Hydrogen Market Size, Share & Industry Analysis by Type (Blue, Green, and Grey), By Production Process (Reforming (Without Carbon Capture), Industrial By-Product, and Others), By End-Use Industry (Steel, Refineries, Ammonia, Methanol, and Others), and Regional Forecast, 2026-2034

Hydrogen Market Size and Future Outlook

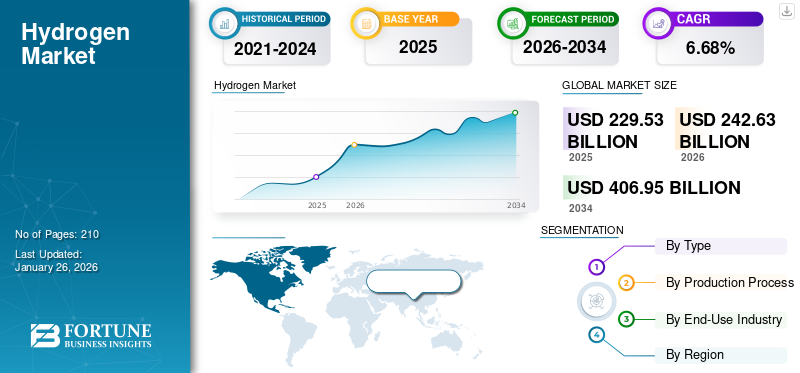

The global hydrogen market size was valued at USD 229.53 billion in 2025. The market is projected to grow from USD 242.63 billion in 2026 to USD 406.95 billion by 2034, exhibiting a CAGR of 6.68% during the forecast period. Asia Pacific dominated the hydrogen market with a market share of 31.45%% in 2025.

The main target of reducing carbon emissions is a major factor that leads the hydrogen industry to success. Hydrogen is increasingly recognized as a flexible component of the energy system, supporting power generation, storage, and decarbonization across various sectors. Industries such as steel, cement, refining, and chemicals are facing many problems in the route to achieving full adaptation to the decarbonization goals. Therefore, hydrogen, as a low-carbon substitute for fossil fuels, is filling this gap by supporting these nations in gathering their net-zero pledges and also assisting the change to renewable energy. The market is emerging as a key pillar of the energy sector, driving decarbonization and enabling cleaner fuels, power generation, and industrial applications.

Key players in the market include Air Liquide, Linde, Air Products, Shell, BP, Siemens Energy, Plug Power, and Cummins, which lead in hydrogen production, storage, and fuel cell technologies. These companies drive advancements in green hydrogen, infrastructure development, and large-scale decarbonization projects globally.

- In February 2025, Siemens, Guofu Hydrogen, a prominent China-based supplier of comprehensive solutions for hydrogen energy, and RCT GH Hydrogen, a German-based supplier of hydrogen systems and services, agreed to collaborate on the development of the hydrogen value chain by signing a Memorandum of Understanding (MoU). Their partnership is a pivotal move toward the international growth of green hydrogen technology since it aims at the process and the subsequent production of green hydrogen using electrolyzers.

Download Free sample to learn more about this report.

Hydrogen Market KEY TAKEAWAYS

- 2025 Market Size: USD 229.53 billion

- 2026 Market Size: USD 242.63 billion

- 2034 Forecast Market Size: USD 406.95 billion

- CAGR: 6.68% from 2026–2034

- Asia Pacific dominated the hydrogen market with a 31.45% share in 2025.

- The grey hydrogen segment accounted for the largest market share of 95.25% in 2026.

- The reforming (without carbon capture) segment held an 81.00% share in 2026.

Asia Pacific

Asia Pacific generated USD 110.46 billion in 2025 and is projected to reach USD 117.28 billion in 2026, supported by strong industrial demand and clean energy initiatives.

Europe

Europe reached USD 46.1 billion in 2025 and is expected to grow to USD 49.17 billion in 2026, driven by decarbonization policies and hydrogen adoption across industries.

North America

North America generated USD 40.96 billion in 2025 and is projected to reach USD 42.96 billion in 2026, supported by investments in hydrogen production and infrastructure.

U.S.

U.S. The hydrogen market is estimated to reach USD 36.10 billion in 2026, driven by growing investments in clean hydrogen projects and supportive government initiatives.

Japan

Japan Rising adoption of hydrogen fuel cell technologies, ambitious carbon neutrality targets, and continued investments in hydrogen infrastructure are supporting market growth.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Renewable Integration and Energy Storage to Propel the Market Growth

The market growth is being driven by renewable integration and energy storage as green hydrogen allows the storage of excess solar and wind energy that can be utilized in the form of electricity or as fuel for industries and transportation. This ensures grid stability, raising the resilience of energy and aiding the shift to a carbon emission-free economy. The hydrogen market is evolving rapidly, guided by regulatory frameworks that set safety, certification, and policy standards to accelerate adoption across the energy sector.

- In April 2025, the Asian Development Bank (ADB) gave green light to an investment of USD 104 million toward helping Georgia improve the energy supply. As per the Energy Storage and Green Hydrogen Development Project by ADB, the bank will accompany Georgia to establish the first energy storage system in the country and also investigate the potential of green hydrogen in the country.

MARKET RESTRAINTS:

High Production Costs to Restrict Market Expansion

The high cost of producing hydrogen remains a primary barrier to its widespread adoption. Producing green hydrogen via electrolysis requires such a major input of electricity from renewable sources that the price of green hydrogen is currently higher than hydrogen from fossil fuels as well as in comparison to conventional energy options. Additionally, electrolyzers, fuel cells, and the ancillary infrastructure for hydrogen storage, transport, and refueling costs add to the total cost of hydrogen, making it uncompetitive in the marketplace.

Furthermore, hydrogen production, compression, and liquefaction are such energy-intensive that the overall cost of supply is still high compared to the relatively low cost of natural gas, coal, or even in relation to specific renewable energy solutions. Due to these high current costs, hydrogen faces market limitations as many industries and utilities are reluctant to convert their offerings until either the technology can be adopted at scale or the costs of hydrogen become more favorable.

MARKET OPPORTUNITIES:

Shift toward Hydrogen-Based Steelmaking to Cut CO2 Emissions to Create Growth Opportunities

The manufacturing of steel generates significant carbon dioxide emissions, making it one of the largest industrial sectors for those emissions. Traditional steel making is almost entirely reliant on coal via the BF-BOF route to access the coking coal needed through a blast furnace to create molten steel. There is notable global pressure to decarbonize industrial sectors to reach net-zero targets, albeit for those sectors that are harder to decarbonize. Hydrogen enhances energy security by diversifying energy sources, reducing reliance on imported fossil fuels and enabling long-term clean energy storage.

Major steel producers in Europe, Asia (Japan, South Korea, and China), and the Middle East have planned investments in pilot plants and commercial-scale hydrogen DRI facilities and funding is growing from governments. In addition to the plans and investments that large steel producers have made to identify commercial hydrogen DRI plants and pilot studies, the use of hydrogen will increase, thereby increasing DRI utilization, particularly when green transition policies are present. The use of hydrogen or DRI in steel making is likely to increase the demand for hydrogen, making the steel industry a major contributor to hydrogen market growth in the forthcoming years.

- In August 2024, Linde Engineering signed an agreement with Shell Deutschland GmbH (“Shell”) that entails the construction of a 100 MW renewable hydrogen unit for the REFHYNE II project. The project is located in Wesseling, Germany at the Shell Energy and Chemicals Park Rheinland. REFHYNE II is expected to produce up to 44,000 kilograms per day of renewable hydrogen to decarbonize site operations. It will be used to produce cleaner energy products, such as transport fuels, with a lower carbon intensity.

HYDROGEN MARKET TRENDS:

Rising Adoption in Shipping and Heavy-Duty Vehicles to Drive Market Growth

The transportation sector, especially shipping and heavy-duty vehicles, is headed toward becoming the leading growth opportunity for market players. Unlike passenger cars, which can be electrified with batteries in a nearly universal way, these sectors face complications with battery electrification due to weight, range, and refueling infrastructure challenges. Hydrogen (whether hydrogen fuel cells, or hydrogen-derived fuels such as green ammonia and methanol) is a viable option since hydrogen allows longer ranges, quicker refueling, and lower emissions. Furthermore, the hydrogen market is expanding with integrated supply chains spanning production, storage, transport, and end-use applications to support global energy transition goals. In addition, the current hydrogen trends are driven by large-scale hydrogen projects focused on green production, infrastructure development, and integration into global energy markets.

- In May 2024, Volvo Trucks is working on a truck powered by combustion engines fueled by hydrogen. The road testing of trucks with hydrogen-powered combustion engines will take place starting in 2026, with commercial availability slated for the latter part of this decade. The delivery of trucks using green hydrogen represents a big move for Volvo in reaching its net-zero objective and allowing customers to also reach their decarbonization goals.

MARKET CHALLENGES:

High Production Costs to Hamper Market Growth

One of the major challenges for the hydrogen market is the high cost of production, especially for green hydrogen produced from electrolysis. Grey hydrogen offers the benefits of being produced using natural gas at a lower cost, while green hydrogen takes a lot of renewable electricity, expensive electrolyzer systems, and elaborate storage. All of these factors together make green hydrogen expensive to produce, less competitive with traditional fuels, and other low-carbon fuels.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Low Production Cost of Grey Hydrogen to Drive Segment Growth

On the basis of segmentation by type, the market is classified into blue, green, and grey.

In 2026, the grey segment dominates the market with a 95.25% share. Grey hydrogen is the cheapest and widely used type and is derived from natural gas through the process of steam methane reforming (SMR) without carbon capture. The relative abundance of natural gas, the relatively established technology, and the more established infrastructure associated with grey hydrogen make it much cheaper to produce than green hydrogen and blue hydrogen, which take more investment and newer technology to produce.

The green hydrogen segment is experiencing the fastest growth and is expected to grow at a CAGR of 15.33% over the analysis period. Governments, industries, and investors look to decarbonize with the help of declining renewable energy prices, robust policy support, and large project investment, propelling segment growth. In January 2025, India launched its first green hydrogen hub, to which around USD 21.6 billion is expected to be invested to set up 20 GW of renewable energy projects that will produce 1500 tons of green hydrogen and 7500 tons of green hydrogen derivatives such as green urea, green methanol, and sustainable aviation fuel per day.

By Production Process

Low Production Cost to Drive the Reforming (Without Carbon Capture) Segment Growth

In terms of production process, the market is categorized into reforming (without carbon capture), industrial by-product, and others (water electrolysis and reforming with carbon capture).

The reforming (without carbon capture) segment dominates the global hydrogen market share. By production process, the reforming (without carbon capture) segment held a market share of 81.00% in 2026. Reforming using conventional means, without capture, dominates the market as it has the lowest cost of production, uses existing steam methane reforming (SMR) technology that has been commercially proven, and utilizes existing natural gas infrastructure. Despite the high CO2 emissions associated with this process, it is the most cost-effective and popular process.

- In July 2022, Shanghai Chemical Industry Park Industrial Gases Co., Ltd, a subsidiary of Air Liquide, announced plans to invest over USD 200 million to construct two hydrogen production facilities and supporting infrastructure in Shanghai Chemical Industry Park. The two new hydrogen production units will yield substantial environmental benefits, as they will replace the existing supply from a third-party coal-based gasification facility, will have CO2 capture and recycle technology, and will be integrated with SCIPIG's local existing network.

The others segment is the fastest-growing segment with a growth rate of 9.27% over the forecast period. This has been recorded as other processes help meet local and global decarbonization objectives by providing low-carbon solutions eligible for government support. The segment is also is growing rapidly and expanding into industrial and energy applications seeking cleaner hydrogen, as the sector evolves.

By End-Use Industry

Refineries Dominate the Market as they Utilize Large Volumes of Hydrogen for Hydrocracking

In terms of end-use industry, the market is categorized into steel, refineries, ammonia, methanol, and others.

The refineries segment is the dominant segment in the market. This segment is set to hold a 40.53% share in 2025. Refineries are the largest users of hydrogen in processes such as hydrocracking and desulfurization, are known for their heavy reliance on well-established grey hydrogen production, and already have extensive infrastructure in place, making them the world's primary end user of hydrogen. In June 2025, India announced its preparation for green hydrogen ventures valued at about Indian rupees INR 2 trillion (USD 23 billion). These will include tenders for 42,000 tonne/year of green hydrogen production by domestic oil refineries.

The methanol segment is projected to grow at a CAGR of 7.90% over the study period as hydrogen is an important feedstock in methanol production. The increased demand for methanol as a chemical intermediate and clean fuel is generating further hydrogen usage in this segment.

To know how our report can help streamline your business, Speak to Analyst

Hydrogen Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Hydrogen Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific generated USD 110.46 billion, contributing 31.45% to global market revenue, and is projected to grow to USD 117.28 billion in 2026. The hydrogen market in the Asia Pacific region is rising due to strong industrial demand, abundant renewable resources, government policies supporting hydrogen adoption, and large-scale planned projects in steel, refining, and clean mobility.

In 2026, the China market is estimated to have reached USD 51.43 billion. The market in China is expanding due to healthy government backing for decarbonization, rapid growth in green hydrogen and electrolyzer production, growing demand from industrial customers such as steel, chemicals, and cement, and rising deployment of hydrogen fuel cell vehicles, which is increasing the number of hydrogen refueling stations.

- For instance, in September 2025, the Energy and Mineral Resources Ministry of Jordan announced that it had signed a memorandum of understanding with UEG Green Hydrogen Development Holding Limited from China to carry out a feasibility study for a green hydrogen project worth USD 1.15 billion (EUR 981 million) in the country.

Europe

Europe maintained a strong presence in the global market, reaching USD 46.1 billion in 2025, accounting for 40.53% share, and is expected to reach USD 49.17 billion in 2026. Other regions, such as North America and Europe, are anticipated to witness notable growth in the coming years. During the forecast period, the Europe region is projected to record a growth rate of 7.30%, which is the second highest amongst all the regions, and reach the valuation of USD 46.10 billion in 2025. The growth of the Europe market is strong, driven by ambitious decarbonization targets, large government investments, and coordinated internal industrial efforts, making hydrogen a key component of Europe's energy transition. Backed by these factors, Germany is expected to have recorded a valuation of USD 11.45 billion, and the rest of Europe, USD 7.15 billion, in 2025.

North America

The North America region captured 8.26% of the global market in 2025, generating USD 40.96 billion in revenue, and is projected to reach USD 42.96 billion in 2026. After Europe, the market in North America is estimated to reach USD 40.96 billion in 2025 and secure the position of the third-largest region in the market. In the region, the U.S. is estimated to have reached USD 36.10 billion in 2026. The hydrogen market in North America is expanding quickly due to supportive government policy, rising industrial demand for cleaner energy solutions, and major investments in hydrogen infrastructure and technology development.

Latin America

The Latin America market generated USD 24.65 billion in 2025, representing 15.06% of the global market landscape, and is expected to reach USD 25.65 billion in 2026.Considering Latin America, the countries in the region have tremendous opportunities for renewable energy generation, including solar, wind, and hydropower. According to the International Energy Agency (IEA), about 60% of their electricity comes from renewables, making it a great environment for producing green hydrogen. The Latin America market, in 2025, is set to have recorded a value of USD 7.35 billion.

Middle East & Africa

Middle East & Africa recorded a market size of USD 7.35 billion in 2025, capturing 4.70% of the global market share, and is projected to reach USD 7.57 billion in 2026. The Middle East & Africa region has among the highest solar radiation levels in the world, making it an ideal location for producing green hydrogen via electrolysis. Saudi Arabia, Egypt, and South Africa are capitalizing on their renewable energy potentials to produce green hydrogen to satisfy domestic and export energy consumption needs. In the Middle East & Africa, the GCC is set to have touched a value of USD 13.47 billion in 2025.

COMPETITIVE LANDSCAPE

Key Players are Heavily Investing in Hydrogen Infrastructure to maintain their Leading Position

Linde plc and Air Liquide are acknowledged as major participants in the market as each firm is very experienced, innovative, and has invested heavily in hydrogen infrastructure. For instance, in March 2025, Air Products Qudra (APQ) and Aramco, a leading integrated energy and chemicals company, announced that Aramco had completed the takeover of a 50% equity interest in the Blue Hydrogen Industrial Gases Company (BHIG) in Jubail, Saudi Arabia. This agreement combines expertise and capabilities to supply hydrogen, inclusive of lower-carbon hydrogen, to the Jubail Industrial City area at scale.

LIST OF KEY HYDROGEN COMPANIES PROFILED:

- Linde plc (U.K.)

- Air Liquide (France)

- Air Products & Chemicals, Inc. (U.S.)

- Shell plc (U.K.)

- Aramco (Saudi Arabia)

- Toyota Motor Corp. (Japan)

- ITM Power (U.K.)

- Nel ASA (Norway)

- Technip Energies (France)

- Cummins Inc. (U.S.)

- Messer Group (Germany)

- Ballard Power Systems Inc. (Canada)

- Plug Power (U.S.)

- BP Plc (U.K.)

- ExxonMobil (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- In May 2025, Technology Company Technip Energies and Graphitic Energy, a U.S. clean energy technology company, previously known as C-Zero, announced their strategic collaboration to accelerate the adoption of clean hydrogen technologies.

- In March 2025, Nel ASA entered into an EPC collaboration agreement enabling SAMSUNG E&A to deliver complete hydrogen plants of its own design to its customers, utilizing Nel's electrolyzers. Additionally, as part of a separate transaction, SAMSUNG E&A will acquire 10% of newly issued Nel ASA shares via a direct placement, resulting in 9.1% ownership post-transaction, making it the largest single shareholder in Nel.

- In July 2024, Virya Energy and its partners HyoffGreen and Messer finalized the investment decision for the Hyoffwind project located in Zeebrugge, Belgium. This was the final piece of validation before starting construction of the first 25MW renewable hydrogen production facility in Belgium, which will produce its first molecules in 2026. It will deliver 25,000 tons of CO2 reduction per year across the mobility and industrial segments.

- In July 2024, ITM Power executed a supply agreement and binding heads of terms on a long-term services agreement for the Milford Haven-based (U.K.) 20 MW West Wales hydrogen project. The project has all necessary permits and is just about to finalize commercial terms with project stakeholders, with a final investment decision anticipated prior to the end of 2025.

- In February 2023, Air Liquide announced a joint venture with Siemens Energy to mass-produce electrolyzers, supporting projects such as the 200 MW Normand’Hy facility in France.

REPORT COVERAGE

The global market analysis provides an in-depth study of the market size and forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year |

2026 |

| Forecast Period | 2021-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.68% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Type

By Production Process

By End-Use Industry

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 229.53 billion in 2025 and is projected to reach USD 406.95 billion by 2034.

In 2025, the market value stood at USD 229.53 billion.

The market is expected to exhibit a CAGR of 6.68% during the forecast period of 2025-2032.

The refineries segment leads the market by end-use industry.

Renewable integration and energy storage are key factors slated to propel the market growth.

Linde plc, Air Liquide, Shell plc, and others are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

The shift toward hydrogen-based steelmaking to cut CO2 emissions is anticipated to create growth opportunities.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us