Water and Sewer Line Construction Market Size, Share & Industry Analysis, By Application (Potable Water, Wastewater/Sewer, and Stormwater/Drainage), By Service (New Construction, Rehabilitation & Replacement, and Others (Maintenance, Repair & Upgrades), and Regional Forecast, 2026-2034

WATER AND SEWER LINE CONSTRUCTION MARKET SIZE AND FUTURE OUTLOOK

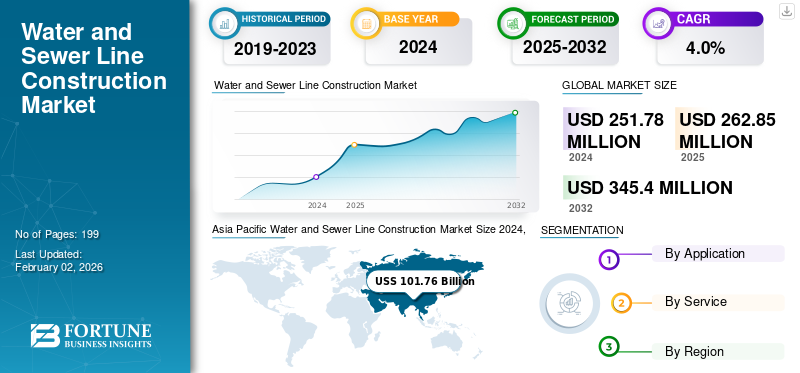

The global water and sewer line construction market size was valued at USD 262.85 billion in 2025. The market is projected to grow from USD 273.99 billion in 2026 to USD 370.55 billion by 2034, exhibiting a CAGR of 3.80% during the forecast period. Asia Pacific dominated the water and sewer line construction market with a market share of 40.80% in 2025.

Water and sewer line construction includes the preparation of the trench, the laying and joining of pipes, and backfilling and testing the lines. Some of the essential measures are to make sure that the pipes are correctly sloped and bedded, to use sight rails to align the pipes, to construct manholes at junctions or changes in direction, and to ensure that the lines are watertight and operational before the project is completed.

The significant drivers of the market expansion include population growth and urbanization, which are increasing the demand for new and expanded infrastructure. Another factor that is important in growth is aging existing infrastructure requiring replacement, government funding and regulations, and development of smart cities with improved water management systems.

The leading companies in the industry are China State Construction Engineering Corporation Ltd., Vinci SA, Bechtel Corporation, Hochtief AG, and Webuild S.p.A.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Aging Infrastructure, Urbanization, and Government Infrastructure Fuels the Market Growth

The water and sewer line construction market growth is experiencing stability due to old infrastructure and the high rate of urbanization in emerging economies. Most of these old water supply and wastewater systems require many upgrades to stay up to date in terms of efficiency and safety. At the same time, the growth in the cities and number of government projects based on sanitation such as the Jal Jeevan Mission in India, the Infrastructure Investment and Jobs Act in the U.S., and the Green Deal in Europe, are ensuring that capital is constantly invested. Moreover, there is growing regulatory focus on local minimization, pollution management, and climate resilience to support new project pipelines as well as long-term infrastructure sustainability objectives.

Market Restraints

Cost Escalation, Labor Shortages, and Project Delays Hinder Growth

The industry is constrained by persistent operational and financial challenges despite stable market growth. Increasing raw material costs, limited availability of skilled labor, and disruptions in global supply chains have increased construction costs and slowed down the project execution timelines. Workforce constraints are prominent in specialized areas such as trenchless installation techniques. Furthermore, the presence of complex approval frameworks and extended procurement processes often delay project rollouts. Public infrastructure initiatives are also affected by highly competitive, price-driven bidding mechanisms that narrow profit margins. The strong footprint of small and regionally fragmented contracting firms limits scalability and adoption of digital construction technologies.

Market Opportunities

Digital Asset Management, Rehabilitation Boom & PPP Models Drive Growth, Creating Opportunities

The market is transforming by advancements in digitalization, modernization, and financing frameworks that are reshaping business opportunities. The integration of digital twin technologies is resulting in improved asset monitoring, predictive maintenance, and operational capabilities across infrastructure networks. Rehabilitation and pipeline replacement activities are projected to rise in developed regions which can be attributed to the adoption of trenchless and other minimally disruptive implementation techniques. The growth in PPP models continues to attract private investment for large scale water infrastructure development. In parallel, the increasing emphasis toward sustainability has resulted in surged use of water recycling systems, intelligent leak detection, and resource-efficient materials, thus opening up growth prospects across North America, Europe, and the Asia Pacific regions.

WATER AND SEWER LINE CONSTRUCTION MARKET TRENDS

Transition to Smart Infrastructure, Trenchless Technologies & Sustainable Materials Emerges as a Major Market Trend

The water and sewer line construction industry is transforming to smarter and more sustainable infrastructure solutions. Trenchless technologies such as horizontal directional drilling (HDD), cured-in-place pipe (CIPP), and micro tunneling are fast becoming popular among utilities and engineering companies to reduce the amount of surface disturbance and carbon emissions. The latest types of smart network systems include IoT sensors, GIS mapping, and real-time leak detection to enhance operational control. Simultaneously, the sustainability mission is pushing change to less impactful materials such as HDPE, GRP, and recycled PVC. These developments are collectively transforming the project design, performance monitoring, and asset management in the watershed of the global water infrastructure.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Application

Ongoing Investment in Expanding Water Access Boosts Potable Water Segment Growth

Based on the application, the market is segmented into potable water, wastewater/sewer, and stormwater/drainage.

The potable water segment held the largest water and sewer line construction market share of USD 122.05 million in the overall global market in the year 2026. The segment covers the broadest infrastructure footprint, encompassing municipal water supply networks, distribution mains, and service connections in both urban and rural areas. The ongoing investment in expanding water access, reducing non-revenue water, and replacing aging mains ensures steady, recurring project flow. Regulatory prioritization of potable water delivery and quality monitoring sustains consistent funding across regions, giving it the largest share of overall construction value.

Of all the segments, wastewater/sewer holds the highest CAGR of 4.7% in the global market. The growth is due to heightened environmental regulations, rapid urbanization, and increasing sanitation coverage mandates in emerging markets. Upgrades of outdated sewer networks, new wastewater treatment tie-ins, and adoption of trenchless rehabilitation methods such as CIPP, and microtunneling are accelerating investments. Public-private partnerships and compliance-driven spending create long-term growth momentum that outpaces the relatively mature potable water segment.

To know how our report can help streamline your business, Speak to Analyst

By Service

New Construction Segment Dominates Market Owing to Its Urban Infrastructure Expansions

Based on service, the market is divided into new construction, rehabilitation & replacement, and others (maintenance, repair & upgrades).

The new construction segment dominates with a market share of USD 145.31 million in 2026. The segment continues to generate the major revenue due to its extensive greenfield network buildouts in Asia, the Middle East, and Africa, as well as urban infrastructure expansions and industrial corridor developments. Large-scale distribution and transmission line projects under government programs underpin a steady pipeline of high-value contracts, securing the largest revenue share within the sector.

Rehabilitation & replacement holds the highest CAGR of 5.2% in the global market. The segment is rising sharply as aging infrastructure in developed regions demands systematic renewal. Increasing emphasis on asset condition monitoring, leak detection, and trenchless rehabilitation is driving faster, higher-margin growth. Stricter performance regulations and sustainability objectives accelerate replacement cycles, lifting CAGR above new construction rates globally.

WATER AND SEWER LINE CONSTRUCTION MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

In 2025, North America generated USD 66.81 Billion, contributing 25.40% to global market revenue, and is projected to grow to USD 69.22 Billion in 2026. The region’s growth is driven by aging water and sewer infrastructure requiring replacement, increasing urbanization, government investments in utility modernization, and stricter environmental regulations. Continuous investments in resilient water management systems and wastewater treatment projects are further supporting market expansion. The U.S. market is projected to reach USD 54.43 Billion in 2026, supported by large-scale infrastructure funding programs and rising demand for network rehabilitation projects.

Europe

The Europe market accounted for USD 53.82 Billion in 2025, representing 20.50% of the global industry, and is expected to reach USD 55.54 Billion in 2026. Growth in the region is supported by strong construction activities, smart city initiatives, and increasing investments in sustainable water infrastructure. Efforts to improve water management efficiency and address climate-related challenges, including water scarcity and pollution, continue to create opportunities for market growth. The U.K. and Germany markets are projected to reach USD 9.11 Billion and USD 9.81 Billion in 2026, respectively.

Asia Pacific

Asia Pacific Water and Sewer Line Construction Market Size 2025,(USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific recorded a market size of USD 107.26 Billion in 2025, capturing 40.80% of the global market share, and is projected to reach USD 112.83 Billion in 2026. The region dominates the global market due to its large population base, rapid urbanization, expanding water and sewer networks, and sustained government infrastructure development programs. Growing investments in municipal water systems, industrial water infrastructure, and rural sanitation projects continue to support strong market demand. The China market is projected to reach USD 51.84 Billion in 2026, while India and Japan are expected to reach USD 23.23 Billion and USD 13.75 Billion, respectively.

Middle East & Africa

The Middle East & Africa market generated USD 20.78 Billion in 2025, representing 7.90% of the global market landscape, and is expected to reach USD 21.68 Billion in 2026. Market growth is driven by rising investments in water security projects, expanding urban infrastructure, desalination developments, and increasing efforts to improve access to sanitation services. Government-backed infrastructure programs and growing demand for sustainable water management solutions continue to support regional growth.

Latin America

Latin America accounted for USD 14.18 Billion in 2025, representing 5.40% of the global market share, and is projected to reach USD 14.72 Billion in 2026. The region’s growth is supported by increasing urbanization, rising demand for clean water and sanitation services, and ongoing investments in public utility infrastructure. Expansion of water distribution and wastewater treatment networks across emerging economies is expected to create long-term opportunities for market participants.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Focus On Mergers and Acquisitions to Lead the Industry

The leading companies in the industry are China State Construction Engineering Corporation Ltd., Vinci SA, Bechtel Corporation, Hochtief AG, and Webuild S.p.A. The companies use strategies such as strategic partnerships, mergers, and acquisitions to expand their market shares and leverage resources. They also focus on investing in R&D to launch new products, adopting cost-effective local manufacturing, and integrating smart technologies such as IoT and AI for improved efficiency and infrastructure monitoring.

LIST OF KEY WATER AND SEWER LINE CONSTRUCTION COMPANIES PROFILED

- China State Construction Engineering Corporation Ltd. (China)

- Vinci SA (France)

- Bechtel Corporation (U.S.)

- Hochtief AG (Germany)

- Webuild S.p.A. (Italy)

- China Communications Construction Company Ltd. (China)

- Michels Corporation (U.S.)

- Layne Christensen Company (U.S.)

- China International Water & Electric Corporation (China)

- Hassan Allam Holding (Egypt)

- Xylem Inc. (U.S.)

- Murray & Roberts Holdings Ltd. (South Africa)

- China Railway Construction Corporation Ltd. (China)

- China Railway Group Ltd. (China)

- Clarke Construction Group, LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2024- SA Water will be working with five major construction companies to deliver its record USD 3.3 billion capital program over the next four years. This capital program includes a USD 1.5 billion investment. This significant investment will help increase capacity of the water and sewer network through upgrades to pipes, pump stations and tanks, ultimately unlocking up to 40,000 new allotments across South Australia.

- February 2023- The Vortex Companies (Vortex), a leading provider of advanced trenchless water and sewer technologies and infrastructure renewal services, announced the addition of the small diameter IMS MICROcure LED CIPP Curing System (MICROcure) to its portfolio of UV CIPP solutions.

- September 2022- AECOM, the world’s trusted infrastructure consulting firm, announced it is expanding its Digital AECOM offering with the launch of PipeInsights, a digital platform that helps clients deliver superior rehabilitation and maintenance outcomes for their sewer systems.

- July 2021- Artera Services (“Artera”), one of the nation’s industry-leading providers of integrated infrastructure services to natural gas and electric industries, completed the previously announced acquisition of K.R. Swerdfeger Construction (“KRSC”). KRSC is a strong strategic fit for Artera, expanding its core gas distribution services into Colorado and New Mexico while strengthening its existing water and wastewater service offerings.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the water and sewer line construction market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attributes | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 3.80% from 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Segmentation | By Application, Service, and Region |

| By Application |

|

| By Service |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 262.85 billion in 2025 and is projected to reach USD 370.55 billion by 2034.

The market is expected to exhibit steady growth at a CAGR of 3.80% during the forecast period (2026-2034).

Aging infrastructure, urbanization and government infrastructure stimulus is speeding up the market growth.

China State Construction Engineering Corporation Ltd., Vinci SA, Bechtel Corporation, Hochtief AG, and Webuild S.p.A. are some of the top players in the market.

The Asia Pacific region held the largest market share.

Asia Pacific was valued at USD 101.76 million in 2025.

- 2021-2034

- 2025

- 2021-2024

- 199

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us