Zero Waste Packaging Market Size, Share & Industry Analysis by Material (Paper & Paperboard, Bioplastics & Biopolymers, Glass, Metal, and Others), By Type (Recyclable, Reusable, Compostable, and Others), By End-use Industry (Food & Beverages, Healthcare, E-commerce, Personal Care & Cosmetics, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

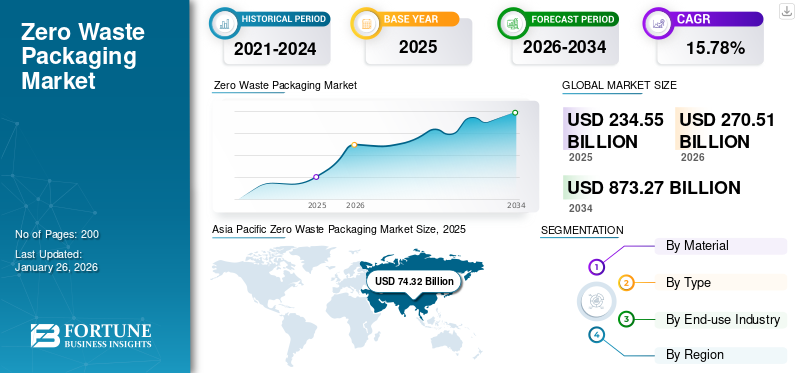

The global zero waste packaging market size was valued at USD 234.55 billion in 2025 and is projected to grow from USD 270.51 billion in 2026 to USD 873.27 billion by 2034, exhibiting a CAGR of 15.78% during the forecast period. Asia Pacific dominated the zero waste packaging market with a market share of 31.69% in 2025.

Zero waste packaging pertains to packaging solutions that aim to eradicate waste by encouraging reuse, recycling, or composting once they reach the end of their life cycle. This concept is in harmony with the circular economy, striving to lessen environmental impact by guaranteeing that packaging materials do not find their way into landfills or oceans. Such packaging frequently employs biodegradable, compostable, or entirely recyclable materials, and may also feature refillable or reusable designs to reduce single-use waste. The rising demand for such packaging solutions amongst several end-use industries enhances the market development.

Furthermore, the market encompasses several key players, DS Smith, Smurfit Kappa, and Huhtamaki Oyj, at the forefront. Broad portfolio with innovative product launches and strong initiatives for expansion of geographical presence have supported the leading positions of these companies in the global market.

Download Free sample to learn more about this report.

ZERO WASTE PACKAGING MARKET KEY TAKEAWAYS

Market Size & Forecast

Market Size & Forecast

- 2025 Market Size: USD 2.46 Billion

- 2026 Market Size: USD 3.33 Billion

- 2034 Forecast Market Size: USD 7.27 Billion

- CAGR: 11.80% from 2026–2034

Market Share

Market Share

- Asia Pacific dominated the zero waste packaging market with a market share of 31.69% in 2025.

- Recyclable packaging dominated the type segment with an expected 46.82% share in 2026.

- Food & Beverages held the largest end-use industry share, accounting for an expected 43.18% in 2026.

Key Regional Highlights

Key Regional Highlights

North America

North America held 24.75% of the global market share, reaching a valuation of USD 58.06 billion, and is projected to grow to USD 67.06 billion in 2026.

Europe

The market in europe is projected to reach USD 54.21 billion in 2026.

Asia Pacific

Asia Pacific contributed approximately USD 74.32 billion to the global market in 2025, accounting for 31.69% share, and is expected to reach USD 86.45 billion in 2026.

U.S.

In 2026, the U.S. market is estimated to have reached USD 52.83 billion.

Japan

Advanced recycling infrastructure and increasing adoption of reusable packaging systems are supporting market expansion.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing Environmental Concerns and Sustainability Awareness to Drive the Market Growth

The heightened awareness regarding the detrimental impacts of plastic waste on the environment has resulted in a growing inclination toward eco-friendly and recyclable packaging. Authorities, businesses, and consumers are stressing the importance of sustainable packaging options that reduce landfill waste. The worldwide movement toward carbon neutrality and circular economy principles is urging companies to implement zero waste packaging to lessen their environmental impact and adhere to sustainability requirements. This increasing eco-awareness is a significant factor driving the zero waste packaging market growth.

MARKET RESTRAINTS

High Upfront Cost of Sustainable Packaging Materials to Impede the Market Growth

A significant limitation in the zero-waste packaging sector is the increased cost linked to biodegradable or compostable materials when compared to conventional plastic packaging. Materials such as plant-based polymers, paper composites, and reusable containers necessitate more intricate manufacturing processes, which in turn raise production costs. This disparity in expenses poses challenges for small and medium enterprises (SMEs) aiming to shift to zero waste packaging, thereby hindering broader acceptance.

Moreover, in numerous developing areas, the absence of effective recycling and composting systems presents a significant obstacle to the establishment of zero-waste initiatives. In the absence of adequate facilities to handle biodegradable or reusable materials, the anticipated environmental advantages are not completely achieved. This deficiency in infrastructure limits the expansion of zero-waste packaging, especially in emerging markets.

MARKET OPPORTUNITIES

Technological Advancements and Material Innovation to Offer Profitable Growth Opportunities

Advancements in bio-based materials, nanotechnology, and packaging design offer profitable prospects for manufacturers of zero waste packaging solutions. Firms are creating innovative materials sourced from agricultural waste, seaweed, and mushroom mycelium, which provide both utility and compostability. Additionally, smart packaging technologies that facilitate reuse and refill systems are beginning to surface, generating new market opportunity and enhancing circularity within supply chains.

ZERO WASTE PACKAGING MARKET TRENDS

Technological Advancements and Circular Economy Initiatives to Emerge as a Market Trend

The global market is witnessing a significant trend focused on innovative materials and practices related to the circular economy. Businesses are increasingly allocating resources toward research and development to create cutting-edge biodegradable polymers, hybrid composites of paper and plastic, as well as coatings that improve strength and moisture resistance while still being environmentally friendly. Furthermore, the move toward sustainability-driven branding is evident in the rise of closed-loop recycling, bio-based inks, and minimalist packaging designs. Collaboration among packaging manufacturers, recyclers, and consumer goods enterprises is becoming more prevalent to guarantee the traceability and end-of-life recovery of materials. The use of digital tracking tools, including QR codes and blockchain for packaging transparency, further illustrates the ongoing consumer demand for sustainable and smart packaging.

MARKET CHALLENGES

Supply Chain Complexity and Transition Barriers May Challenge the Market Growth

Shifting from conventional packaging to zero waste models necessitates significant restructuring of the supply chain. Organizations must procure sustainable raw materials, reconfigure packaging systems, and guarantee compatibility with current logistics operations. These modifications are both time-consuming and require considerable capital, resulting in operational difficulties throughout the transition period. Moreover, despite the increasing consumer awareness regarding sustainability, the uptake of reusable or refillable packaging systems remains restricted due to concerns about convenience, creating challenges for market growth.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material

Remarkable Benefits Offered by Paper & Paperboard Material to Propel Segment Growth

In terms of material, the market is categorized into paper & paperboard, bioplastics & biopolymers, glass, metal, and others.

The paper and paperboard material segment captured the largest share of the market in 2024. In 2026, the segment dominates with a expected share 41.57%. Paper and paperboard materials are crucial in fostering the expansion of the zero waste packaging market due to their biodegradability, recyclability, and renewable sources. These materials originate from sustainably managed forests and agricultural byproducts, rendering them an environmentally friendly substitute for plastic-based packaging. Paper and paperboard provide outstanding printability, lightweight durability, and cost-effectiveness, which makes them particularly appropriate for use in foodservice, personal care, e-commerce, and retail packaging.

The bioplastics and biopolymers segment is expected to grow at a CAGR of 15.70% over the forecast period.

By Type

Noteworthy Characteristics of Recyclable Packaging to Boost the Segment’s Growth

In terms of type, the market is categorized into recyclable, reusable, compostable, and others.

The recyclable segment led the global zero waste packaging market share in 2024. In 2026, the segment dominates with a expected share 46.82%. Recyclable packaging is experiencing significant growth in the zero waste packaging sector, attributed to its environmentally friendly attributes and broad applicability across various industries. This type of packaging allows for the collection, processing, and reuse of materials such as paper, cardboard, glass, metal, and specific plastics, which helps to reduce landfill waste and preserve natural resources. The straightforward process of material recovery and reprocessing positions recyclable packaging as a viable option for manufacturers aiming to comply with sustainability regulations and lower their carbon emissions.

The reusable segment is expected to grow at a CAGR of 16.48% over the forecast period.

By End-use Industry

Surge in Demand for Zero Waste Packaging Solutions from the Food & Beverages Sector to Drive Segmental Growth

Based on end-use industry, the market is segmented into food & beverages, healthcare, e-commerce, personal care & cosmetics, and others.

To know how our report can help streamline your business, Speak to Analyst

In 2025, the global market was dominated by food and beverages in terms of end-use industry. Furthermore, the segment holds a 43.18% expected share in 2026. The growing consumer inclination toward environmentally friendly and non-toxic packaging has prompted food manufacturers, quick-service restaurants, and beverage companies to embrace sustainable options that reduce waste production. The increasing awareness regarding plastic pollution and food contamination associated with traditional packaging has further expedited this transition. Collectively, these factors are greatly advancing the implementation of zero waste packaging within the food and beverage sector, establishing it as a crucial end-use category that is driving overall segmental growth.

In addition, the healthcare segment is projected to grow at a CAGR of 16.48% during the study period.

Zero Waste Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Zero Waste Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed approximately USD 74.32 billion to the global market in 2025, accounting for 31.69% share, and is expected to reach USD 86.45 billion in 2026. The Asia Pacific zero-waste packaging industry is driven by urbanization, governmental prohibitions on plastics, and the emergence of environmentally aware consumer groups in significant economies. Nations such as India and China have implemented stringent regulations on single use plastics. In contrast, Japan and South Korea are at the forefront of developing recycling systems and reusable packaging within the retail and food industries.

In the region, the India and China markets are anticipated to have reached USD 23.29 and USD 28.11 billion respectively in 2026.

North America

In 2025, North America held 24.75% of the global market share, reaching a valuation of USD 58.06 billion, and is projected to grow to USD 67.06 billion in 2026. Other regions such as North America and Europe are anticipated to witness notable growth in the coming years. In North America, the primary market drivers are regulatory pressure and corporate sustainability initiatives. The U.S. and Canada are experiencing an increase in consumer demand for environmentally friendly packaging, especially in the sectors of food, beverages, and e-commerce. Additionally, multinational corporations based in this region are making significant investments in zero waste and circular economy programs to achieve their ESG objectives, propelling market growth. In 2026, the U.S. market is estimated to have reached USD 52.83 billion.

Europe

The market in Europe reached USD 47.12 billion in 2025, representing 20.09% of total market revenue, and is projected to reach USD 54.21 billion in 2026. Europe is witnessing substantial growth as a result of strict environmental regulations, including the EU Packaging and Packaging Waste Regulation (PPWR) and Green Deal initiatives. The area prioritizes circular economy principles, with significant corporations and local governments setting zero waste goals. Increased consumer awareness and readiness to pay more for sustainable products are also driving further adoption.

Backed by these factors, countries including the UK, Germany, and France markets are expected to have recorded valuations of USD 10.46 billion, USD 11.98 billion, and USD 7.29 billion, respectively, in 2026 for the U.K. and Germany, while France maintained a valuation of USD 7.29 billion in 2025.

Latin America and the Middle East & Africa

The Middle East & Africa region captured 8.92% of the global market in 2025, generating USD 20.92 billion in revenue, and is projected to reach USD 23.77 billion in 2026. In 2025, Latin America generated USD 34.13 billion, contributing 14.55% to global market revenue, and is projected to grow to USD 39.01 billion in 2026. Over the analysis period, Latin America and the Middle East & Africa regions would record moderate growth. The Latin America market, in 2025, is set to record USD 34.13 billion as its valuation. The zero waste movement in Latin America is gaining traction due to grassroots environmental activism and governmental sustainability objectives. Nations such as Brazil and Chile have enacted laws prohibiting plastic bags and encouraging the use of compostable alternatives.

COMPETITIVE LANDSCAPE

Key Industry Players

Wide Range of Product Offerings and Strong Distribution Network of Key Companies Supported their Leading Positions

The global zero waste packaging industry depicts a semi-concentrated structure with various small- to mid-size players actively operating across the globe. These players are actively involved in strategic collaborations, product innovation, and geographic expansion.

DS Smith, Smurfit Kappa, and Huhtamaki Oyj are some of the dominating players in the market. A comprehensive range of unit-dose packaging products, global presence through a strong distribution network, and collaborations with research and academic institutes are a few characteristics of these players that support their dominance.

Apart from this, other prominent players in the market include Tipa Ltd., Notpla, Ecovative LLC, and others. These participants are undertaking numerous strategic initiatives, such as R&D investments and collaborations with pharma companies to strengthen their market presence.

LIST OF KEY ZERO WASTE PACKAGING COMPANIES PROFILED

- DS Smith (U.K.)

- Smurfit Kappa (Ireland)

- Huhtamaki Oyj (Finland)

- Tipa Ltd. (Israel)

- Notpla (U.K.)

- Ecovative LLC (U.S.)

- Ranpak Corporation (U.S.)

- TerraCycle, Inc. (U.S.)

- Apeel Sciences (U.S.)

- Green Dot Bioplastics (U.S.)

- Avani Eco (Indonesia)

- Loliware Inc. (U.S.)

- Sulapac Oy (Finland)

- Evoware (Indonesia)

- Vegware (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Finetech introduced a new line of eco-friendly packaging that is compatible with both compostable and recyclable materials. This initiative is designed to assist pharmaceutical manufacturers in moving toward sustainable packaging solutions, while ensuring that product integrity and regulatory compliance are not compromised. These advancements demonstrate the company's continuous commitment to enhancing production processes and fostering a more sustainable future.

- July 2025: Mars, Incorporated advanced its efforts in recyclable pet food packaging with the introduction of a new mono-material pouch for its WHISKAS brand in the U.K. and Germany. The newly designed WHISKAS pouches are intended to be recyclable and are compatible with existing or developing recycling systems. This innovative packaging departs from conventional multi-material pouches, which pose challenges for consumers attempting to recycle them due to the inseparable nature of the plastic and aluminum components.

- June 2025: Shellworks introduced completely home-compostable pipette dropper packaging. This eco-friendly, zero-plastic option has already gained the approval of multiple brands. Constructed from a flexible grade of the company’s plastic-free substance, Vivomer, this biodegradable alternative is said to replicate the characteristics of the various materials typically found in a dropper pipette: glass, ceramic, plastic, and rubber.

- November 2023: Cadbury, the renowned confectionery brand from the U.K., pioneered sustainable packaging by introducing 300,000 paper-based 'Heroes' tubs. This initiative represents a first-of-its-kind trial in the U.K. It is part of parent company Mondelēz International's larger effort to minimize the use of virgin plastic and create scalable, recyclable packaging solutions. The new tubs have been created in collaboration with DS Smith, a leader in sustainable packaging, and are currently being launched in select Tesco stores throughout the U.K.

- December 2020: Global supplier of flexible packaging and lidding films, KM Packaging, introduced a new line of compostable products. The C-Range consists of bio-plastic packaging materials such as shrink wrap, stretch wrap, adhesive tape, nets, and bags. This addition strengthens KM’s collection of sustainable flexible packaging solutions and provides customers with a broader selection. The bio-plastic items have been created in collaboration with Treetop Biopak, a company that specializes in delivering innovative compostable packaging solutions.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 15.78% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material, Type, End-use Industry, and Region |

|

By Material |

· Paper & Paperboard · Bioplastics & Biopolymers · Glass · Metal · Others |

|

By Type |

· Recyclable · Reusable · Compostable · Others |

|

By End-use Industry |

· Food & Beverages · Healthcare · E-commerce · Personal Care & Cosmetics · Others |

|

By Geography |

· North America (By Material, Type, End-use Industry, and Country) o U.S. o Canada · Europe (By Material, Type, End-use Industry, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Russia o Poland o Romania o Rest of Europe · Asia Pacific (By Material, Type, End-use Industry, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Material, Type, End-use Industry, and Country/Sub-region) o Brazil o Mexico o Argentina o Rest of Latin America · Middle East & Africa (By Material, Type, End-use Industry, and Country/Sub-region) o Saudi Arabia o UAE o Oman o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 234.55 billion in 2025 and is projected to reach USD 873.27 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 74.32 billion.

The market is expected to exhibit a CAGR of 15.78% during the forecast period of 2026-2034.

In 2025, the paper and paperboard segment led the market by material.

The key factors driving the market growth are the increasing environmental concerns and sustainability awareness.

DS Smith, Smurfit Kappa, Huhtamaki Oyj, Tipa Ltd., Notpla, and Ecovative LLC are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

Augmenting demand from the food and beverages sector is one of the factors that is expected to favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us