4D Imaging Radar Market Size, Share & Industry Analysis, By Radar Architecture (MIMO, DBF, FMCW, Doppler Radar, & Synthetic Aperture Radar), By Component (Radar SoC / RFIC, Antenna-in-Package, Transceivers, Software, & Embedded Systems), By Imaging Capability (2D Radar, 3D Radar, & 4D Imaging Radar), By Deployment Mode (OEM-Installed, Aftermarket, and Integrated into Perception Stacks), By Range (Short-Range (up to ~30 m), Mid-Range (30–100 m), and Long-Range (>100 m)), By Frequency Band (24 GHz, 60 GHz, 76–77 GHz, 77–81 GHz, and >81 GHz), By Application, and Regional Forecast 2026-2034

4D Imaging Radar Market Size and Future Outlook

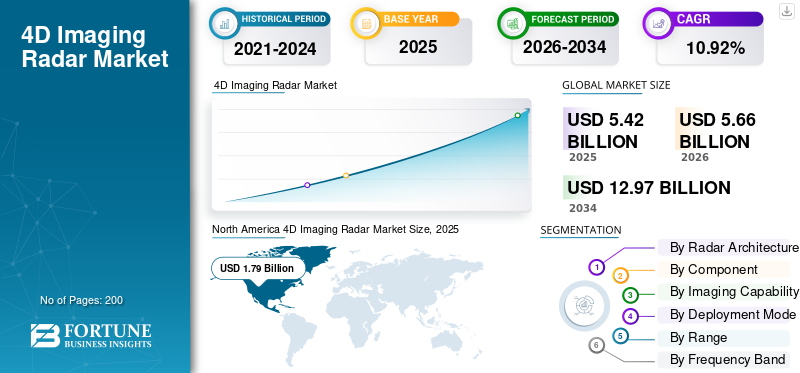

The global 4D imaging radar market size was valued at USD 5.42 billion in 2025. The market is projected to grow from USD 5.66 billion in 2026 to USD 12.97 billion by 2034, exhibiting a CAGR of 10.92% during the forecast period. North America dominated the 4D imaging radar market with a market share of 33.03% in 2025.

4D imaging radar is an advanced radar sensor technology that utilizes MIMO antenna arrays operating in the 76-81 GHz mmWave band to generate high-resolution point clouds capturing range, azimuth, elevation, and velocity (Doppler) of objects in real-time.

The market is experiencing significant growth driven by surging demand for autonomous vehicles, regulatory mandates for safety regulations features in Europe and North America, and integration with sensor fusion technologies by OEMs such as BMW, Tesla, and Mercedes-Benz. Advancements in signal processing, cost reductions, and superior performance in poor visibility further accelerate adoption across automotive (dominant segment), defense, and industrial sectors. Expansion into long-range variants enhances highway and urban navigation capabilities.

The 4D imaging radar market is highly consolidated, with top players Texas Instruments, NXP Semiconductors, Infineon Technologies, Robert Bosch, and Mobileye holding 65-90% share through advanced mmWave SoCs, OEM partnerships, and R&D in AI-enabled processing.

Download Free sample to learn more about this report.

4D Imaging Radar Market Key Takeaways

- 2025 Market Size: USD 5.42 billion

- 2026 Market Size: USD 5.66 billion

- 2034 Forecast Market Size: USD 12.97 billion

- CAGR: 10.92% from 2026–2034

- North America dominated the 4D imaging radar market with a 33.03% share in 2025.

- The Digital Beamforming (DBF) sub-segment accounted for 39.21% of the global market share in 2025.

- The transceivers sub-segment held 35.08% of the market share in 2025.

Asia Pacific

Asia Pacific emerged as the second-largest regional market with a valuation of USD 1.56 billion in 2025.

North America

North America generated USD 1.79 billion in revenue in 2025 and is projected to reach USD 1.86 billion in 2026.

Europe

Europe recorded a market value of USD 1.28 billion in 2025 and is projected to grow at the second-fastest CAGR of 11.47%.

U.S.

The U.S. 4D imaging radar market was valued at USD 1.70 billion in 2025.

Japan

Rising adoption of next-generation automotive safety technologies and increasing investments in intelligent mobility solutions are driving demand across the 4D imaging radar market.

Read More

4D Imaging Radar Market Trends

Increasing Shift from Incremental Channel Scaling to Architectural Innovation Leads to Market Trend

On the technology front, 4D imaging radar is undergoing a shift from incremental channel scaling to architectural and algorithmic innovation designed specifically for high‑fidelity point‑cloud generation. An IEEE paper on 4D automotive radar sensing proposes a joint sparsity design in frequency spectrum and array configuration, using random sparse step‑frequency waveforms and 2D sparse MIMO arrays to emulate large uniform arrays with far fewer physical elements, while maintaining range and angular resolution.

This approach addresses cost, power, and packaging constraints by achieving "virtual" aperture gains through signal processing rather than pure hardware scaling. A 2023–2024 survey on 4D mmWave radar in autonomous driving further details trends such as learning radar-based data generation, pre‑CFAR feature extraction, and multi‑modal fusion with vision and LiDAR, highlighting how radar perception is being integrated into end‑to‑end AI pipelines rather than treated as a standalone sensor.

Download Free sample to learn more about this report.

Market Dynamics

MARKET DRIVERS

Structural Demand Drivers for 4D Imaging Radar Adoption Regulation Fuels Market Expansion

From a demand perspective, the primary driver for the global 4D imaging radar market growth is the shift from basic ADAS toward L2+/L3 automation, which requires robust perception under all weather and lighting conditions that cameras and LiDAR alone cannot reliably provide. 4D mmWave radar delivers range, azimuth, elevation, and Doppler information, enabling precise object classification and tracking in adverse environments, and is therefore becoming a default element in redundancy-driven sensor stacks.

Vayyar's automotive white paper explicitly links 4D imaging radar to gaining Euro NCAP points for functions such as Child Presence Detection and occupant status monitoring, underscoring its role in regulatory compliance. For instance, in January 2026, AB Dynamics highlighted Euro NCAP's provisional 2026 protocols, which tighten advanced driver assistance systems ADAS test requirements and implicitly push OEMs toward higher performance sensing, including imaging radar.

MARKET RESTRAINTS

Hike in Cost and Increasing Complexity of 4D Imaging Radar System Hampers the Market Growth

Despite strong pull, the economics and complexity of the 4D imaging radar system remain major constraints, particularly for cost‑sensitive vehicle segments and non‑automotive customers. Vayyar notes that modern vehicles can integrate up to 200 sensors, with electronics already accounting for more than 35% of total vehicle cost, expected to rise toward 50% by 2030, making any new sensor's bill‑of‑materials and integration burden highly scrutinized.

4D radar modules add RF front‑ends, large MIMO arrays, and high‑performance processing, which are more expensive than legacy 2D/3D radar and raise cooling, packaging, and EMC design requirements. The Vayyar white paper explicitly positions 4D radar as a response to rising complexity and cost-effectiveness in meeting Euro NCAP protocols, but also acknowledges that OEMs expect multi-functionality (in‑cabin, perimeter, and ADAS) from a single platform to justify investment.

MARKET OPPORTUNITIES

New verticals, New Use Cases, and Platform Monetization Growth lead to a Lucrative Market Opportunity

From a strategic growth lens, 4D imaging radar is positioned to move from a "feature enabler" in passenger cars to a horizontal sensing platform serving multiple mobility and infrastructure domains. A July 2025 industry article from Arbe Robotics frames 4D radar as a "game‑changing technology in countless verticals", highlighting opportunities in commercial vehicles, aerial platforms, and static installations for traffic management, site safety, and smart cities.

These deployments monetize the same core capabilities, high‑resolution point clouds, and velocity information across automated trucking, last‑mile delivery robots, urban intersections, and construction sites. The January 2026 Berkeley Wireless Research Center talk with Zadar Labs similarly emphasizes use cases in robotics perception, perimeter security, and smart traffic infrastructure, positioning 4D radar as a "cornerstone technology" for intelligent systems that must operate in rain, fog, and low light.

MARKET CHALLENGES

Interference, Test Complexity, Standardization, and Safety Regulations Cause Challenges in the Market

Even as technology advances, the industry faces structural challenges in achieving reliable, scalable deployment of 4D imaging radar across heterogeneous environments and vehicle fleets. The March 2025 review of 4D mmWave radar in adverse environments notes gaps in publicly available datasets covering diverse weather, urban clutter, and mixed traffic, which limits the ability to benchmark algorithms and can lead to overfitting to narrow conditions.

The broader 4D mmWave survey also highlights issues such as noise, sparsity handling, data standardization, and the need for richer datasets for SLAM and scene reconstruction, implying that perception stacks may not generalize well across regions and driving cultures without substantial localization effort.

SEGMENTATION ANALYSIS

By Radar Architecture

Growing Need of FMCW Radar Boosts the Short Range Radars Anticipate the Growth of the Market

By radar architecture, the segment is further divided into Multiple-Input Multiple-Output (MIMO), Digital Beamforming (DBF), Frequency Modulated Continuous Wave (FMCW), Doppler radar, and synthetic aperture radar.

The Frequency Modulated Continuous Wave (FMCW) sub-segment is estimated to be the fastest growing with the highest CAGR of 12.17% during the forecast period. The growth is driven by the de‑facto standard for mmWave automotive safety radar, combining accurate range/velocity estimation with relatively simple RF hardware that scales efficiently from single‑chip short‑range sensors to long‑range front radars.

Digital Beamforming (DBF) sub-segment is accounted for the largest 4D imaging radar market share of 39.21% in 2025, and is expected to record a CAGR of 11.63% during the forecast period.

By Component

AI-Native Radar Software Architectures Drive Scalable Expansion of the Market Growth

By component, the segment is further divided into radar SoC/RFIC, antenna-in-package (aip), transceivers, software, and embedded systems.

The software sub-segment is estimated to be the fastest growing with the highest CAGR of 12.72% during the forecast period. The growth is driven by the scalability of software across multiple radar nodes and vehicle generations, further amplifying growth potential, as OEMs seek unified perception stacks that integrate 4D radar data with camera, LiDAR, and map inputs for robust environmental modeling.

The transceivers sub-segment is accounted for the largest market share of 35.08%, and is expected to record a CAGR of 9.58% during the forecast period.

By Imaging Capability

Growing Elevation of 4D Radar Enhances Precision and ADAS Compliance that Cater the Market Growth

By imaging capability, the segment is further divided into 2D radar, 3D radar, and 4D imaging radar.

The 4D imaging radar sub-segment is estimated to be the fastest growing with the highest CAGR of 11.74% during the forecast period. The growth is driven by its breakthrough addition of elevation angle measurement, transforming conventional 3D point clouds into rich volumetric representations that enable cyclist/pedestrian discrimination, precise height radar-based tracking, and clutter rejection critical for Level 3+ highway pilot and urban autonomy validation.

The 3D radar sub-segment is accounted for the second-largest market share of 47.44% globally, with a CAGR of 10.66% during the forecast period.

By Deployment Mode

Perception Stacks Lead via OEMs Shifting To Unified AI-Native Pipeline Catalyze the Market Growth

By deployment mode, the market is divided into OEM-installed, aftermarket, and integrated into perception stacks.

Integrated into perception stacks sub-segment is estimated to be the fastest growing with the largest CAGR of 13.23% during the forecast period. The growth is anticipated by OEMs' transition from discrete sensor silos to unified AI-native processing pipelines where 4D radar data streams feed centralized domain controllers alongside camera, LiDAR, and HD map inputs, unlocking end-to-end occupancy network models for robust scene understanding.

The OEM-Installed sub-segment is accounted for the largest market share of 63.01% globally, with a CAGR of 9.71% during the forecast period.

By Range

Explosive Proliferation Driven by Urban ADAS Expansion Leads to Short-Range (up to ~30m) Segmental Growth

By range, the segment is further divided into short-range (up to ~30 m), mid-range (30–100 m), and long-range (>100 m).

Short-range (up to ~30 m) sub-segment is estimated to be the fastest growing with the highest CAGR of 12.88% during the forecast period. Growth trajectory as urban mobility demands proliferate blind-spot intervention, rear cross-traffic alert, parking assist, and vulnerable road user protection around vehicle corners, where sub-30-meter high-resolution elevation data prevents collisions with pedestrians, two-wheelers, and infrastructure.

The long-range (>100 m) sub-segment accounted for the largest market share of 52.67% globally, with a CAGR of 11.02% during the forecast period.

By Frequency Band

Growth of the Market is Driven by Increasing Adoption of 77–81 GHz Band Across Global Automotive Sector

By frequency band, the segment is further divided into 24 GHz, 60 GHz, 76–77 GHz, 77–81 GHz, and >81 GHz (Sub-THz).

The 77–81 GHz sub-segment is estimated to be the fastest growing with the highest CAGR of 12.88% during the forecast period. The growth is driven by its regulatory approval across major automotive markets, including Europe, North America, China, and Japan, providing up to 4 GHz of contiguous spectrum that delivers unprecedented range resolution below 5 cm alongside long-range detection exceeding 300 meters, essential for highway merge and cut-in scenarios.

The 76–77 GHz sub-segment accounted for the second-largest market share of the market with an 18.16% share globally, with a CAGR of 9.13%.

By Application

Smart Infrastructure Fuels Intelligent Transportation Growth Across Emerging Countries

By application, the segment is further divided into automotive, industrial automation & robotics, aerospace & defense, smart infrastructure, security & surveillance, maritime navigation, healthcare & elderly monitoring, and consumer electronics.

The smart infrastructure sub-segment is estimated to be the fastest growing with the highest CAGR of 13.73% during the forecast period. The growth is driven by cities worldwide deploying intelligent transportation systems featuring roadside units at intersections, highways, and smart poles to enable cooperative perception, dynamic signal timing, and vulnerable road user protection through Radar-LiDAR-camera fusion networks.

The automotive sub-segment accounts for the second-largest market share of 49.04% globally, with a CAGR of 11.45% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

4D Imaging Radar Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, the Middle East & Africa, and Latin America.

North America 4D Imaging Radar Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America held the dominant share in 2025, valued at USD 1.79 billion, and will also maintain the leading share in 2026, with an anticipated USD 1.86 billion. The region is experiencing rapid growth driven by the surge in ADAS and autonomous vehicle (AV) adoption. Key factors include stringent vehicle safety mandates, the need for high-resolution environmental mapping in challenging weather, and significant R&D investments from major automakers such as Ford and GM.

U.S. 4D Imaging Radar Market

Based on North America's strong contribution and the U.S. dominance within the region, the U.S. market reached USD 1.70 billion in 2025 and is estimated to have a CAGR of 10.78% during the forecast period.

Europe

Europe is projected to grow at the second-fastest rate with a CAGR of 11.47% during the forecast period. In 2025, the market value stood at USD 1.28 billion. Europe exhibits significant growth through the stringent EU General Safety Regulation 2019/2144 mandating AEB for VRUs by 2024 and Euro NCAP 2026 protocols elevating radar resolution requirements, with Volkswagen Group and Stellantis embedding 4D sensors across mid-to-premium segments for city/highway autonomy.

U.K. 4D Imaging Radar Market

The U.K. market growth in 2025 is valued at USD 0.26 billion and is estimated to grow at a rate of 10.91% during the forecast period.

Eastern Europe 4D Imaging Radar Market

The Eastern market growth in 2025 is valued at USD 0.40 billion and is estimated to grow at a rate of 13.12% during the forecast period.

Germany 4D Imaging Radar Market

The German market growth in 2025 is valued at USD 0.18 billion and is estimated to grow at a rate of 9.80% during the forecast period.

Asia Pacific

The Asia Pacific market is valued at USD 1.56 billion in 2025 and secures the position of the second-largest region in the market. Also, the region is estimated to be the fastest growing with the highest CAGR of 12.16% during the forecast period. Asia Pacific surges as the fastest-growing region, propelled by China's NEV dual-credit policy mandating intelligent driving scores and India's Smart Cities Mission deploying radar-enabled traffic management, with domestic OEMs such as BYD and NIO scaling 4D radar across mass-market EVs to meet MIIT's L2+ penetration targets exceeding 50% by 2027.

China 4D Imaging Radar Market

China's market growth in 2025 is valued at USD 0.72 billion and has an estimated growth rate of 11.92% during the forecast period.

India 4D Imaging Radar Market

India's market in 2025 is valued at USD 0.19 billion and has an estimated growth rate of 15.73% during the forecast period.

Japan 4D Imaging Radar Market

The Japanese market in 2025 is valued at USD 0.16 billion and has an estimated growth rate of 14.81% during the forecast period.

Middle East & Africa and Latin America

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is valued at USD 0.22 billion in 2025. The Middle East & Africa market is valued at USD 0.56 billion in 2025.

Brazil 4D Imaging Radar Market

The Brazilian market growth in 2025 is valued at USD 0.16 billion and is estimated to grow at a rate of 9.43% during the forecast period.

Turkey 4D Imaging Radar Market

Turkey's market growth in 2025 is valued at USD 0.16 billion and is estimated to have a growth rate of 11.41% during the forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players

Established Tier-1 Automotive Industry Suppliers Strengthen Key Company Players Across the Globe

The 4D imaging radar market exhibits a consolidated competitive structure dominated by established Tier-1 automotive industry suppliers who leverage long-term platform contracts, automotive-grade manufacturing scale, and integrated ADAS portfolios to secure the majority of production awards from global OEMs.

These leaders differentiate through end-to-end system responsibility encompassing radar hardware, perception software, vehicle integration, and ASIL-certified validation, creating high switching costs that preserve margins despite commoditizing RF front-ends.

LIST OF KEY 4D IMAGING RADAR COMPANY PROFILED

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- Aptiv PLC (Ireland)

- Denso Corporation (Japan)

- Valeo SA (France)

- Magna International (Canada)

- Mobileye (Intel) (Israel)

- Huawei Technologies (China)

- Texas Instruments (TI) (U.S.)

- NXP Semiconductors (Netherlands)

- Infineon Technologies AG (Germany)

- Renesas Electronics Corp. (Japan)

- Arbe Robotics Ltd. (Israel)

- Zadar Labs, Inc. (U.S.)

- Smart Radar System, Inc. (South Korea)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Arbe Robotics Ltd. announced that Sensrad Company, based in Sweden, has begun delivering its first radar series powered by Arbe's chipset to customers. These radars are destined for deployment in a defense sector autonomous off-road vehicle application and in an intelligent road infrastructure project.

- July 2025: German defense electronics firm HENSOLDT has received a major contract to deliver radar systems that will enhance Ukraine's air defense capabilities. The comprehensive package, worth over USD 370 million, includes deliveries of high-performance TRML-4D radars and short-range SPEXER 2000 3D MkIII surveillance systems.

- July 2025: Arbe Robotics (ARBE) is developing a new class of automotive radar technology with its ultra-high-resolution 4D imaging radar chipset. While the product appears differentiated and interest from major OEMs is growing, Arbe remains pre-revenue in any meaningful sense.

- September 2024: Arbe Robotics, its tier‑1 partner Sensrad, signed a framework agreement to supply 4D imaging radars to China‑based Tianyi Transportation Technology. Sensrad described the deal as its first commercial contract after a year‑long evaluation using Arbe's chipset and Gapwaves' waveguide antenna technology.

- December 2023: The Bihar police is going to introduce a speed violation detection system with 4D imaging radar to monitor traffic on national highways in the state effectively

REPORT COVERAGE

The global 4D imaging radar market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2024 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.92% from 2026-2034 |

|

Unit |

USD Billion |

|

Segmentation |

By Radar Architecture

By Component

By Imaging Capability

By Deployment Mode

By Range

By Frequency Band

By Application

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.42 billion in 2025 and is projected to reach USD 12.97 billion by 2034.

In 2025, the European market value stood at USD 1.28 billion.

The market is expected to exhibit a CAGR of 10.92% during the forecast period.

The smart infrastructure sub-segment is expected to hold the highest CAGR over the forecast period.

Structural demand drivers for 4D imaging radar adoption, regulation, OEM platform decisions, and safety positioning.

Texas Instruments, NXP Semiconductors, Infineon Technologies, Robert Bosch, and Mobileye are the top key players in the market.

North America dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us