"Smart Strategies, Giving Speed to your Growth Trajectory"

3D Scanning Market Size, Share & Industry Analysis, By Component (Hardware, Software), By Range (Short Range, Medium Range, Long Range), By Device (Portable, Stationary), By Application (Reverse Engineering, Quality Control and Inspection, Rapid Prototyping, Full Body Scanning), By End-User (Aerospace and Defense, Healthcare, Automotive, Architecture and Construction, Industrial Manufacturing), and Regional Forecast Report 2026-2034

Last Updated: July 20, 2026

| Format: PDF

| Report ID:

FBI102627

Thank you for your interest in the

"United States Medical Devices Market!"

To receive a sample report, please provide the following details:

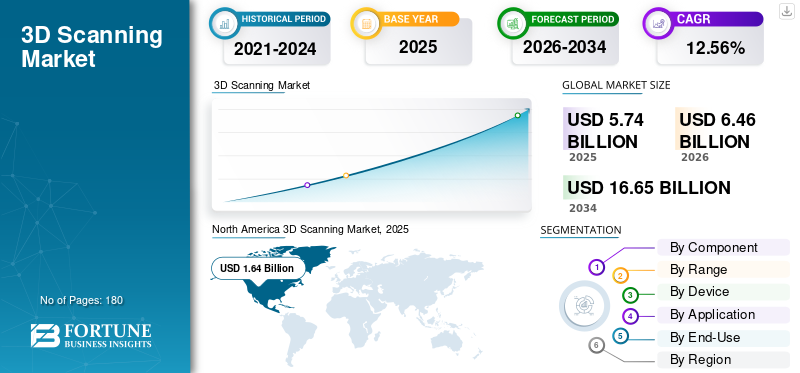

The global 3D scanning market size was valued at USD 5.74 billion in 2025. The market is projected to grow from USD 6.46 billion in 2026 to USD 16.65 billion by 2034, exhibiting a CAGR of 12.56% during the forecast period. North America dominated the global market with a share of 32.67% in 2025.

The 3D scanning market driven by a widening range of industrial and commercial applications. Adoption has moved beyond early experimentation into operational integration across manufacturing, engineering, healthcare, and digital content creation. The market’s current scale reflects sustained demand from both established industrial users and emerging digital-first sectors that rely on high-precision spatial data.

Historically, market expansion was driven by industrial metrology, automotive inspection, and reverse engineering. Over time, adoption broadened to include architecture, medical imaging, heritage preservation, and consumer-facing applications. This transition marked a shift from niche technical use toward enterprise-grade deployment, supported by falling hardware costs and rising software sophistication. The industry has now entered a more structured growth phase characterized by diversified demand rather than dependence on a few core verticals.

Near-term growth continues to be supported by accelerating digital transformation initiatives and increased automation across manufacturing and design workflows. Medium-term expansion is expected to be shaped by deeper integration of scanning technologies into digital twins, simulation platforms, and quality management systems. Over the longer horizon, the 3D scanning market is positioned for sustained expansion as spatial data becomes foundational to industrial intelligence, advanced manufacturing, and immersive digital environments.

Momentum indicators include rising enterprise adoption, increased integration with downstream analytics platforms, and broader acceptance across regulated industries. These dynamics signal a market transitioning from adoption-led expansion toward long-term structural embeddedness within global production ecosystems.

3D scanning has emerged as a significant technology in product lifecycle management (PLM), providing greater precision, speed, and efficiency in design, manufacturing, and quality control processes. In areas such as gaming and entertainment, technology has transformed the way virtual worlds and lifelike characters are modeled. It has also altered documentation and measurement processes in industries such as engineering, architecture, and healthcare.

The industry has continued to evolve with the incorporation of artificial intelligence (AI), edge computing, and 5G connection, allowing for real-time data transfer and cloud-based collaboration in scanning operations. AI-assisted scanning systems now automate mesh correction, object detection, and feature extraction, resulting in significantly shorter design cycle times. Furthermore, enterprises are implementing sustainable manufacturing tactics, such as 3D scanning, which reduces material waste in additive manufacturing processes via closed-loop feedback. Compliance with international standards such as ISO 10360 (geometrical product requirements) and NIST traceability rules is becoming an important differentiation for providers in the precision engineering market.

Modern scanning systems are becoming more integrated into professional processes, allowing measurement specialists to boost accuracy and throughput. For example, in April 2019, ScanTech unveiled the KSCAN 3D scanner, a metrology-grade device with an integrated photogrammetry system that improves volumetric accuracy and scanning range. As the demand for precision-driven digital modeling develops, 3D scanning transitions from a specialist technology to a critical component of digital transformation initiatives across many industries.

North America dominated the 3D scanning market with a 32.67% share in 2025.

The hardware segment held the largest market share in 2025.

The short-range scanner segment held the largest market share in 2025.

Key Regional Highlights

North America

North America leads the market due to strong demand from aerospace, automotive, healthcare, and manufacturing sectors.

Europe

Europe is driven by growing adoption of advanced metrology and industrial automation technologies.

Asia Pacific

Asia Pacific is the fastest-growing region due to rapid industrialization and increasing smart manufacturing investments.

U.S.

High adoption of digital engineering and precision measurement solutions supports market growth.

Japan

Rising investments in automation and advanced manufacturing technologies are driving demand for 3D scanning solutions.

Read More

What major trends are shaping the future of the 3D scanning market?

Expeditious Utilization of 3D Scanners to Create Digital Models for Virtual Cinematography and Video Games

The usage of 3D scanning in virtual cinematography and video game creation has become one of the market's fastest growing trends. In the entertainment sector, studios are increasingly using scanners to produce digital counterparts of actual performers and things, which reduces modeling time and improves realism. Combined with computer-aided design (CAD) software, 3D scanning enables costume and prop designers to finish precise models in hours rather than days.

The 3D scanning market is being reshaped by a convergence of digital transformation, automation, and data-centric workflows. One of the most influential trends is the shift from standalone scanning tools toward integrated digital ecosystems. Organizations increasingly view scanning technologies as foundational inputs for broader digital twins, simulation environments, and lifecycle management platforms. This shift elevates the strategic importance of scanning data across design, production, and maintenance functions.

Automation is another defining force. Advances in robotics and autonomous scanning systems are reducing reliance on manual operation while improving consistency and repeatability. These capabilities are particularly valuable in large-scale industrial environments where speed, safety, and accuracy are critical. Automation also supports continuous data capture, enabling more dynamic monitoring of physical assets over time.

Artificial intelligence and advanced analytics are reshaping how scan data is interpreted and applied. Machine learning algorithms enhance feature recognition, defect detection, and surface analysis, transforming raw point clouds into actionable insights. This evolution shortens analysis cycles and supports predictive decision-making across engineering and quality control workflows.

Sustainability considerations are increasingly influencing technology adoption. Organizations are using 3D scanning to reduce material waste, optimize resource use, and support circular manufacturing practices. At the same time, customer expectations are shifting toward interoperable, future-ready platforms that can scale alongside evolving digital infrastructures. These trends collectively redefine how value is created within the 3D scanning market.

What are the key drivers accelerating growth in the 3D scanning market?

Prerequisite of 3D Scanning in Product Lifecycle Management to Uplift the Market Growth

The integration of 3D scanning into product lifecycle management (PLM) has emerged as a key industry growth driver. Companies are progressively using scanning technologies at all stages of the lifecycle, from concept design and prototype to manufacturing, quality control, and maintenance. Scanning speeds up requirement analysis and model validation in the concept phase, while it improves CAD modeling, quick prototyping, and simulation accuracy in the design stage.

In manufacturing, 3D scanning aids in tool design, assembly validation, and production quality assurance by assuring dimensional consistency and lowering rework costs. During the servicing phase, it allows for the documenting, restoration, and replacement of complicated components, extending asset life cycle. FARO Technologies' 8-Axis Design ScanArm 2.5C, for example, is commonly used for reverse engineering and CAD-based modeling, which helps to streamline design-to-production processes.

Growth in the 3D scanning market is being driven by a combination of structural demand shifts, technological advancement, and evolving enterprise priorities. At the demand level, organizations across manufacturing, construction, healthcare, and design are under pressure to improve accuracy, reduce rework, and shorten development cycles. Three-dimensional data capture enables faster iteration, tighter quality control, and improved asset documentation, making it increasingly central to modern workflows.

Customer behavior has also shifted toward data-rich, interoperable systems. End users now expect scanning solutions to integrate seamlessly with computer-aided design (CAD), building information modeling (BIM), and digital twin platforms. This expectation has expanded demand beyond standalone hardware toward complete scanning ecosystems that include software, analytics, and lifecycle support.

On the supply side, technological maturation has lowered adoption barriers. Advances in sensor resolution, photogrammetry, structured light, and laser-based scanning have improved accuracy while reducing system complexity. Miniaturization and mobility have expanded use cases beyond controlled environments into field operations. Capital availability remains strong, supported by continued investment in industrial automation and smart infrastructure.

External forces also play a significant role. Regulatory emphasis on quality assurance, traceability, and compliance in sectors such as aerospace, healthcare, and construction has increased reliance on high-fidelity digital measurement. At the same time, macroeconomic pressure to improve productivity and reduce material waste reinforces the value proposition of precise, data-driven inspection tools. Together, these factors continue to accelerate 3D scanning market growth across multiple industries.

What challenges and constraints impact market expansion?

High Initial Cost Associated with 3D Scanning Solutions to Hinder the Adoption

Despite its benefits, the 3D scanning industry faces various adoption barriers, the most significant of which are high initial prices and integration complexity. The initial investment in hardware, software, and system training can be expensive, especially for small and medium-sized businesses (SMEs). Many organizations also spend money on employee training to guarantee that scanning technology is used effectively.

Despite strong structural momentum, the 3D scanning market faces several constraints that shape adoption patterns and investment decisions. One of the most persistent challenges is the high upfront cost associated with advanced scanning hardware and supporting software. For small and mid-sized enterprises, capital expenditure requirements can delay adoption, particularly when return on investment is not immediately quantifiable.

Operational complexity also presents a barrier. Effective deployment often requires specialized technical expertise, from calibration and data processing to system integration. Skills shortages in metrology, data analysis, and 3D modeling limit scalability, particularly in regions with less mature industrial ecosystems. Training requirements further extend implementation timelines and increase total cost of ownership.

Regulatory and compliance factors introduce additional friction. In sectors such as aerospace, healthcare, and construction, certification standards and data governance requirements can slow adoption and increase validation costs. Interoperability challenges persist as well, particularly when integrating scanning outputs with legacy software environments or proprietary enterprise systems.

Market dynamics also introduce risk. Competitive pressure has intensified as new entrants target niche applications with lower-cost solutions. This has contributed to price sensitivity and margin compression in certain segments. At the same time, rapid technological evolution raises the risk of asset obsolescence, compelling buyers to balance innovation with long-term investment stability.

SEGMENTATION ANALYSIS

By Component Analysis

Laser Scanner Segment to Hold the Largest Market Share Owing to its Ability to Capture Millions of Data Points in Seconds

The 3D scanning industry is divided into hardware and software segments, with hardware dominating due to ongoing innovation in laser, structured light, and optical scanners. 3D laser scanners have the largest market share due to their capacity to gather millions of data points in seconds.

Hardware includes handheld, tripod-mounted, and fixed-position scanning systems using laser, structured light, or photogrammetry technologies. While hardware remains foundational, its relative share of total value creation is gradually declining. Hardware has become more standardized, with competitive pressure driving incremental innovation rather than step-change differentiation.

Software represents the fastest-growing and highest-margin component. Advanced processing engines, visualization platforms, and data management tools now account for a growing portion of overall value. Software enables scan alignment, defect detection, surface reconstruction, and integration with downstream applications such as computer-aided design and manufacturing. Vendors that control proprietary software ecosystems retain stronger pricing power and longer customer relationships.

Laser scanners are suitable for scanning delicate settings and things that require noncontact precision. Meanwhile, structured light scanners are quickly gaining popularity as manufacturers incorporate this technology into handheld scanners to improve accuracy and processing speed. In July 2019, FARO Technologies unveiled the Cobalt Design structured light scanner, which can capture precise surface details, hues, and complicated shapes in seconds.

Hybrid systems that combine laser and structured light technologies have been in widespread use since 2024. These systems allow for dynamic switching based on surface qualities and illumination conditions, broadening their applications to industrial inspection, medical imaging, and cultural preservation. AI-powered noise reduction and real-time visualization are also improving data interpretation speed and accuracy.

By Range Analysis

To know how our report can help streamline your business, Speak to Analyst

Short Range Scanners Likely to Drive Market Growth due to Less Sensitivity to Ambient and Changing Light Condition

The 3D scanning market is segmented into short-range, medium-range, and long-range systems based on scanning distance.

Short-range scanners hold the dominant position due to their lower sensitivity to ambient lighting and ability to deliver high-resolution data in diverse conditions. These scanners are particularly suited for detailed inspections of small or reflective surfaces and are generally cost-effective and safe for human interaction.

Short-range 3D scanning dominates applications requiring high precision and fine detail, including quality inspection, reverse engineering, and medical modeling. These systems are typically used in controlled environments and generate high-resolution datasets.

Medium-range scanners are increasingly adopted for geological mapping, architectural documentation, and infrastructure monitoring, offering a balance between portability and measurement distance. They are ideal for capturing mid-sized environments like bridges, industrial facilities, and archaeological sites with high accuracy. Medium-range scanning supports broader industrial applications, balancing accuracy with coverage for factory floors, construction sites, and large components.

Long-range scanners, on the other hand, cater to applications requiring large-scale mapping such as buildings, ships, aircraft, and defense vehicles. As range and precision technologies improve, manufacturers are incorporating hybrid systems capable of switching between ranges dynamically. This trend is enabling a wider range of industrial, construction, and survey applications, reflecting a broader shift toward flexible and multi-environment 3D scanning solutions.

Long-range scanning serves infrastructure, surveying, and large-scale asset management. Growth in this segment is driven by infrastructure development, urban planning, and digital twin initiatives. Although unit volumes are lower, average deal values are higher due to system complexity and service requirements.

Manufacturers are also working on adaptive range algorithms that automatically change scan resolution to object geometry, maximizing accuracy while decreasing data volume. This innovation responds to the increased demand for energy-efficient, intelligent scanning systems in the manufacturing and construction sectors.

By Device Analysis

Handheld 3D Scanner to be the Fastest Growing Segment as it helps in Accessing Areas that are Difficult to Reach

Based on device type, the 3D scanning market is divided into portable (handheld) and stationary systems.

Stationary scanners are typically mounted on fixed structures such as arms or tripods, offering high stability and accuracy for scanning large-scale objects like vehicles, aircraft, and infrastructure components. These systems require minimal operator intervention and are optimized for controlled environments.

The latest handheld variants now include LiDAR and photogrammetry fusion, allowing for precise outdoor and mobile scanning applications. Integration with 5G-enabled edge devices allows for seamless data flow from field to cloud, resulting in speedier design collaboration and real-time inspection analysis.

Portable scanners account for a growing share of deployments. Their flexibility, declining weight, and improved accuracy make them suitable for decentralized operations and field-based workflows. Stationary systems remain critical for high-precision manufacturing and quality control environments, where repeatability and stability are paramount.

The shift toward portability reflects broader changes in how organizations deploy technical capabilities. Decentralized production and inspection models favor equipment that can move with workflows rather than remain fixed to specific facilities.

In contrast, handheld 3D scanners are gaining rapid traction due to their portability, flexibility, and ability to access complex or confined spaces. They are increasingly used in industries such as automotive design, cultural heritage documentation, and field-based maintenance. Handheld devices can capture both small and large objects with ease, providing fast and accurate 3D models in real time.

The growing preference for handheld scanners is also driven by ergonomic designs, wireless operation, and integration with mobile computing platforms. This flexibility allows engineers and designers to perform on-site measurements without compromising precision. Consequently, the handheld segment is projected to record the fastest growth during the forecast period, reshaping how scanning technology is deployed in industrial and design workflows.

By Application Analysis

Reverse Engineering to Gain Traction During forecast Period owing to Need of Accurate and Precise Result

3D scanning serves diverse applications including reverse engineering, quality control, rapid prototyping, body scanning, and gaming.

General industrial inspection and quality control represent the largest application area. Manufacturers rely on 3D scanning to detect deviations, reduce scrap, and improve process control. Reverse engineering follows closely, particularly in legacy system replication and aftermarket component design.

In product development, rapid prototyping and design validation continue to drive adoption. 3D scanning shortens development cycles and improves design accuracy, supporting faster innovation cycles. In healthcare, applications include orthotics, prosthetics, and anatomical modeling, where customization and precision are critical.

Emerging applications such as full-body scanning, cultural heritage preservation, and virtual environment creation remain smaller in scale but exhibit strong growth potential as technologies mature and costs decline.

By End-Use Analysis

Industrial Manufacturing Segment to Exhibit Highest Growth owing to its Use in Various Stages of Product Design Development and Implementation

End-use industries for 3D scanning include aerospace and defense, healthcare, automotive, architecture and construction, industrial manufacturing, and entertainment and media. Among these, industrial manufacturing leads the market, utilizing scanning at nearly every stage of product development from initial design and prototyping to assembly and quality inspection.

Large enterprises account for a significant portion of total market value due to their capital intensity and integration requirements. Aerospace, automotive, and heavy manufacturing firms leverage scanning technologies across multiple stages of the value chain. These users prioritize accuracy, reliability, and system interoperability.

Small and medium-sized enterprises represent a growing opportunity. As systems become more affordable and easier to deploy, adoption among SMEs is accelerating. These users value modular solutions, flexible pricing, and rapid return on investment.

Public sector and research institutions also contribute to demand, particularly in infrastructure planning, cultural preservation, and academic research. Their purchasing behavior is often influenced by funding cycles and long-term project horizons.

Value creation is increasingly concentrated in software, services, and data-driven capabilities rather than in hardware alone. Recurring revenue models, including licensing, subscriptions, and support contracts, provide more predictable cash flows and higher margins. Companies that successfully bundle hardware with analytics and workflow integration capture a disproportionate share of lifetime customer value.

Profitability also varies by application. High-precision industrial and medical uses command premium pricing due to performance requirements and regulatory constraints. In contrast, commoditized scanning solutions face margin compression as competition intensifies.

REGIONAL ANALYSIS

Geographically, the global 3D scanning market is studied across five major regions, namely North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America. They are further categorized into countries.

North America

Among all regions, North America followed by Europe dominance the global market owing to increasing application of scanning in various industries, including, healthcare, automotive, entertainment, manufacturing among others. Growing focus of companies towards 3D printing, and 3D machine vision are also some of the factors driving the growth of North America market.

North America represents one of the most mature and technologically advanced markets for 3D scanning solutions. Adoption is driven by strong demand from aerospace, automotive, healthcare, and advanced manufacturing sectors. Organizations in this region prioritize precision, compliance, and integration with digital engineering workflows, reinforcing demand for high-performance scanning systems.

The region benefits from a well-developed innovation ecosystem, including strong university-industry collaboration, venture capital activity, and early adoption of emerging technologies. Regulatory clarity and established quality standards support consistent investment cycles. Growth in this market increasingly depends on system upgrades, software-driven enhancements, and expanded use cases rather than first-time adoption.

Europe

Europe presents a diverse market landscape shaped by varying industrial bases and regulatory frameworks. Western Europe demonstrates stable demand anchored in automotive engineering, industrial automation, and heritage preservation. Stringent quality and sustainability standards encourage the adoption of advanced metrology and inspection technologies.

Central and Eastern Europe represent a different growth profile, characterized by expanding manufacturing capacity and increasing foreign investment. Adoption in these regions is driven by cost efficiency and integration into global supply chains. However, procurement processes are often influenced by public funding structures and regulatory compliance requirements, which can extend purchasing cycles.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by rapid industrialization, infrastructure expansion, and digital transformation initiatives. Manufacturing hubs in East Asia are investing heavily in automation and smart factory capabilities, making 3D scanning a critical enabling technology. The region’s scale and diversity create strong demand across automotive, electronics, construction, and consumer goods sectors.

Local manufacturing ecosystems and government-backed innovation programs support the development and adoption of scanning technologies. At the same time, price sensitivity and localization requirements influence purchasing behavior. Vendors that adapt product offerings to regional cost structures and operational needs tend to achieve stronger market penetration.

Latin America

Latin America remains an emerging market for 3D scanning, characterized by uneven adoption and limited penetration outside major industrial centers. Demand is primarily driven by automotive manufacturing, infrastructure development, and select mining applications. Economic volatility and constrained capital expenditure can slow adoption cycles, though targeted investments in modernization continue to create incremental opportunities.

Growth in this region often depends on the availability of local service partners and financing models that lower entry barriers. As industrial digitalization gains traction, demand for scanning technologies is expected to rise gradually.

Middle East and Africa

The Middle East and Africa represent an early-stage but strategically significant market. Adoption is concentrated in infrastructure development, energy, and large-scale construction projects. Governments in several countries are investing heavily in smart city initiatives and digital transformation, creating long-term potential for advanced scanning solutions.

Market growth is constrained by skills shortages and uneven regulatory frameworks, yet large-scale public projects provide opportunities for high-value deployments. Over time, increasing emphasis on asset management and digital documentation is expected to support broader uptake.

Across all regions, the interplay between regulatory maturity, industrial structure, and technological readiness shapes adoption patterns. While regional dynamics differ, the overarching trajectory points toward deeper integration of 3D scanning into industrial and digital ecosystems worldwide.

North America 3D Scanning Market, 2025 (USD Billion)

Who are the key players, and how competitive is the market?

Companies like Artec Europe, CREAFORM, and THOR3D are Adopting Organic and Inorganic Strategies to Strengthen their Market Position

The global 3D scanning market features several prominent players, including Artec Europe, Creaform, and Thor3D, each pursuing strategies to enhance competitiveness and technological capabilities.

Thor3D, active since 2015, specializes in developing wireless handheld scanners known for their lightweight design and high accuracy. The company has expanded its product portfolio through partnerships and collaborations, such as its January 2020 agreement with Quicksurface to bundle advanced 3D modeling software with its Calibry 3D scanner.

The 3D scanning market is characterized by a mix of established technology providers, specialized solution developers, and emerging innovators. Market leadership is concentrated among firms with deep technical expertise, extensive intellectual property portfolios, and strong global distribution networks. These players benefit from long-standing relationships with industrial customers and the ability to deliver integrated hardware–software ecosystems.

Large, diversified technology companies typically compete on system performance, reliability, and end-to-end solution capability. Their strategies emphasize platform expansion, software integration, and long-term service contracts. These incumbents often leverage scale advantages in research, manufacturing, and global support infrastructure to maintain competitive positioning.

Alongside these leaders, a growing cohort of specialized vendors targets specific applications or industries. These challengers differentiate through focused innovation, such as niche scanning modalities, enhanced portability, or application-specific analytics. Their agility allows faster adaptation to emerging customer requirements, though scale limitations can constrain global reach.

Market competition is further shaped by partnerships and acquisitions. Strategic alliances between hardware manufacturers, software developers, and system integrators are increasingly common, enabling broader solution portfolios and accelerated market entry. Acquisition activity often centers on software capabilities, data processing expertise, or regional market access.

How are innovation, technology, and digital transformation shaping the market?

Innovation plays a central role in reshaping the competitive structure of the 3D scanning market. Advances in sensing technologies, data processing, and computational modeling have expanded the functional scope of scanning systems well beyond traditional measurement tasks. Modern platforms increasingly operate as integrated digital infrastructure rather than standalone tools.

Artificial intelligence and machine learning are becoming foundational enablers. These technologies support automated feature recognition, defect detection, and predictive analytics, reducing reliance on manual interpretation. As algorithms mature, they enable faster processing of complex datasets and improve consistency across large-scale operations. This shift enhances productivity while lowering dependency on specialized human expertise.

Cloud-based architectures are also redefining deployment models. Cloud integration allows centralized data management, remote collaboration, and continuous software updates. This approach supports scalable operations and enables organizations to standardize workflows across geographically dispersed sites. It also facilitates data-driven decision-making by linking scan outputs with enterprise systems such as product lifecycle management and enterprise resource planning.

From a cost perspective, digital transformation is improving operational efficiency. Automation reduces labor intensity, while predictive maintenance lowers downtime and extends asset life. These improvements strengthen return on investment and reinforce the long-term economic case for adoption. As digital maturity increases, competitive advantage will increasingly depend on the ability to integrate scanning technologies seamlessly into broader digital ecosystems.

What are the growth opportunities?

The most compelling opportunities within the 3D scanning market lie at the intersection of technological innovation and unmet operational needs. High-growth potential exists in sectors undergoing rapid digital transformation, including advanced manufacturing, infrastructure development, and healthcare diagnostics. These areas demand precise, repeatable, and data-rich measurement capabilities.

Geographically, emerging economies present long-term growth potential as industrial modernization accelerates. Investments in infrastructure, smart manufacturing, and urban development are expanding the addressable market for scanning technologies. Companies that localize offerings and build regional partnerships are better positioned to capture this demand.

From a strategic perspective, software-driven solutions represent a significant value opportunity. Analytics platforms, cloud-based collaboration tools, and subscription-based service models generate recurring revenue and deepen customer engagement. Adjacent opportunities also exist in digital twin development, simulation, and predictive maintenance applications.

KEY INDUSTRY DEVELOPMENTS:

February 2020 – Artec 3D, introduced professional 3D scanners and Geomagic 3D education software suite for schools, universities & research institutes. These 3D scanners along with software serves a wide array of courses, including engineering, manufacturing, art and computer graphics, architecture, history and heritage preservation, medicine, science, among others.

November 2019 – Creaform launched HandySCAN AEROPACK, a 3D scanning solution suite to tackle the specific challenges of aircraft quality control, such as aircraft incidents, assessing damage from hailstorms and flap and spoiler inspections.

REPORT COVERAGE

The 3D Scanning market report offers qualitative and quantitative insights on 3D scanning and the detailed analysis of market size & growth rate for all possible segments in the market.

Along with this, the report provides an elaborative analysis of market dynamics, emerging trends, and competitive landscape. Key insights offered in the report are the adoption of 3D scanning by individual segments, recent industry developments such as partnerships, mergers & acquisitions, consolidated SWOT analysis of key players, Porter’s five forces analysis, business strategies of leading market players, macro and micro-economic indicators, and key industry trends.

The short range segment is leading the market as they have the ability to scan tough surfaces, such as dark and shiny surface finishes and are available at low cost.

The healthcare segment is expected to show the highest CAGR during the forecast period as 3D scanning allows medical professionals to study body parts in detail, prior to a surgical procedure.

Some of the key players in the market are THOR3D, CREAFORM, Artec 3D, CyberOptics Corporation, NeoMetrix Technologies, Inc., and Faro Technologies, Inc.

Seeking Comprehensive Intelligence on Different Markets?Get in Touch with Our Experts

Speak to an Expert

The global 3D scanning market size is valued at USD 6.46 billion in 2026, projected to reach USD 16.65 billion by 2034 at a CAGR of 12.56% during 2026–2034.