Venous Stents Market Size, Share & Industry Analysis, By Stent Type (Self-Expanding Venous Stents, Balloon-Expandable Venous Stents, and Others), By Material (Nitinol Venous Stents, Stainless Steel Venous Stents, and Others), By Application (Chronic Venous Obstruction, Post-Thrombotic Syndrome, Deep Vein Thrombosis (DVT), May–Thurner Syndrome, and Others), By End-user (Hospitals & ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Venous Stents Market Size and Future Outlook

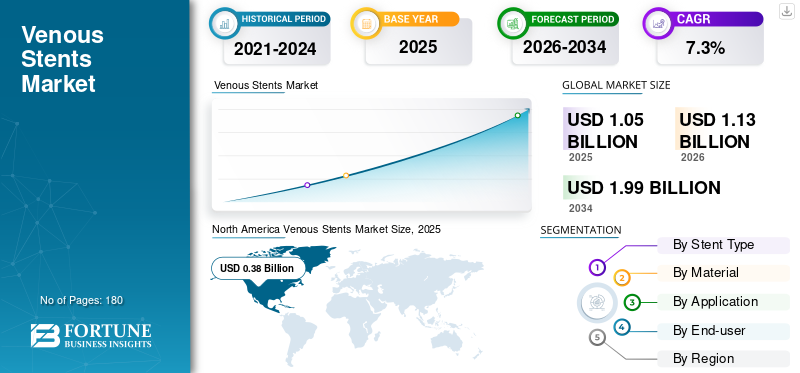

The global venous stents market size was valued at USD 1.05 billion in 2025. The market is projected to grow from USD 1.13 billion in 2026 to USD 1.99 billion by 2034, exhibiting a CAGR of 7.3% during the forecast period. North America dominated the venous stents market with a market share of 36.19% in 2025.

Venous stents are specialized medical devices implanted in veins to restore and maintain adequate blood flow in patients suffering from venous obstructions, stenosis, or compression disorders. The global market is witnessing steady growth due to the rising prevalence of venous diseases, increasing awareness about minimally invasive vascular procedures, and advancements in endovascular technologies.

Furthermore, Boston Scientific Corporation, Cook, and Medtronic held the highest market share in 2025 due to strategic initiatives such as partnerships, collaborations, and new product launches.

Download Free sample to learn more about this report.

Venous Stents Market KEY TAKEAWAYS

- 2025 Market Size: USD 1.05 billion

- 2026 Market Size: USD 1.13 billion

- 2034 Forecast Market Size: USD 1.99 billion

- CAGR: 7.3% from 2026–2034

- North America dominated the venous stents market with a 36.19% share in 2025.

- The self-expanding venous stents segment accounted for the largest market share in 2025.

- The nitinol venous stents segment held the largest market share in 2025.

North America

North America remained the leading regional market, reaching a valuation of USD 0.38 billion in 2025.

Asia Pacific

Asia Pacific is projected to reach approximately USD 0.24 billion by 2026, making it the second-largest regional market.

Europe

Europe is expected to grow at a CAGR of 6.8% during the forecast period, reaching USD 0.32 billion by 2026.

U.S.

U.S. The venous stents market is anticipated to reach USD 0.36 billion by 2026, supported by strong adoption of advanced vascular interventions.

Japan

Japan The market is projected to generate approximately USD 0.05 billion in revenue by 2026, driven by growing demand for minimally invasive treatment options.

Read More

VENOUS STENTS MARKET TRENDS

Development of Dedicated Venous Stent Systems to Emerge as a Key Trend

Currently, key players are focusing on the development of dedicated venous stent systems specifically designed for venous anatomy due to improved radial force, flexibility, and resistance to compression in large veins. Also, several manufacturers are increasingly focusing on innovative designs that enhance long-term patency and reduce complications such as stent migration or restenosis.

- For instance, according to the data published by Sage Journals in April 2021, dedicated venous stent technology is rapidly advancing, paralleling the growing use of endovascular deep venous stenting to treat iliocaval vein conditions.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Prevalence of Chronic Venous Diseases to Fuel Market Expansion

In recent years, there has been an increasing prevalence of chronic venous disorders such as deep vein thrombosis, chronic venous insufficiency, and post-thrombotic syndrome, which often lead to severe complications, including venous obstruction, swelling, pain, and ulcer formation, requiring effective long-term treatment solutions. In such a scenario, venous stents offer improved vessel patency and durable clinical outcomes compared to traditional treatments. This is anticipated to drive the global venous stents market growth.

MARKET RESTRAINTS

High Procedure Costs and Limited Reimbursement to Restrict Market Growth

Despite significant adoption of venous stents, the cost of venous stenting procedures is high due to the need for advanced imaging systems, specialized stent devices, and skilled vascular specialists, which is expected to hamper its adoption in low-and middle-income countries. Also, in these countries, the reimbursement is limited, which is expected to restrict access to such procedures, hindering the market growth.

MARKET OPPORTUNITIES

Expansion of Endovascular Treatment Programs to Create Significant Growth Opportunities

In recent years, there has been a significant expansion of minimally invasive endovascular treatment programs across hospitals and specialized vascular centers, which are increasingly prioritizing minimally invasive procedures due to their advantages, such as shorter hospital stays, reduced complication rates, and faster patient recovery. This is expected to create significant opportunities for the use of venous stents.

Also, emerging markets in the Asia Pacific and Latin America are witnessing improvements in healthcare infrastructure and increased access to advanced vascular interventions, driving further demand for venous stents.

MARKET CHALLENGES

Limited Awareness and Diagnostic Delays to Challenge Market Expansion

In several emerging and underdeveloped countries, there is limited awareness and underdiagnosis of venous diseases due to limited access to care and a shortage of healthcare providers. These factors contribute to delayed treatment and are expected to lower the adoption of venous stenting procedures, challenging the market expansion.

- For instance, according to the Rural Health Statistics (RHS) 2021–2022, data revealed an 83.2% shortage of surgeons in India.

Segmentation Analysis

By Stent Type

Significant Advantage of Self-Expanding Venous Stents Boosted Segment Growth

Based on stent type, the market is segmented into self-expanding venous stents, balloon-expandable venous stents, and others.

To know how our report can help streamline your business, Speak to Analyst

The self-expanding venous stents segment accounted for the largest global venous stents market share in 2025. The segment’s growth is attributed to its superior adaptability and radial strength, which are major factors behind its high adoption among vascular surgeons and interventional radiologists.

Additionally, the balloon-expandable venous stents segment is projected to grow at a CAGR of 8.7% during the forecast period.

By Material

Higher Utilization of Nitinol in Venous Stents by Leading Players Fueled Segment’s Growth

By material, the market is segmented into nitinol venous stents, stainless steel venous stents, and others.

The nitinol venous stents segment accounted for the largest market share in 2025. The segment’s growth is attributed to its unique mechanical properties, such as superelasticity, shape memory, and high corrosion resistance, which are driving its usage in venous stents of manufacturers, including Medtronic, Boston Scientific Corporation, and Cook.

Additionally, the stainless steel venous stents segment is anticipated to grow at a CAGR of 5.3% over the forecast period.

By Application

Growing Prevalence of Long-Standing Venous Blockages and Compression Syndromes Boosted Chronic Venous Obstruction Segment’s Growth

By application, the market is classified into chronic venous obstruction, post-thrombotic syndrome, deep vein thrombosis (DVT), May–Thurner syndrome, and others.

The chronic venous obstruction segment accounted for the largest market share in 2025. The growth is attributed to the growing prevalence of long-standing venous blockages and compression syndromes that often lead to persistent venous narrowing, causing symptoms including swelling, pain, and skin changes. In such a condition, venous stenting serves as an effective treatment option for restoring blood flow, driving its adoption. Moreover, the segment is projected to hold a 36.6% share in 2026.

Additionally, the post-thrombotic syndrome segment is expected to grow at a CAGR of 6.9% during the forecast period.

By End-user

Large Number of Hospitals & ASCs in Developed Countries Propelled Segment’s Growth

On the basis of end-user, the market is segmented into hospitals & ASCs, specialty clinics, and others.

In 2025, hospitals & ASCs dominated the market by end-users. The growth is attributed to a significant number of hospitals in the developed countries, such as the U.S., U.K., Germany, and France, which contribute to the majority of venous stenting procedures due to the availability of advanced infrastructure and specialized vascular care teams. This is expected to fuel the segment’s growth. Furthermore, the segment is set to hold 71.9% share in 2026.

- For instance, according to the American Hospital Association (AHA) Fast Facts, as of early 2025, there are 6,093 total hospitals in the U.S.

In addition, the specialty clinics segment is projected to grow at a CAGR of 9.5% during the forecast period.

Venous Stents Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Venous Stents Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest share of revenues in 2024, valued at USD 0.36 billion, and also reached a valuation of USD 0.38 billion in 2025. The growth is driven by the high prevalence of chronic venous diseases, strong healthcare infrastructure, and early adoption of advanced endovascular technologies, which are expected to favor the adoption of venous stents in the region.

U.S. Venous Stents Market

In 2026, the U.S. is anticipated to reach USD 0.36 billion, accounting for approximately 31.8% of the global market.

Asia Pacific

By 2026, the Asia Pacific’s market is projected to reach approximately USD 0.24 billion, making it the second-largest market globally. The growth is attributed to the rising incidence of deep vein thrombosis and chronic venous obstruction due to aging populations and lifestyle changes, which is influencing key players to expand product presence in the region.

Japan Venous Stents Market

Japan is projected to generate approximately USD 0.05 billion in revenue by 2026, representing nearly 4.0% of the global market.

China Venous Stents Market

China’s market is anticipated to reach around USD 0.08 billion by 2026, accounting for nearly 7.2% of global revenues.

India Venous Stents Market

India’s market is expected to generate approximately USD 0.04 billion by 2026, representing around 3.2% of the global market revenue.

Europe

Europe is projected to record a 6.8% growth rate during the forecast period, the third-highest globally, reaching USD 0.32 billion by 2026. The growth is attributed to well-established healthcare systems in Germany, the U.K., and France, which are expected to boost the adoption of venous stents in the region.

U.K. Venous Stents Market

The U.K. market is projected to reach USD 0.06 billion by 2026, representing approximately 5.4% of global revenues.

Germany Venous Stents Market

Germany's market is predicted to reach around USD 0.07 billion by 2026, representing around 6.5% of global revenue.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate growth, with the Latin America market estimated to reach approximately USD 0.09 billion by 2026. The growing awareness among healthcare professionals is encouraging the use of venous stents for treating chronic venous obstruction and post-thrombotic syndrome, supported by improved healthcare access in these regions.

GCC Venous Stents Market

By 2026, the GCC market is estimated to reach approximately USD 0.03 billion, representing around 2.6% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Portfolios and Extensive Distribution Network to Strengthen Market Position of Key Players

In 2025, Boston Scientific Corporation, Cook, and Medtronic held the largest global market share. This share is attributed to their strong vascular intervention portfolios and extensive distribution networks. Also, these companies are focused on new product innovations dedicated to various applications to broaden their portfolio.

Moreover, other major players are focused on strengthening their presence in international markets through expanded regulatory approvals and partnerships with healthcare institutions, which is expected to improve their market share.

LIST OF KEY VENOUS STENTS COMPANIES PROFILED IN REPORT

- BD (U.S.)

- Boston Scientific Corporation (U.S.)

- Medtronic (Ireland)

- Koninklijke Philips N.V. (Netherlands)

- optimed Medizinische Instrumente GmbH (Germany)

- Cook (U.S.)

- Bentley InnoMed GmbH (Germany)

- Merit Medical Systems (U.S.)

- Sinomed (China)

- MicroPort Scientific Corporation (China)

KEY INDUSTRY DEVELOPMENTS

- January 2026: L. Gore & Associates received FDA approval for the GORE VIABAHN FORTEGRA venous stent, the first device indicated for treating deep venous disease in the IVC, iliac, and iliofemoral veins.

- February 2025: Serenity Medical announced the publication of 1-year results from the RIVER study in the Journal of NeuroInterventional Surgery, marking the first prospective multicenter trial of the River venous sinus stent for treating Idiopathic Intracranial Hypertension (IIH) in medication-refractory patients.

- October 2024: Cook announced results from the VIVO clinical study showing that the Zilver Vena venous self-expanding stent demonstrated sustained high patency rates for up to three years in patients with iliofemoral venous obstruction.

- June 2024: Koninklijke Philips N.V. launched the Duo Venous Stent System following FDA premarket approval, featuring Duo Hybrid and Duo Extend stents for treating symptomatic venous outflow obstruction in chronic venous insufficiency patients.

- May 2022: BD's Venovo venous stent returned to the U.S. market following a 2021 recall, after completing required post-market surveillance and receiving updated FDA clearance.

- December 2021: Vesper Medical, Inc. announced the completion of enrollment in its pivotal VIVID clinical trial, achieving the key milestone ahead of schedule with 160 patients across U.S. and European centers.

- October 2021: MicroPort Scientific Corporation completed enrollment in the pre-market multicenter clinical trial for its Vflower venous stent system after just 10 months, achieving 100.0% success in device, technical, and procedural outcomes.

REPORT COVERAGE

The global venous stents market report offers a comprehensive analysis of all market segments, examining the key drivers, emerging trends, growth opportunities, major restraints, and challenges influencing the market landscape. It also provides insights into technological advancements, the prevalence of related diseases, notable industry developments, market share analysis of leading companies, and detailed profiles of key market players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Stent Type, Material, Application, End-user, and Region |

| By Stent Type |

|

| By Material |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.05 billion in 2025 and is projected to reach USD 1.99 billion by 2034.

In 2025, the North Americas market value stood at USD 0.38 billion.

The market is expected to exhibit a CAGR of 7.3% during the forecast period of 2026-2034.

Self-expanding venous stents segment led the market by stent type.

The key factor driving the market is the rising prevalence of chronic venous diseases.

Boston Scientific Corporation, Cook, and Medtronic are among the prominent players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us