Electric Vehicle Range Extender Market Size, Share & Industry Analysis, By Technology Type (ICE-based, Rotary (Wankel) Engine, Fuel Cell-based, Micro Gas Turbine, and Alternative Generator-based), By Vehicle Type (Hatchback & Sedans, SUVs, LCVs, and HCVs), By Integration Type (OEM and Aftermarket), By Power Output Capacity (Below 25 kW, 25–50 kW, 50–100 kW, and Above 100 kW), By Fuel Type Used (Gasoline, Diesel, Hydrogen, and Alternative Fuels), and Regional Forecast, 2026-2034

Electric Vehicle Range Extender Market Size & Industry Overview

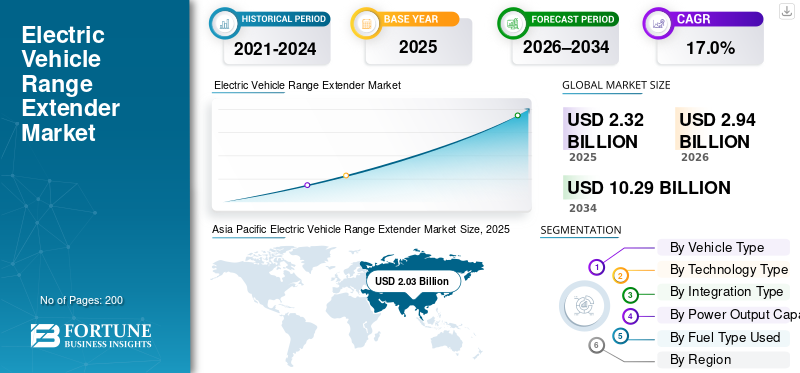

The global electric vehicle range extender market size was valued at USD 2.32 billion in 2025. The market is projected to grow from USD 2.94 billion in 2026 to USD 10.29 billion by 2034, exhibiting a CAGR of 17.0% during the forecast period. Asia Pacific dominated the Electric vehicle range extender market with a market share of 87.5% in 2025.

An electric vehicle range extender is a secondary power source, typically a small engine or fuel cell, that generates electricity to recharge the battery and extend driving range beyond battery-only limits. The global market is driven by rising electric vehicle adoption, range anxiety reduction, limited charging infrastructure, demand for longer driving range, regulatory emission targets, fleet electrification needs, and advancements in compact auxiliary power technologies.

Major players in the market include Cummins, MAHLE, AVL, Rheinmetall, and Ballard Power Systems, competing with their respective efficient range extender systems, fuel flexibility, compact design, emissions compliance, and integration with electric powertrains.

Download Free sample to learn more about this report.

Electric Vehicle Range Extender Market Key Takeaways

- 2025 Market Size: USD 2.32 billion

- 2026 Market Size: USD 2.94 billion

- 2034 Forecast Market Size: USD 10.29 billion

- CAGR: 17.0% from 2026–2034

- Asia Pacific dominated the electric vehicle range extender market with an 87.5% share in 2025.

- The fuel cell-based segment is the fastest-growing segment, registering a CAGR of 23.2%.

- The aftermarket segment is the fastest-growing channel, expanding at a CAGR of 22.5%.

Asia Pacific

Asia Pacific leads the market due to strong EV adoption, government incentives, and expanding demand for long-range electric mobility.

Europe

Europe is the second-largest regional market and is projected to grow at a CAGR of 13.1% during the forecast period.

North America

North America remains a key market, supported by growing demand for electric SUVs, pickup trucks, and commercial fleets.

U.S.

The electric vehicle range extender market is estimated at USD 0.09 billion in 2026.

Japan

The electric vehicle range extender market is estimated at USD 0.01 billion in 2026.

Read More

ELECTRIC VEHICLE RANGE EXTENDER MARKET TRENDS

Shift Toward Hydrogen and Alternative-Fuel Range Extenders is the Key Trend

One of the key market trends is a shift toward hydrogen and alternative-fuel range extenders. The global market is witnessing a shift from conventional gasoline-based range extenders toward hydrogen fuel cells and alternative fuels. This trend aligns with stricter emission norms and long-term decarbonization goals. Hydrogen-based range extenders offer zero tailpipe emissions, quieter operation, and higher efficiency. R&D investments focus on compact fuel cell stacks and modular architectures, enabling broader adoption across passenger cars, light commercial vehicles, and specialized mobility applications.

- In February 2025, U.K. cleantech company Viritech Ltd. began a study on using a hydrogen fuel cell range extenders (REX) for light electric vehicles, focusing on integrating portable sub-5 kW fuel cells with existing battery packs to extend BEV range and maintain payload, supported by a grant from the UK Department for Business and Trade, Advanced Propulsion Centre, and Niche Vehicle Network. The project targets last-mile delivery vans and L-Cat applications to develop a commercially viable zero-emission solution.

MARKET DYNAMICS

MARKET DRIVERS

Rising EV Adoption and Range Anxiety to Drive Market Growth

Growing adoption of electric mobility across passenger and commercial segments is driving demand for range extender systems. Consumers and fleet operators seek solutions that mitigate range anxiety, especially in regions with uneven charging infrastructure. Range extenders enable longer operational flexibility without fully relying on fast-charging networks, supporting EV penetration in remote, rural, and long-haul use cases. OEMs increasingly integrate range extenders to balance battery size, cost, and usability, accelerating market uptake. Thus, rising EV adoption and range anxiety is expected to drive the electric vehicle range extender market growth over the forecasted period.

- In 2024, according to IEA, global electric vehicle sales surpassed 17 million units, accounting for over 20% of total globally passenger vehicle sales.

MARKET RESTRAINTS

High System Cost and Integration Complexity to Restrain Product Adoption

Electric vehicle range extender adds cost, weight, and engineering complexity to electric vehicle platforms and supply chains. Integrating auxiliary engines or fuel cells requires additional thermal management, packaging space, and compliance with emissions regulations, increasing development timelines. For cost-sensitive vehicle segments, especially entry-level EVs, these factors limit adoption. OEMs may also prioritize larger batteries or charging solutions, reducing near-term demand for range extenders in highly developed charging markets.

MARKET CHALLENGES

Regulatory Uncertainty and Emission Classification to Pose a Key Challenge

Range extenders face regulatory challenges related to emission classification and incentive eligibility. In some regions, vehicles with onboard combustion-based range extenders may not qualify for full EV incentives or zero-emission mandates. Inconsistent global regulations create uncertainty for OEMs planning long-term product strategies. Aligning range extender technologies with evolving regulatory frameworks, especially in Europe and North America, remains a critical challenge for market participants.

MARKET OPPORTUNITIES

Fleet Electrification and Emerging Markets to Create New Growth Aspects in the Market

Commercial fleets, logistics operators, and public transport agencies present strong opportunities for electric vehicle range extender adoption. These users prioritize uptime, predictable operations, and flexible routing, where range extenders reduce charging downtime. Emerging markets with limited fast-charging infrastructure further amplify opportunity, as range extenders enable EV deployment without full grid readiness. Partnerships amongst OEMs, fleet operators, and technology providers are expected to unlock scalable, application-specific range extender solutions.

- In November 2023, Amazon UK planned to add 1,000 new electric delivery vans to its U.K. fleet, including Mercedes-Benz eSprinter and Renault Master ZE models. The expansion supports zero-emission urban deliveries, charging infrastructure deployment, and reduced carbon emissions.

Download Free sample to learn more about this report.

Electric Vehicle Range Extender Market Segmentation Analysis

By Vehicle Type

Growing Preference for Long-Range and Versatile Mobility to Drive SUV Segment’s Dominance

Based on vehicle type, the market is segmented into hatchbacks & sedans, SUVs, LCVs, and HCVs.

The SUVs segment dominates the market due to higher battery capacity requirements, longer driving expectations, and diverse usage patterns. Consumers increasingly prefer SUVs for intercity travel, premium comfort, and utility, amplifying range anxiety concerns. Range extenders help balance vehicle weight, cost, and usable range without oversized batteries. OEMs integrate range extenders in SUVs to enhance practicality, towing capability, and flexibility, particularly in regions with uneven charging infrastructure.

- In January 2025, Chinese EV maker Leapmotor selected ZF’s range extender system for its D19 SUV, integrating a compact gasoline-powered 30–40 kW range extender with the electric powertrain to improve driving range and charging flexibility in long-distance applications.

The LCVs segment is the fastest growing, expanding at a 20.0% CAGR. Rising electrification of logistics, delivery, and municipal fleets drives demand for range extenders that reduce downtime, extend daily operating range, and ensure consistent vehicle availability despite limited charging access.

By Technology Type

Proven Performance, Cost Efficiency, and OEM’s Dependency Sustains ICE-Based Technology Demand

Based on technology type, the market is segmented into ICE-based, rotary (Wankel) engine, fuel cell-based, micro gas turbine, and alternative generator-based.

ICE-based range extender technology dominates the market due to its technological maturity, cost-effectiveness, and established supplier ecosystem. OEMs favor internal combustion engine ICE-based systems for near-term deployment as they leverage existing engine platforms, fuel infrastructure, and regulatory familiarity. ICE range extender systems offer reliable power generation, easier integration, and faster commercialization across SUVs and LCVs, particularly in regions with limited hydrogen infrastructure or slower fuel cell readiness.

- In January 2026, Geely Galaxy began pre-sales of the Galaxy V900, an extended-range electric SUV featuring a 1.5-liter gasoline range extender, high-capacity battery pack, and intelligent energy management system, targeting long-range performance and reduced charging dependence for family-oriented users.

The fuel cell–based segment is the fastest growing, registering a 23.2% CAGR. Growth is driven by zero-emission operation, tightening emission norms, hydrogen ecosystem development, and increasing OEM investment in compact, high-efficiency fuel cell range extender solutions.

By Integration Type

Factory-Level Optimization, Warranty Coverage, and System Integration to Drive OEM’s Leadership

By integration type, the market is divided into OEM and aftermarket.

The OEM segment dominates the market as manufacturers increasingly integrate range extenders during the design and production stage. OEM integration enables optimized packaging, seamless powertrain control, regulatory compliance, and full warranty coverage. This approach ensures higher reliability, safety, and performance, particularly for SUVs and commercial EVs, making factory-fitted range extender solutions the preferred choice across major automotive markets.

- In May 2022, French automaker Renault revealed the Scénic Vision EV concept featuring a 160 kW electric motor from the Renault Mégane E-Tech, a 40 kWh battery, and a 16 kW hydrogen fuel cell range extender designed to enable long-distance driving with fast hydrogen refueling.

The aftermarket segment is the fastest-growing, expanding at a 22.5% CAGR. Growth is supported by retrofitting demand from fleets, extended vehicle lifecycles, cost-sensitive operators, and emerging markets seeking range enhancement without replacing existing electric vehicles EVs.

By Power Output Capacity

Compact Design, Cost Efficiency, and Urban Usability to Augment the Below 25 kW Segment Demand

By power output capacity, the market is categorized into below 25 kW, 25-50 kW , 50-100 kW, and above 100 kW.

The below 25 kW power output segment dominates the market due to its suitability for urban driving, compact SUVs, and light-duty applications. These systems are lightweight, cost-effective, and easier to integrate, providing sufficient supplemental power to reduce range anxiety without significantly increasing vehicle complexity, weight, or emissions, especially in passenger-focused electric vehicle platforms.

The 50–100 kW segment is the fastest growing, recording a 19.7% CAGR. Growth is driven by rising demand from larger SUVs and LCVs requiring higher continuous power, improved highway performance, and extended operational capability under heavy load conditions.

To know how our report can help streamline your business, Speak to Analyst

By Fuel Type Used

Established Fuel Infrastructure, Cost Advantage, and Technology Maturity to Sustain Gasoline Segment’s Leadership

By fuel type used, the market is segmented into gasoline, diesel, hydrogen, and alternative fuels.

Gasoline-based range extenders hold the largest market share due to widespread fuel availability, lower system costs, and mature engine technology. OEMs favor gasoline for near-term deployment as it enables quick scalability, simpler integration, and consistent performance across regions, especially where charging and alternative fuel infrastructure remain underdeveloped.

- In December 2025, Volkswagen Group confirmed it is evaluating Extended-Range Electric Vehicles (EREVs) using small gasoline-powered generators as range extenders. The approach targets larger SUVs and North American markets to address charging gaps, range anxiety, and customer demand for long-distance flexibility.

The hydrogen segment is the fastest growing, expanding at a 26.0% CAGR during the forecast period. The growth of the segment is driven by zero-emission operation, supportive government policies, expanding hydrogen refueling networks, and increasing adoption of fuel cell–based range extenders for long-range and commercial electric vehicles.

Electric Vehicle Range Extender Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Electric Vehicle Range Extender Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates and is the fastest-growing region in the market due to strong EV adoption, government incentives, and uneven charging stations infrastructure across large geographies. China leads with policy-backed EV production, while Japan and South Korea are advancing in fuel cell technologies. Growing SUV and LCV demand, expanding logistics fleets, and cost-sensitive consumers favor range extenders to balance affordability and usability. Emerging economies further accelerate adoption where grid readiness and fast-charging networks remain limited.

- In August 2024, GAC Group announced it would launch its Xingyuan range extender technology, featuring a high-efficiency gasoline engine with over 44% thermal efficiency, an integrated generator, and an intelligent energy management system to support extended-range electric SUVs and sedans.

China Electric Vehicle Range Extender Market

The China market in 2026 is estimated at around USD 2.33 billion, accounting for roughly 79.4% of global market revenues. China dominates the Asia Pacific region as well as the global market. The demand is driven by vast EV penetration, EREV popularity, range-anxiety mitigation, supportive policies, and rapid electrified powertrain innovation.

Japan Electric Vehicle Range Extender Market

The Japan market in 2026 is estimated at around USD 0.01 billion, accounting for roughly 0.3% of global market revenues. Growth remains moderate in Japan, supported by hybrid expertise, efficiency-focused engineering, and selective OEM experimentation.

India Electric Vehicle Range Extender Market

The India market in 2026 is estimated at around USD 0.02 billion, accounting for roughly 0.7% of global market revenues. Fast growth in India is fueled by infrastructure gaps, commercial EV demand, cost sensitivity, and interest in alternative electrification pathways.

Europe

Europe represents the second position in the global electric vehicle range extender market share, growing at a 13.1% CAGR. The regional market is driven by strict emission regulations and a strong OEM focus on electrification. Range extenders support compliance while addressing long-distance and cross-border travel needs. Adoption is higher in premium SUVs and commercial EVs, particularly in Germany, France, and the U.K. Increasing interest in hydrogen-based solutions and R&D investments further strengthens Europe’s strategic position in advanced range extender technologies.

- In November 2025, XPeng reported rising extended-range EV (EREV) sales in Europe, positioning its battery-electric platforms with gasoline range extenders as a compliance solution amid stricter emission rules, enabling longer driving range while navigating impending combustion-engine bans.

Germany Electric Vehicle Range Extender Market

The Germany market in 2026 is estimated at around USD 0.03 billion, accounting for roughly 1.0% of global market revenues. Germany market supported by premium OEM R&D, emissions compliance, and transitional electrification strategies.

U.K. Electric Vehicle Range Extender Market

The U.K. market in 2026 is estimated at around USD 0.02 billion, accounting for roughly 0.8% of global market revenues. U.K.’s market expansion is driven by niche EREV applications, regulatory pressure, and urban range-reliability requirements.

North America

North America is the third-largest market supported by high demand for SUVs and pickup-based electric platforms with long-range expectations. Range extenders address range anxiety over long driving distances and limited rural charging access. Commercial fleets, recreational vehicles, and utility applications increasingly adopt range extenders to improve operational flexibility.

- In September 2025, Ford Motor Company debuted the F-150 Lightning EREV, integrating a gasoline-powered onboard range extender generator to supplement the battery system, targeting extended driving range, improved towing capability, and reduced charging downtime for recreational and commercial truck users.

U.S. Electric Vehicle Range Extender Market

The U.S. market in 2026 is estimated at around USD 0.09 billion, accounting for roughly 2.9% of global market revenues. The U.S. dominates the North American market due to strong SUV and light commercial vehicle penetration, long-distance driving patterns, and fleet electrification initiatives. Range extenders are favored to reduce downtime, support rural operations, and improve EV practicality beyond urban charging networks in the U.S.

Rest of the World

The Rest of the World market grows steadily, driven by EV adoption in South America, the Middle East, and parts of Africa. Limited fast-charging infrastructure, long travel distances, and grid constraints increase reliance on range extenders. Adoption is strongest in commercial fleets, government projects, and premium imports. Gradual policy support and improving EV awareness create long-term potential rather than immediate large-scale deployment.

- In April 2025, Exeed by Al Ghurair launched an electric and hybrid vehicle fleet in the UAE, featuring extended-range and plug-in hybrid vehicle model with advanced battery systems and range extender technology, supporting corporate mobility, sustainability goals, and reduced fleet emissions across commercial operations.

COMPETITIVE LANDSCAPE

Key Industry Players

Technology Diversification, Fuel Innovation, and OEM Partnerships is Defining Competitive Intensity

The electric vehicle range extender market is moderately fragmented, with established automotive suppliers and emerging fuel cell specialists competing across ICE-based and fuel cell–based technologies. Key market players such as Cummins, MAHLE, AVL, Rheinmetall, and Ballard Power Systems compete through efficiency improvements, fuel flexibility, and compact system integration. Companies focus on OEM collaborations, modular platforms, and regional customization. Investments in hydrogen technology, emissions compliance, and scalable architectures help address diverse vehicle segments and evolving regulatory requirements.

LIST OF KEY ELECTRIC VEHICLE RANGE EXTENDER COMPANIES PROFILED

- Horse Powertrain (U.K.)

- AVL List GmbH (Austria)

- MAHLE GmbH (Germany)

- Robert Bosch GmbH (Germany)

- Cummins Inc. (U.S.)

- Weichai Power Co., Ltd. (China)

- Dana Incorporated (U.S.)

- Toyota Industries Corporation (Japan)

- Mazda Motor Corporation (Japan)

- ZF Friedrichshafen AG (Germany)

- Ballard Power Systems (Canada)

- Hyundai Mobis (South Korea)

- Hyzon Motors (U.S.)

- Ricardo plc (U.K.)

- SAIC Motor Corporation (China)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Li Auto expanded the L9 into Russia, highlighting its electric vehicle range extender (EREV) system combining a high-capacity battery with a turbocharged gasoline generator, enabling extended driving range, reduced range anxiety, and efficient long-distance electric mobility.

- January 2026: Renault revealed its Super Range Extender concept, combining a compact gasoline engine, high-efficiency generator, and optimized energy management software to significantly extend EV driving range while reducing battery size, cost, and lifecycle emissions.

- December 2025: Schaeffler showcased a compact EV range extender integrating an electric motor, power electronics, and generator unit into a single module, enabling space-efficient installation, higher system efficiency, and simplified OEM integration for electric vehicles.

- September 2025: Seres Power debuted its Super Range Extender System at IAA Mobility 2025, featuring a high-efficiency ICE generator, modular architecture, and an intelligent control unit, designed to support global EREV development across SUVs and light commercial vehicles.

- September 2025: HORSE Powertrain, backed by Renault Group and Geely, unveiled a next-generation range extender system featuring a high-efficiency combustion engine and generator, targeting cost-effective extended-range EV solutions for global mass-market applications.

- August 2025: IM Motors launched its Hengxing Super Range Extender, integrating a high-efficiency gasoline engine, onboard generator, and intelligent energy management system to significantly extend driving range, improve fuel efficiency, and support extended-range electric sedan and SUV applications.

- May 2025: ZF Group announced entry into the electric range extender system market, unveiling next-generation eRE and eRE+ systems with 70–150 kW output, 400V/800V compatibility, integrated motors, inverters, and planetary gears, targeting mass production from 2026 to address EV range anxiety cost-effectively.

- August 2024: South Korea’s Hyundai-linked suppliers advanced development of extended-range EV powertrains, combining compact gasoline generators and high-capacity batteries, aimed at improving driving range while complying with tightening global emission and efficiency regulations.

- July 2024: Geely Holding Group confirmed progress on its next-generation extended-range EV platform, integrating a small-displacement gasoline range extender engine with advanced thermal efficiency to support scalable EREV deployment across multiple passenger vehicle segments.

- May 2024: HORSE Powertrain presented its next-generation range extender technology, focusing on improved thermal efficiency, reduced NVH, and modular scalability, supporting automakers transitioning from conventional ICE platforms to extended-range electric vehicle architectures.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 17.0% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, By Technology Type, By Integration Type, By Power Output Capacity, By Fuel Type Used, and By Region |

|

By Vehicle Type |

· Hatchbacks & Sedans · SUVs · LCVs · HCVs |

|

By Technology Type |

· ICE-based · Rotary (Wankel) Engine · Fuel Cell-based · Micro Gas Turbine · Alternative Generator-based |

|

By Integration Type |

· OEM · Aftermarket |

|

By Power Output Capacity |

· Below 25 kW · 25–50 kW · 50–100 kW · Above 100 kW |

|

By Fuel Type Used |

· Gasoline · Diesel · Hydrogen · Alternative Fuels |

|

By Region |

· North America (By Vehicle Type, By Technology Type, By Integration Type, By Power Output Capacity, By Fuel Type Used, and By Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Vehicle Type, By Technology Type, By Integration Type, By Power Output Capacity, By Fuel Type Used, and By Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Vehicle Type, By Technology Type, By Integration Type, By Power Output Capacity, By Fuel Type Used, and By Country) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o South Korea (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World (By Vehicle Type, By Technology Type, By Integration Type, By Power Output Capacity, By Fuel Type Used) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.32 billion in 2025 and is projected to reach USD 10.29 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 2.03 billion.

The market is expected to exhibit a CAGR of 17.0% during the forecast period.

The SUVs segment leads the market in terms of vehicle type.

Rising EV adoption and range anxiety to drive market growth.

Key players in the market include Cummins, MAHLE, AVL, Rheinmetall, and Ballard Power Systems, among others.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us