologies is anticipated to improve operational efficiency and foster innovation. Rising defense budgets, international partnerships, and the growth of public-private collaborations in defense contracts will further promote market expansion. These elements position the underwater warfare sector for ongoing development and technological progress.

MARKET CHALLENGES

Expenses Associated with the Research, Development, and Deployment of Advanced Underwater Systems Hinder Market Growth

A significant obstacle in the underwater warfare sector is the considerable expense associated with the research, development, and deployment of advanced underwater systems, including submarines, sonar technologies, and Unmanned Underwater Vehicles (UUVs). The complexity of these technologies necessitates substantial financial investment and extended development timelines, which can limit accessibility for certain nations. Additionally, the challenging and often hostile underwater environment poses technical difficulties regarding system reliability and performance. Another concern is the compatibility of new technologies with existing legacy systems, as military forces aim to merge contemporary innovations with established frameworks. Security vulnerabilities, such as the risk of cyberattacks on underwater defense systems, further jeopardize operational integrity. Lastly, geopolitical tensions and regulatory obstacles within international defense agreements may hinder cross-border cooperation and impede market expansion.

SEGMENTATION ANALYSIS

By Platform

Submarines to Take the Lead Due to Government Initiatives and Technological Advancements

Based on the platform, the market has been segmented into submarines, surface ships, and naval helicopters.

The submarines segment is projected to dominate the market with a share of 46.58% in 2026, owing to technological advancements and government initiatives. The integration of advanced technologies such as stealth capabilities, nuclear power, and sophisticated combat systems enhances the operational efficiency and strategic value of submarines. These advancements make submarines crucial assets for naval forces, contributing to their growing demand.

Surface ships are expected to be the fastest-growing segment for the period of 2025-2032. Surface ships are increasingly equipped with advanced technologies such as sonar systems, Unmanned Underwater Vehicles (UUVs), and electronic warfare systems, enhancing their capabilities in anti-submarine warfare and intelligence gathering.

- The surface ships segment is expected to hold a 32.3% share in 2024.

To know how our report can help streamline your business, Speak to Analyst

By System

Integration of Artificial Intelligence (AI), Machine Learning, and Improved Signal Processing in Sonar Systems Boosted Segment Expansion

By system, the market is segmented into communications, electronic warfare, weapons, unmanned, and sonar.

The SOR segment is expected to account for 45.00% of the market share in 2026. The integration of advanced technologies such as Artificial Intelligence (AI), machine learning, and improved signal processing has enhanced the detection and tracking capabilities of sonar systems. This makes them more effective in anti-submarine warfare (ASW) and underwater surveillance.

Electronic warfare is expected to be the segment with the highest growth rate during the forecast period. Electronic warfare systems play a critical role in disrupting enemy communications and radar systems, which can be vital in underwater warfare for maintaining operational secrecy and disrupting enemy operations. Electronic warfare systems are often integrated with other underwater warfare systems, such as sonar and communication systems, to enhance overall effectiveness. This integration allows for more comprehensive surveillance and countermeasures against enemy submarines and underwater threats.

By End User

Increase in Geopolitical Tensions Propelled Naval Segment Expansion

Based on end user, the market has been segmented into commercial and naval.

The VAL segment dominated the global market with a market share of 86.95% in 2026. The increasing adoption of advanced technologies such as sonar systems, Unmanned Underwater Vehicles (UUVs), and Autonomous Underwater Vehicles (AUVs) drives demand. These technologies enhance surveillance, reconnaissance, and combat capabilities, making them crucial for naval operations. The naval segment is a dominant end-user in the market, driven by technological advancements, geopolitical tensions, and strategic importance.

The commercial is expected to be the segment with the highest growth rate during the forecast period. Commercial technology firms contribute significantly to the market by developing advanced sensors, communication systems, and Autonomous Underwater Vehicles (AUVs). These technologies are often adapted for military use but initially developed for commercial applications such as oceanographic research or environmental monitoring.

UNDERWATER WARFARE MARKET REGIONAL OUTLOOK

The global market is divided into North America, Europe, Asia Pacific, and the Rest of the World, according to region.

North America

North America Underwater Warfare Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America is expected to dominate the underwater warfare market due to the extensive naval fleet and modernization efforts of the U.S. Navy. The U.S. invests heavily in next-generation submarines, Unmanned Underwater vehicles (UUVs), and advanced sonar systems. The region's growth is driven by a focus on anti-submarine warfare and securing critical underwater assets. Collaborations between defense contractors, technology firms, and government agencies foster innovation in underwater warfare capabilities. The U.S. market is projected to reach USD 5.76 billion by 2026. North America contributed 41.05% to the global market in 2025, with a valuation of USD 6.44 billion, and is projected to reach USD 6.93 billion in 2026.

Europe

Europe is projected to witness significant growth, driven by heavy investments in naval modernization to counter future underwater threats. The region benefits from significant R&D activities and technological advancements in the naval industry. The presence of key industry players and collaborative defense initiatives contributes to region’s leading position in the market. The UK market is projected to reach USD 1.54 billion by 2026, while the Germany market is projected to reach USD 0.95 billion by 2026. Europe accounted for USD 5.29 billion in 2025, representing 33.75% of the global market share, and is projected to reach USD 5.77 billion in 2026.

Asia Pacific

The Asia Pacific region is experiencing the fastest market growth due to rising geopolitical tensions and investments in naval capabilities. Countries such as China, India, and Japan are enhancing their underwater warfare capabilities to secure vital sea lanes. The adoption of advanced technologies such as Autonomous Underwater Vehicles (AUVs), AI-driven sonar systems, and torpedoes drives market demand in the region. The Japan market is projected to reach USD 0.89 billion by 2026, the China market is projected to reach USD 0.95 billion by 2026, and the India market is projected to reach USD 0.52 billion by 2026. The Asia Pacific market was valued at USD 2.76 billion in 2025, capturing 17.57% of global revenue, and is estimated to reach USD 3.02 billion in 2026.

Rest of the World

While specific data for the Rest of the World is less detailed, this region includes Latin America and the Middle East & Africa. These regions are also investing in underwater warfare capabilities, albeit at a slower pace compared to North America, Europe, and Asia Pacific. Geopolitical tensions, the need for maritime security, and investments in defense technologies influence growth in these regions. The Rest of the World region captured 7.63% of the global market in 2025, generating USD 1.2 billion in revenue, and is projected to reach USD 1.34 billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Focus on Providing Technological Advanced Underwater Systems in Market

The competitive environment of the undersea warfare market is marked by swift technological progress and growing investments in research and development. Businesses in this industry are concentrating on boosting the capabilities of their systems, including advancing sonar technologies, autonomous underwater vehicles, and underwater communication systems. There is a significant focus on innovation and strategic collaborations to create more advanced and efficient methods for detecting and countering underwater dangers. Moreover, defense agencies and private companies are working together to combine state-of-the-art technologies and tackle new challenges in undersea warfare. The necessity for improved security and operational efficiency in naval operations fuels this evolving landscape.

LIST OF KEY UNDERWATER WARFARE COMPANIES PROFILED

- Lockheed Martin Corporation (U.S.)

- BAE Systems (U.K.)

- Northrop Grumman (U.S.)

- Thales (France)

- RTX (U.S.)

- Saab AB (Sweden)

- L3Harris Technologies, Inc. (U.S.)

- KONGSBERG (Norway)

- General Dynamics Corporation (U.S.)

- Elbit Systems Ltd. (Israel)

- Raytheon Technologies (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025 – Thales Australia’s BlueSentry thin-line towed sonar array has been effectively incorporated into Saildrone’s Surveyor-class Uncrewed Surface Vehicle (USV), showcasing outstanding operational performance during an extended mission carried out off the U.S.

- March 2025 – Thales, a long-time collaborator with both Naval Group and the Royal Netherlands Navy, announced the delivery of an extensive range of high-performance sonar systems for the next generation of submarines that will succeed the Walrus-class ships currently in operation. The agreement will equip the submarines with a detailed understanding of the underwater acoustic conditions, assisting the Netherlands in ensuring operational dominance.

- March 2025 – Thales achieved a significant milestone by providing the Royal Navy with the first complete end-to-end autonomous maritime mine-hunting system. This accomplishment occurs under the auspices of the Joint Armament Cooperation Organization (OCCAr) and within the context of the Franco-British MMCM (Maritime Mine Counter Measures) initiative.

- January 2025 – Lockheed Martin Rotary and Mission Systems received a USD 502 million indefinite-delivery/indefinite-quantity contract for Hypervisor Technology Zero Surface Ship Undersea Warfare combat systems and spare parts.

- June 2024 – BAE Systems effectively finished sea trials for a new submarine equipped with advanced sonar systems and autonomous underwater vehicles. The trials showcased the submarine’s enhanced abilities in underwater detection and combat, marking a considerable achievement in BAE Systems’ development initiatives.

REPORT COVERAGE

The undersea warfare market is set for considerable expansion, influenced by shifting geopolitical situations, growing maritime risks, and the upgrading initiatives of naval forces across the globe. Innovations in technology, including the creation of more covert submarines, autonomous underwater vehicles, and sophisticated sonar systems, are improving the operational effectiveness of undersea warfare systems. Furthermore, increasing investments in naval defense budgets, especially in developing countries, are driving the need for upgraded undersea warfare capabilities. Nonetheless, obstacles such as budget limitations, technological intricacies, and regulatory challenges might limit market expansion to a degree. In summary, the market offers profitable prospects for manufacturers, service providers, and technology developers to innovate and work together in providing advanced undersea warfare solutions that cater to the changing demands of naval forces worldwide.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Growth Rate |

CAGR of 6.80% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Platform

|

|

By System

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market size was USD 15.69 billion in 2025 and is anticipated to record a valuation of USD 28.78 billion by 2034.

Registering a CAGR of 6.80% , the market will exhibit steady growth during the forecast period of 2025-2032.

Based on the platform, the surface ships segment will likely be the fastest-growing segment in this market during the forecast period.

North America dominated the market in terms of share in 2025.

Lockheed Martin Corporation (U.S.), BAE Systems (U.K.), Northrop Grumman (U.S.), Thales (France), RTX (U.S.), Saab AB (Sweden), and others are the major players in the market.

China dominated the Asia Pacific market in terms of share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us