Liquefied Natural Gas Market Size, Share & Industry Analysis, By Type (LNG Liquefaction and LNG Regasification), By Application (Power Generation, Industrial, Transportation, Residential, and Others), and Regional Forecast, 2025-2032

Liquefied Natural Gas Market Size

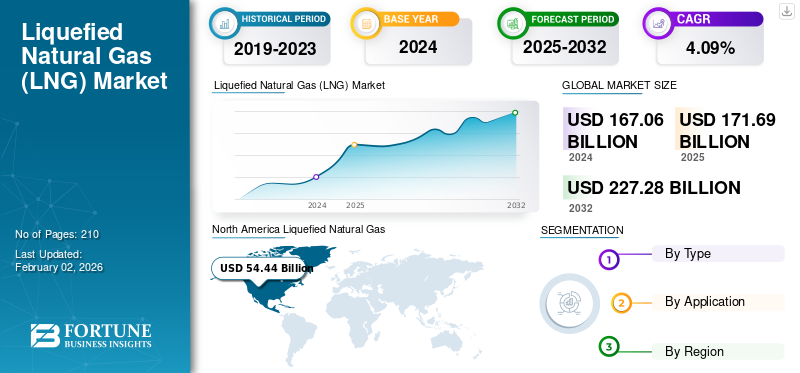

The global liquefied natural gas market size was valued at USD 167.06 billion in 2024 and is projected to grow from USD 171.69 billion in 2025 to USD 227.28 billion by 2032, exhibiting a CAGR of 4.09% during the forecast period. The North America region dominated the LNG market with 32.58% market share in 2024.

The global liquefied natural gas market is undergoing structural transformation, supported by energy security priorities, fuel diversification strategies, and the transition toward lower-emission energy sources. Liquefied natural gas has moved beyond its historical role as a balancing fuel and increasingly functions as a strategic component of global energy systems. Market expansion is influenced by supply diversification, rising natural gas exports, and accelerating investment in infrastructure across importing and exporting economies.

Download Free sample to learn more about this report.

Liquefied Natural Gas (LNG) Market Key Takeaways

- 2024 Market Size: USD 167.06 billion

- 2025 Market Size: USD 171.69 billion

- 2032 Forecast Market Size: USD 227.28 billion

- CAGR: 4.09% from 2025–2032

- North America dominated the liquefied natural gas market with a 32.58% share in 2024.

- LNG liquefaction facilities accounted for the largest market share.

- The industrial segment is expected to dominate the market during the forecast period.

Asia Pacific

Rising urbanization and cleaner energy adoption continue to strengthen LNG demand.

North America

Abundant shale gas reserves and export infrastructure support continued LNG market growth.

Europe

LNG demand remains supported by energy diversification and evolving import infrastructure.

U.S.

Expanding export terminals and abundant shale gas reinforce its position as a leading LNG exporter.

Japan

Strong import demand supports national energy security and power generation requirements.

Read More

Key Market Insights

- The global liquefied natural gas (LNG) market was valued at USD 167.06 billion in 2024 and is projected to grow from USD 171.69 billion in 2025 to USD 227.28 billion by 2032, reflecting sustained demand for cleaner energy alternatives across industrial and power generation sectors.

- Rising natural gas demand and the transition away from coal and oil are expected to accelerate LNG adoption, supported by growing investments in import terminals, liquefaction infrastructure, and cross-border gas trade.

- Asia Pacific LNG market is driven by strong consumption across major importing economies and increasing reliance on LNG to meet industrial, residential, and electricity generation requirements.

- Power generation remains a major application area for LNG, as governments and utilities increasingly position natural gas as a transition fuel to support energy security and lower carbon emissions relative to conventional fossil fuels.

Demand continues to strengthen as governments and industrial operators seek alternatives to coal and oil-based systems. Power plants remain a major consumption center, particularly in economies transitioning toward lower-carbon electricity generation. Industrial users are also increasing their adoption to improve energy efficiency and secure a stable fuel supply in energy-intensive sectors.

The Liquefied Natural Gas market signifies the global trade and infrastructure network involved in the process of cooling natural gas to a liquid state for transportation and storage, and then converting it back to its gaseous form for consumption. This market enables the movement of natural gas to areas not reachable by pipelines, facilitating global energy distribution.

The liquefied natural gas market is expected to witness significant growth owing to factors such as increasing demand for cleaner energy sources, growing economic growth, especially in the Asia Pacific, and increased use of LNG applications in industries. In addition, there is a rising demand for electricity, particularly from power generation using natural gas as a lower-carbon alternative to coal.

- According to the International Energy Agency, India’s natural gas demand is expected to increase by 60% by 2030 owing to the rapid growth in the country’s energy landscape.

Furthermore, the growing applications as a transportation fuel and the rise of LNG bunkering in the maritime industry also contribute to market expansion.

Qatar Energy LNG is a prominent player in the global market, holding the title of the world's largest LNG company. They produce and supply a significant volume of LNG, with a total production capacity of 77 million metric tons per annum (MTPA). Their dominance is rooted in access to the North Field, the world's largest non-associated gas field, which offers natural gas to their LNG trains.

The United States has emerged as a pivotal contributor to trade due to its abundant shale gas resources and growing liquefaction capacity. Rising export activity from North America is reshaping trade flows and intensifying competition among established suppliers in the Middle East, Africa, and Asia-Pacific regions. Import terminals are expanding globally, reflecting growing concerns around supply resilience and geopolitical uncertainty.

Technological advancements in liquefaction efficiency, storage systems, and gas marketing infrastructure are supporting cost optimization and operational scalability. Small-scale LNG solutions are gaining relevance in transportation and distributed energy applications, particularly in regions with limited pipeline access. Imports are increasingly integrated into national energy security frameworks, improving market resilience.

Latest LNG Market Trends

Growing Demand for Floating LNG Infrastructure is expected to Fuel Market Growth.

The demand for Floating (FLNG) infrastructure is growing rapidly, driven by rising global demand, especially in regions with limited onshore infrastructure and the need for flexible, cost-effective solutions. FLNG systems, such as Floating Storage and Regasification Units (FSRUs) and floating liquefaction facilities, offer deployment speed, cost, and adaptability advantages. This growth is projected to rise, particularly in Asia, Europe, and Latin America, as countries seek to expand infrastructure.

- In May 2025, Hoegh Evi signed a charter agreement with EGAS to deploy a floating storage and regasification unit at the Port of Sumed, Egypt, by 2026 to boost Egypt's import capacity.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Emissions Reductions in Heavy Industry and Transport are Driving Market Growth

The shift toward natural gas-based vehicles is driving the market growth. This transition is due to the awareness regarding pollution caused by diesel and gasoline vehicles. According to the European Commission’s impact study accompanying the CO2 standards proposal for heavy-duty vehicles, LNG engines could have ~20 % lower TTW CO2 emissions as compared to diesel vehicles. The shift to LNG trucks would also have an optimistic effect on air pollutant emissions. In addition, due to its molecular structure, methane has less carbon content than diesel and produces less CO2 per unit of energy.

Growth in the liquefied natural gas market is supported by increasing global energy demand and the strategic need for supply diversification. Many countries are reducing dependence on single-source pipeline systems and expanding imports to improve energy security. This transition has accelerated following geopolitical disruptions that exposed vulnerabilities in traditional energy supply structures.

Rising demand from power plants remains a primary growth catalyst. Utilities increasingly use natural gas as a transition fuel due to lower emissions intensity compared to coal. Industrial facilities are also adopting LNG to stabilize energy supply and improve operational efficiency in energy-intensive manufacturing processes.

Furthermore, LNG is gaining prominence as a cleaner alternative fuel for heavy marine vessels, offering significant reductions in greenhouse gas emissions compared to traditional fuels such as HFO. While LNG is a transitional fuel, its adoption is growing due to its immediate environmental benefits and potential for future advancements in alternative fuels.

For instance, in June 2024, Mitsubishi Shipbuilding launched an LNG-fuelled RoRo vessel in Japan, aligning with the carbon reduction objective in the marine industry.

In December 2024, Adani Ports and Special Economic Zone (APSEZ) announced the docking of the first LNG-powered container marine vessel, reflecting the industry's shift toward low-carbon fuels and contributing to the global transition to sustainable marine fuels and practices.

LNG Infrastructure Development to Drive Market Growth

The expansion of Liquefied Natural Gas infrastructure is a significant driver of the market, facilitating global trade and meeting increasing energy demands. Investments in liquefaction facilities, regasification terminals, storage, and transportation networks enhance supply chain reliability and accessibility, making it more attractive for diverse applications such as power generation and industrial use.

Investment momentum is also driven by technological advancements in liquefaction efficiency, shipping, and regasification systems. Modern import terminals are improving operational flexibility and lowering handling costs. Small-scale LNG networks are expanding access to underserved regions, particularly where pipeline development remains economically unviable. These factors collectively support sustained liquefied natural gas market growth and strengthen long-term market visibility.

In May 2025, Deutsche Energy Terminal GmbH announced the initiation of operations at the Wilhelmshaven 2 LNG terminal in Germany. This terminal is equipped with regasification capacity up to 4.6 billion cubic meters (bcm) of LNG per year by 2027. Such large-scale developments are expected to fuel the growth of the market, especially in regions with high energy demand in the near future.

MARKET RESTRAINTS

Price Volatility and Supply Imbalances to Restrain Market Demand

The Liquefied Natural Gas market growth is restrained by both price volatility and supply imbalances. Price volatility is driven by shipping costs, geopolitical events, and supply-demand discrepancies, making prices vulnerable to fluctuations. In recent times, geopolitical turmoil has become a major reason for volatility in the supply and prices. For instance, according to World Bank commodities price data, the natural gas Europe index price witnessed a significant decline of 67.50% in 2023 from 2022 and 16.40% in 2024. Uncertain price fluctuations are expected to restrain market growth globally in the near future.

The liquefied natural gas market faces structural challenges related to capital intensity, pricing volatility, and infrastructure complexity. Production facilities require substantial upfront investment, with liquefaction terminals often involving long construction cycles and complex financing arrangements. These conditions create barriers to entry and increase project execution risk.

Gas price volatility remains a persistent constraint across the value chain. Fluctuations in natural gas prices affect procurement economics, profitability, and contracting strategies for both buyers and suppliers. Sudden shifts in regional demand or geopolitical instability can intensify price uncertainty, influencing purchasing behavior and delaying investment decisions.

Furthermore, geopolitical events cause changes in shipping routes as maritime security becomes a major factor in geopolitical problems. Major recent geopolitical events include the Russia-Ukraine War and the Iran-Israel War. Most of the energy and world trade takes place through the Strait of Hormuz, which is near Iran, and the conflict in the region could create problems for the countries importing energy through that route.

Regulatory and environmental concerns are becoming increasingly relevant. Permitting requirements for export facilities, storage systems, and import terminals continue to tighten across multiple regions. Carbon emissions scrutiny may also influence financing conditions, particularly among institutional investors prioritizing sustainability metrics.

Infrastructure bottlenecks create additional limitations. Many emerging economies lack adequate import capacity, storage networks, and regasification facilities. Transportation logistics also remain vulnerable to shipping disruptions and vessel availability constraints. Competition from renewable energy sources may moderate long-term demand growth, introducing uncertainty into future market expansion.

MARKET OPPORTUNITIES

Economic Growth in the Asia Pacific is Expected to Lead Market Growth

The market presents significant opportunities driven by rising demand in emerging economies and expanding applications beyond traditional sectors. Economic growth in the Asia Pacific, particularly, is fueling demand for LNG as a cleaner energy source for power generation, industrial processes, and transportation.

The liquefied natural gas market presents meaningful opportunities through expanding energy access, industrial fuel switching, and infrastructure modernization. Many developing economies continue to experience energy shortages, creating strong potential for imports as governments diversify fuel supply sources. Countries with limited domestic natural gas production increasingly view liquefied natural gas LNG as a strategic mechanism to strengthen energy resilience and reduce supply disruptions.

Power generation offers a substantial opportunity across emerging and developed economies. Coal-to-gas transitions are accelerating as policymakers seek cleaner energy sources capable of balancing renewable intermittency. LNG-powered power plants provide operational flexibility and support grid stability, particularly in markets where renewable infrastructure remains insufficient to meet baseload demand.

As global energy demand increases, particularly in emerging economies, LNG ensures energy security while aligning with global decarbonization targets. LNG is increasingly being adopted as a cleaner alternative to coal and oil, emitting up to 40% less emissions than coal, nearly zero sulfur, and particulate matter.

According to the Institute for Energy Economics and Financial Analysis, global supply is expected to increase to 666.5 MTPA by 2028, which surpasses International Energy Agency (IEA) demand scenarios through 2050.

China, India, and Southeast Asia are increasing their infrastructure to meet electricity demands for growing urban populations and industrial sectors. For instance, in May 2025, THINK Gas announced the expansion of its LNG network with the launch of 6 new dispensing stations to support India’s green transition.

Investment opportunities are increasing across import terminals and regasification infrastructure. Emerging economies in Asia-Pacific, Latin America, and parts of the Middle East and Africa continue expanding LNG receiving capacity to address rising electricity demand and industrial growth. Institutional investors increasingly evaluate investing in infrastructure as a long-duration asset class with relatively stable utilization potential.

Small-scale LNG deployment presents additional growth visibility. Mining operations, industrial clusters, and remote manufacturing facilities are increasingly adopting LNG when pipeline access is unavailable or economically unviable. Transportation fuel applications are also expanding, particularly in marine logistics.

MARKET CHALLENGES

Potential Geopolitical Conflicts to Create Challenges for Market Players

Geopolitical risks significantly impact the market, potentially disrupting supply, increasing price volatility, and affecting investment decisions. These risks include regional conflicts, trade disputes, and political instability, which can disrupt supply chains, damage infrastructure, and alter trade patterns.

For instance, the Israel-Hamas war and the Russia-Ukraine conflict have led to regional instability and disruption of LNG flows and infrastructure. In June 2025, the closure of the Leviathan gas field due to the Israel-Hamas conflict impacted pipeline flows to Egypt. Moreover, Disruptions or blockades at critical maritime areas, such as the Strait of Hormuz or the Red Sea, can impact LNG tanker routes, increasing shipping costs and potentially delaying deliveries, which is expected to create numerous challenges for the market players in the near future.

IMPACT OF TARIFFS

Tariffs implemented by the U.S. government have a multi-faceted impact on the global LNG industry, primarily through their effect on global trade and economic activity. Some tariffs directly affect trade; for instance, due to the U.S.’s tariff on goods coming to the U.S. from China as a retaliatory action, China imposed a 15% tariff on U.S. imports to China. In February 2025, the overall impact is more indirect, affecting global demand and investment decisions. The tariffs on the products manufactured by China would negatively impact the industrial activity in China, leading to less energy demand. This would be impacting the market. Furthermore, tariffs increase infrastructure costs, particularly in the U.S., due to higher prices for steel and other materials used in LNG terminal construction. The uncertain tariff rates can delay or hinder the final investment decisions for new projects, which are crucial for increasing supply.

SEGMENTATION ANALYSIS

By Type

Increasing LNG Trade is Anticipated to Propel the Growth of the Infrastructure Segment

Based on type, the market is segmented into liquefaction and regasification.

LNG Liquefaction

LNG liquefaction facilities currently dominate the market with a larger share due to increased global demand and the ability to easily transport and store natural gas in liquid form. The segment is experiencing significant growth globally due to the increasing demand for cleaner energy and the need to transport natural gas to regions lacking pipeline access. This involves the construction of facilities that cool natural gas to a liquid state, enabling efficient storage and transportation via specialized ships. The development of LNG infrastructure is crucial for enabling global trade and meeting the energy needs of various countries.

LNG liquefaction represents the supply-side foundation of the liquefied natural gas market and remains one of the most capital-intensive segments across the value chain. Liquefaction facilities convert natural gas into liquid form through advanced cryogenic processes, enabling cost-efficient transport to markets where pipeline connectivity remains unavailable or commercially impractical. The segment remains strategically concentrated among major export-oriented economies with abundant gas reserves and large-scale infrastructure capacity.

Rising natural gas exports from North America continue reshaping global LNG market dynamics, increasing supply diversification while reducing dependence on historically dominant exporters. Major production hubs in Qatar, Australia, and the Middle East and Africa continue strengthening competitive positioning through low-cost feedstock access and infrastructure efficiency.

Capital allocation within the segment continues to favor projects supported by long-term contracts and predictable demand visibility. Procurement teams increasingly evaluate supplier resilience, export LNG capabilities, and geopolitical stability before entering purchasing agreements. This is especially relevant as trade patterns become increasingly diversified.

LNG Regasification

LNG regasification serves as the downstream conversion gateway of the liquefied natural gas market and plays an increasingly important role in national energy planning. Regasification facilities convert imported LNG back into gaseous form for transmission into domestic energy systems. The segment is expanding rapidly as countries seek diversified energy sources and reduce exposure to geopolitical supply instability.

Demand growth remains strongest in regions lacking sufficient domestic gas production or stable cross-border pipeline networks. Asian economies continue to dominate LNG imports due to great industrial demand and limited indigenous supply. Europe has also accelerated investment in import terminals following supply disruptions that increased emphasis on energy resilience and sourcing diversification.

Regasification facilities are also growing, primarily driven by rising imports and the need to diversify energy sources.

- In July 2024, DESFA launched the first regional storage and gasification station catering to Central and Western Macedonia in Greece. Developing robust infrastructure in smaller countries will propel market growth over the forecast period.

Moreover, regasification facilities are expected to have a significant growth rate owing to the increased demand for cleaner energy, geopolitical factors, and technological advancements, which is supported by strong LNG demand in the Asia Pacific region, where China and India are projected to consume significantly more natural gas than they can produce domestically, leading to greater reliance on LNG imports and the need for more regasification infrastructure in future.

Floating storage and regasification units are significantly reshaping deployment economics. Compared with traditional onshore facilities, these systems offer lower upfront costs and faster commissioning timelines. Countries pursuing immediate energy diversification increasingly view floating systems as practical alternatives to conventional infrastructure.

Investment in import infrastructure continues to expand throughout Asia-Pacific, Latin America, and select African economies. Policymakers increasingly position LNG-powered power plants as transitional assets capable of stabilizing electricity grids while supporting broader decarbonization goals. Import terminals are also becoming critical components of national energy security strategies.

By Application

To know how our report can help streamline your business, Speak to Analyst

Rising LNG Demand in the Industrial Processes to Aid Market Growth

Based on application, the market is broadly categorized into power generation, industrial, transportation, residential, and others.

Industrial

The industrial segment is expected to have the largest market share over the forecast period. Industrial demand is surging due to its versatility and cleaner-burning properties compared to traditional fossil fuels. It is used in various sectors for heating, drying, and powering in food processing, manufacturing, and steel production. Additionally, LNG serves as a raw material for fertilizers and plastics, and it is increasingly adopted in transportation as a cleaner fuel for trucks and ships.

The industrial segment represents a major consumption center within the liquefied natural gas market, driven by energy-intensive manufacturing, chemicals, refining, metals, and heavy industrial processing. LNG increasingly serves as an alternative to coal and fuel oil, helping industrial operators improve emissions performance while maintaining energy reliability.

Energy-intensive facilities continue prioritizing supply stability due to the direct relationship between fuel costs and operating margins. Industrial users are increasingly adopting LNG when pipeline access is inconsistent or unavailable. This trend is particularly evident in export-oriented manufacturing economies seeking greater energy diversification.

Demand remains strong among sectors requiring high-temperature process heat, including cement, steel, ceramics, and petrochemicals. Companies increasingly compare LNG against competing energy sources based on emissions obligations, procurement flexibility, and long-term affordability.

- In April 2024, GreenLine Mobility Solutions Ltd launched an LNG truck fleet for logistics operations for Bekaert’s plant in Maharashtra, India.

Transportation

Transportation represents an expanding application segment within the liquefied natural gas market, supported by tightening environmental regulations and increasing pressure to reduce emissions across heavy-duty transport systems. LNG adoption is particularly visible in maritime shipping, where international emissions standards continue accelerating the transition away from conventional marine fuels. As shipping operators modernize fleets, liquefied natural gas LNG is increasingly viewed as a commercially viable transitional fuel with lower sulfur and particulate emissions.

The maritime industry accounts for a substantial portion of transportation-related demand for LNG. Shipping companies are increasing investment in LNG-fueled vessels to comply with emissions mandates while improving long-term operating economics. Growth in bunkering infrastructure near major ports is improving fuel accessibility, particularly across Europe and the Asia-Pacific. This infrastructure expansion strengthens confidence in LNG adoption across international shipping corridors.

Furthermore, the transportation segment is expected to grow significantly, driven by the need for efficient and long-range fuel options, particularly for long-haul vehicles such as trucks and ships. LNG, a compressed form of natural gas, offers a higher energy density per volume than natural gas in its gaseous form, allowing for greater fuel storage capacity and longer driving ranges. This makes it a compelling alternative for heavy-duty transportation, where fuel efficiency and range are critical.

Power Generation

Power generation represents the largest application segment within the liquefied natural gas market, supported by increasing electricity demand and accelerating fuel-switching initiatives. Utilities continue transitioning from coal-based systems toward natural gas due to lower emissions intensity and greater operational flexibility. LNG-powered power plants increasingly function as balancing assets supporting renewable integration while maintaining grid stability.

Emerging economies remain particularly important growth centers for LNG-based electricity generation. Countries facing power shortages increasingly rely on imports to diversify electricity sources and improve supply reliability. This trend is especially visible in rapidly urbanizing economies where electricity consumption continues to increase alongside industrial activity.

Operational flexibility remains one of LNG’s strongest advantages within power generation. Gas-fired facilities can ramp production more rapidly than coal systems, supporting grid balancing requirements during fluctuations in renewable output. This capability strengthens LNG’s role within broader energy transition frameworks and long-term infrastructure planning.

Residential

The residential segment maintains a comparatively smaller yet strategically relevant position within the liquefied natural gas market, particularly across regions lacking mature gas distribution systems. LNG functions as an alternative energy source for heating, cooking, and localized electricity generation where traditional natural gas pipelines remain unavailable or economically unfeasible. Adoption patterns vary considerably depending on affordability, climate conditions, and government energy policies.

Emerging economies increasingly incorporate LNG into decentralized residential energy systems to strengthen energy access and reduce dependence on coal, diesel, and biomass. Demand remains particularly visible in remote communities, island economies, and colder regions requiring a stable heating supply. Imports increasingly support regional energy diversification strategies where domestic production remains constrained.

Small-scale LNG distribution continues to improve accessibility. Mobile storage systems, localized regasification units, and modular delivery infrastructure are expanding reach while reducing logistics complexity. Policymakers in some countries also encourage LNG usage to strengthen residential energy reliability and reduce environmental impacts associated with higher-emission fuels.

Price sensitivity remains a defining challenge. Residential consumers are highly exposed to gas price fluctuations, limiting adoption during periods of elevated costs. Electrification initiatives and renewable-based heating alternatives may also moderate long-term demand growth.

Regional Insights

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America Liquefied Natural Gas Market Analysis

North America Liquefied Natural Gas (LNG) Market Size, 2024 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Increasing LNG Export Drives Market Growth in North America

North America is a major global market driven by significant natural gas reserves, particularly in the U.S. and Canada. It encompasses the entire value chain, from production and liquefaction to export and distribution, with major companies such as Cheniere Energy and Dominion Energy playing key roles.

North America represents a strategically significant liquefied natural gas market, supported by abundant shale gas reserves and large-scale export infrastructure. Regional growth is driven by rising natural gas exports, expanding liquefaction capacity, and strong investment in infrastructure. Demand remains linked to industrial activity and energy security priorities, strengthening the region’s position within global market dynamics.

United States Liquefied Natural Gas Market

Rising LNG production to Propel Market Growth in the Country

The U.S. has become a leading liquefied natural gas exporter, driven by abundant domestic resources and expanding export infrastructure. LNG exports are vital for meeting global energy demand, particularly in Europe, and have become a key factor in the global energy transition. The U.S. LNG industry is expected to continue expanding, driven by international demand and the development of new export facilities.

- In June 2025, TotalEnergies announced an agreement with NextDecade to procure 1.5 Mtpa of LNG for 20 years for Train 4 at the Rio Grande LNG facility, located in Texas, U.S.

The United States dominates the regional market size due to extensive shale gas production and rapidly expanding production capabilities. Increasing natural gas exports continue to reshape trade flows, strengthening global supply diversification.

Investment in liquefaction terminals and export infrastructure remains robust. The market benefits from technological advancements, strong private capital participation, and expanding international procurement agreements.

Europe Liquefied Natural Gas Market Analysis

Increasing LNG Imports in the Region to Boost Market Growth

The European market is expected to grow moderately due to fluctuating demand and a shift toward more sustainable energy sources. However, imports have been impacted by reduced gas demand due to renewable energy adoption and lower overall gas consumption. They are also expected to increase in the coming years, particularly with the commissioning of new projects in North America and Qatar in the near future.

- In March 2025, Securing Energy for Europe (SEFE) signed an agreement with Delfin Midstream to supply LNG from the coast of Cameron, Louisiana, on the U.S. Gulf Coast. Increasing trade in the region is expected to foster infrastructural development in the near future.

Europe’s liquefied natural gas market is expanding as countries prioritize energy diversification and reduce pipeline dependency. Rising imports and accelerated investment in import terminals continue to strengthen supply resilience.

Demand remains influenced by industrial activity, heating requirements, and electricity generation needs. Energy security concerns increasingly position LNG as a strategic component of regional energy systems.

Germany Liquefied Natural Gas Market

Germany continues expanding its import capacity to diversify supply sources and strengthen domestic energy resilience. Investment in floating import terminals and regasification infrastructure remains central to long-term planning.

Industrial demand and electricity generation requirements continue to support adoption. The country increasingly views liquefied natural gas LNG as an important transitional fuel within evolving energy frameworks.

United Kingdom Liquefied Natural Gas Market

The United Kingdom maintains an established liquefied natural gas market supported by mature import infrastructure and strong trade participation. Demand remains concentrated across power plants, industrial users, and residential consumption.

Market dynamics increasingly reflect energy security priorities and procurement diversification strategies. Continued infrastructure optimization supports resilience against supply disruptions and price fluctuations.

Asia-Pacific Liquefied Natural Gas Market Analysis

Significant Shift toward Adoption of Natural Gas Drives Market Growth

The Asia Pacific market is expected to grow rapidly, particularly in China, Southeast Asia, and South Asia, due to increased urbanization and the need for cleaner energy. This growth will be fueled by a shift toward natural gas as a transition fuel and a need to support energy security as China, Japan, and South Korea expand their energy portfolios. The region is also expected to remain the largest destination for imports, with a significant portion of global trade attributed to the Asia Pacific.

- In February 2025, TotalEnergies announced plans to supply Gujarat State Petroleum Corporation Limited (GSPC) under a sale and purchase agreement (SPA) to supply GSPC with 400,000 tons of LNG.

Asia-Pacific represents the largest regional liquefied natural gas market, driven by rising electricity demand, industrialization, and increasing imports. Countries across the region continue investing in infrastructure to support economic growth and strengthen energy access. Demand for LNG remains especially strong among industrial users and utilities seeking cleaner alternatives to coal-based systems.

Japan Liquefied Natural Gas Market

Japan remains a leading import market due to limited domestic energy resources and substantial electricity demand. LNG continues playing a central role in national energy planning and power generation strategies.

Procurement diversification and long-term supply agreements remain critical priorities. Technological advancements and infrastructure efficiency continue to support stable market operations and energy security.

China Liquefied Natural Gas Market

Rising Demand of Natural Gas for Power Generation and Industrial Propels Market Growth across the Country

The LNG market in China is expected to have a significant share of the global market, driven by rising demand for natural gas for power generation and industrial applications, and a push to reduce coal reliance and improve air quality. While domestic gas production and pipeline imports also contribute to China's gas demand growth and overall energy supply, imports remain a major factor in meeting the nation's growing energy needs.

- According to the U.S. Energy Information Administration, China is the world's largest importer of LNG in 2023, with its imports averaging 9.5 bcf/d. Hence, this signifies the increasing growth of the market over the forecast period.

China demonstrates strong liquefied natural gas market growth, supported by industrial expansion, urbanization, and environmental policy priorities. Rising imports continue supporting coal-to-gas transition strategies across industrial and residential sectors.

Investment in import terminals and storage infrastructure remains substantial. The country increasingly strengthens trade participation to diversify supply and improve energy resilience.

Latin America Liquefied Natural Gas Market Analysis

Limited LNG Import/Export Infrastructure leads to Moderate Growth

The Latin American market is driven by increasing demand, particularly for power generation, and growing regional imports. While the region has significant natural gas resources, including shale gas, it is unlikely to become a major exporter in the near future due to infrastructure limitations and energy resource development challenges.

However, Brazil is expected to be a key player in the region's market, with a high CAGR. Growing investment in import infrastructure and gas-fired power plants is expected to support the region's growing energy demands and promote energy security over the forecast period.

Latin America presents emerging opportunities within the liquefied natural gas market, supported by rising electricity demand and infrastructure modernization. Countries increasingly invest in imports and regasification facilities to reduce fuel shortages and strengthen energy reliability.

Industrial activity and expanding power generation capacity continue to support the long-term adoption across several developing economies.

Middle East & Africa Liquefied Natural Gas Market Analysis

Government Efforts to Reduce Reliance on Traditional Fuels are Expected to Drive Market Growth

The Middle East & Africa market is characterized by a growing demand for cleaner energy, particularly for power generation, and a focus on sustainable shipping practices driven by government efforts to reduce reliance on traditional fuels and meet decarbonization targets.

Furthermore, the Middle East & Africa region is actively adopting as a transition fuel, especially in remote areas with less availability of conventional energy infrastructure. This trend has supported investments in LNG-ready ports, storage facilities, and other necessary components.

The Middle East and Africa remain strategically important due to strong production capacity and expanding export activity. Major producers continue strengthening liquefaction capabilities while select importing nations increase infrastructure investment.

Regional growth reflects both supply-side leadership and increasing domestic demand for cleaner energy sources across the industrial and electricity sectors.

Liquefied Natural Gas Industry Competitive Landscape

The liquefied natural gas market is characterized by a concentrated competitive structure, where integrated energy companies, national oil enterprises, infrastructure developers, and trading firms collectively shape supply availability and pricing dynamics. Market share remains largely concentrated among organizations with upstream gas reserves, liquefaction capabilities, shipping access, and downstream distribution networks. Competitive positioning increasingly depends on infrastructure scale, supply reliability, contract flexibility, and geographic diversification.

Major participants continue strengthening vertical integration strategies to improve profitability and reduce operational risk exposure. Companies with control across production, shipping, regasification, and gas marketing activities maintain stronger resilience during periods of gas price volatility. This integrated operating model enables suppliers to optimize cargo allocation and strengthen bargaining power across regional trade routes.

The United States has emerged as a major competitive force due to abundant shale gas production and expanding liquefaction infrastructure. Export activity from North America continues to intensify competition with established producers in Qatar, Australia, and the Middle East and Africa. Suppliers increasingly compete through pricing flexibility, destination flexibility, and diversified contract structures rather than traditional, rigid, long-term agreements.

Strategic partnerships are becoming increasingly important across the liquefied natural gas industry. Energy companies are forming long-term procurement partnerships with utilities, industrial operators, and governments to secure predictable offtake demand. Joint ventures between infrastructure developers and institutional investors also continue expanding, particularly for import terminals and regasification projects.

Emerging players are focusing on small-scale LNG, floating infrastructure, and modular technologies to reduce capital intensity and improve deployment speed. These companies often target underserved regions where pipeline infrastructure remains underdeveloped. Technological advancements in liquefaction efficiency, storage optimization, and shipping logistics continue shaping competitive differentiation.

KEY INDUSTRY PLAYERS

Key Players are Focused on Acquiring Long-term Supply Contracts to Fuel Market Share

The market is dominated by a few large players but is expected to become increasingly competitive due to new entrants and expanding demand. Key players include major international oil and gas companies such as BP, Chevron, and ExxonMobil, along with national energy companies such as QatarEnergy LNG, Gas Authority of India Ltd (GAIL), and Petronet LNG Limited. In May 2025, QatarEnergy LNG announced plans to ink a long-term supply deal with Japan through its North Field expansion project. The key players compete through strategic investments, long-term contracts, and diversifying their offerings to capitalize on the growing demand for LNG. Asia Pacific, particularly China, India, and Japan, is a key market for LNG.

List of Key Liquefied Natural Gas Companies Profiled

- Chevron Corporation (U.S.)

- Royal Dutch Shell plc (U.K.)

- Exxon Mobil Corporation (U.S.)

- QatarEnergy LNG (Qatar)

- Cheniere Energy, Inc. (U.S.)

- PETRONAS (Malaysia)

- Woodside Petroleum Limited (Australia)

- TotalEnergies (France)

- BP plc (U.K.)

- Petronet LNG Ltd (India)

- Equinor ASA (Norway)

- Gazprom (Russia)

KEY INDUSTRY DEVELOPMENTS

- In June 2025, Penn America Energy Holdings (PAE) announced plans to build a large-scale LNG Export Terminal at Pennsylvania’s Delaware River. The facility is expected to export 7.2 million tons of liquefied natural gas annually.

- In June 2025, BP Singapore announced a sales agreement with Torrent Power to supply LNG gas up to 0.41 million metric tons per annum from 2027 through 2036, which is aimed at powering Torrent’s combined cycle gas-based plants with a capacity of 2,730 MW.

- In May 2025, GAIL revealed expansion plans for the Dabhol terminal, increasing its capacity to 12.5 mtpa by 2031-32.

- In May 2025, the Government of Qatar announced plans to increase its LNG production to increase trading of LNG cargoes to 30 to 40 million by 2030. The Country’s LNG production capacity is expected to increase to 160 million tons.

- In April 2025, Woodside Energy approved the development of a USD 17.5 billion LNG project in Louisiana. This development will allow Woodside to supply approximately 24 Mtpa of LNG by 2030.

Investment Analysis and Opportunities

The developing economies present a significant investment opportunity to the market:

- In March 2025, Venture Global announced expansion plans with an investment of USD 18 billion to upgrade the Louisiana LNG terminal to the largest LNG terminal in North America. Moreover, the company also proposed to expand the capacity of the Plaquemines plant in the U.S. to 45 MTPA by adding 24 trains to the facility.

- In December 2024, Cheniere Energy, Inc. LNG production from the first train from the Corpus Christi Stage 3 Liquefaction Project (“CCL Stage 3”) located in Texas, U.S. The plant is expected to be commissioned by the first quarter of 2025.

REPORT COVERAGE

The global Liquefied Natural Gas market report delivers a detailed insight into the market. It focuses on key aspects, such as leading companies. Besides, the report offers regional insights and global market trends & technology, and highlights key industry developments. In addition to the factors above, the report encompasses several factors and challenges that contributed to the growth and downfall of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 4.09% from 2025 to 2032 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type · Liquefaction · Regasification |

|

By Application · Power generation · Industrial · Transportation · Residential · Others |

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 167.06 billion in 2024.

The market is likely to grow at a CAGR of 4.09% over the forecast period (2025-2032).

The industrial segment is expected to lead the market over the forecast period.

The market size of North America stood at USD 54.44 billion in 2024.

Rising energy demand and clean energy transition drive foster market growth.

Some of the top players in the market are QatarEnergy LNG, Gas Authority of India Ltd (GAIL), BP PLC, and others.

The global market size is expected to reach USD 227.28 billion by 2032.

- 2019-2032

- 2024

- 2019-2023

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us