Wide Band Gap Semiconductor Market Size, Share & Industry Analysis, By Material Type (Silicon Carbide (SiC), Gallium Nitride (GaN), and Others), By Device Type (Power Devices, RF Devices, and Optoelectronic Devices), By End-user (Automotive, Consumer Electronics, Telecommunications, Aerospace & Defense, Energy & Power, and Others) and Regional Forecast, 2026-2034

WIDE BAND GAP SEMICONDUCTOR MARKET SIZE AND FUTURE OUTLOOK

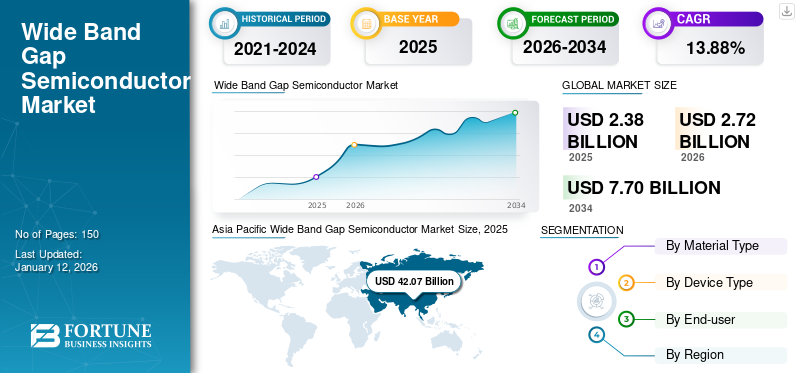

The global wide band gap semiconductor market size was valued at USD 2.38 billion in 2025 and is projected to grow from USD 2.72 billion in 2026 to USD 7.70 billion by 2034, exhibiting a CAGR of 13.88% during the forecast period. Asia Pacific dominated the market with a share of 42.07% in 2025.

The wide band gap semiconductor industry focuses on the production and development of materials such as silicon carbide (SiC), gallium nitride (GaN), Aluminium Nitride (AIN), and others. The market is expanding rapidly, particularly in sectors such as power semiconductors, automotive, telecommunications, and electronics devices. The growth is fueled by the superior characteristics of wide band gap semiconductors, including high thermal stability, low power losses, and the ability to operate under extreme conditions. Furthermore, advancements in technologies such as electric vehicles (EVs), 5G infrastructure, and smart grids are further propelling the demand for these materials.

Major companies in the market are driving innovation through advancements in SiC and GaN technologies. These firms leverage strategic partnerships, acquisitions, and extensive R&D investments to enhance power efficiency, improve thermal performance, and expand their applications in various sectors.

The COVID-19 pandemic initially disrupted the market due to supply chain interruptions and reduced manufacturing activities. However, the increasing adoption of digital technologies, remote work infrastructure, and growth in sectors such as healthcare and telecommunications during the pandemic accelerated demand for these semiconductors, fueling the wide band gap in semiconductor market growth.

Download Free sample to learn more about this report.

MARKET DYNAMICS

WIDE BAND GAP SEMICONDUCTOR MARKET TRENDS

Growing Adoption of Silicon Carbide (SiC) and Gallium Nitride (GaN) in Various Sectors Drives Market Progress

The growing adoption of GaN and SiC in Electric Vehicles (EVs) and renewable energy applications is driving the expansion of the market.

- For instance, according to industry experts, "Power Electronics for Electric Vehicles 2025-2035: Technologies, Markets, and Forecasts," examines the adoption of Si IGBTs, SiC MOSFETs, and GaN HEMTs, along with advancements in automotive power electronics technologies. The report highlights the market landscape, predicting it will reach USD 36 billion by 2035.

These materials offer superior energy efficiency, higher thermal stability, and reduced power losses compared to traditional semiconductors, making them ideal for applications requiring high performance and reliability. In the EV sector, SiC and GaN are increasingly used in power inverters, onboard chargers, and charging infrastructure to improve efficiency and extend vehicle range. Similarly, in renewable energy systems such as solar inverters and wind power converters, these materials enhance energy conversion efficiency and system durability. These factors align with the global focus on sustainability and energy-efficient technologies, significantly boosting the wide band gap semiconductor market share.

Market Drivers

Rapid Growth of 5G Telecommunications Infrastructure Fuels Market Growth

The demand for faster, more reliable mobile networks necessitates high performance components capable of handling higher frequencies, greater power densities, and challenging operating conditions. For instance,

- According to Ericsson, the global expansion of 5G continues, with approximately 320 networks launched worldwide in 2024.

Wide band gap semiconductors, particularly gallium nitride (GaN), are essential for these applications due to their superior ability to manage power and frequency levels, making them ideal for use in 5G base stations, signal amplifiers, and other critical components. As global investments in 5G infrastructure accelerate and the demand for enhanced data transmission capabilities rises, the need for these semiconductors continues to grow, driving the continued growth in the market.

Market Restraints

Higher Production Costs to Impede Market Expansion

The high production costs of materials such as silicon carbide (SiC) and gallium nitride (GaN), compared to traditional silicon-based semiconductors, pose a challenge to market growth. The manufacturing process for these materials is more complex and requires specialized equipment, further increasing costs. Additionally, the limited availability of skilled labor and a smaller number of suppliers in the market could impede the widespread adoption of wide band gap semiconductors. Moreover, integrating these materials into existing systems often requires significant adjustments, potentially slowing their adoption across different industries. These factors could present barriers to the wide band gap semiconductor market growth.

Market Opportunities

Growing Demand for EVs Presents a Significant Growth Opportunities for Market Players

As the automotive industry increasingly embraces electrification, wide band gap materials such as silicon carbide (SiC) and gallium nitride (GaN) are becoming critical components in EV powertrains, including power inverters, on-board chargers, and fast-charging stations.

- For instance, according to the International Energy Agency (IEA), nearly 14 million new electric cars were listed globally in 2023, bringing the total number of electric vehicles (EVs) on the roads to 40 million, raising the need for these materials.

These materials enable higher energy efficiency, faster charging times, and longer battery life, addressing key performance requirements in EVs. Additionally, the global push for reducing carbon emissions and the adoption of government incentives to promote EVs are expected to accelerate the demand for wide band gap semiconductors. This shift toward electric mobility provides a robust opportunity for market expansion, with wide band gap materials playing a major role in the ongoing development of next-generation EV technologies.

SEGMENTATION ANALYSIS

By Material Type

Rising Need to Operate at Higher Temperatures to Boost the Silicon Carbide (SiC) Segment Growth

Based on material type, the market is divided into Silicon Carbide (SiC), Gallium Nitride (GaN), and others.

Silicon carbide (SiC) segment is projected to dominate the market with a share of 57.13% in the market in 2026, due to its superior thermal conductivity, high breakdown voltage, and ability to operate at higher temperatures. It is ideal for power electronics applications such as electric vehicles and renewable energy systems. Its proven reliability and widespread adoption in high-power applications further contribute to its dominance.

Gallium nitride (GaN) is expected to grow at the highest CAGR due to its exceptional performance in high-frequency and high-power applications, such as 5G telecommunications and advanced radar systems. The increasing demand for faster, more efficient communication networks and the expansion of 5G infrastructure are key factors driving the rapid growth of the segment.

By Device Type

Power Devices Segment Dominates due to their Crucial Role in High-power Applications

Based on device type, the market is categorized into power devices, RF devices, and optoelectronic devices.

Power devices are expected to lead the market share by 48.38% in 2026, due to their critical role in high-power applications such as electric vehicles, renewable energy systems, and industrial applications. The superior efficiency and thermal stability of wide band gap materials such as SiC in power devices make them essential for optimizing energy conversion and reducing power losses in these sectors.

Radiofrequency (RF) devices are expected to witness the highest CAGR of 15.62% during the forecast period due to the growing demand for high-performance communication systems, particularly in 5G networks. The unique properties of these semiconductors, such as GaN, enable RF devices to operate at higher frequencies and power levels, making them ideal for the expanding telecommunications infrastructure.

By End-user

Growing Adoption of EVs Fuels the Automotive Sector Growth

By end-user, the market is categorized into automotive, consumer electronics, telecommunications, aerospace & defense, energy & power, and others.

The automotive segment is projected to dominate the market with a share of 29.48% in 2026 of the market share and the highest CAGR in the market due to the rapid adoption of electric vehicles (EVs) and the need for more efficient power systems in automotive applications. The increasing reliance on wide band gap materials such as silicon carbide (SiC) for power inverters, fast-charging stations, and battery management systems is driving significant market growth in the automotive industry.

Consumer electronics is expected to attain a CAGR of 16.56% during the forecast period in the market, as wide band gap semiconductors are increasingly used in energy-efficient and high performing devices such as smartphones, laptops, and wearable technology. The demand for faster charging and smaller, more efficient power supplies is pushing the adoption of wide band gap materials such as gallium nitride (GaN) in consumer electronics applications, contributing to its strong market position.

To know how our report can help streamline your business, Speak to Analyst

WIDE BANDGAP SEMICONDUCTORS MARKET REGIONAL OUTLOOK

Based on the region, the market is studied across Asia Pacific, North America, Europe, South America, and Middle East & Africa.

Asia Pacific

In 2025, Asia Pacific generated USD 1 billion, contributing 42.07% to global market revenue, and is projected to grow to USD 1.16 billion in 2026. large-scale adoption of advanced technologies, government support, and the presence of key players in the semiconductor industry.

- For instance, the Indian government has implemented various schemes throughout the electric vehicle (EV) value chain to promote production, adoption, and usage. In July 2023, NITI Aayog outlined a roadmap for sector growth, setting specific targets by vehicle type to reach a 30% EV sales penetration by 2030.

The region benefits from substantial investments in sectors such as electric vehicles, renewable energy, and telecommunications where wide band gap semiconductors are increasingly in demand. Additionally, countries such as China, Japan, and South Korea have rapidly expanded semiconductors adoption, further consolidating Asia Pacific's dominant market position.

Asia Pacific Wide Band Gap Semiconductor Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

China and Japan dominate the Asia Pacific market due to their significant contributions to the semiconductor manufacturing sector and the large-scale adoption of wide band gap materials. China’s rapidly expanding electric vehicle and renewable energy sectors drive demand for power electronics, while Japan remains a leader in advanced semiconductor production and research. Both countries have made substantial investments in high-performance electronic components, further solidifying their positions in the Asia Pacific market. The market in China is estimated to be USD 0.34 billion in 2026.

Download Free sample to learn more about this report.

Japan’s market size is anticipated to be valued at USD 0.27 billion in 2026 and India’s likely to be USD 0.22 billion in 2026.

North America

The North America region captured 27.51% of the global market in 2025, generating USD 0.65 billion in revenue, and is projected to reach USD 0.75 billion in 2026. recording the second-largest CAGR of 13.77% during the forecast period. due to its established automotive and technology industries, where high-performance electronic devices are in high demand. The region's focus on sustainability and innovation in electric vehicles, renewable energy, and 5G infrastructure is driving the adoption of wide band gap materials such as silicon carbide (SiC) and gallium nitride (GaN). Furthermore, significant research and development investments in semiconductor technologies have positioned the region as a key player in advancing wide band gap applications.

The U.S. market is projected to hit USD 0.44 billion in 2026. The U.S. dominates the North American market due to its strong presence of key industry players and significant government support for research and development. Additionally, the country benefits from a well-established semiconductor manufacturing ecosystem, advanced technological infrastructure, and increasing adoption of SiC and GaN devices across various industries.

Europe

Europe maintained a strong presence in the global market, reaching USD 0.51 billion in 2025, accounting for 21.35% share, and is expected to reach USD 0.58 billion in 2026. Europe holds a significant share of the market due to its strong focus on sustainability and green technologies, particularly in the automotive and energy sectors. The European Union's ambitious goals for electric vehicle adoption and renewable energy deployment have increased the demand for wide band gap materials, especially in power electronics and energy-efficient systems.

- For instance, in June 2024, Nexperia invested USD 200 million to develop next-generation wide band gap semiconductors, including silicon carbide (SiC) and gallium nitride (GaN), while expanding production infrastructure at its Hamburg site.

Countries in the region are heavily investing in smart grid technology and 5G infrastructure and are further driving the market for wide band gap semiconductors. The market in U.K. is likely to hit USD 0.14 billion in 2026. The market for France is expected to reach USD 0.08 billion and Germany’s market is likely to hit USD 0.12 billion in 2026.

Latin America

The Latin America market generated USD 0.08 billion in 2025, representing 3.37% of the global market landscape, and is expected to reach USD 0.09 billion in 2026.

Middle East & Africa (MEA) and South America

Middle East & Africa recorded a market size of USD 0.14 billion in 2025, capturing 5.69% of the global market share, and is projected to reach USD 0.15 billion in 2026. The Middle East & Africa and South America are expected to grow at a moderate pace in the market due to slower adoption of advanced technologies compared to other regions. While interest in electric vehicles and renewable energy is growing, the overall pace of technological development and infrastructure investment remains relatively slow. However, as global trends push toward sustainability and energy efficiency, there is potential for gradual growth in these markets, particularly in key industries such as automotive and telecommunications. The GCC market size is estimated to be USD 0.05 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Market Players Launch New Products to Strengthen their Market Positions

Players operating in the market are launching new products to enhance their market positions by leveraging technological advancements, addressing diverse consumer needs, and staying ahead of competitors. Companies prioritize portfolio enhancement through strategic collaborations, acquisitions, and partnerships to strengthen their product offerings. These strategic product launches help companies maintain and grow their market share in a rapidly evolving industry.

List of Companies Studied:

- Infineon Technologies AG (Germany)

- STMicroelectronics (Switzerland)

- Analog Devices, Inc. (U.S.)

- NXP Semiconductors (Netherlands)

- ROHM Co., Ltd. (Japan)

- Macom Technology Solutions (U.S.)

- TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION (Japan)

- Mitsubishi Electric (Japan)

- Fuji Electric Co., Ltd. (Japan)

- Vishay Intertechnology, Inc. (U.S.)

- Nexperia (Netherlands)

- KYOCERA AVX Components Corporation (U.S.)

- ON Semiconductor (U.S.)

- Texas Instruments (U.S.)

- SiTime Corporation (U.S.)

- Qorvo, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- December 2024- ROHM Co., Ltd. announced a strategic partnership with TSMC for the development and mass production of GaN power devices aimed at electric vehicle applications. The collaboration would combine ROHM's expertise with TSMC's leading GaN-on-silicon process technology to address the increasing demand for high-voltage and high-frequency properties in power devices, surpassing silicon-based solutions.

- November 2024- MACOM Technology Solutions Inc. was elected for a development project focused on advancing GaN on SiC process technologies for RF and microwave applications. The project aimed to develop semiconductor manufacturing processes for monolithic microwave integrated circuits (MMICs) and GaN-based materials that perform efficiently at high voltages and millimeter-wave frequencies.

- November 2024- NXP Semiconductors N.V. introduced its industry-first wireless battery management system (BMS) featuring Ultra-Wideband (UWB) capabilities. This innovative UWB BMS solution addresses development challenges, including expensive and complex manufacturing processes, and is expected to accelerate the adoption of electric vehicles (EVs).

- October 2024- Raytheon secured a three-year, two-phase agreement from DARPA to improve foundational ultra WBG semiconductors. The project focuses on utilizing diamond and aluminum nitride technology to enhance power delivery and thermal management in sensors and other electronic applications.

- November 2023- Mitsubishi Electric Corporation partnered with Nexperia to collaboratively develop SiC semiconductors for the power electronics market. The company would produce SiC MOSFET chips, which Nexperia utilizes to create SiC discrete devices.

INVESTMENT ANALYSIS AND OPPORTUNITIES

The market is experiencing significant growth driven by the increasing demand for energy-efficient devices in sectors such as automotive, renewable energy, and telecommunications. Key technologies such as silicon carbide (SiC) and gallium nitride (GaN) are leading the market due to their superior performance in high-voltage, high-frequency, and high-temperature environments. Investment in WBG semiconductor technologies is expected to continue rising as companies seek to capitalize on the shift toward electrification, renewable energy, and advanced power electronics.

For instance, in September 2024, FUJIFILM Corporation announced a USD 0.13 billion investment to enhance its semiconductor materials business, focusing on the development, production, and quality evaluation of advanced materials.

REPORT COVERAGE

The report provides a detailed market analysis and focuses on key aspects such as leading companies, product/service types, and leading product End-users. Besides, the report offers insights into the market trends and highlights vital industry developments. In addition to the factors above, the report encompasses several factors that contributed to the market's growth in recent years. The market segmentation is mentioned below:

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

|

Study Period |

2021-2034 |

|

|

Base Year |

2025 |

|

|

Forecast Period |

2026-2034 |

|

|

Historical Period |

2021-2024 |

|

|

Unit |

Value (USD Billion) |

|

|

Growth Rate |

CAGR of 13.88% from 2026 to 2034 |

|

|

Segmentation |

By Material Type, Device Type, End-user, and Region |

|

|

Segmentation |

By Material Type

By Device Type

By End-user

By Region

|

|

|

Companies Profiled in the Report |

|

|

Frequently Asked Questions

The market is projected to reach USD 7.70 billion by 2034.

In 2026, the market size stood at USD 2.72 billion.

The market is projected to grow at a CAGR of 13.88% during the forecast period.

By end-user, the automotive segment is leading the market.

The rapid growth of 5G telecommunications infrastructure is a key factor fueling market growth.

ROHM Co., Ltd., Mitsubishi Electric, Fuji Electric Co., Ltd., and Infineon Technologies AG are the top players in the market.

Asia Pacific holds the dominant position in the market.

Asia Pacific is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us