Vehicle Remarketing, Inspection & Reconditioning Services Market Size, Share & Industry Analysis, By Service Type (Remarketing Services, Inspection Services, and Reconditioning Services), By Vehicle Type (Hatchback/Sedan, SUV, Light Duty Vehicle, and Heavy Duty Vehicle) By Sales Channel (Online Channel, Dealer-to-Dealer, and Others), By Vehicle Ownership Type (Off-lease/Lease Returns, Rental Fleet De-fleet, and Corporate/Commercial Fleet), and Regional Forecast, 2026-2034

Vehicle Remarketing, Inspection & Reconditioning Services Market Size and Future Outlook

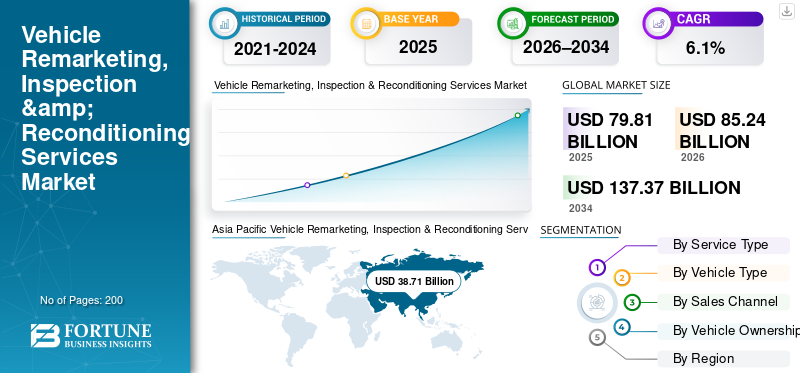

The global vehicle remarketing, inspection & reconditioning services market size was valued at USD 79.81 billion in 2025. The market is projected to grow from USD 85.24 billion in 2026 to USD 137.37 billion by 2034, exhibiting a CAGR of 6.1% during the forecast period. Asia Pacific dominated the Vehicle remarketing, Inspection & Reconditioning Services Market with a market share of 48.5% in 2025.

The global market for vehicle remarketing, inspection & reconditioning services refers to the global automotive ecosystem of service providers that support the systematic resale of used and end-of-life vehicles by enabling condition assessment, value optimization, and efficient channel disposition. The market encompasses professional vehicle inspection, certification, cosmetic and mechanical reconditioning, and structured remarketing services that enable OEMs, fleet operators, leasing companies, rental firms, financial institutions, and dealer groups to maximize residual values and reduce inventory holding periods. Growth of this market is driven by rising off-lease and fleet vehicle volumes, increasing penetration of digital wholesale platforms, stricter quality and transparency expectations in used-vehicle transactions, and expanding role of Certified Pre-Owned (CPO) programs across major automotive markets.

Key players in the market include Cox Automotive, KAR Global, Manheim, OPENLANE, SGS, DEKRA, TÜV SÜD, Alliance Inspection Management (AIM), IAA, and ADESA, alongside regional reconditioning and inspection specialists. These players compete on the basis of inspection accuracy, turnaround time, digital remarketing capabilities, geographic coverage, and the ability to offer end-to-end solutions that span inspection, refurbishment, and vehicle disposition.

Download Free sample to learn more about this report.

VEHICLE REMARKETING, INSPECTION & RECONDITIONING SERVICES MARKET TRENDS

Increasing Focus on Value-Enhancing Reconditioning Services to Shape Market Evolution

A key trend in the market is the increasing emphasis by OEMs, fleet operators, leasing companies, and remarketing service providers on value-enhancing reconditioning to maximize resale prices and reduce inventory aging. Market participants are expanding their in-house and partner-based reconditioning capabilities to cover cosmetic repairs, mechanical fixes, detailing, and smart refurbishment, ensuring vehicles meet standardized resale and certification requirements. This trend is strengthening demand for fast-turn reconditioning hubs, fixed-price refurbishment programs, and integrated inspection-to-reconditioning workflows, enabling sellers to improve residual values, enhance buyer confidence, and accelerate time-to-market in competitive used-vehicle channels.

- In February 2024, Cox Automotive expanded its centralized vehicle reconditioning operations in the U.S. by investing in high-throughput recon centers and digital work-order management systems, aimed at helping dealers and fleet clients increase vehicle resale values and shorten remarketing cycle times.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Penetration of Certified Pre-Owned (CPO) Programs to Drive Market Growth

A key driver of the market is increasing penetration of Certified Pre-Owned (CPO) programs across major automotive markets. OEMs and authorized dealer networks are expanding their CPO service offerings to capture the rising demand from consumers for reliable, warranty-backed used vehicles with transparent condition histories. This expansion is significantly increasing the need for standardized multi-point inspections, mechanical and cosmetic reconditioning, and formal certification processes to ensure vehicles meet brand-specific quality and vehicle safety benchmarks. As a result, remarketing and service providers play a critical role in supporting OEMs and dealers by delivering consistent inspection accuracy, refurbishment quality, and compliance across large and geographically dispersed vehicle volumes.

MARKET RESTRAINTS

Operational Complexity and Capacity Constraints to Limit Market Growth

A key restraint in the market development is the high level of operational complexity and capacity constraints associated with managing large and variable vehicle volumes. Service providers must manage skilled labor, inspection accuracy, parts availability, reconditioning workflows, quality control, and turnaround timelines across multiple locations, often under strict service-level agreements from OEMs and fleet clients. Fluctuations in off-lease and fleet return volumes further strain capacity utilization, making it challenging to maintain consistent service quality and cost efficiency. These operational challenges increase capital and labor requirements, limit rapid scalability, and can restrict market participation, particularly for small and mid-sized players.

MARKET CHALLENGES

Lack of Standardization in Inspection and Grading Criteria to Challenge Market Growth

The lack of standardized inspection and vehicle grading criteria represents a significant challenge for the market, as inconsistencies in assessment methodologies lead to variability in vehicle condition reports and valuations. Differences in inspection depth, damage classification, and grading scales across service providers and regions can reduce buyer confidence, complicate cross-border transactions, and increase dispute rates. This challenge is particularly pronounced in digital and remote remarketing environments, where purchasing decisions rely heavily on inspection data. Addressing standardization gaps remains crucial for ensuring transparency, enhancing pricing accuracy, and facilitating scalable growth across global remarketing channels.

MARKET OPPORTUNITIES

Growth in Electric Vehicle (EV) Remarketing and Reconditioning to Create New Growth Prospects in the Market

The increasing volume of electric vehicles entering the used-vehicle ecosystem is creating new opportunities for the vehicle remarketing, inspection & reconditioning services market growth. Unlike internal combustion engine vehicles, used EVs require specialized inspection and reconditioning capabilities, including battery health diagnostics, software validation, high-voltage system checks, and EV-specific refurbishment standards. As OEMs, fleet operators, and leasing companies expand EV portfolios and CPO programs, demand is rising for service providers that can ensure performance transparency, safety compliance, and residual value optimization for used EVs. This shift is encouraging market players to invest in EV-ready infrastructure, skilled technicians, and advanced diagnostic tools to support the evolving remarketing landscape.

- In April 2024, DEKRA expanded its EV inspection and battery health assessment services across key European markets, focusing on standardized battery diagnostics and safety checks to support OEM and fleet-led used EV remarketing programs.

Download Free sample to learn more about this report.

Segmentation Analysis

By Service Type

Rising Focus on Asset Monetization and Value Optimization to Shape Reconditioning Services’ Dominance

Based on service type, the market is segmented into remarketing services, inspection services, and reconditioning services.

The reconditioning services segment dominates the market due to the critical role of mechanical and cosmetic refurbishment due to their role in enhancing vehicle resale value and reducing time-to-sale. OEMs, leasing companies, fleet operators, and dealers are increasingly investing in structured reconditioning programs, including smart repairs, detailing, minor bodywork, and mechanical fixes, to meet certification standards and buyer expectations. The direct impact of reconditioning on residual value improvement and pricing realization makes it a core service offering within integrated remarketing workflows, driving high revenue contribution across both wholesale and retail channels.

The inspection services segment is the fastest growing, registering a CAGR of 7.6%, driven by the expansion of digital auctions, cross-border used-vehicle trade, and CPO programs. The growing reliance on remote purchasing decisions is increasing the demand for accurate, standardized, and technology enabling inspections, including diagnostic scans and condition grading.

By Vehicle Type

Strong Consumer Preference for Utility Vehicles and Higher Residual Values to Drive SUV Segment Dominance

Based on vehicle type, the market is segmented into hatchbacks/sedans, SUVs, light-duty vehicles, and heavy-duty vehicles.

The SUV segment dominates the market and is also the fastest growing, registering a CAGR of 7.0%. The segment driven by strong global demand for used SUVs, higher resale values, and sustained production and sales volumes over the past decade. SUVs generate significant remarketing activity across OEM off-lease returns, rental fleet rotations, and dealer trade-ins, creating consistent demand for inspections, cosmetic refurbishment, and mechanical reconditioning. Higher average transaction values also encourage greater investment in reconditioning and certification services, reinforcing the segment’s leading contribution in revenue.

To know how our report can help streamline your business, Speak to Analyst

By Sales Channel

Digital Adoption and Expanding Wholesale Networks to Position Dealer-to-Dealer Channel in Leading Position

Based on sales channel, the market is segmented into online channel, dealer-to-dealer, and others.

The dealer-to-dealer channel dominates the market, supported by long-established wholesale networks, franchise dealer relationships, and high transaction volumes of off-lease, trade-in, and fleet vehicles. This channel relies heavily on standardized inspections, rapid reconditioning, and trusted remarketing partners to ensure pricing transparency and fast inventory turnover. Strong buyer confidence, physical auction presence, and recurring dealer participation continue to sustain its leading share in overall market revenues.

The online channel is the fastest-growing, registering a CAGR of 6.9%, driven by the rapid shift toward digital auctions, remote vehicle sourcing, and cross-regional transactions. Increasing reliance on digital condition reports, image-based inspections, and data-driven pricing is accelerating demand for inspection and reconditioning services tailored to online remarketing platforms.

By Vehicle Ownership Type

Rising Fleet Turnover and Structured Disposal Programs to Outline the Demand for Corporate/Commercial Fleet

Based on vehicle ownership type, the market is segmented into off-lease/lease returns, rental fleet de-fleet, and corporate/commercial fleet.

The corporate/commercial fleet segment dominates the market, driven by large, recurring vehicle volumes generated by logistics companies, service fleets, utilities, and enterprise-owned vehicle programs. Fleet operators are increasingly relying on professional inspections, standardized reconditioning, and organized remarketing services to optimize residual values, ensure compliance, and minimize vehicle downtime. Long-term service contracts and predictable disposal cycles further reinforce the segment’s leading contribution to market revenues.

The off-lease/lease return segment is expected to grow at a CAGR of 7.0%, driven by expanding vehicle leasing penetration and increasing volumes of vehicles reaching end-of-lease terms. OEM captive finance companies and leasing firms are placing greater emphasis on inspection accuracy, refurbishment quality, and certification readiness to protect residual values. Meanwhile, the rental fleet de-fleet segment continues to generate steady demand due to frequent fleet rotation cycles and the need for fast-turn inspection and reconditioning to support timely vehicle resale.

Vehicle Remarketing, Inspection & Reconditioning Services Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Vehicle Remarketing, Inspection & Reconditioning Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates and is the fastest-growing regional market, driven by its large vehicle parc, high fleet turnover, and rapidly formalizing used-vehicle ecosystem. Substantial off-lease volumes, expansion of organized used-car retailing, and increasing adoption of digital auctions across China, Japan, India, and Southeast Asia are accelerating demand for professional inspection, refurbishment, and remarketing services. OEM-led Certified Pre-Owned (CPO) programs, growing rental and ride-hailing fleets, and rising cross-border vehicle trade further reinforce the regional leadership of Asia Pacific and sustained high-growth momentum.

China Vehicle Remarketing, Inspection & Reconditioning Services Market

The China market in 2026 is estimated to be around USD 22.53 billion, dominating the Asia Pacific, driven by used-car trade, online platforms, fleet turnover, and standardization.

India Vehicle Remarketing, Inspection & Reconditioning Services Market

The India market in 2026 is estimated at USD 3.35 billion and is fastest-growing, fueled by rising used-car demand, dealerships, digital inspections, and financing access.

Europe

Europe is the second-largest region in the vehicle remarketing, inspection & reconditioning services market share, supported by high vehicle leasing penetration, structured end-of-lease return cycles, and strict regulatory and quality standards for used vehicles. Strong off-lease volumes across Germany, the U.K., France, and Nordic countries are driving consistent demand for standardized inspections, certification, and value-enhancing reconditioning services. The early adoption of digital wholesale platforms and the increasing volumes of used electric vehicles further support the regional market growth.

Germany Vehicle Remarketing, Inspection & Reconditioning Services Market

The Germany market in 2026 is estimated at USD 3.97 billion, supported by strong leasing returns, OEM-certified programs, cross-border trade, and high reconditioning standards.

U.K. Vehicle Remarketing, Inspection & Reconditioning Services Market

The U.K. market in 2026 is estimated at USD 2.64 billion, driven by online remarketing, fleet defleeting, compliance requirements, and demand for vehicle turnaround.

North America

North America’s market growth is driven by large-scale fleet operations, high rental fleet de-fleeting activity, and mature dealer-to-dealer remarketing networks across the U.S. and Canada. Strong adoption of digital and hybrid auctions, coupled with robust consumer demand for certified used vehicles, sustains demand for fast-turn inspections and reconditioning services. Increasingly volumes of used EV are also creating demand for advanced diagnostics and specialized refurbishment capabilities.

U.S. Vehicle Remarketing, Inspection & Reconditioning Services Market

The U.S. market in 2026 is estimated at USD 12.67 billion, benefiting from auction networks, high lease returns, advanced inspections, and large-scale reconditioning facilities.

Rest of the World

The Rest of the World market is gradually expanding, supported by the improvement of used-vehicle market organization in Latin America, the Middle East, and parts of Africa. Rising vehicle ownership, expanding fleet and rental operations, and increasing cross-border vehicle trade are creating opportunities for professional inspection and reconditioning services. Although growth remains moderate, regulatory improvements and digital adoption are expected to accelerate market development over the forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players

Digitalization, Integrated Service Platforms, and Scale-Based Execution is Defining Competition Intensity

The market is characterized by the presence of large, integrated service providers alongside regional specialists competing on scale, technology adoption, service turnaround, and geographic coverage. Key players, including Cox Automotive, KAR Global, Manheim, OPENLANE, IAA, ADESA, SGS, DEKRA, TÜV SÜD, and Alliance Inspection Management (AIM), are strengthening their market positions through digital auction platforms, standardized inspection frameworks, and expanded reconditioning networks. Competitive strategies focus on offering end-to-end solutions spanning inspection, refurbishment, and remarketing, supported by data-driven pricing, AI-enabled condition reporting, and long-term contracts with OEMs, leasing companies, rental firms, and fleet operators. Investments in centralized reconditioning centers, EV-ready inspection capabilities, and integrated digital ecosystems are increasingly shaping competitive differentiation and their market positioning.

- In March 2024, Cox Automotive expanded its Manheim Marketplace capabilities by integrating enhanced digital condition reports and centralized reconditioning services, enabling dealers and fleet clients to accelerate vehicle remarketing while improving price realization and inventory turnover.

LIST OF KEY VEHICLE REMARKETING, INSPECTION & RECONDITIONING SERVICES COMPANIES PROFILED:

- Cox Automotive (U.S.)

- SGS (U.S.)

- DEKRA SE (Germany)

- TUV Rheinland (Germany)

- Copart, Inc. (U.S.)

- Element Fleet Management (Canada)

- Ravin AI (U.S.)

- Flexco Fleet Services (U.S.)

- ServNet Auctions (U.S.)

- Fleet Street Remarketing (U.S.)

- ATS Euromaster (U.K.)

- VQS (U.K.)

- Carchex (U.K.)

KEY INDUSTRY DEVELOPMENTS

- May 2025: TyreSwift and Instavalo launched InstaScan, an AI-powered drive-through vehicle damage inspection system in the U.K., enabling rapid, contactless detection of tire and body damage to improve inspection speed, accuracy and operational efficiency for fleets and service providers.

- March 2025: Stellantis announced the expansion of its mobile service program across the U.S., enabling dealers to provide on-site maintenance and repair services for customers, improving convenience, boosting service retention and supporting dealerships’ parts and service revenue growth.

- February 2025: Self Inspection, a San Diego-based startup with an AI-powered vehicle inspection platform, raised USD 3 million in a seed funding round co-led by Costanoa Ventures and DVx Ventures (with Westlake Financial participating) to accelerate and expand its solution.

- August 2024: Manheim announced the acquisition of Better Tech to enhance under-car digital imaging, thereby strengthening vehicle inspection accuracy and transparency by integrating advanced imaging technology across its auctions to support buyers, sellers, and more efficient wholesale remarketing operations.

- June 2024: AUTOVIN announced that it had rebranded as OPENLANE Inspections, aligning its vehicle inspection services with the OPENLANE marketplace brand. The company will continue to provide condition reports, inspections, and data solutions for commercial, fleet, and remarketing customers across North America.

- May 2024: Click-Ins launched its AI-driven vehicle inspection technology in the U.S., opening a Kansas City headquarters and naming Charles Lukens as CEO as it expands its visual intelligence platform, which delivers highly accurate, mobile-friendly vehicle damage assessments across the automotive sector.

- March 2023: CARS24 launched a pre-owned car market research and development centre in Bengaluru to strengthen its pricing, inspection and remarketing capabilities to improve efficiency, transparency, and customer experience across its used-vehicle ecosystem. They are set to achieve this by leveraging data science and technology.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.1% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Service Type, By Vehicle Type, By Sales Channel, By Vehicle Ownership Type, and By Region |

|

By Service Type |

· Remarketing Services · Inspection Services · Reconditioning Services |

|

By Vehicle Type |

· Hatchback/Sedan · SUV · Light Duty Vehicle · Heavy Duty Vehicle |

|

By Sales Channel |

· Online Channel · Dealer-to-Dealer · Others |

|

By Vehicle Ownership Type |

· Off-lease/Lease Returns · Rental Fleet De-fleet · Corporate/Commercial Fleet |

|

By Region |

· North America (By Service Type, By Vehicle Type, By Sales Channel, By Vehicle Ownership Type, and By Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Service Type, By Vehicle Type, By Sales Channel, By Vehicle Ownership Type, and By Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Service Type, By Vehicle Type, By Sales Channel, By Vehicle Ownership Type, and By Country) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o South Korea (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World (By Service Type, By Vehicle Type, By Sales Channel, By Vehicle Ownership Type, and By Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 79.81 billion in 2025 and is projected to reach USD 137.37 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 38.71 billion.

The market is expected to exhibit a CAGR of 6.1% during the forecast period.

The SUV segment leads the market in terms of vehicle type.

Increasing penetration of Certified Pre-Owned (CPO) Programs to drive market growth.

Key players in the market include Cox Automotive, DEKRA SE, Copart, Inc., and ATS Euromaster are the leading companies in the market.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us