Weapon Mounts Market Size, Share & Industry Analysis, By Weapon Type (LMG & MMG, Heavy Machine Guns, Multi-Barrel Machine Guns, and Others), By Mount Architecture (Turreted Systems, Remote Weapon Stations (RWS), Open Mounts, and others), By Control System (Control Mode, Stabilization Level Mode, Fire-Control / Sensor Suite, and others), By Mobility (Integrated Static Mounts, Fixed but Relocatable Mounts, and others), By Caliber (Small Caliber, Medium Caliber, and others), By Platform, By End User (Military, Law Enforcement, Homeland Security, and others), and Regional Forecast 2026-2034

KEY MARKET INSIGHTS

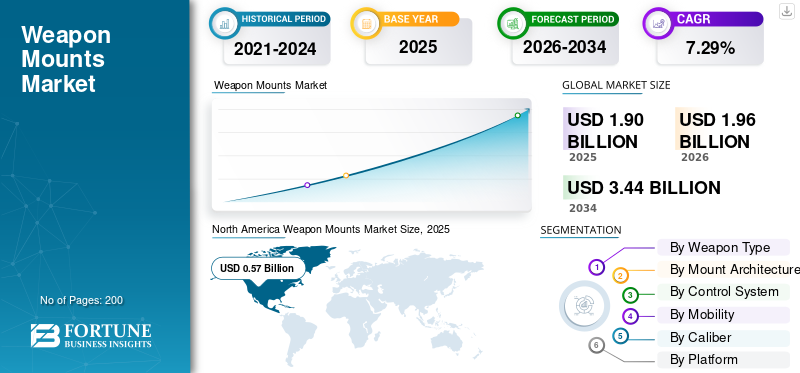

The global weapon mounts market size was valued at USD 1.90 billion in 2025. The market is projected to grow from USD 1.96 billion in 2026 to USD 3.44 billion by 2034, exhibiting a CAGR of 7.29% during the forecast period. North America dominated the global market with a market share of 30.% in 2025.

Weapon mounts are specialized mechanical or electromechanical assemblies designed to secure armaments onto military platforms, providing stability, recoil management, and targeting accuracy. The systems vary from simple manual pestle mounts and tripods to advanced gyro-stabilized Remote Weapon Stations allowing operation from within a protected vehicle hull. They are found across every domain in defense, with the majority share taken up by land applications, such as armored vehicles, tanks, and UGVs.

Such expansion is principally driven by a strategic shift toward increasing demand for crew survivability, whereby militaries are compelled to replace manual, exposed mounts with remote systems allowing soldiers to operate weapons from under armor.

The market is moderately concentrated, with the domination of Tier-1 defense primes such as Kongsberg Gruppen, BAE Systems, Rheinmetall AG, Elbit Systems, and so on that have advantages in economies of scale and global support networks.

Download Free sample to learn more about this report.

Weapon Mounts Market Key Takeaways

- 2025 Market Size: USD 1.90 billion

- 2026 Market Size: USD 1.96 billion

- 2034 Forecast Market Size: USD 3.44 billion

- CAGR: 7.29% from 2026–2034

- North America dominated the global market with a 30.16% share in 2025.

- Military segment dominated the market with an 82.39% share in 2025.

- LMG & MMG segment held the largest share of 20.34% in 2025.

North America

North America led the market in 2025, valued at USD 0.57 billion.

Asia Pacific

Asia Pacific is expected to witness the fastest growth due to indigenous defense manufacturing and modernization programs.

Europe

Europe is experiencing strong growth driven by fleet modernization and digital turret deployment.

U.S.

Growth supported by investments in mobile air defense and multi-mission weapon platforms.

Germany

Demand driven by advanced air-defense turret systems and military modernization programs.

Read More

Market Dynamics

Market Drivers

Proliferation of Asymmetric Threats and Counter-UAS Requirements Drive Market Growth

The rapid democratization of drone warfare has forced defense ministries to procure weapon mounts capable of kinetic counter-UAS missions. Traditional heavy caliber mounts are being adapted with high-elevation capabilities and airburst ammunition programming to effectively engage small aerial targets.

- For instance, in January 2024, EOS Defense Systems secured a USD 15 million contract to supply its Slinger counter-drone system to Diehl Defence for integration onto lightweight 4x4 platforms.

Furthermore, Rheinmetall's Skyranger 30 system represents the pinnacle of this driver; in August 2025, the company announced expectations for a framework contract worth up to USD 8 billion with the German Bundeswehr, with initial units delivered in January 2025, highlighting the critical need for mobile, stabilized air defense mounts.

Market Restraints

Supply Chain Fragility and Semiconductor Shortages Can Hamper Market Growth

It is an industry faced with acute production bottlenecks despite high demand due to persistent shortages in weapons-grade microelectronics and other critical raw materials. A report published in March 2025 indicated that while lead times have improved since 2022, the AI boom has drawn essential GPU and chip supply away from defense manufacturers, making lead times unpredictable. A November 2025 report by the USCC warned that reliance on Chinese PCBs presents a serious security threat, one potentially shutting down production lines if trade tensions escalate.

Market Opportunities

Unmanned Ground Vehicle (UGV) and USV Integration Catalyze Market Growth

The transition to robotic warfare creates a growing market for lightweight, low-recoil weapon mounts suitable for unmanned platforms. Unlike manned vehicles, UGVs need digitized mounts with complete, autonomous target acquisition and engagement protocols.

- In October 2025, Leonardo revealed the Lionfish 30 naval turret, which would suit both manned ships and future USVs, marking a strategic turn toward autonomous maritime defense.

Academic and industrial peer reviews in August of 2025 highlighted that the capacity to integrate modular payloads into UGVs was one of the critical force multipliers, driving a new market segment for mounts with a strong focus on power efficiency and data-link robustness, rather than traditional armor protection.

Market Challenges

Cybersecurity Vulnerabilities and Zero-Day Exploits Hinder Market Growth

As weapon mounts become increasingly networked and software-dependent, they inherit critical cybersecurity vulnerabilities. A report by Deepstrike.io from October 2025 stated that weaponization speed for new software vulnerabilities has accelerated, with 1 in 3 exploits occurring within 24 hours of disclosure.

This patch’s fast pressure is huge for the weapon systems, which traditionally have slow update cycles. Theoretically, an unpatched RWS could be hacked to disable firing circuits or, in a worst-case scenario, be remotely commandeered. The manufacturer thus faces a dual challenge of hardening these embedded systems against state-sponsored cyberattacks while maintaining the open architecture necessary for interoperability.

Weapon Mounts Market Trends

AI-Driven Fire Control and Edge Computing Systems Escalate Market Growth

Direct integration of AI into the fire control computer of the weapon mount is a requirement becoming standard for next-generation systems. This allows for aided target recognition (AiTR), where the mount identifies and prioritizes threats more quickly than a human operator could. EOS Defense Systems' Slinger system uses such advanced algorithms to track and strike erratic drone targets with a single shot.

Technological reviews from the end of 2025 show a movement toward edge AI, processing locally on the mount rather than a central vehicle computer, reducing latency critical to engage hypersonic or swarming threats. This forces mount manufacturers to be software-defined, differentiating their hardware through better code and sensor fusion algorithms.

Download Free sample to learn more about this report.

SEGMENTATION

By Weapon Type

LMG & MMG are Leading Weapon Types Owing to their Need in Close Range Defense

The global market is segmented by weapon type into LMG & MMG, heavy machine guns, multi-barrel machine guns, Automatic Grenade Launchers (AGL), Medium-Caliber Autocannons (20–40 mm), Large-Caliber Guns (≥ 57 mm), Anti-Tank Guided Missiles (ATGM), air-defense gun systems, and others.

The others segment encompassing mortars/auto-mortars in turrets, non-lethal mounts, hybrid/mixed packs, loitering munitions mounts, early DE mounts and so on is estimated to exhibit the fastest growth during the forecast period. Conventional kinetic projectiles are often beyond the price range or simply ineffectual against a swarm of cheap kamikaze drones. The defense forces are rapidly acquiring launch systems that can launch suicide drones far beyond line-of-sight engagements or deliver laser beams for low-cost aerial denial or non-lethal weapons. The segment is anticipated to deliver the highest CAGR of 10.87% during the forecast period.

The LMG & MMG sub-segment holds the largest market share of 20.34% and will grow at a CAGR of 5.67% during the forecast period. Dominance driven by practically all forms of military transport from logistics trucks and utility jeeps through main battle tanks will carry at least one auxiliary machine gun mount for closer defense protections.

By Mount Architecture

RWS’s Ability to Provide a Universal Interface Results in its Dominance

The global market is segmented by mount architecture into turreted systems, Remote Weapon Stations (RWS), open mounts, pedestal / post mounts, coaxial mounts, and infantry & ground support mounts.

Remote Weapon Station (RWS) is estimated to be the fastest growing sub-segment during the forecast period with a CAGR of 8.72%. RWS systems are increasing in popularity, since they provide a universal interface. Since an RWS has never been deeply installed inside a vehicle similar to a traditional manned turret, it can be described as a “bolt-on" system that does not penetrate the deck. It becomes an imperative component since an RWS can be transferred from an impaired vehicle to an unruffled one in an hour or less.

The turreted system accounted for the largest market share with 29.90% while growing at a CAGR of 7.99%. Turreted systems (both manned and unmanned) remain the market leader in terms of revenue and market presence as its architecture is designed to accommodate heavy weapons such as 30mm guns to 120mm tank guns along with the corresponding ammunition.

By Control System

Software / AI Layer Upgrades over Traditional Uses Drives Segment Growth

The global market is segmented by control system into control mode, stabilization level mode, fire-control / sensor suite, and software / AI layer.

The software / AI layer is estimated to be the fastest growing sub-segment with a CAGR of 8.84%. The segment is experiencing exponential growth that is driving change in military sales, where there is a transition from human-in-the-loop to human-on-the-loop operations.

The control mode accounted for the largest market share of 30.64% with a CAGR of 5.81%. The control mode sub-sector involving the hardware Fire Control Units (FCUs), hardened joysticks, grips, and servo drive electronics continues to generate the most revenue due to the 100% attach rate.

By Mobility

Dispersed Operations & Rapid Deployment Powers Containerized Segment’s Rapid Growth

By mobility, the market is segmented into integrated static mounts, fixed but relocatable mounts, man-portable infantry mounts, quick-detach modular mounts, and containerized.

Containerized sub-segment will exhibit the highest CAGR of 10.16%, driven by the operational shift toward Distributed Maritime Operations and Expeditionary Advanced Base Operations. The militaries are moving away from permanent, vulnerable bases to temporary, dispersed firing points.

The integrated static mounts accounted for the largest market share of 45.68% with a CAGR of 6.15%. The segment includes pintle mounts on vehicles, tripod systems, and fixed base defense turrets, due to the scale of global infrastructure protection. Every forward operating base, airfield, naval port, and border checkpoint requires dozens of fixed weapon points for perimeter security.

By Caliber

Economic Advantages of Directed Energy Caliber Increases its Adoption and Accelerates Growth

By caliber, the market is segmented into small caliber, medium caliber, missile-only mounts (no gun), and directed energy.

Directed energy is estimated to be the fastest-growing segment with a CAGR of 11.22%. The segment’s growth is driven by the cost-per-shot economic imperative. It is expanding fast as Navies and Land Forces rush to integrate HELs onto standard mounts to provide a bottomless layer of defense against swarms-effectively breaking the "cost curve" of modern air defense.

The small caliber segment remains dominant with a market share of 49.73% and a CAGR of 6.29%. The military logistics truck, every utility vehicle, and every light patrol craft has a ring mount or pintle station designed for these calibers.

By Platform

Increased Need for Asymmetric Threat Protection Accelerates Naval Platform’s Growth

By platform, the market is classified into land platforms, air platforms, and naval platforms

The naval platform is estimated to depict the fastest growth rate of 8.60% during 2026-2034. The growth is fueled by the need to safeguard high-value ships against low-cost asymmetric threats such as suicide Unmanned Surface Vehicles (USV) and swarming attacker boats.

The land platform sub-segment accounted for the largest market share of 57.46% with a CAGR of 7.10%. This position is reinforced by the doctrinal shift in arming "non-combat" vehicles. The need to equip fuel trucks, recovery vehicles, and engineering plant equipment with remote weapon stations to facilitate self-protection purposes propels the market growth.

By End User

To know how our report can help streamline your business, Speak to Analyst

PMSCs Fast Acquisitions of Weapon Mount Systems Sets them to Gain Quick Growth

By end user, the market is categorized into military, law enforcement, homeland security & border forces, and private sector.

The private sector is estimated to be the fastest growing segment with a CAGR of 9.44% during the forecast period. The growth is fueled by the increasing demand of the private security companies in contrast to military procurement which takes several years. PMSCs (Private Maritime Security Companies) are swiftly acquiring bolt-on fixed mounts and LMG posts to instantly harden merchant ships and consequently fueling an increase in the sales of Commercial off the Shelf (COTS) weapon mount sales.

The military segment accounted for the largest weapon mounts market share of 82.39% in 2025 by end user and is estimated to grow at a CAGR of 7.22%. The key reason for the dominance is the scale of the military’s business as emerging countries are not purchasing arms for warfare but are developing ‘all platforms’ forces on a massive scale for the security of their boundaries.

Weapon Mounts Market Regional Outlook

The global market is divided into North America, Europe, Asia Pacific, the Middle East & Africa and Latin America.

Asia Pacific

North America Weapon Mounts Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is estimated to be the fastest growing region with a CAGR of 8.96% impelled by aggressive indigenization mandates in India and major platform acquisitions in Australia and East Asia. The regional market is transitioning from direct imports to buy local frameworks that compel global OEMs to establish joint ventures for domestic manufacturing. For instance in February 2024, the Indian Ministry of Defence inked a contract with Advanced Weapon Equipment India Limited to supply 463 indigenous 12.7mm Stabilized Remote Control Guns for the Indian Navy-a pivotal shift away from foreign dependency.

North America

North America continues to lead with a 30.16% of the global weapon mounts market share due to huge, continuous investments in air defense and naval modernization programs that require high-end stabilized mounts. Emphasis is placed on swappable and multi-mission functionalities that combine kinetic weapons with directed energy and electronic warfare systems. In December 2024, Moog Inc. was awarded a follow-on contract to support the U.S. Army's SGT Stout (M-SHORAD) program for its Reconfigurable Integrated-weapons Platform (RIwP), which has become the standard for mobile air defense.

Europe

Europe is witnessing a sharp recovery in demand, driven by the imperative of restocking and replacing Cold War-era fleets with digital and networked turrets. The market is typified by cross-border consortiums and quick fielding of sovereign European solutions to lessen dependence on non-EU suppliers. In Euronaval 2024/2025, where KNDS, ex-Nexter, presented improved capabilities for its "RapidFire" naval turret, a 40mm system designed to autonomously engage aerial threats, now being fitted onto French naval platforms.

Middle East & Africa

The Middle East & Africa is developing strongly, impelled by a twofold strategy related to the diversification of arms suppliers and the development of defense industrial base, with particular regard for the UAE, Saudi Arabia, and Turkey. Local customers give priority to ruggedized systems operating in very hot and sandy environments, while counter drone integration is very welcome.

Latin America

Latin America is observing moderate yet consistent growth, driven for the most part by the modernization of aging armored vehicle fleets in Brazil, Chile, and Colombia. Here, the prevailing market dynamics favor cost-effective, modular upgrades rather than brand-new platform acquisitions, with a strong emphasis on technology transfer.

COMPETATIVE LANDSCAPE

Key Market Players

Growing Demand of Advanced Systems by Major Key Players Catalyze Market Expansion

The global weapon mounts market is moderately concentrated with a well-defined tiered hierarchy. The high-end segment is dominated by a few Tier-1 defense primes that provide fully integrated, stabilized Remote Weapon Stations for key government programs. These organizations leverage massive economies of scale and deep integration with vehicle OEMs to lock in long-term contracts and boost the weapon mounts market grow th.

Below them is a fragmented long tail of Tier-2 and Tier-3 manufacturers that compete aggressively in the manual mount, tripod, and light-vehicle retrofit segments. This bifurcation reflects asymmetric competition: top-tier players compete on system capability-software, sensor fusion, and support logistics-while lower-tier players compete almost exclusively on unit cost and production agility.

The fundamental basis of competitive advantage shifted from mechanical robustness to digital intelligence. Traditionally, manufacturers competed on weight reduction and recoil attenuation.

List of Key Weapon Mounts Companies Profiled

- Kongsberg Defence & Aerospace AS (Norway)

- FN Herstal SA (Belgium)

- Rafael Advanced Defense Systems Ltd. (Israel)

- Elbit Systems Ltd. (Israel)

- Rheinmetall AG (Germany)

- KNDS Deutschland GmbH & Co. KG (Germany)

- Nexter Systems SA (France)

- Denel Land Systems (South Africa)

- Electro Optic Systems Pty Ltd (Australia)

- Aselsan A.Ş. (Turkey)

- Saab AB (Sweden)

- Leonardo S.p.A (Italy)

- Thales Group (France)

- Bharat Electronics Limited (BEL) (India)

- Tata Advanced Systems Limited (TASL) (India)

KEY DEVELOPMENTS

- December 2025: German defense firm Rheinmetall has secured a major contract from the Netherlands for its Skyranger 30 air defense systems. The Skyranger weapon system includes a standard Skyranger 30 air defense turret with a lower mount, enabling it to be used mobile on armored combat support vehicles or in static ground operations.

- October 2025: EOS informed that it has secured a contract to deliver tailored Remote Weapon Stations (RWS) for the Australian Army's latest fleet of AS21 Redback infantry fighting vehicles.

- October 2025: MKU Limited entered into an agreement with the Indian Army to deliver 29,762 units of its advanced Netro NW 3000 Night Vision Weapon Sights. This deal, finalized under the authority of the Raksha Mantri, ranks as one of the largest orders for electro-optics ever made by the Indian Army.

- August 2025: The Ministry of Defence (MOD) has released a transparency notice indicating its plan to grant a four-year contract to ISTEC Services Limited for the provision of universal gun mount spare parts and related items.

- July 2025: The Indian Army is progressing steadily with its initiative to integrate long-range homegrown artillery systems, as the Advanced Towed Artillery Gun System (ATAGS) is prepared for its inaugural product model test, while the trial for the Mounted Gun System (MGS) technology demonstrator is pending.

REPORT COVERAGE

The global weapon mounts market analysis provides an in-depth study of market size & forecast by all the segments included in the report. It includes details on the weapon mounts market trends and market dynamics expected to drive the market expansion over the forecast period. It offers information on the technological advancements, new product type launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.29% from 2026-2034 |

|

Unit |

USD Billion |

|

Segmentation |

By Weapon Type · LMG & MMG · Heavy Machine Guns · Multi-Barrel Machine Guns · Automatic Grenade Launchers (AGL) · Medium-Caliber Autocannons (20–40 mm) · Large-Caliber Guns (≥ 57 mm) · Anti-Tank Guided Missiles (ATGM) · Air-Defense Gun Systems · Others By Mount Architecture · Turreted Systems · Remote Weapon Stations (RWS) · Open Mounts · Pedestal / Post Mounts · Coaxial Mounts · Infantry & Ground Support Mounts By Control System · Control Mode · Stabilization Level Mode · Fire-Control / Sensor Suite · Software / AI Layer By Mobility · Integrated Static Mounts · Fixed but Relocatable Mounts · Man-portable Infantry Mounts · Quick-detach Modular Mounts · Containerized By Caliber · Small Caliber · Medium Caliber · Missile-only mounts (no gun) · Directed energy By Platform · Land Platforms · Air Platforms · Naval Platforms By End User · Military · Law Enforcement · Homeland Security & Border Forces · Private Sector By Region North America (By Weapon Type, Mount Architecture, Control System, Mobility, Caliber, Platform, End User, and Country) · U.S. (By Platform) · Canada (By Platform) Europe (By Weapon Type, Mount Architecture, Control System, Mobility, Caliber, Platform, End User, and Country) · U.K. (By Platform) · Germany (By Platform) · France (By Platform) · Russia (By Platform) · Nordic Countries (By Platform) · Rest of Europe (By Platform) Asia Pacific (By Weapon Type, Mount Architecture, Control System, Mobility, Caliber, Platform, End User, and Country) · China (By Platform) · India (By Platform) · Japan (By Platform) · South Korea (By Platform) · Australia (By Platform) · Rest of Asia Pacific (By Platform) Middle East & Africa (By Weapon Type, Mount Architecture, Control System, Mobility, Caliber, Platform, End User, and Country) · Israel (By Platform) · Iran (By Platform) · Saudi Arabia (By Platform) · UAE (By Platform) · South Africa (By Platform) · Rest of the Middle East & Africa (By Platform) Latin America (By Weapon Type, Mount Architecture, Control System, Mobility, Caliber, Platform, End User, and Country) · Brazil (By Platform) · Argentina (By Platform) · Rest of Latin America (By Platform) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.90 billion in 2025 and is projected to reach USD 3.44 billion by 2034.

In 2025, North Americas market value stood at USD 0.57 billion.

The market is expected to exhibit a CAGR of 7.29% during the forecast period of 2026-2034.

The directed energy sub-segment is expected to hold the highest CAGR over the forecast period.

Proliferation of asymmetric threats and counter-UAS requirements are key factors driving the markets growth.

Kongsberg Gruppen, BAE Systems, Rheinmetall AG, Elbit Systems and among others are top players in the market.

North America dominated the market in 2025 in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us