800V Electric Vehicle Architecture Market Size, Share & Industry Analysis, By Component Type (Battery Pack, Power Electronics, Electric Motor, Charging System, and Thermal Management Systems), By Vehicle Type (Passenger Vehicles, LCVs, and HCVs), By Propulsion Type (BEVs and PHEVs), By Power Output Level (Below 150 kW, 150–300 kW, and Above 300 kW), and Regional Forecast, 2026–2034

800V Electric Vehicle Architecture Market Size and Future Outlook

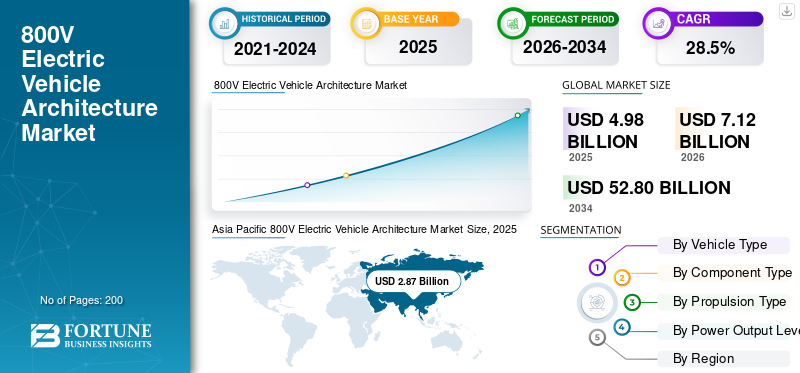

The global 800V electric vehicle architecture market size was valued at USD 4.98 billion in 2025. The market is projected to grow from USD 7.12 billion in 2026 to USD 52.80 billion by 2034, exhibiting a CAGR of 28.5% during the forecast period. Asia Pacific dominated the 800v electric vehicle architecture market with a market share of 57.63% in 2025.

800V electric vehicle architecture refers to a high-voltage power system in EVs that enables faster charging, improved efficiency, reduced energy losses, and enhanced performance compared to conventional 400V systems. Market growth is driven by rising demand for fast-charging electric vehicles, increasing adoption of high-performance EV platforms, advancements in battery technology, and growing investments by automakers in next-generation vehicle architectures.

Major players in the market include Porsche AG, Hyundai Motor Company, Kia Corporation, Lucid Motors, Tesla, and BYD. These players compete through high-voltage platform innovation, ultra-fast charging capabilities, efficiency optimization, and advanced power electronics integration.

Download Free sample to learn more about this report.

800V ELECTRIC VEHICLE ARCHITECTURE MARKET TRENDS

Rising Deployment of Ultra-Fast Charging Infrastructure Supports Market Expansion

The increasing deployment of ultra-fast charging infrastructure is significantly influencing market growth for 800V electric vehicle architecture. Charging networks capable of supporting higher voltages enable reduced charging time, making EVs more convenient for long-distance travel and daily usage. Governments and private players are investing heavily in high power levels charging corridors, especially across Europe, North America, and the Asia Pacific. This expansion of infrastructure is encouraging automakers to adopt 800v systems, as compatibility with ultra-fast chargers becomes a key differentiator in enhancing consumer acceptance.

For instance, in March 2026, SK Signet launched a 400kW ultra-fast EV charger featuring silicon carbide technology and 96.5% efficiency, supporting high-voltage 800V architectures. The solution enhances charging speed, reduces footprint by 54%, and enables scalable infrastructure deployment, accelerating global ultra-fast charging network expansion.

Integration of Advanced Power Electronics to Amplify Product Demand

One of the key market trends is the growing integration of advanced power electronics such as silicon carbide inverters and high-efficiency converters within 800V architectures. These technologies reduce energy losses, improve thermal performance, and enhance overall drivetrain efficiency. Automakers are increasingly focusing on optimizing vehicle range and performance through such innovations. The shift toward lightweight, compact, and high-performance components also support vehicle design flexibility. Additionally, this trend is also expected to play a crucial role during the market forecast period, strengthening the competitive landscape and influencing market share distribution of the major players operating globally.

- For instance, in March 2026, STMicroelectronics expanded its 800V DC power conversion portfolio with new 12V and 6V architectures in collaboration with NVIDIA. The solutions enhance energy efficiency, reduce power losses, and support scalable, high-density AI infrastructure, highlighting broader adoption of high-voltage systems beyond automotive applications.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for High-Performance Electric Vehicles Drives Market Expansion

The growing consumer preference for high-performance electric vehicles is a major driver accelerating the adoption of 800V architectures. These systems enable superior acceleration, higher power output, and improved driving dynamics compared to conventional platforms. Premium and performance EV segments are leading this transition, as manufacturers aim to differentiate through enhanced capabilities. Increasing disposable incomes and evolving consumer expectations for performance and efficiency are further fueling market demand. These factors play a critical role in shaping the market, supporting sustained expansion across developed and emerging regions.

- For instance, in March 2026, Alpine unveiled its dedicated 800V EV sports car platform, Alpine Performance Platform, featuring cell-to-pack batteries, dual electric motors, and silicon carbide inverters. The architecture enhances performance, reduces weight, and enables faster charging, supporting next-generation high-performance electric sports cars.

Automaker Investments in Next-Generation Platforms to Strengthen Market Growth

Automotive manufacturers are heavily investing in next-generation EV platforms, which are significantly contributing to 800V electric vehicle architecture market growth. Leading OEMs are developing dedicated 800V architectures to future-proof their vehicle lineups and meet evolving efficiency standards. These investments are driven by the need to reduce charging time, improve vehicle range, and achieve cost efficiencies over time. Strategic collaborations with component suppliers and technology providers are also accelerating development cycles. These factors are expected to positively influence the market and enhance the scalability of high-voltage EV systems globally.

For instance, in April 2026, Kia outlined its 2030 strategy at its CEO Investor Day, planning significant investments to expand its electrified vehicle lineup and advanced mobility solutions. The roadmap emphasizes EV growth, autonomous driving, and next-generation technologies, supporting increased adoption of high-voltage architectures and strengthening global manufacturing and innovation capabilities.

MARKET RESTRAINTS

High Initial System Costs to Limit Product Adoption

One of the primary restraints in the market is the high initial cost associated with 800V electric vehicle architecture. Advanced components such as silicon carbide semiconductors, specialized wiring, and enhanced insulation systems contribute to increased production expenses along with supply chain hurdles. These costs make it challenging for mass-market vehicle segments to adopt the technology at scale. Additionally, limited economies of scale further restrict cost reduction in the short term, impacting market growth by slowing penetration in price-sensitive regions, thereby influencing overall market.

MARKET OPPORTUNITIES

Expansion into Mid-Range Vehicle Segments Creates New Growth Opportunities

The gradual expansion of 800V architecture into mid-range electric vehicle segments presents significant market opportunities. As the technology matures and component costs decline, automakers are increasingly expected to integrate high-voltage systems beyond premium vehicles. This transition will broaden the mid range vehicles and accelerates adoption rates across a wider consumer base. Increasing competition among manufacturers is also driving innovation and cost optimization. This opportunity is likely to strengthen 800V electric vehicle architecture market demand and contribute positively to market growth during the forecast period, particularly in emerging automotive markets.

- For instance, in March 2026, Renault unveiled its new 800V EV platform under the futuREady strategy, offering up to 750 km range and 1,400 km with a range extender. The platform supports ultra-fast charging and scalable configurations, accelerating global electrification and next-generation EV development.

Development of Integrated Charging Ecosystems Unlocks Market Potential

The evolution of integrated charging ecosystems, combining hardware, software, and energy management solutions, offers strong growth opportunities for the market. Comppppanies are focusing on creating seamless charging experiences through smart grid integration, vehicle-to-grid capabilities, and digital platforms. These ecosystems enhance energy efficiency and optimize charging infrastructure utilization. As 800v platforms align well with high-power charging solutions, their adoption is expected to increase.

- For instance, in February 2025, BMW unveiled its sixth-generation eDrive technology featuring advanced 800V architecture for the Neue Klasse platform. The innovation delivers 30% faster charging and increased range, integrating high-voltage batteries and silicon carbide components to enhance efficiency, performance, and scalability across future electric vehicle models.

MARKET CHALLENGES

Technical Complexity in System Integration Poses Operational Challenges

The implementation of 800V architecture involves significant technical complexity, posing challenges for market players. Integrating high voltage platforms components requires advanced engineering capabilities, stringent safety standards, and specialized manufacturing processes. Compatibility issues with existing 400V infrastructure and components can also complicate system design. Additionally, workforce skill gaps in handling high-voltage systems may hinder efficient deployment. These challenges can slow the pace of market growth and highlight the need for continuous innovation and expertise development to enable successful large-scale adoption of 800V EV systems.

Segmentation Analysis

By Vehicle Type

High Adoption of Premium EV Platforms Boosts Passenger Vehicles Segment Growth

Based on vehicle type, the market is segmented into passenger vehicles, LCVs, and HCVs.

The passenger vehicles segment dominates the market due to high adoption of advanced EV technologies and strong presence of premium electric models utilizing 800V architecture. Leading automakers are integrating high-voltage systems in passenger EVs to enhance charging speed, driving range, and performance. Increasing consumer demand for fast-charging, high-efficiency vehicles, along with growing availability of premium EV models, continues to support widespread adoption and strengthens the segment’s overall market share globally.

- For instance, in February 2026, Polestar outlined plans to launch four new EV models, including high-performance vehicles with up to 650 kW output and extended driving range. The expansion strategy strengthens its electric portfolio, supporting increased adoption of advanced EV architectures and enhancing competitiveness in the premium electric vehicle market.

The HCVs segment is projected to grow at a CAGR of 32.0% over the forecast period. Rising electrification of long-haul and heavy-duty transport, along with demand for ultra-fast charging and high-power output, is accelerating the adoption of 800V systems in this segment.

To know how our report can help streamline your business, Speak to Analyst

By Component Type

High Cost Contribution and Continuous advancements in Cell Chemistry Strengthens Battery Pack Segment Growth

Based on component type, the market is segmented into battery pack, power electronics, electric motor, charging system, and thermal management systems.

The battery pack segment holds the largest 800V electric vehicle architecture market share due to its critical role as the primary energy storage unit and its significant contribution to overall vehicle cost. In 800V architectures, advanced battery technologies systems are designed to support higher voltage levels, enabling faster charging and improved energy efficiency. Continuous advancements in cell chemistry, packaging, and energy density further drive demand, reinforcing the segment’s dominance in the market.

- For instance, in February 2026, BYD launched the ATTO 3 EVO featuring 800V architecture, enabling DC fast charging up to 220 kW and 10-80% charging in 25 minutes. Equipped with a 74.8 kWh battery, the model enhances performance and range, supporting broader adoption of high-voltage EV systems.

The charging system segment is expected to grow at a CAGR of 31.2% during the forecast period. Increasing deployment of ultra-fast charging infrastructure and rising demand for reduced charging time are accelerating the adoption of high-voltage compatible charging systems.

By Propulsion Type

Full Electrification Shift and High-Voltage Compatibility Accelerate the BEVs Segment Growth

Based on propulsion type, the market is segmented into BEVs and PHEVs.

BEVs dominates the market and is also the fastest-growing segment due to its complete reliance on electric powertrains, making it highly compatible with 800V architecture. Automakers are prioritizing BEV market for next-generation platforms to achieve faster charging, extended range, and improved efficiency. Strong policy support, expanding charging infrastructure, and increasing consumer preference for zero-emission vehicles further drive market demand, reinforcing BEVs’ leading market share during the forecast period.

- For instance, in March 2026, Mercedes-Benz unveiled the VLE electric van featuring an 800V architecture and a 115 kWh battery pack, delivering up to 700 km range. The model supports 300 kW fast charging and highlights the expansion of high-voltage EV systems into luxury multi-purpose vehicle segments.

The PHEVs segment is projected to grow at a CAGR of 21.9% over the forecast period. Gradual electrification transition and demand for flexible powertrain solutions continue to support steady adoption, particularly in regions with developing charging infrastructure.

By Power Output Level

Balanced Performance Requirements and Wide Vehicle Applicability Sustain 150-300 kW Segment Demand

Based on power output level, the market is segmented into below 150 kW, 150-300 kW, and above 300 kW.

The 150-300 kW segment dominates the market due to its optimal balance between performance, efficiency, and cost, making it suitable for a wide range of passenger electric 800V vehicles. This power range supports enhanced driving dynamics and compatibility with 800V systems without significantly increasing system complexity. Automakers widely adopt this segment across mid-range and premium EVs, contributing to strong market demand and stable market share across global markets.

- For instance, in December 2025, Volkswagen introduced the ID.UNYX 08 electric crossover with 800V architecture, offering up to 730 km range and a 230 kW power output. Co-developed with XPeng, the model supports ultra-fast charging above 300 kW, enhancing performance and efficiency in next-generation EV platforms.

The above 300 kW segment is projected to grow at a CAGR of 30.0% during the forecast period. Increasing demand for high-performance EVs, luxury vehicles, and heavy-duty applications is driving the adoption of higher power output systems.

800V Electric Vehicle Architecture Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific 800V Electric Vehicle Architecture Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the largest market share due to strong electric vehicle production and sales across China, Japan, and South Korea. Government incentives, large-scale battery manufacturing, and rapid expansion of charging infrastructure support widespread adoption of advanced EV technologies. Leading automakers in the region are actively deploying 800V architectures to enhance vehicle performance and efficiency. Additionally, increasing urbanization and rising consumer demand for high-performance electric vehicles continue to drive market growth and strengthen regional dominance during the market forecast period.

- For instance, in April 2026, Nissan launched the NX8 SUV in China, featuring an advanced 800V silicon carbide platform, enabling ultra-fast charging from 10% to 80% in 12 minutes. The model offers up to 650 km electric range and up to 250 kW power output, highlighting advancements in high-voltage EV performance and efficiency.

- According to the IEA, China continued to lead the global market, with electric vehicles accounting for nearly half of total car sales in 2024. More than 11 million electric cars were sold in the country, exceeding global sales from just two years prior. This sustained growth has resulted in approximately one in every ten cars on Chinese roads now being electric.

China 800V Electric Vehicle Architecture Market

The Chinese market is estimated to reach around USD 3.25 billion by 2026, accounting for roughly 45.6% of global revenues. Strong EV production scale, government incentives, and rapid charging infrastructure expansion drive market growth and strengthen domestic OEM leadership.

Japan 800V Electric Vehicle Architecture Market

The Japanese market is estimated to touch around USD 0.18 billion by 2026, accounting for roughly 2.6% of global revenues. Growth in the country is supported by strong technological innovation, a continued focus on energy efficiency, and the development of premium EVs.

India 800V Electric Vehicle Architecture Market

The Indian market is estimated to reach around USD 0.07 billion by 2026, accounting for roughly 1.1% of global revenues. Rapid electrification initiatives, policy support, and infrastructure expansion accelerate market growth and future adoption potential.

Europe

Europe represents the second-largest market, supported by stringent emission regulations and a strong policy push toward electrification. Countries such as Germany, Norway, and the Netherlands are leading in EV adoption and infrastructure development. Automakers in the region are focusing on premium electric vehicles equipped with 800V systems to meet efficiency and performance expectations. High consumer awareness, well-established charging networks, and continuous technological advancements contribute to sustained market demand and reinforce region’s significant market share.

- For instance, in January 2024, Stellantis unveiled its STLA Large platform supporting both 400V and 800V architectures, enabling up to 800 km range and ultra-fast charging. Designed for multiple vehicle types, the flexible platform enhances performance, efficiency, and scalability, supporting global EV expansion strategies.

Germany 800V Electric Vehicle Architecture Market

The Germany market is estimated to touch around USD 0.68 billion by 2026, accounting for roughly 9.5% of global revenues. Strong premium automotive base, innovation in EV platforms, and charging infrastructure advancements drive sustained market demand.

U.K. 800V Electric Vehicle Architecture Market

The U.K. market is estimated to reach around USD 0.45 billion by 2026, accounting for roughly 6.3% of global revenues. Government electrification targets, EV adoption incentives, and expanding fast-charging networks support consistent market growth.

North America

North America is the third-largest market, driven by the increasing adoption of electric vehicles in the U.S. and Canada. Strong investments by automakers and technology companies in next-generation EV platforms are supporting the deployment of 800V architectures. Expansion of fast-charging networks and rising demand for high-performance electric vehicles further contribute to market growth. Additionally, favorable government incentives and growing consumer awareness toward sustainable mobility solutions continue to boost regional market demand during the forecast period.

- For instance, in September 2023, Kia America unveiled the EV9 electric SUV featuring an advanced 800V E-GMP architecture, enabling ultra-fast charging from 10% to 80% in around 25 minutes. The model integrates a high-capacity battery, long driving range, bidirectional charging capability, and advanced power electronics, enhancing efficiency, performance, and real-world usability for next-generation electric mobility.

U.S. 800V Electric Vehicle Architecture Market

The U.S. market is estimated to reach around USD 0.71 billion by 2026, accounting for roughly 9.9% of global revenues. Strong OEM investments, rising demand for high-performance EVs, and infrastructure expansion drive market growth.

South America

South America is projected to be the fastest-growing region, with a CAGR of 37.1% during the forecast period. Growth is driven by increasing government focus on emission reductions and the gradual electrification of transportation across key economies. Expanding urban mobility needs and rising investments in EV infrastructure are supporting the adoption of advanced vehicle technologies. Although currently at a nascent stage, improving economic conditions and growing awareness of electric mobility are expected to significantly boost market growth and create new opportunities across the region.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth, driven by increasing diversification toward sustainable mobility and clean energy adoption. Countries such as the UAE and Saudi Arabia are investing in EV infrastructure and promoting electric vehicle adoption through strategic initiatives. Growing focus on reducing dependence on fossil fuels and enhancing energy efficiency is encouraging the introduction of advanced EV technologies. Although adoption remains gradual, improving infrastructure and supportive policies are expected to drive long-term market growth.

- For instance, in September 2025, Zeekr launched the 7X electric SUV in the UAE, featuring an advanced 800V architecture enabling ultra-fast charging from 10% to 80% in 10-16 minutes. Equipped with up to 103 kWh battery and high-performance output, the model enhances efficiency, range, and premium EV capabilities.

COMPETITIVE LANDSCAPE

Key Industry Players

Industry Participants Are Investing in Silicon Carbide Technologies to Gain Competitive Edge

The market is moderately consolidated, with a mix of established automakers and emerging EV manufacturers competing through advanced high-voltage platform development and performance optimization. Key players such as Porsche AG, Hyundai Motor Company, Kia Corporation, Lucid Motors, Tesla, and BYD focus on ultra-fast charging capabilities, efficient power electronics, and integrated vehicle architectures. Companies are investing in silicon carbide technologies, in-house platform development, and strategic collaborations to gain competitive edge in the market.

- For instance, in September 2025, Hyundai announced plans to launch India’s first locally designed EV and expand its Pune plant capacity by 250,000 units by 2030. The strategy strengthens India’s role as a global EV hub, supporting localized production, electrification growth, and next-generation vehicle technologies, including high-voltage architectures and software-defined manufacturing capabilities.

LIST OF KEY 800V ELECTRIC VEHICLE ARCHITECTURE COMPANIES PROFILED

- Porsche AG (Germany)

- Hyundai Motor Company (South Korea)

- Kia Corporation (South Korea)

- Lucid Motors, Inc. (U.S.)

- Tesla, Inc. (U.S.)

- BYD Company Ltd. (China)

- Mercedes-Benz Group AG (Germany)

- BMW AG (Germany)

- Audi AG (Germany)

- Volkswagen AG (Germany)

- NIO Inc. (China)

- XPeng Inc. (China)

- Stellantis N.V. (Netherlands)

- Bosch (Robert Bosch GmbH) (Germany)

- Continental AG (Germany)

- BorgWarner Inc. (U.S.)

- Magna International Inc. (Canada)

- STMicroelectronics N.V. (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Porsche introduced its Cayenne Electric featuring an advanced 800V architecture, enabling ultra-fast charging up to 400 kW and over 600 km range. The model integrates a high-voltage battery, predictive thermal management, and dual cooling systems, enhancing efficiency, performance, and real-world usability. The development highlights growing innovation in high-voltage EV platforms, supporting faster charging and improved energy management capabilities globally.

- October 2025: Changan announced the Qiyuan A06 electric sedan is set for launch in China. The model features an advanced 800V SiC platform with 6C fast charging capability, enabling 30-80% charging in around 9 minutes. It also includes LiDAR integration and extended driving range, highlighting advancements in high-performance EV architecture.

- July 2025: Mercedes-Benz launched the CLA EV in China, featuring an advanced 800V-capable MMA platform, enabling fast charging and extended range up to 866 km. Powered by a 200 kW motor, the model enhances efficiency, performance, and next-generation electric mobility capabilities.

- November 2024: Magna secured its first award for its Dedicated Hybrid Drive Duo system featuring an advanced 800V architecture. The solution integrates dual e-motors and multi-speed transmission, enhancing efficiency, performance, and scalability across vehicle segments, supporting next-generation hybrid electrification strategies.

- February 2024: Zeekr introduced the updated Zeekr 001 featuring an advanced 800V architecture and Qualcomm 8295 chipset, enabling faster charging, improved energy efficiency, and enhanced computing capabilities. The model supports high-performance electric mobility with upgraded power electronics, intelligent systems, and next-generation digital cockpit integration.

- March 2023: Porsche Engineering highlighted advanced EV platform strategies, emphasizing scalable architectures such as PPE that reduce development time and costs. These platforms enhance flexibility, support high-performance 800V systems, and enable efficient production of multiple electric vehicle models.

REPORT COVERAGE

The global 800V electric vehicle architecture market analysis provides an in-depth study of the market size & forecast by all the market segments included in the market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on market intelligence, technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 28.5% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, By Component Type, By Propulsion Type, By Power Output Level, and By Region |

| By Vehicle Type |

|

| By Component Type |

|

| By Propulsion Type |

|

| By Power Output Level |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.98 billion in 2025 and is projected to reach USD 52.80 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 2.87 billion.

The market is expected to exhibit a CAGR of 28.5% during the forecast period.

The passenger vehicles segment leads the market in terms of vehicle type.

Rising demand for high-performance electric vehicles is the key factor driving market growth.

Major players in the market include Porsche AG, Hyundai Motor Company, Kia Corporation, Lucid Motors, Tesla, and BYD.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us