Women Health Diagnostics Market Size, Share & Industry Analysis, By Product (Diagnostic Devices, Diagnostic Test Kits, and Standalone Consumables & Reagents), By Technology (Immunoassay, Molecular Diagnostics, Imaging, and Others), By Application (Cancer, Infectious Diseases, Osteoporosis, Pregnancy, Fertility & Prenatal Diagnostics, and Others), By End-user (Hospitals, Specialty Clinics, Diagnostic Laboratories, Homecare, and Others), and Regional Forecast, 2026-2034

Women Health Diagnostics Market Size and Future Outlook

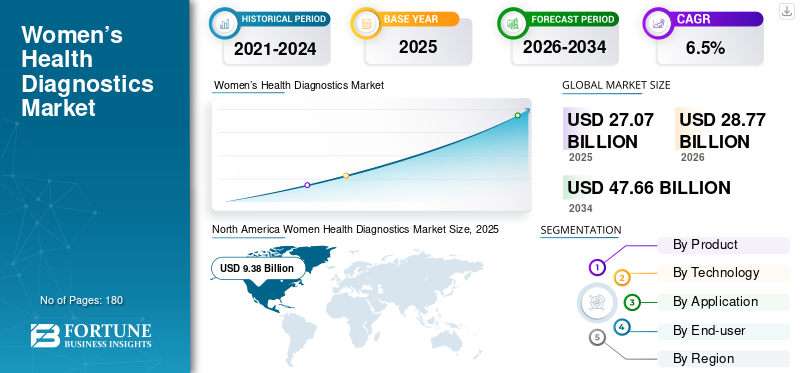

The global women health diagnostics market size was valued at USD 27.07 billion in 2025. The market is projected to grow from USD 28.77 billion in 2026 to USD 47.66 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period. North America dominated the women health diagnostics market with a market share of 34.65% in 2025.

Women’s health diagnostics includes tests and imaging devices to detect, stratify risk, and monitor conditions that extremely affect women, most particularly in Sexually Transmitted Infections (STIs), cervical and breast cancers, fertility & reproductive endocrinology disorders, and pregnancy or prenatal risks. The market’s growth is attributed to increasing screening programs, women’s health funding, and awareness about women's health diagnoses, which drives the demand for products such as devices and tests.

Furthermore, Hologic, Inc., GE HealthCare, and Koninklijke Philips N.V. held the highest market share, driven by strategic initiatives such as collaborations, new product launches, and other initiatives.

Download Free sample to learn more about this report.

WOMEN HEALTH DIAGNOSTICS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 27.07 Billion

- 2026 Market Size: USD 28.77 Billion

- 2034 Forecast Market Size: USD 47.66 Billion

- CAGR: 6.5% from 2026–2034

- North America dominated the women health diagnostics market with a 34.65% share in 2025.

- Diagnostic devices accounted for the largest product segment in 2025.

- The cancer segment is projected to hold 37.5% of the market in 2026.

North America

North America generated USD 9.38 billion in 2025 and accounted for 34.65% of the global market.

Asia Pacific

Asia Pacific is projected to reach USD 8.35 billion in 2026, making it the second-largest regional market.

Europe

Europe is expected to reach USD 5.90 billion in 2026, growing at a CAGR of 5.8% during the forecast period.

U.S.

The women health diagnostics market is projected to reach USD 9.09 billion in 2026, representing 31.6% of global revenue.

Japan

The women health diagnostics market is projected to reach USD 1.25 billion in 2026, accounting for approximately 4.3% of global revenue.

Read More

WOMEN HEALTH DIAGNOSTICS MARKET TRENDS

AI-enabled Women’s Imaging and Workflow Automation to Emerge as a Key Trend

Currently, breast diagnostics is increasingly shaped by artificial intelligence, supporting detection, density assessment, triage, and workflow arrangement. Health systems seek faster turnaround times and consistent diagnostic accuracy. In response, leading companies are forming partnerships and offering bundled solutions.

For instance, in November 2024, GE HealthCare and RadNet's DeepHealth announced a collaboration to develop SmartTechnology AI solutions for imaging, starting with integrating DeepHealth’s SmartMammo into GE’s Senographe Pristina mammography system to boost breast cancer screening efficiency and accuracy.

Such a trend is enhancing radiologists' efficiency, reducing unnecessary biopsies, and driving the demand for advanced imaging equipment.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of Overall Women's Health Test Kits to Fuel Market Growth

In recent years, there has been an increase in women entering routine cervical cancer screening, breast imaging, and STI testing, supported by public health initiatives, guideline updates, and increased payer coverage.

Moreover, the increasing incidence of chronic conditions such as osteoporosis, cancer, and infertility is additionally driving the demand for diagnostic test kits and devices, including follow-up diagnoses. Such a scenario is anticipated to drive the global women health diagnostics market growth.

For instance, in December 2025, the National Breast Cancer Foundation, Inc. stated that approximately 316,950 women in the U.S. are projected to receive a diagnosis of invasive breast cancer, alongside 59,080 cases of non-invasive (in situ) breast cancer.

MARKET RESTRAINTS

Reimbursement Gaps and Affordability for Advanced Testing to Restrict Market Growth

Despite significant adoption of advanced tests in high-income markets, reimbursement gaps are expected to lag novel diagnostics, slowing uptake and forcing manufacturers to rely on legacy methods.

Moreover, the cost pressure is augmented where women’s health budgets compete with broader chronic disease priorities, limiting the adoption of advanced products in lower-resource settings. Also, several other tests are hindered by limited government initiatives.

MARKET OPPORTUNITIES

Decentralized and At-home Pathways to Create Significant Growth Opportunities

In recent years, a significant amount of the women population is moving toward outside traditional exam rooms for diagnosis, while keeping lab-grade accuracy. One such example is the evolution of cervical screening from clinician-collected samples to self-collection. As a result, several at-home cervical cancer screening tests are being approved in the market.

For example, following clinic-based self-collection approvals, the U.S. FDA approved the first at-home cervical cancer screening test (Teal Health) in May 2025, creating a scalable direct-to-consumer and telehealth funnel to increase participation in screening.

MARKET CHALLENGES

Operational Complexity and Compliance in Multi-step Pathways to Challenge Market Expansion

Women’s diagnostics often require multi-step pathways across different sites. Each added step introduces a drop-off risk and operational load, including lab capacity, follow-up navigation, and sample logistics. New models, such as self-collection, increase reach but also require robust labeling, clear patient instructions, stable transport, and well-defined referral workflows when results are positive.

Moreover, scaling Artificial Intelligence (AI) in imaging introduces additional hurdles, including validation across populations, medico-legal responsibility, integration into PACS/RIS, clinician trust, and ongoing performance monitoring. These execution challenges are expected to hinder the real-world impact, even with the availability of advanced technology.

Segmentation Analysis

By Product

Automation and Upgrades in Diagnostic Devices Supports its Dominance

Based on product, the market is segmented into diagnostic devices, diagnostic test kits, and standalone consumables & reagents.

To know how our report can help streamline your business, Speak to Analyst

The diagnostic devices segment accounted for the largest women health diagnostics market share in 2025. Diagnostic devices are a foundational structure in hospitals and labs, and must be installed to support high-throughput women’s health menus. The upgrades in such devices are pushed by automation, faster turnaround time, and connectivity.

The diagnostic test kits segment is projected to grow at a CAGR of 7.1% during the forecast period.

By Technology

Immunoassay is the Leading Technology Due to its Cost-Effectiveness

By technology, the market is segmented into immunoassay, molecular diagnostics, imaging, and others.

The immunoassay segment accounted for the largest market share in 2025 owing to the cost-effectiveness and scalability of routine women’s health testing, which covers fertility or reproductive hormones, pregnancy-related markers, and oncology adjunct markers. Moreover, the segment is anticipated to hold a 32.6% market share in 2026.

The molecular diagnostics segment is anticipated to grow at a CAGR of 6.7% over the forecast period.

By Application

High Incidence of Lung Cancer to Boost the Segmental Growth

By application, the market is classified into cancer, infectious diseases, osteoporosis, pregnancy, fertility & prenatal diagnostics, and others.

The cancer segment accounted for the largest market share in 2025 fueled by the growing incidence of cervical and breast cancer, which is driving the demand for biopsy, imaging, pathology, and other screening tests. Moreover, the segment is projected to hold a 37.5% share in 2026.

- For instance, according to the data from the American Cancer Society, Inc. in November 2025, about 13,360 new cases of invasive cervical cancer were estimated to be diagnosed in the same year.

Additionally, the infectious diseases segment is expected to grow at a CAGR of 6.8% during the forecast period.

By End-user

Hospitals Dominate Due to the Availability of Several Procedures in these Settings

On the basis of end-user, the market is segmented into hospitals, specialty clinics, diagnostic laboratories, homecare, and others.

In 2025, hospitals dominated the market owing to a large number of hospitals worldwide, contributing to a significant volume of pregnancy, cancer screening, infectious disease, and other tests in these settings. Furthermore, the segment is set to hold 36.1% market share in 2026.

- For example, according to the American Hospital Association (AHA) Fast Facts, as of early 2025, there are 6,093 total hospitals in the U.S.

The diagnostic laboratories segment is projected to grow at a CAGR of 7.0% during the forecast period.

Women Health Diagnostics Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Women Health Diagnostics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest share of revenues in 2024, valued at USD 8.86 billion, and reached USD 9.38 billion in 2025. The growth is attributed to the increasing prevalence of osteoporosis in women, which is anticipated to drive the demand for osteoporosis tests.

In September 2025, the National Center for Biotechnology Information (NCBI) reported that epidemiological studies indicate a steady rise in osteoporosis, with a prevalence of 23.0% among women compared to 11.0% among men.

U.S. Women Health Diagnostics Market

In 2026, the U.S. is anticipated to reach USD 9.09 billion, accounting for approximately 31.6% of the global market.

Europe

Europe is projected to record a 5.8% growth rate during the forecast period, the third-highest globally, reaching USD 5.90 billion by 2026. The strong presence of specialty clinics and diagnostic laboratories is primarily expected to drive the region’s growth.

U.K. Women Health Diagnostics Market

The U.K. market is projected to reach USD 0.96 billion by 2026, representing approximately 3.4% of global revenues.

Germany Women Health Diagnostics Market

Germany is predicted to reach around USD 1.58 billion by 2026, representing around 5.5% of global revenue.

Asia Pacific

In 2026, Asia Pacific’s market is projected to reach approximately USD 8.35 billion, making it the second-largest market worldwide. The growth is attributed to a higher patient pool of breast cancer, osteoporosis, and infectious diseases, which is driving the demand for women's health tests and devices.

Japan Women Health Diagnostics Market

Japan is projected to generate approximately USD 1.25 billion in revenue by 2026, representing nearly 4.3% of the global market.

China Women Health Diagnostics Market

The Chinese market is anticipated to reach around USD 3.39 billion by 2026, accounting for nearly 11.8% of global revenues.

India Women Health Diagnostics Market

India is expected to generate approximately USD 1.90 billion by 2026, representing around 6.6% of the global market revenue.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are anticipated to witness moderate growth, with Latin America anticipated to reach approximately USD 2.96 billion in 2026. The growth is attributed to increasing government initiatives for women's health diagnosis, boosting the adoption of tests.

GCC Women Health Diagnostics Market

In 2026, the GCC market is estimated to reach approximately USD 0.92 billion, representing around 3.2% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

New Launches and Partnerships to Strengthen Market Position of Key Players

In 2025, Hologic, Inc., GE HealthCare, and Koninklijke Philips N.V. held the major market share. These companies emphasize on launching new product launches and expand their distribution networks and partnerships. Moreover, other major players, including Quest Diagnostics Incorporated and Abbott are expanding their geographic reach and investments to gain a significant market share in the upcoming years.

LIST OF KEY WOMEN HEALTH DIAGNOSTICS COMPANIES PROFILED

- Thermo Fisher Scientific Inc. (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- Hologic, Inc. (U.S.)

- Cardinal Health, Inc. (U.S.)

- Quest Diagnostics Incorporated (U.S.)

- Abbott (U.S.)

- BD (U.S.)

- GE Healthcare (U.S.)

- Koninklijke Philips N.V. (Netherland)

- Aspira Women's Health (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2025: BD submitted an FDA application for a new at-home HPV self-collection test using a simple Q-tip-sized swab, processed via BD COR System robotics to detect more high-risk HPV strains than other tests.

- May 2025: Abbott received FDA clearance for its Alinity m STI Assay, the first test to simultaneously detect and differentiate four common sexually transmitted infections, including Chlamydia trachomatis, Neisseria gonorrhoeae, Trichomonas vaginalis, and Mycoplasma genitalium, from a single swab or urine sample.

- October 2024: Family Medical Practice launched Siemens Healthineers' MAMMOMAT Inspiration 3D mammography system, integrated with Transpara AI, to enhance breast cancer detection accuracy.

- May 2025: Frame and Labcorp announced a partnership to expand access to fertility testing, integrating Frame's virtual care model with Labcorp's diagnostics, like hormone panels, semen analysis, and genetic screening.

- May 2024: BD received FDA approval for women in the U.S. to self-collect vaginal samples for HPV testing using the BD Onclarity Assay in healthcare settings such as pharmacies or mobile clinics.

- May 2024: Hoffmann-La Roche Ltd received FDA approval for its HPV self-collection solution, one of the first in the U.S., enabling women to privately collect vaginal samples in healthcare settings for analysis on cobas systems.

- April 2024: GE HealthCare showcased its Mobile Mammography Screening Truck alongside the latest MyBreastAI Suite and Pristina Bright at the SBI 2024 Breast Cancer Imaging Symposium in Montreal.

REPORT COVERAGE

The report provides an in-depth analysis across all market segments, highlighting primary drivers, emerging trends, growth opportunities, key restraints, and potential challenges that shape the landscape. It also explores cutting-edge technological advancements, key disease prevalence, significant industry developments, company market share analysis, and company profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Technology, Application, End-user, and Region |

| By Product |

|

| By Technology |

|

| By Application |

|

| By End-user |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 27.07 billion in 2025 and is projected to reach USD 47.66 billion by 2034.

In 2025, the market value of North America stood at USD 9.38 billion.

The market is expected to exhibit a CAGR of 6.5% during the forecast period of 2026-2034.

The diagnostic devices segment led the market by product.

Expansion of overall womens health test kits are the key factors that fuel market growth.

Hologic, Inc., GE HealthCare, and Koninklijke Philips N.V. are among the prominent players in the market.

North America dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us