Water Recycle and Reuse Market Size, Share & Industry Analysis, By Technology (Membrane Filtration, Biological Treatment, Disinfection, Filtration and Adsorption, Advanced Oxidation/Advanced Treatment, and Others), By End-User (Industrial, Commercial, and Residential), and Regional Forecast, 2026-2034

Water Recycle and Reuse Market Overview

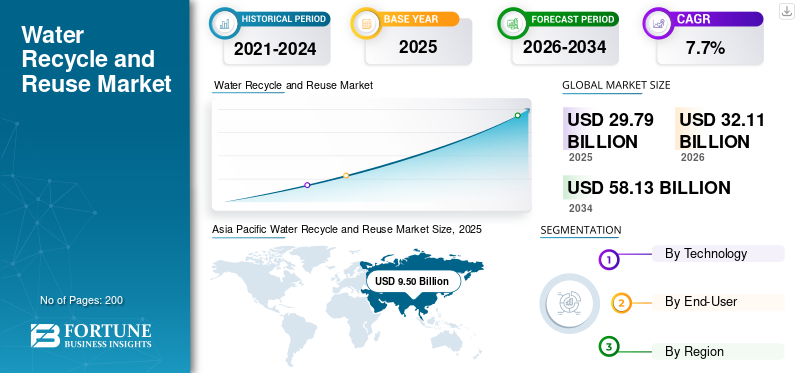

The water recycle and reuse market size was valued at USD 29.79 billion in 2025. The market is projected to grow from USD 32.11 billion in 2026 to USD 58.13 billion by 2034, exhibiting a CAGR of 7.7% during the forecast period. Asia Pacific dominated the water recycle and reuse market with a market share of 31.89% in 2025.

Water recycle and reuse refers to the technologies, systems, infrastructure, and services used to collect, treat, reclaim, distribute, and monitor used water for beneficial secondary use rather than discharge. The market includes municipal wastewater reclamation, industrial effluent recycling, tertiary polishing, greywater recycling, reuse-oriented storage and conveyance, and digital monitoring solutions deployed for non-potable and selected potable applications.

The market growth is driven by rising freshwater demand, tightening industrial sectors water-efficiency requirements, increasing urban demand for resilient non-conventional water supplies, and broader adoption of membrane-led advanced treatment systems. Similarly, policy support for circular water management, potable reuse readiness, and industrial water circularity is improving the economics of projects for utilities, commercial developments, and high-water-demand manufacturing sites.

Furthermore, the market comprises several major players, including Veolia Water Technologies, Xylem, SUEZ, DuPont, and Ecolab. A broad technology portfolio, strong reference projects, and multi-region engineering and service footprints support competitive positioning in this market.

WATER RECYCLE AND REUSE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 29.79 Billion

- 2026 Market Size: USD 32.11 Billion

- 2034 Forecast Market Size: USD 58.13 Billion

- CAGR: 7.7% from 2026–2034

- Asia Pacific dominated the water recycle and reuse market with a 31.89% share in 2025.

- The membrane filtration segment accounted for 26.0% of the market in 2025.

- The industrial segment held 48.2% of the market share in 2025.

Asia Pacific

Asia Pacific reached USD 9.50 billion in 2025, accounting for 31.89% of global market revenue.

North America

North America is projected to reach USD 8.85 billion in 2026.

Europe

Europe is projected to reach USD 5.93 billion in 2026, growing at a CAGR of 7.4%.

U.S.

The market was valued at USD 7.31 billion in 2025.

Japan

Japan remains a key contributor to the Asia Pacific market through advanced water reuse systems and industrial applications.

Read More

Download Free sample to learn more about this report.

WATER RECYCLE AND REUSE MARKET TRENDS

Municipal and Industrial Water Circularity and Regulatory Normalization are Significant Market Trends

Utilities and industrial users are adopting advanced membrane filtration, biologically robust treatment trains, UV, and advanced oxidation polishing, and digital monitoring to recover more water resources while meeting tighter quality targets. At the same time, governments are formalizing reuse policies and expanding funding and incentive mechanisms, thereby improving the bankability of commercial, industrial, and municipal reuse projects.

- For instance, in December 2023, China issued a guideline targeting more than 25% utilization of recycled water in water-scarce prefecture-level cities by 2025, while also calling for 100 green and low-carbon benchmark sewage treatment plants.

- In Singapore, PUB states that NEWater factories have a supply capacity of 760,000 m3/day, almost 40% of national water demand, demonstrating the commercial scale achievable in high-grade reclaimed-water systems.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Industrial Water Efficiency Requirements is Accelerating Market Growth

Water recycling and reuse are positioned as a practical response to constrained freshwater availability, drought risk, and rising demand from urban and industrial users. Reclaimed water helps utilities diversify their supply portfolios, while industrial facilities use internal recycling and external reclaimed-water sourcing to reduce raw-water withdrawals, improve compliance, and maintain operational continuity. Commercial campuses, data centers, hospitality assets, and mixed-use developments are also adopting reuse systems to reduce dependence on potable water and strengthen sustainability performance.

- For instance, the U.S. EPA states that more than 500 facilities in the U.S. recycle water to meet community needs, underscoring the maturity of reuse deployment in leading markets.

MARKET RESTRAINTS

High Capital Intensity and Regulatory Complexity Restricts Market Expansion

Reuse projects frequently require advanced treatment equipment, dual distribution or storage infrastructure, application-specific quality validation, and long development cycles with multiple stakeholders. Potable and industrial reuse projects also require costly polishing steps, concentrate handling, and redundancy measures. In many regions, permitting frameworks remain fragmented across wastewater, drinking water, industrial discharge, and urban planning authorities, which can delay project closure and raise implementation costs, thus limiting water recycle and reuse market growth.

MARKET OPPORTUNITIES

Reuse-Integrated Urban Infrastructure to Create Lucrative Growth Opportunities

Future opportunities are expanding in direct and indirect potable reuse, industrial minimal-liquid-discharge and zero-liquid-discharge systems, and reuse-integrated urban developments where reclaimed water supports cooling, flushing, landscaping, and process applications. Water-intensive sectors such as semiconductors, food processing, textiles, power, mining, and data centers are creating larger addressable opportunities for high-recovery treatment trains. Meanwhile, new industrial parks and smart-city projects are increasingly considering reclaimed water as a designed utility rather than a retrofit option.

- For example, the World Bank states that potable and industrial water reuse could grow eightfold by 2040 and unlock up to USD 340 billion in potential investment, indicating substantial headroom for scale-up.

MARKET CHALLENGES

High Energy Use and Fragmented Institutional Responsibilities Hampers Market Growth

Despite strong fundamentals, the market still faces challenges related to energy consumption in membrane-led systems, disposal or valorization of brines and concentrated residuals, public acceptance in selected potable reuse applications, and misaligned pricing that does not always reward water recovery. Project execution can also be slowed by fragmented institutional responsibilities, limited technical capacity in smaller municipalities, and the need to align treatment design with highly variable end-use water quality requirements.

Segmentation Analysis

By Technology

Membrane Filtration Segment Holds Largest Share due to its Growing Demand in Industrial Reuse

Based on technology, the market is segmented into membrane filtration, biological treatment, disinfection, filtration and adsorption, advanced oxidation/advanced treatment, and others.

The membrane filtration segment accounted for the largest water recycle and reuse market share in 2025. The segment is driven by the broad use of ultrafiltration, microfiltration, nanofiltration, and reverse osmosis in municipal reclamation, industrial reuse, and high-spec polishing trains. Furthermore, the segment held 26.0% share in 2025.

The biological treatment segment is expected to grow favorably throughout the forecast period, driven by MBR, MBBR, activated sludge, and hybrid secondary treatment platforms that remain central to cost-effective water recovery and polishing flowsheets. The segment is projected to grow at a 7.9% CAGR during the study period.

Moreover, the growth of advanced oxidation/advanced treatment segment is supported by potable-reuse readiness, micropollutant-removal requirements, and high-quality industrial process-water applications.

By End-User

To know how our report can help streamline your business, Speak to Analyst

Industrial Segment Dominates Due to Extensive Use of Reclaimed Water in Process and Utility Applications

By end-user, the market is categorized into industrial, commercial, and residential.

The industrial segment accounted for the largest share in 2025, driven by the large-scale use of reclaimed water in cooling systems, boiler feed preparation, process reuse, and water-intensity-reduction strategies across manufacturing facilities. Furthermore, the segment held 48.2% share in 2025.

The commercial segment is expected to experience favorable growth over the projected period. The segment's growth is supported by campuses, hotels, hospitals, malls, office complexes, and mixed-use developments seeking resilience and reduced dependence on potable water. It is expected to grow at a CAGR of 7.5% over the forecast period.

The residential segment is expected to experience favorable growth throughout the forecast period, driven by building-level greywater reuse, decentralized treatment systems, and the adoption of dual plumbing in drought-prone and high-density urban environments.

Water Recycle and Reuse Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Water Recycle and Reuse Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 9.50 billion, and is expected to maintain its leading share in 2026, at USD 10.31 billion. The region benefits from severe urban water stress across several markets, large industrial water demand, expanding wastewater treatment capacity, and stronger policy support for recycled water utilization. China remains the largest consumer base, while Singapore, Japan, and South Korea contribute significantly through advanced reuse systems and high-quality industrial applications.

China Water Recycle and Reuse Market

In 2025, the China market reached USD 12.2 billion, supported by large-scale municipal reclamation initiatives, industrial water circularity needs, and policy targets that favor higher recycled-water utilization in water-scarce cities.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is also a significant contributor to the market, with the market estimated to reach USD 8.85 billion by 2026. The market growth is supported by drought-resilience planning, preparedness for potable reuse, industrial water reuse in manufacturing and energy-intensive sectors, and the continued expansion of municipal reclaimed-water networks. The U.S. accounts for the majority of regional consumption through utility-scale reuse programs and industrial/commercial demand.

U.S. Water Recycle and Reuse Market

In 2025, the U.S. market was valued at USD 7.31 billion. The market is driven by reclaimed-water distribution systems, industrial water circularity initiatives, drought-related supply diversification, and continued momentum in advanced potable and non-potable reuse projects.

Europe

Europe is expected to experience significant growth in the coming years. During the forecast period, the European region is projected to grow at 7.4% and reach a valuation of USD 5.93 billion in 2026. The region's growth is driven by circular-economy priorities, increasing water stress in selected southern markets, the gradual adoption of common water-reuse rules, and growing industrial recirculation efforts. Germany remains a key industrial technology hub.

U.K. Water Recycle and Reuse Market

The U.K. market in 2025 was at USD 0.92 billion, representing approximately 2.6% of global market revenue.

Germany Water Recycle and Reuse Market

Germany’s market reached USD 0.77 billion in 2025, accounting for about 3.1% of global sales.

Latin America

Latin America is experiencing steady growth. The Latin America market in 2026 is expected to reach a valuation of USD 3.15 billion. Demand in the region is tied to industrial water-efficiency needs, sanitation upgrades, emerging reuse regulation and the selective adoption of reclaimed water in commercial and utility applications.

Brazil Water Recycle and Reuse Market

Brazil reached USD 1.17 billion by 2025, accounting for approximately 3.9% of global revenues.

The Middle East & Africa

The Middle East & Africa region is gradually expanding, and reached USD 3.87 billion in 2025. The market’s growth is driven by structural water scarcity, industrial city development, and rising use of treated water & wastewater in the GCC and other water-stressed economies. In several countries, limited freshwater availability and strong policy backing continue to improve the business case for advanced reuse and recovery systems.

GCC Water Recycle and Reuse Market

GCC reached USD 1.54 billion by 2025, accounting for approximately 5.2% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Expanding Integrated Technology Portfolios to Maintain Their Market Positions

Market competition is shaped by the ability to deliver fit-for-purpose treatment trains, manage lifecycle operating cost, meet local regulatory requirements, and integrate treatment with storage, distribution, monitoring, and water-recovery objectives. Leading suppliers differentiate through broad portfolios spanning biological treatment, membranes, disinfection, advanced oxidation, and high-recovery systems, alongside strong EPC, O&M, and digital optimization capabilities. Some of the key market players include Veolia Water Technologies, Xylem, SUEZ, DuPont, and Ecolab. Sustainability, energy efficiency, water recovery rate, and service-network depth are increasingly influencing procurement and supplier selection.

LIST OF KEY WATER RECYCLE AND REUSE COMPANIES PROFILED

- Veolia Water Technologies (France)

- Xylem (U.S.)

- SUEZ (France)

- DuPont (U.S.)

- Kurita America Inc. (Japan)

- TORAY INDUSTRIES, INC. (Japan)

- Ecolab (U.S.)

- Fluence Corporation Limited (U.S.)

- IDE Technologies (Israel)

- METAWATER Co., Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- September 2024: Shanghai’s first large-scale industrial reclaimed-water project, jointly launched by Waigaoqiao Shipbuilding and Shanghai Chengtou, was put into operation and is expected to save 700,000 tons of tap water annually, signaling broader industrial adoption of reclaimed water in China.

- July 2024: Veolia Water Technologies delivered the largest water reuse facility in Qatar for Katara Cultural Village, with freshwater savings of 5,000–15,000 m³/day, signaling stronger uptake of reuse in commercial, district cooling, and urban utility applications in the Gulf.

- April 2023: Orange County Water District and OC San completed the final expansion of the Groundwater Replenishment System to 130 MGD, recycling 100% of OC San’s reclaimable wastewater flows, signaling continued scale-up of large indirect potable reuse infrastructure.

- July 2022: Veolia launched an unprecedented wastewater reuse program in France, targeting around 100 compatible wastewater treatment plants and aiming to save ~3 million cubic meters of drinking water, signaling faster commercialization of compact reuse units in Europe.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.7% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Technology, End-User, and Region |

| By Technology |

|

| By End-User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights estimates that the global market size was USD 29.79 billion in 2025 and is projected to reach USD 58.13 billion by 2034.

Recording a CAGR of 7.7%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The industrial end-user segment led in the market.

Asia Pacific held the highest market share.

Veolia Water Technologies, Xylem, SUEZ, DuPont, and Ecolab are top players in the market.

The growth in global water stress is driving market growth.

The major factors expected to favor product adoption in the market are stronger reuse policies, and greater investment in advanced treatment and reuse infrastructure.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us