Wireless Testing Market Size, Share & Industry Analysis, By Offering (Hardware, Software, and Services), By Technology (WiFi, Bluetooth, 2G/3G, 4G/LTE, and 5G), By Application (Consumer Electronics, IT and Telecommunication, Automotive, Medical Devices, Aerospace and Defense, and Others) and Regional Forecast, 2026 – 2034

WIRELESS TESTING MARKET SIZE AND FUTURE OUTLOOK

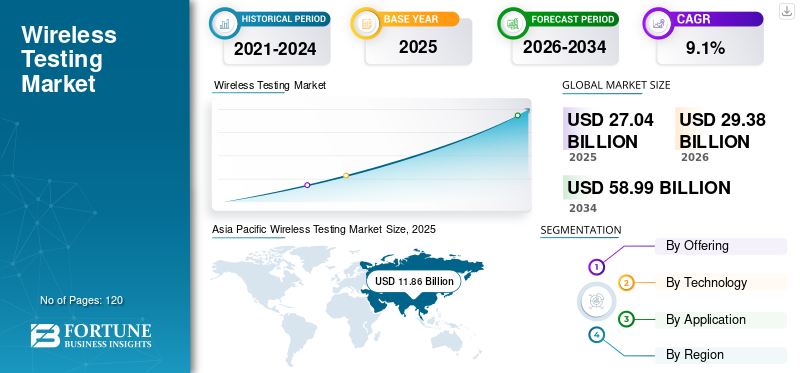

The wireless testing market size was valued at USD 27.04 billion in 2025. The market is projected to grow from USD 29.38 billion in 2026 to USD 58.99 billion by 2034, exhibiting a CAGR of 9.1% during the forecast period. Asia Pacific dominated the wireless testing market with a market share of 43.86% in 2025.

Wireless testing refers to the process of evaluating the performance, reliability, interoperability, and regulatory compliance of wireless devices, networks, and communication systems. It plays a critical role in ensuring that technologies such as Wi-Fi, Bluetooth, 4G/LTE, 5G, IoT, and other RF-based systems operate efficiently across different frequency bands, network conditions, and usage environments. The market is growing as connected devices, telecom infrastructure, smart vehicles, industrial IoT systems, and advanced communication networks become more complex and require accurate validation before deployment.

Additionally, the continuous expansion of wireless connectivity across consumer, enterprise, industrial, automotive, and telecom applications also boosts market expansion. As devices increasingly combine multiple wireless technologies, testing requirements are moving beyond basic signal validation toward advanced RF testing, over-the-air testing, protocol testing, network performance testing, coexistence testing, and certification support. The rollout of 5G, rising adoption of Wi-Fi 7, continued reliance on 4G/LTE, and growing demand for private wireless networks are further increasing the need for reliable and scalable wireless testing solutions.

Key companies such as Keysight Technologies, Inc., Rohde & Schwarz GmbH & Co. KG, Anritsu Corporation, and EXFO, Inc. are strengthening their presence through advanced wireless testing equipment, software-based testing platforms, automation capabilities, and solutions for emerging wireless standards. These players are also focusing on improving testing accuracy, reducing validation time, and supporting complex use cases such as 5G-Advanced, connected vehicles, IoT, and telecom network optimization, thereby playing a central role in the market growth.

Download Free sample to learn more about this report.

IMPACT OF GENERATIVE AI

Use of Generative AI in Intelligent Test Generation and Network Simulation Enhances Wireless Testing Efficiency

The use of generative AI in the market is enabling faster, more efficient, and intelligent testing processes by automating complex and time-consuming tasks. Generative AI can create realistic test scenarios by simulating various network conditions, user behaviors, interference patterns, and device movements, which helps validate wireless performance across real-world environments. For instance,

- In July 2025, A research paper on arXiv introduces AI5GTest, an AI-driven framework designed to automate the testing and validation of 5G O-RAN wireless components. It uses generative AI models to create test procedures, verify network behavior, and detect issues. The system significantly reduces manual effort while improving accuracy and speed.

It also enhances data analysis by quickly identifying failure patterns, signal degradation issues, latency bottlenecks, and interoperability challenges, reducing the time required for manual troubleshooting. In addition, generative AI supports advanced testing approaches such as digital twins and AI-driven network modeling, which are particularly important for 5G-Advanced and emerging 6G technologies.

WIRELESS TESTING MARKET TRENDS

Rising Integration of Multi-Connectivity Systems in Vehicles Drives Connected Vehicle Testing Trend

The trend of connected vehicle wireless testing is emerging in the market, as modern vehicles are increasingly becoming connected digital platforms equipped with multiple wireless technologies such as cellular, Wi-Fi, Bluetooth, GNSS, UWB, V2X, infotainment, and telematics systems. These technologies support functions such as navigation, remote diagnostics, over-the-air updates, driver assistance, and communication with other vehicles and infrastructure, which significantly increases the complexity of in-vehicle wireless environments.

As a result, there is a growing need for advanced testing solutions, including antenna testing, coexistence testing, field performance validation, and safety-focused reliability testing to ensure consistent performance across diverse real-world conditions such as urban areas, highways, tunnels, and remote locations. For instance,

- In April 2026, the Telecom Regulatory Authority of India began consultation on spectrum allocation and pricing for Vehicle-to-Everything (V2X) wireless communication. This system enables real-time data exchange between vehicles, infrastructure, pedestrians, and networks to support autonomous driving. The initiative is aimed at improving road safety, reducing accidents, and enabling smarter traffic management.

This trend is further strengthened by the shift toward autonomous driving and smart mobility, where reliable wireless connectivity is critical for safety and operational efficiency, thereby driving demand for comprehensive testing solutions across automotive OEMs, suppliers, and technology providers.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Increasing Adoption of Smart and Connected Devices Supports Market Growth

The growing number of connected devices is a major driver of the wireless testing market growth, as the global ecosystem of smartphones, wearables, smart home products, industrial sensors, routers, medical devices, and IoT modules continues to expand rapidly. For instance,

- According to Soax, the number of connected Internet of Things (IoT) devices worldwide reached 19.8 billion in 2025 and is projected to grow from 13.8 billion in 2022 to 24.2 billion by 2027, an increase of 10.4 billion devices, representing a 75% surge in just five years.

Each of these devices relies on wireless technologies such as cellular, Wi-Fi, Bluetooth, and other connectivity protocols to function effectively, which increases the need for thorough validation before commercial deployment. As device volumes grow across both consumer and industrial applications, manufacturers must ensure that products deliver consistent performance, maintain stable connectivity, and operate efficiently across different network environments and conditions. This expansion is further increasing the demand for comprehensive wireless testing, including RF performance testing, interoperability validation, coexistence testing, and regulatory compliance testing.

Market Restraints

High Cost of Advanced Testing Infrastructure Limits Market Growth

The high cost of wireless test equipment acts as a major restraint for market growth, as advanced technologies such as 5G, mmWave, and next-generation Wi-Fi require highly sophisticated and expensive testing infrastructure. Equipment such as high-frequency spectrum analyzers, vector signal generators, network analyzers, and Over-The-Air (OTA) chambers involves significant upfront investment, along with additional costs related to installation, controlled testing environments, and regular calibration.

As wireless technologies continue to evolve toward higher frequencies and more complex architectures, testing facilities are required to frequently upgrade or replace existing systems, further increasing the financial burden. This high cost limits the ability of small and mid-sized testing labs, start-ups, and regional manufacturers to adopt advanced testing capabilities, thereby restricting their participation in the market and slowing the overall expansion of wireless testing infrastructure.

Market Opportunities

Advancements in 5G-Advanced and Emergence of 6G Creates Lucrative Market Opportunities

The expansion of 5G-Advanced and future 6G testing presents a strong growth opportunity for the market, as networks evolve beyond basic connectivity toward more complex, high-performance use cases. 5G-Advanced enables applications such as massive MIMO, enhanced uplink, ultra-low latency communication, extended reality, industrial IoT, and intelligent network optimization. These advancements require devices and network infrastructure to operate efficiently across multiple frequency bands and dense environments, increasing the need for advanced RF, protocol, conformance, interoperability, and over-the-air testing.

Similarly, early development of 6G technologies is expected to accelerate demand for next-generation testing solutions. With the shift toward higher frequencies, AI-driven networks, and extremely low-latency applications, testing requirements will become more sophisticated. For instance,

- In February 2026, Ericsson conducted the world’s first live pre-standard 6G over-the-air trial in Texas, effectively serving as early wireless testing for next-generation networks. The test evaluated real-time performance, including AI-driven robotics control and video streaming. It focused on key wireless metrics such as latency, uplink efficiency, and spectrum use.

Segmentation Analysis

By Application

Continuous Network Validation and Infrastructure Testing Requirements Drives IT & Telecommunication Segment Growth

Based on application, the market is divided into consumer electronics, IT and telecommunications, automotive, medical devices, aerospace and defense, and others.

IT & Telecom held the majority in the wireless testing market share in 2025 as this segment directly depends on continuous validation of networks, devices, base stations, routers, antennas, and telecom infrastructure. Telecom operators and network equipment vendors require regular testing for signal quality, coverage, latency, handover performance, interoperability, and compliance, especially with the ongoing rollout of 4G/LTE, 5G, private networks, and Wi-Fi technologies. Unlike other applications, testing in IT and telecom is not limited to product launch stages but continues throughout network deployment, optimization, upgrades, and maintenance.

Automotive is expected to witness the highest CAGR of 13.1% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Offering

High Dependence on Advanced Test Equipment Across Wireless Ecosystem Boosts Hardware Segment Dominance

Based on offering, the market is segmented into hardware, software, and services.

Hardware held the majority share in 2025 with a share of 59.9%, as the core validation process depends on physical test instruments such as spectrum analyzers, signal generators, network analyzers, RF chambers, antennas, probes, and OTA test systems. As wireless devices move into higher frequency bands, especially 5G, mmWave, Wi-Fi 7, and V2X, testing requires more advanced and expensive equipment rather than only software-based tools. Hardware also needs frequent upgrades, calibration, and replacement to support new frequency ranges, antenna configurations, and compliance requirements.

Software segment is expected to witness the highest CAGR of 14.0% during the forecast period.

By Technology

Widespread Deployment and Continued Relevance of LTE Networks Propels 4G/LTE Segment Leadership

Based on technology, the market is segmented into WiFi, bluetooth, 2G/3G, 4G/LTE and 5G.

4G/LTE held the majority share of 32.4%, by application in 2025. It remains the most widely deployed and commercially active cellular technology across the globe, even as 5G adoption grows. A large installed base of LTE networks, devices, modules, and infrastructure continues to require ongoing testing for performance optimization, maintenance, interoperability, and compliance. Many regions, especially in emerging markets, still rely heavily on LTE for primary connectivity, while even in advanced markets, 5G operates alongside LTE through non-standalone architectures, further sustaining LTE testing demand.

5G is expected to witness the highest CAGR of 12.4% during the forecast period.

WIRELESS TESTING MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and Middle East & Africa.

North America

Asia Pacific Wireless Testing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the second largest share of the market due to strong presence of telecom operators, technology companies, semiconductor firms, and advanced device manufacturers. The region has been an early adopter of 5G, Wi-Fi 6/7, IoT, connected vehicles, and private wireless networks, creating steady demand for RF testing, OTA testing, network validation, and certification services. The U.S. also has strict wireless compliance requirements, which makes regulatory testing important for devices entering the market. North American market held a share of USD 6.31 billion in 2025.

U.S. Wireless Testing Market

Based on North America’s strong contribution, the U.S. market reached USD 5.23 billion in 2025, accounting for roughly 19.3% of sales.

Europe

Europe is projected to record a growth rate of 8.6% in the coming years, and reached a valuation of USD 4.15 billion in 2025. It is due to its mature telecom infrastructure, strong regulatory environment, and consistent adoption of advanced wireless technologies. The region already has established 4G/LTE and 5G networks, so growth is mainly driven by network upgrades, private 5G deployments, connected vehicle testing, industrial automation, and Wi-Fi 7 adoption rather than large-scale first-time infrastructure expansion. Europe’s strong automotive, aerospace, industrial, and medical device sectors also create recurring demand for RF, interoperability, OTA, and compliance testing.

U.K. Wireless Testing Market

The U.K. market in 2025 was at USD 0.55 billion, representing roughly 2.0% of global revenues.

Germany Wireless Testing Market

Germany’s market was at USD 0.65 billion in 2025, equivalent to around 2.4% of global sales.

Asia Pacific

Asia Pacific holds the largest share of the market and reached a valuation of USD 11.86 billion by 2025. It is due to its strong electronics manufacturing base, large telecom subscriber population, and rapid deployment of 4G/LTE, 5G, Wi-Fi, and IoT technologies. Countries such as China, Japan, South Korea, Taiwan, and India are major hubs for smartphones, consumer electronics, semiconductors, telecom equipment, and connected devices, all of which require extensive RF, OTA, interoperability, and compliance testing before launch. The region also has a dense network of telecom operators, device manufacturers, and certification labs, creating continuous demand for wireless testing across both product development and network deployment stages.

Japan Wireless Testing Market

The Japan market in 2025 was at USD 1.35 billion, accounting for roughly 5.0% of global revenues.

China Wireless Testing Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues valued at USD 4.19 billion, representing roughly 15.4% of global sales.

India Wireless Testing Market

The India market in 2025 reached USD 1.51 billion, accounting for roughly 5.6% of global share.

South America and Middle East & Africa

The Middle East & Africa is projected to record a highest growth rate of 11.0% in the coming years and reached USD 3.12 billion in 2025, as the fourth-largest market. This is due to rapid telecom modernization, expanding 5G rollouts, and rising investment in smart city, industrial connectivity, and digital infrastructure projects. GCC countries such as Saudi Arabia, the UAE, and Qatar are accelerating private networks, IoT deployment, connected mobility, and smart utility systems, all of which require RF, network performance, interoperability, and compliance testing.

South America is expected to record strong growth in the market as telecom operators in Brazil and Chile are rapidly expanding 5G coverage despite historically inconsistent network quality, increasing the need for extensive validation and performance testing. The region’s challenging geography, including rainforest areas, mountainous terrain, and remote industrial zones, makes network optimization and field testing more important than in other regions.

GCC Wireless Testing Market

The GCC market was valued at USD 0.81 billion in 2025, representing roughly 3.0% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Technological Advancements and Strategic Collaborations to Strengthen Market Position

Market players are continuously enhancing their testing solutions and product portfolios to address the growing complexity of wireless technologies such as 5G-Advanced, Wi-Fi 7, IoT, and connected devices. They are investing in advanced RF testing systems, automation capabilities, and software-defined testing platforms to improve accuracy, speed, and scalability. Keysight Technologies, Anritsu Corporation, VIAVI Solutions Inc., EXFO Inc. and SGS SA among others, are the largest players in the market.

LIST OF KEY WIRELESS TESTING COMPANIES PROFILED

- Keysight Technologies, Inc. (U.S.)

- Rohde & Schwarz GmbH & Co. KG (Germany)

- Anritsu Corporation (Japan)

- VIAVI Solutions Inc. (U.S.)

- LitePoint Corporation (U.S.)

- EXFO Inc. (U.S.)

- SGS SA (Switzerland)

- Bureau Veritas SA (France)

- Intertek Group plc (U.K.)

- UL Solutions Inc. (U.S.)

- DEKRA SE (Germany)

- Tektronix, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: University of British Columbia Okanagan researchers, led by Anas Chaaban, developed a new approach using nonlinear Stacked Intelligent Surfaces (SIS) to enhance wireless communication. This technology improves signal reliability, efficiency, and security by enabling AI-like processing of electromagnetic waves. The breakthrough could play a key role in advancing next-generation networks, including 6G.

- April 2026: UL Solutions began construction of a new EMC and wireless testing laboratory in Neu-Isenburg, Germany, to expand its capacity for testing large, high-power connected products. The facility will support industries such as automotive, medical, and consumer electronics with advanced testing for connectivity, cybersecurity, and performance.

- January 2026: Keysight Technologies has launched a new Wireless Coexistence Test Solution to help engineers validate device performance in crowded RF environments. The automated platform aligns with ANSI C63.27 standards, reduces testing time by over 50%, and improves repeatability while identifying interference risks early. It supports real-world simulation with predefined scenarios and scalable signal generation.

- December 2025: SGS expanded its wireless testing capabilities after its Piracicaba lab in São Paulo received accreditation from Brazilian authorities INMETRO and ANATEL. The facility can now conduct advanced safety, quality, and certification testing for technologies like Wi-Fi, Bluetooth, and 2G–5G devices. This strengthens local support for manufacturers and speeds up product certification for both Brazilian and global markets.

- February 2025: Wellell has adopted wireless testing solutions from Anritsu to ensure the quality and stability of its IoT-enabled medical devices. Using tools such as the MT8821C and MT8862A, Wellell can test connectivity for technologies including LTE and Wi-Fi 7. This collaboration enhances device reliability, reduces testing time, and supports the development of safer, high-quality smart healthcare products.

- October 2024: Spirent Communications launched new 5G Fixed Wireless Access (FWA) testing services to help telecom operators and device makers evaluate network performance. The solution includes lab testing and real-world benchmarking for services like video streaming, gaming, and web browsing. It aims to improve user experience, identify network issues early, and reduce troubleshooting costs.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies. Besides, it offers insights into the market trends and highlights key industry developments. In addition to the factors above, it encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.1% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Offering, Technology, Application and Region |

| By Offering |

|

| By Technology |

|

| By Application |

|

| By Geography |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 27.04 billion in 2025 and is projected to reach USD 58.99 billion by 2034.

The market is projected to grow at a CAGR of 9.1% during the forecast period of 2026-2034.

The IT & telecom segment holds the highest share of the market.

Increasing adoption of smart and connected devices supporting market growth.

Keysight Technologies, Inc., Rohde & Schwarz GmbH & Co. KG, Anritsu Corporation, and EXFO, Inc. are the top players in the market.

Asia Pacific is expected to hold the highest market share.

By application, automotive is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us