5G Fixed Wireless Access Market Size, Share & Industry Analysis, By Offering (Hardware and Services), By Operating Frequency (Sub-6 GHz, mmWave 24 to 39 GHz, and mmWave above 39 GHz), By Demography Type (Urban, Semi-urban/Suburban, and Rural), By End User (Residential, Commercial/SMB, Industrial, and Government/Public Sector), and Regional Forecast, 2026 - 2034

KEY MARKET INSIGHTS

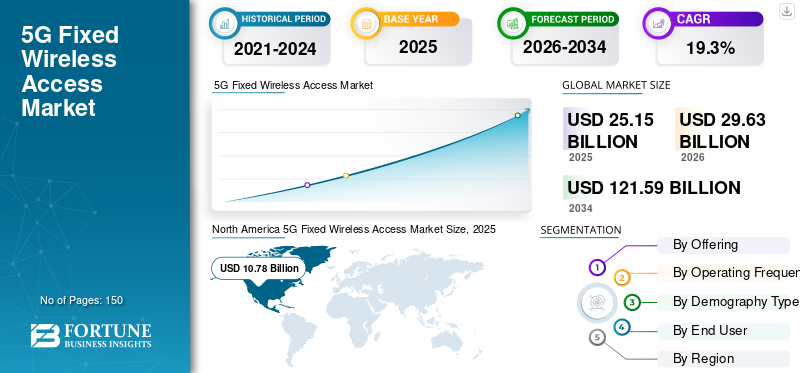

The global 5G fixed wireless access market size was valued at USD 25.15 billion in 2025. The market is projected to grow from USD 29.63 billion in 2026 to USD 121.59 billion by 2034, exhibiting a CAGR of 19.3% during the forecast period. North America dominated the global market with a market share of 42.86% in 2025.

The 5G Fixed Wireless Access (FWA) delivers fixed broadband connectivity to consumers and businesses using cellular technology based on 5G cellular networks, instead of traditional wired infrastructure, such as fiber or cable. It enables the rapid and cost-efficient deployment of high-quality broadband services. It is especially beneficial for residential locations in areas where developing wired broadband services would be too costly or impractical. Market growth is driven by increasing demand for high-speed broadband, rapid expansion of 5G networks, and improvements in 5G device and CPE performance.

Furthermore, many key industry players, such as Telefonaktiebolaget LM Ericsson, Nokia, Samsung Electronics, Huawei Technologies Co., Ltd., and ZTE Corporation, operating in the market, are focusing on rapid network expansion using mid band spectrum, subsidized and bundled CPE offerings, speed based broadband pricing, partnerships with device vendors, and targeting underserved residential and SME segments to scale subscriber adoption quickly.

Download Free sample to learn more about this report.

5G Fixed Wireless Access Market MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 25.15 billion

- 2026 Market Size: USD 29.63 billion

- 2034 Forecast Market Size: USD 121.59 billion

- CAGR: 19.3% from 2026–2034

- North America dominated the global market with a 42.86% share in 2025.

- The residential segment accounted for 70.7% of the market share in 2025.

- Services segment led the market due to strong recurring subscription-based revenue models.

North American

North America led the market with USD 10.78 billion in 2025, driven by large-scale 5G FWA adoption and operator expansion.

Europe

Europe is witnessing strong growth supported by affordable broadband expansion and digital connectivity goals.

Asia Pacific

Asia Pacific is emerging as a key growth region with rapid 5G FWA rollout and large subscriber potential.

U.S.

Market estimated at USD 9.39 billion in 2026, driven by strong operator-led FWA expansion.

Japan

Market estimated at USD 1.32 billion in 2026, supported by dense 5G networks and urban broadband demand.

Read More

IMPACT OF GENERATIVE AI

Rising Generative AI Usage Driving Higher Performance Requirements for 5G FWA

Generative AI enhances the 5G FWA by increasing demand for higher, more consistent broadband performance at home and in small offices, particularly where fiber is limited, as AI assistants and multimodal apps lead to heavier upstream usage and tighter latency expectations. As the demand for more uplink data through AI solutions increases, telecommunications service providers have a greater incentive to enhance their 5G networks with additional capacity, allowing them to maximize the monetization of premium broadband opportunities through differentiated broadband plans. Additionally, as AI continues to create a more intelligent user experience and enhance the user experience of CPEs through on-device artificial intelligence, CPEs will exhibit enhanced reliability and experience fewer support calls when used in conjunction with AI-intensive solutions. Finally, as AI is pushing data processing to the "edge" of the network, FWA is a very attractive option for companies to provide broadband for remote or temporary sites that require high-speed access quickly and at a low cost. For instance,

- In 2025, Nokia states that broader adoption of today’s AI apps could drive uplink traffic growth by more than 50%, highlighting why uplink capacity becomes a planning and investment priority.

5G FIXED WIRELESS ACCESS MARKET TRENDS

Increasing Use of Speed-Based and Tiered Pricing Models by Operators Fuels Market Growth

As more operators offer similar 5G FWA products with comparable speed offerings, the primary differentiator of 5G FWA has become the way consumers compare broadband. A consumer typically compares the advertised speeds, as well as the reliability, of a broadband service. Therefore, operators have transitioned from using the traditional model of offering multiple tiers (data buckets) to a tiered speed-based offering. This approach also helps operators monetize capacity upgrades by charging more for higher-speed tiers while steering heavy users toward plans that match the network's capability in each coverage zone. It improves customer clarity at the point of purchase, reduces bill shock and throttling complaints, and supports better network management as demand can be shaped through tier design rather than solely through hard data caps.

Overall, by moving the FWA solution to a speed-tiered offer, it can help consumers feel more such as their FWA product is a "real" broadband service, and it can strengthen the conversion of consumers from DSL and cable broadband, especially in markets where fiber is not offered or

available. For instance,

- In June 2025, Ericsson reported that 51% of global CSPs with FWA offerings include speed-based options, up from 40% in June 2024, supporting the idea that operators are monetizing differentiated performance as new traffic types grow.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Quick Connect and Backup Connectivity for SMEs Drives Market Growth

The rapid adoption of 5G FWA by small and medium-sized enterprises (SMEs) is due to the speed at which SMEs can activate this service when expanding into new locations, opening temporary locations, or relocating to a new one. Instead of having to wait weeks for a wired installation, the faster SME's ability to utilize this service directly impacts their ability to generate revenue immediately when Canada Post opens new locations. In addition, due to the risk of short internet service outages causing disruptions to SMEs' point-of-sale systems, online ordering, customer service, and cloud-based software tools, many SMEs also purchase 5G FWA services as a secondary connection.

Wireless internet backup services are crucial for SMEs to mitigate the business risks inherent to these outages. To meet this growing demand, telecom operators have developed plug-and-play packages specifically designed for these "backup internet" applications, which can be installed in just a matter of minutes. As such, there is now a wider range of use cases for these speedy connections and failover products, not just for households, but also for SMEs that require continuity of service and expedited installation times. This is expected to boost the 5G fixed wireless access market growth in the coming years.

For instance,

- In March 2024, AT&T introduced Internet Air for Business, stating businesses can set up the fixed wireless service in minutes and that it is available nationwide, directly supporting the “quick connect” driver.

MARKET RESTRAINTS

Spectrum Limitations and Deployment Economics May Hinder Market Growth

Spectrum limitations and deployment economics hinder the 5G FWA market, as operators require broad, contiguous mid-band spectrum to deliver consistent broadband speeds to multiple households from each cell. In markets where mid-band spectrum is limited, fragmented, or expensive, operators may be forced to either limit the deployment of FWA services or invest heavily to support the densification of their networks and mitigate congestion. The increase in site upgrades, the need to build out additional backhaul facilities, and the need to purchase additional spectrum create additional costs per connection for an operator, thereby making it more difficult for them to price FWA comparably to fiber or cable, which is usually their best option for competitively priced service. Therefore, operators typically employ conservative deployment strategies, resulting in slower growth patterns in the market in regions with limited mid-band spectrum.

MARKET OPPORTUNITIES

Rapid Expansion of Mid Band 5G Networks Enabling Broadband Grade Performance to Create Lucrative Opportunity for Market Growth

The rapid growth in mid-band spectrum, such as 2.5 GHz and C band, will be a great opportunity for Fixed Wireless Access (FWA), as it delivers the right combination of coverage and capacity to provide Fixed Broadband with the stability and "fibery" feel needed. It has much greater throughput and sector capacity than low-band; therefore, an operator can connect a higher number of households to each cell while providing consistent speeds. Mid-band also has a larger footprint than mmWave; therefore, operators are able to rapidly grow their FWA footprint with the lowest cost for homes passed. As mid-band network units continue to become denser, new channel bandwidths become available, and operators can now confidently promote higher-speed product tiers, extend eligibility maps, and grow their subscriber base without impacting the mobile user experience.

Segmentation Analysis

By Offering

Recurring Connectivity Revenues Fueled Services Dominance in Market

Based on the offering, the market is bifurcated into hardware and services.

Services accounted for the largest 5G fixed wireless access market share in 2025 and are expected to grow at the highest CAGR of 20.1% over the forecast period. This is due to 5G FWA generating recurring monthly broadband revenue throughout the entire customer's lifetime. In contrast, hardware sales are essentially one-time and often subsidized or bundled with the service. As subscriber bases scaled rapidly, cumulative connectivity, data plans, and managed service revenues grew much faster than standalone customer premises equipment (CPE) revenue.

Hardware is anticipated to grow at a moderate CAGR during the forecast period. This is due to the fact that rising 5G FWA subscriptions continue to drive demand for indoor and outdoor CPE, but declining device prices and widespread operator subsidies limit overall hardware revenue growth.

By Operating Frequency

Broad Coverage and Cost-Efficient Deployment Boosted Sub-6 GHz Dominance in 5G FWA

Based on operating frequency, the market is categorized into Sub-6 GHz, mmWave 24 to 39 GHz, and mmWave above 39 GHz.

In 2025, the Sub-6 GHz segment dominated the global market. This band has the most advantageous ratio of extensive range compared to a good level of reliable signal penetration indoors, thus making it a very effective solution for delivering Broadband Wireless Access (BWA) on a large scale via 5G networks. Its lower site density and deployment cost compared with mmWave allowed operators to rapidly expand service availability across urban, suburban, and rural areas.

The mmWave segment above 39 GHz is expected to grow at the highest CAGR of 23.4% over the forecast period, as operators increasingly deploy it in dense urban areas and enterprise locations where ultra-high capacity and gigabit-class speeds are required and can be economically justified.

By Demography Type

Dense Network Infrastructure and High Demand Propelled Urban Dominance in 5G FWA

Based on the demography type, the market is divided into urban, semi-urban/suburban, and rural.

The urban segment held a dominating market share in 2025. Urban areas have high population densities, serve as the largest consumers of data usage, and contain the densest number of 5G sites, providing scalability and consistent performance for 5G fixed wireless access (FWA). In addition, operators have targeted urban areas to quickly generate revenue from already deployed 5G capacity, and to compete with traditional broadband services offered by cable companies and legacy providers.

The rural segment is projected to grow at the highest CAGR of 20.9% over the forecast period, as 5G FWA offers a faster and more cost-effective alternative to fiber for expanding broadband coverage in underserved and hard-to-reach locations.

By End User

To know how our report can help streamline your business, Speak to Analyst

Strong Home Broadband Demand Bolstered Residential Leadership in Market

Based on the end user, the market is classified into residential, commercial/SMB, industrial, and government/public sector.

The residential sector is expected to hold a dominant market share over the forecast period. This is due to strong demand for high-speed home internet connectivity for streaming, remote work, gaming, and digital services in areas with limited wired broadband options. Operators also aggressively marketed 5G FWA as a primary or alternative home broadband solution, driving large-scale household adoption.

The industrial sector is anticipated to grow at the highest CAGR of 22.1% during the forecast period. Manufacturers, logistics hubs, and energy sites increasingly adopt 5G FWA for rapid site connectivity, private network support, and reliable backup links in digitally enabled operations.

5G Fixed Wireless Access Market Regional Outlook

By geography, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

North America

North America 5G Fixed Wireless Access Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest 5G fixed wireless access market share in 2024, valued at USD 7.93 billion, and maintained this leading share in 2025, with a value of USD 10.78 billion. The market in North America is expected to increase, as U.S. operators scale 5G FWA as a mainstream home broadband product, along with the rapid deployment of mid-band spectrum networks to increase service eligibility and support higher speed tiers. This enables the world's largest installed base for FWA subscribers and exhibits the fastest revenue growth rate of any major geography. For instance,

- The top three U.S. FWA providers, including AT&T, T-Mobile, and Verizon, reached 14.7 million FWA customers after adding 1.04 million subscribers in Q3 2025.

These factors play a significant role in fueling the market growth.

U.S 5G Fixed Wireless Access Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 9.39 billion in 2026, accounting for roughly 31.7% of global 5G fixed wireless access (FWA) sales.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe is projected to record a growth rate of 18.7% in the coming years, the second-highest among all regions, and reach a valuation of USD 7.07 billion by 2026. The market is experiencing significant growth in the region, driven by the increasing adoption of 5G FWA by operators as a quick and affordable way to provide high-speed broadband in areas with slow or costly fiber deployments, as well as to ensure compliance with the Digital Decade connectivity goals.

U.K 5G Fixed Wireless Access Market

The U.K. market in 2026 is estimated at around USD 1.32 billion, representing roughly 4.5% of global 5G fixed wireless access revenues.

Germany 5G Fixed Wireless Access Market

Germany’s 5G FWA market is projected to reach approximately USD 1.39 billion in 2026, equivalent to around 4.7% of global 5G fixed wireless access sales.

Asia Pacific

Asia Pacific is estimated to reach USD 6.96 billion in 2026 and secure the position of the third-largest region in the market. This is owing to the large, population-based markets that are adopting 5G FWA as a quicker alternative to fiber for home broadband access. Ericsson predicts that approximately 50% of total global FWA connections will be located in the Asia Pacific Region by 2031, due to the region's significant rollout momentum.

Growth in this market is supported by the robust commercialization of 5G FWA in regions such as India. In 2024, devices used for 5G FWA are estimated to be at least 86% 5G-enabled, and many telecommunications companies are offering their customers the chance to use 5G fixed broadband services to generate revenue for their network investment. In the region, India and China are both estimated to reach USD 0.94 billion and USD 1.48 billion, respectively, in 2026.

Japan 5G Fixed Wireless Access Market

The Japanese 5G FWA market in 2026 is estimated at around USD 1.32 billion, accounting for roughly 4.5% of global 5G fixed wireless access revenues. This is due to operators leveraging dense 5G networks to deliver high-quality home broadband and backup connectivity in urban areas, where demand for reliable, high-speed internet remains strong despite mature fiber infrastructure.

China 5G Fixed Wireless Access Market

China’s 5G FWA market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 1.48 billion, representing roughly 5.0% of global 5G FWA sales.

India 5G Fixed Wireless Access Market

The Indian 5G FWA market in 2026 is estimated to be around USD 0.94 billion, accounting for roughly 3.2% of global 5G FWA revenues.

South America

South America is expected to witness moderate growth in this market space during the forecast period. The South America market is set to reach a valuation of USD 1.30 billion in 2026. This is due to the fact that operators use FWA to quickly expand affordable broadband coverage in underserved urban outskirts and rural areas where fiber deployment is slow and costly.

Middle East & Africa

The Middle East & Africa are estimated to reach USD 1.70 billion in 2026 and are expected to grow at a significant rate in the coming years. As 5G FWA enables rapid broadband expansion in areas with limited fixed-line infrastructure, it helps operators address connectivity gaps without incurring heavy fiber investment. In addition, rising digitalization initiatives, smart city projects, and the growing demand for high-speed internet among households and SMEs are accelerating the adoption of 5G FWA across the region. In the Middle East & Africa, the GCC is set to reach a value of USD 0.54 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Product Portfolio by Key Players to Propel Market Progress

The global 5G FWA market has a semi-consolidated market structure, with prominent players such as Telefonaktiebolaget LM Ericsson, Nokia, Samsung Electronics, Huawei Technologies Co., Ltd., and ZTE Corporation holding significant market positions. The leadership of these companies is supported by continuous strategic initiatives, including expansion of 5G radio and core portfolios, development of advanced 5G FWA CPE (customer premises equipment), and optimization of network capacity to support broadband-grade fixed connectivity. Market players are also actively partnering with telecom operators, chipset vendors, and cloud service providers to improve service reliability, enable speed-based broadband offerings, and accelerate large-scale commercial deployments. For instance,

- In June 2025, Ericsson signed a multi-year managed services deal with Bharti Airtel to manage pan-India network operations, including 5G FWA, signaling strategic operator partnerships to strengthen service delivery and operational efficiency.

Other notable players in the global market include NEC Corporation, Fujitsu, Cisco Systems, Inc., Qualcomm Technologies, Inc., and Ciena. These companies are expected to focus on new product launches, enhanced 5G transport and backhaul solutions, software-driven network optimization, and long-term service and support capabilities to strengthen their competitive positioning and expand their global footprint during the forecast period.

LIST OF KEY 5G FIXED WIRELESS ACCESS COMPANIES PROFILED

- Telefonaktiebolaget LM Ericsson (Sweden)

- Nokia (Finland)

- Samsung Electronics (South Korea)

- Huawei Technologies Co., Ltd. (China)

- ZTE Corporation (China)

- NEC Corporation (Japan)

- Fujitsu (Japan)

- Cisco Systems, Inc. (U.S.)

- Qualcomm Technologies, Inc. (U.S.)

- Ciena(U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Indra announced it completed end-to-end testing and operational implementation of V2X tolling on North Carolina’s I-485, positioning it as a live-highway benchmark for connected tolling and safety use cases. The release also pointed to intent for a full-corridor rollout, reinforcing the shift from demonstration to deployment-ready infrastructure.

- October 2025: Nokia is targeting an expanded presence of 5G FWA products in India, with anticipated millimeter-wave FWA launches within six months, aligning with multiple market deals and a push to scale enterprise and hyperscaler broadband solutions.

- March 2025: Fujitsu partnered with Rakuten Mobile to deploy Fujitsu-developed radio units as Rakuten accelerates expansion of its 5G Sub6 coverage in 2025. The rollout enhances network reach and capacity, enabling more consistent broadband-grade performance for services, including 5G FWA.

- February 2025: Samsung Electronics partnered with UScellular to enhance its 5G fixed wireless access service in the U.S. using mmWave and virtualised RAN technology, supporting faster broadband speeds in the mid-Atlantic region.

- May 2024: Cisco Meraki introduced its first 5G Standalone fixed wireless access devices, the Meraki MG52 and MG52E, designed to scale secure 5G connectivity for business sites. Cisco also highlighted these gateways as a way to connect branches faster with primary or failover broadband, aligning directly with 5G FWA adoption for enterprises and SMBs.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 19.3% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Offering, Operating Frequency, Demography Type, End User, and Region |

|

By Offering |

· Hardware · Services |

|

By Operating Frequency |

· Sub-6 GHz · mmWave 24 to 39 GHz · mmWave above 39 GHz |

|

By Demography Type |

· Urban · Semi-urban/Suburban · Rural |

|

By End User |

· Residential · Commercial/SMB · Industrial · Government/Public Sector |

|

By Region |

· North America (By Offering, Operating Frequency, Demography Type, End User, and Country) o U.S. (By End User) o Canada (By End User) o Mexico (By End User) · South America (By Offering, Operating Frequency, Demography Type, End User, and Country) o Brazil (By End User) o Argentina (By End User) o Rest of South America · Europe (By Offering, Operating Frequency, Demography Type, End User, and Country) o U.K. (By End User) o Germany (By End User) o France (By End User) o Italy (By End User) o Spain (By End User) o Russia (By End User) o Benelux (By End User) o Nordics (By End User) o Rest of Europe · Middle East & Africa (By Offering, Operating Frequency, Demography Type, End User, and Country) o Turkey (By End User) o Israel (By End User) o GCC (By End User) o North Africa (By End User) o South Africa (By End User) o Rest of Middle East & Africa · Asia Pacific (By Offering, Operating Frequency, Demography Type, End User, and Country) o China (By End User) o India (By End User) o Japan (By End User) o South Korea (By End User) o ASEAN (By End User) o Oceania (By End User) o Rest of Asia Pacific |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 25.15 billion in 2025 and is projected to reach USD 121.59 billion by 2034.

In 2025, the market value in North America stood at USD 10.78 billion.

The market is expected to exhibit a CAGR of 19.3% during the forecast period of 2026-2034.

By end user, the residential segment is expected to lead the market.

Increasing demand for quick connect and backup connectivity for SMEs drives market growth.

Telefonaktiebolaget LM Ericsson, Nokia, Samsung Electronics, Huawei Technologies Co., Ltd., and ZTE Corporation are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us