Chlorinated Polyethylene Market Size, Share & Industry Analysis, By Application (PVC Impact Modifier, Rubber & Elastomer, Wire & Cable Compounds, and Others) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

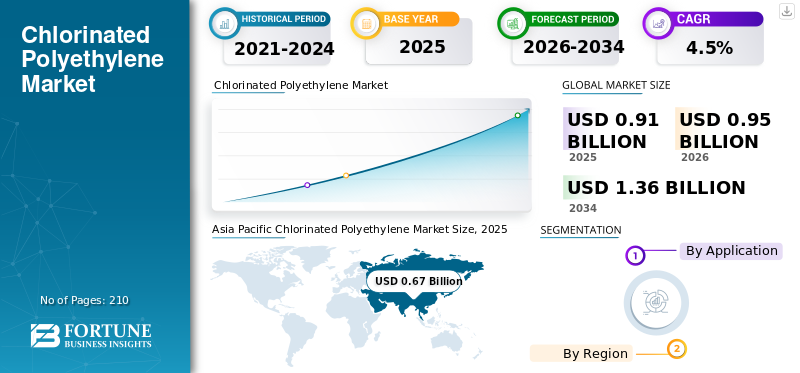

The global chlorinated polyethylene market size was USD 0.91 billion in 2025. The market is projected to grow from USD 0.95 billion in 2026 to USD 1.36 billion by 2034 at a CAGR of 4.5% during the forecast period. Asia Pacific dominated the global market with a market share of 73.62% in 2025.

Chlorinated Polyethylene (CPE) is a flexible, high-performance thermoplastic elastomer produced by chlorinating High-Density Polyethylene (HDPE). It offers a unique balance of impact resistance, weatherability, flame retardancy, and chemical stability. CPE is widely used as an impact modifier in PVC products, a base polymer in rubber compounds, and a performance enhancer in wire and cable jacketing. A major demand driver for CPE is the global growth in infrastructure and construction, particularly in emerging markets, where durable, weather-resistant PVC pipes, profiles, and siding require high-impact modifiers such as CPE to meet performance, longevity, and safety standards across a range of climates. Weifang Yaxing Chemical Co., Ltd., Shandong Gaoxin Chemical Co., Ltd., Sundow Polymers Co., Ltd., Shandong Xuye New Materials Co., Ltd., and Resonac Holdings Corporation are the key players operating in the market.

Download Free sample to learn more about this report.

Chlorinated Polyethylene Market KEY TAKEAWAYS

- 2025 Market Size: USD 0.91 billion

- 2026 Market Size: USD 0.95 billion

- 2034 Forecast Market Size: USD 1.36 billion

- CAGR: 4.5% from 2026–2034

- Asia Pacific dominated the chlorinated polyethylene market with a 73.62% share in 2025.

- The PVC Impact Modifier segment is projected to hold the largest market share during the forecast period.

- The Wire & Cable application is expected to witness strong growth, supported by expanding electrification.

Asia Pacific

The market dominated globally, driven by large-scale infrastructure projects, rapid urbanization.

North America

The market is driven by growing demand for rubber and elastomer applications, including TPO roofing.

Europe

The market is supported by rising demand for specialty elastomers in industrial rubber goods.

U.S.

The market was valued at USD 0.07 billion in 2025, driven by increasing demand for rubber.

Japan

The market was valued at USD 0.04 billion in 2025, supported by steady demand for PVC impact modifiers.

Read More

CHLORINATED POLYETHYLENE MARKET TRENDS

Global Shift Toward Cost-Effective Durability Spurs Product Demand in PVC Manufacturing

Global demand for durable and cost-efficient construction materials is driving a steady shift toward chlorinated polyethylene as a preferred impact modifier in rigid PVC applications. This trend is particularly pronounced in emerging economies such as India, Vietnam, and the Middle East, where infrastructure growth favors high-impact, weather-resistant compounds. CPE is increasingly displacing costlier modifiers such as MBS and acrylics in outdoor-grade PVC pipes, siding, and window profiles. Simultaneously, adoption is rising in flexible membranes, seals, and roofing. The trend reflects a broader materials shift as value-focused buyers are trading premium formulation flexibility for the performance-cost balance that the product offers, thereby driving chlorinated polyethylene market growth in tandem.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Infrastructure-Led Construction Expansion to Drive Market Growth

A major demand driver for the product is the sustained global investment in infrastructure and construction, particularly in the Asia Pacific, Latin America, and Africa. As cities expand and aging pipelines, water systems, and low-cost housing projects grow, rigid PVC demand surges, driving higher CPE consumption as an impact modifier. National initiatives such as India’s Smart Cities Mission, ASEAN connectivity programs, and Middle East mega-projects ensure that demand for impact-resistant PVC compounds remains elevated. As most of these products rely on chlorinated polymers for long-term outdoor performance, the product remains strategically positioned within this growth cycle.

MARKET RESTRAINTS

Environmental Scrutiny on Halogenated Polymers is Likely to Restrain Market Growth

Product’s chlorinated backbone has drawn increasing regulatory and environmental scrutiny, especially in Europe and certain parts of North America. Policymakers, NGOs, and green building standards are pushing for non-halogenated flame retardants and PVC alternatives, citing lifecycle emissions and end-of-life challenges. This shift poses a threat to long-term demand, particularly in wire & cable and interior construction, where low-smoke, halogen-free materials are preferred. As ESG metrics tighten in procurement decisions, some OEMs are proactively phasing out chlorinated materials. While the near-term impact is moderate due to a lack of cost-effective alternatives, regulatory momentum could limit the product’s market growth in future high-compliance applications.

MARKET OPPORTUNITIES

Electrification and EV Infrastructure Open High-Value Growth Opportunities

The global electrification wave, driven by electric vehicles, renewable power sources, and smart grid upgrades, is creating new demand for flame-retardant, weather-resistant cable jackets and battery compartment seals. CPE, with its halogenated flame resistance, low-temperature flexibility, and chemical durability, is emerging as a competitive material for EV cable insulation, solar power cables, and energy storage system gaskets. These applications require polymers that balance mechanical toughness with fire safety, where CPE offers a price-performance advantage over neoprene and some EPDMs. Manufacturers with qualified CPE grades for EVs and renewables stand to capture premium-margin growth in this expanding performance-critical segment.

MARKET CHALLENGES

China-Led Overcapacity and Pricing Pressure Challenge Global Profit Margins

The rapid buildout of CPE production capacity in China, where majority of global output is now concentrated, has introduced persistent pricing pressure and volatility across the supply chain. Chinese producers, many state-backed or vertically integrated, are aggressively pricing exports to gain global market share, often below marginal cost in high-volume grades. This has commoditized large segments of the PVC impact modifier market and compressed margins for non-Chinese players. The lack of meaningful antidumping protections in many markets intensify the issue.

SEGMENTATION ANALYSIS

By Application

To know how our report can help streamline your business, Speak to Analyst

Urban Infrastructure Expansion Powers Demand in PVC Impact Modifier Segment

Based on the application, the market is segmented into PVC impact modifier, rubber & elastomer, wire & cable compounds and others.

The PVC impact modifier segment is anticipated to hold the dominant chlorinated polyethylene market share during the forecast period. A major factor driving product demand in PVC impact modification is the accelerating investment in urban infrastructure across emerging markets. Rapid urbanization in India, Southeast Asia, and Africa fuels demand for PVC pipes, fittings, siding, and window profiles, where the product enhances impact strength, weatherability, and flame retardancy. Compared to alternatives such as MBS or acrylic modifiers, CPE offers a superior cost-performance balance in outdoor-grade formulations, making it the preferred choice in infrastructure-grade rigid PVC systems, driving market growth in tandem.

In wire and cable applications, the primary demand driver is global electrification, particularly from renewable energy, electric vehicles, and smart grid upgrades. These sectors require cable jackets that are both flame retardant and weather resistant. Product’s halogenated structure delivers inherent fire performance, low-temperature flexibility, and oil resistance, making it a cost-effective alternative to high-end rubber or silicone-based materials. As infrastructure projects mandate durable and safe electrical cabling, the product's usage in insulation and sheathing compounds continues to rise.

The wire and cable segment is anticipated to rise with a CAGR of 5.6% over the forecast period.

CHLORINATED POLYETHYLENE MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Chlorinated Polyethylene Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In the Asia Pacific, CPE demand is overwhelmingly driven by its role as a PVC impact modifier, especially in rigid pipes, window profiles, and siding used in large-scale infrastructure and urban housing projects across China, India, and Southeast Asia. Government investment in water systems, affordable housing, and smart cities sustains strong PVC demand. This growth is driven by the wire and cable segment, which is expanding due to electrification, the rise of electric vehicles, and the development of renewable power grids, particularly in China and India. Rubber and elastomer uses are also gaining momentum, as industrial and automotive sectors across the Asia Pacific seek flexible, chemical-resistant alternatives to neoprene and chloroprene rubber, driving market growth in tandem.

Japan Market

Japan’s market recorded the valuation of USD 0.04 billion in 2025, equivalent to around 4.4% of global chlorinated polyethylene sales.

China Market

China’s market is projected to be one of the largest worldwide. It recorded the valuation of USD 0.51 billion in 2025, representing roughly 56.0% of global chlorinated polyethylene sales.

India Market

India’s market reached the valuation of USD 0.08 billion in 2025, equivalent to around 8.8% of global chlorinated polyethylene sales.

North America

In North America, the major driver of demand is its use in rubber and elastomer applications, including TPO roofing, automotive hoses, and flexible membranes, applications where the product offers a cost-effective alternative to neoprene and EPDM. CPE’s chemical resistance and long-term weatherability make it ideal for commercial roofing and under-the-hood components. A supporting growth segment is wire and cable insulation, particularly in EVs, renewables, and industrial power systems, where flame resistance is essential.

U.S. Market

The U.S. market was analytically approximated at around USD 0.07 billion in 2025, accounting for roughly 7.7% of global chlorinated polyethylene sales.

Europe

In Europe, the primary demand driver is the role of specialty elastomers in applications, particularly in industrial rubber goods such as hoses, roofing membranes, and chemical-resistant seals. Demand is supported by strict environmental conditions where CPE’s aging and weather resistance outperform alternatives. While CPE’s use in PVC impact modification is limited due to environmental preferences for non-halogenated additives, its role in low-smoke wire and cable jackets is growing, driving market growth in tandem.

U.K. Market

U.K.’s market recorded the valuation of USD 0.01 billion in 2025, equivalent to around 1.1% of global chlorinated polyethylene sales.

Germany Market

Germany’s market reached the valuation of USD 0.03 billion in 2025, equivalent to around 3.3% of global chlorinated polyethylene sales.

Latin America

Latin America’s product demand is led by PVC impact modification, as governments invest in cost-effective piping, housing, and sanitation infrastructure across Brazil, Mexico, and the Andean region. CPE’s price-performance advantage over acrylics supports its use in rigid vinyl applications, particularly those suited for outdoor environments. A key supporting segment is rubber & elastomer usage, especially in automotive hoses, seals, and roofing materials, where aftermarket and industrial growth fuel consumption. While smaller today, wire & cable compound demand is rising, driven by electrification and renewable energy programs in Brazil, Chile, and Colombia.

Brazil Market

Brazil’s market reached around USD 0.01 billion as its valuation in 2025, equivalent to around 1.1% of global chlorinated polyethylene sales.

Middle East & Africa

In the Middle East & Africa, demand for the product is driven by PVC infrastructure applications, particularly in potable water, wastewater, and electrical conduit systems. These regions are investing in long-life construction materials that perform well in high heat and UV environments, conditions where CPE-modified PVC excels. Increasing investment in power grids and urban electrification is also creating demand for CPE-based wire and cable compounds, favored for their flame resistance and weatherability. Over time, growth in construction-related adhesives and waterproof membranes may lift demand in niche “other” applications as formulation markets develop.

Saudi Arabia Market

Saudi Arabia’s market recorded the valuation of USD 0.01 billion in 2025, equivalent to around 1.1% of global chlorinated polyethylene sales.

COMPETITIVE LANDSCAPE

Key Industry Players

China-Led Giants Dominate Global Market as Overcapacity Pressures Margins Worldwide

The global market is highly consolidated, with China dominating global production through cost-competitive, large-scale manufacturers. The market is shaped by intense price competition, limited product differentiation in high-volume grades, and growing specialization in elastomer and cable-grade CPE. The top producers globally are Weifang Yaxing Chemical Co., Ltd., Shandong Gaoxin Chemical Co., Ltd., Sundow Polymers Co., Ltd., Shandong Xuye New Materials Co., Ltd., and Resonac Holdings Corporation. Chinese players compete aggressively on volume and pricing, while non-Chinese firms focus on specialty grades. Overcapacity in Asia continues to pressure global margins, especially in impact modifier applications.

LIST OF KEY CHLORINATED POLYETHYLENE COMPANIES PROFILED

- Weifang Yaxing Chemical Co., Ltd. (China)

- Shandong Gaoxin Chemical Co., Ltd. (China)

- Sundow Polymers Co., Ltd. (China)

- Shandong Xuye New Materials Co., Ltd. (China)

- Resonac Holdings Corporation (Japan)

- Aurora Material Solutions (U.S.)

- Hangzhou Keli Chemical Co., Ltd. (China)

- Shandong Hongfu Chemical Co. LTD (China)

- Shandong Novista Chemicals Co., Ltd. (China)

- Suntek (India)

- Other Key Players

KEY INDUSTRY DEVELOPMENTS

- August 2024 – Aurora Material Solutions completed a major expansion of its Streetsboro, Ohio, facility, adding over 140 million pounds of new capacity to meet rising demand for rigid PVC, PVC alloys, and chlorinated PVC. The upgraded site features advanced compounding systems and is expected to boost production and job creation.

- January 2023 – Showa Denko K.K. and Showa Denko Materials Co., Ltd. officially merged to form Resonac Group, marking a strategic rebranding and structural integration. Touted as their “second inauguration,” the launch signals a bold transformation aimed at positioning Resonac as a global leader in advanced functional materials.

REPORT COVERAGE

The global market report provides a detailed analysis of the market. It focuses on key aspects such as profiles of leading companies, product types, and leading applications of the product. Besides this, it offers insights into the analysis of key market trends and highlights key industry developments. In addition to the aforementioned factors, it encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Volume (Kiloton); Value (USD Billion) |

|

Growth Rate |

CAGR of 4.5% during 2026-2034 |

|

Segmentation |

By Application, and By Geography |

|

By Application |

· PVC Impact Modifier · Rubber & Elastomer · Wire & Cable Compounds · Others |

|

By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 0.91 billion in 2025 and is projected to record a valuation of USD 1.36 billion by 2034.

In 2025, Asia Pacific market value stood at USD 0.67 billion.

Registering a CAGR of 4.5%, the market will exhibit steady growth during the forecast period of 2026-2034.

The PVC impact modifier application is expected to lead the market.

Infrastructure-led construction expansion is the key factor driving the market.

Weifang Yaxing Chemical Co., Ltd., Shandong Gaoxin Chemical Co., Ltd., Sundow Polymers Co., Ltd., Shandong Xuye New Materials Co., Ltd. and Resonac Holdings Corporation are the major players operating in the market.

Asia Pacific dominated the market in terms of share in 2025.

Global shift toward cost-effective durability spurs product adoption in PVC manufacturing.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us