ADAS Calibration Services Market Size, Share & Industry Analysis, By Calibration Type (Static Calibration, Dynamic Calibration, & Combined), By Vehicle Type (Passenger Cars, LCVs, & HCVs), By Service Provider Type (Authorized OEM Dealerships, Independent Workshops & Collision Repair Centers, and Specialized ADAS Calibration Centers), By ADAS Sensor Type (Camera Sensors, Radar Sensors, LiDAR Sensors, & Ultrasonic Sensors), By End-use (Collision Repair & Body Shop Services, Windshield Replacement & Glass Repair, Suspension, & Others), and Regional Forecast, 2026-2034

ADAS Calibration Services Market Size and Future Outlook

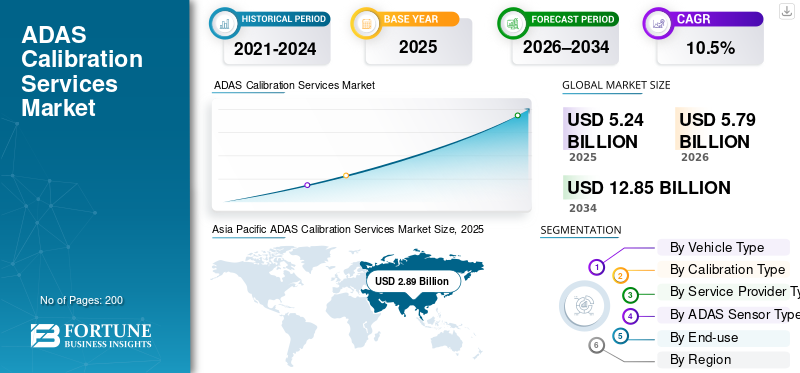

The global ADAS calibration services market size was valued at USD 5.24 billion in 2025. The market is projected to grow from USD 5.79 billion in 2026 to USD 12.85 billion by 2034, exhibiting a CAGR of 10.5% during the forecast period. Asia Pacific dominated the ADAS calibration services market with a market share of 55.15% in 2025.

ADAS calibration services are professional procedures that precisely adjust, test, and verify vehicle camera, radar, LiDAR, and sensor systems to restore accuracy after repairs, replacements, or mechanical disturbances. Market drivers include rising ADAS-equipped vehicle parc, increasing collision repairs, mandatory safety regulations, windshield replacements, growing sensor complexity, and OEM requirements for precise calibration to ensure safety, compliance, and system reliability.

Major players in the market include Bosch, Continental, Hunter Engineering, and Hella Gutmann, competing through advanced calibration systems, software accuracy, automation, OEM coverage, and compliance with evolving vehicle safety standards.

Download Free sample to learn more about this report.

ADAS CALIBRATION SERVICES MARKET TRENDS

Shift Toward Automated, Software-Driven, and Multi-Sensor Calibration Solutions is a Key Market Trend

One of the ADAS calibration services market trends is a shift toward automated calibration systems that reduce manual intervention and human error. Advanced software-driven platforms integrate camera, radar, LiDAR, and ultrasonic sensor calibration within a single workflow. AI-enabled diagnostics, cloud-based updates, and digital documentation are becoming standard to support traceability and regulatory compliance. This trend improves calibration accuracy, reduces service time, and enhances throughput for high-volume workshops and dealerships.

- In January 2023, Continental presented a modular multi-sensor solution for autonomous trucks, integrating radar, LiDAR, cameras, and computing units to enable scalable Level 4 autonomy, improve redundancy, and support safe, reliable automated driving in commercial vehicle applications.

MARKET DYNAMICS

MARKET DRIVERS

Rising Penetration of ADAS-Equipped Vehicles to Drive Service Demand

The growing penetration of Advanced Driver Assistance Systems (ADAS) features across passenger and commercial vehicles is a primary driver for ADAS calibration services market growth. Even minor collisions, windshield replacements, suspension repairs, or wheel alignments can disrupt the ADAS sensors’ accuracy, necessitating recalibration. As automakers increasingly standardize ADAS across mid- and entry-level vehicles, the addressable service base expands rapidly. Regulatory emphasis on functional safety and OEM repair guidelines further ensures recurring calibration requirements throughout the vehicle lifecycle.

- In January 2026, Ford announced it aims to launch its first Level 3 eyes-off autonomous driving system by 2028, debuting on a new EV platform after a 2027 launch. The hands-free system integrates ADAS, lidar, and in-house software to expand advanced driver assistance accessibility across more affordable vehicles.

MARKET RESTRAINTS

High Capital Investment and Skilled Labor Dependency to Restrain Market Growth

ADAS calibration services require a significant upfront investment in calibration frames, targets, diagnostic software, and workshop space that meet strict environmental conditions. Additionally, accurate calibration depends on highly trained technicians, increasing labor costs and limiting scalability. Small independent workshops, particularly in price-sensitive markets, often delay adoption due to uncertain return on investment. These financial and operational barriers restrict uniform market penetration across regions and service provider types.

MARKET OPPORTUNITIES

OEM Collaboration and Certified Calibration Networks to Create New Growth Opportunities

OEMs increasingly prefer certified, standardized calibration networks to ensure consistent repair quality and liability compliance. This creates opportunities for service providers offering OEM-approved calibration solutions, mobile calibration units, and cloud-connected diagnostic platforms. Partnerships between ADAS equipment manufacturers, dealerships, insurers, and collision repair chains can expand service coverage and recurring revenue streams. As vehicle software complexity rises, subscription-based calibration software and remote diagnostics further enhance the long-term opportunity.

- In October 2025, Ready AutoGlass & Windshield Repair expanded its ADAS calibration services to support modern vehicle safety systems, adding advanced camera and radar recalibration capabilities after windshield replacements to ensure OEM compliance, safety accuracy, and reliable ADAS performance across newer vehicle models.

MARKET CHALLENGES

Complex Sensor Architectures and Model Variability to Challenge Service Standardization

A major challenge lies in the increasing diversity of sensor architectures across vehicle models and brands. Variations in mounting positions, software protocols, and calibration procedures limit standardization and increase operational complexity. Frequent model refreshes and software updates require continuous equipment upgrades and technician retraining. For multi-brand service centers, maintaining broad vehicle coverage without compromising accuracy remains a persistent technical and cost-related challenge.

Download Free sample to learn more about this report.

Segmentation Analysis

By Calibration Type

Standardized Workshop Environments and OEM Repair Protocols to Sustain Static Calibration Demand

Based on calibration type, the market is segmented into static calibration, dynamic calibration, and combined.

Static calibration dominates the market due to its alignment with OEM repair procedures requiring controlled workshop conditions, fixed targets, and precise vehicle positioning. It is widely used after windshield replacements, collision repairs, and sensor replacements. High accuracy, repeatability, and compatibility with multi-brand vehicles make static calibration the preferred choice for dealerships and independent workshops, ensuring consistent service volumes and predictable workflows.

- In August 2025, Mitchell announced the launch of Mitchell Diagnostics Sync, a cloud-based solution that integrates ADAS diagnostics, pre- and post-scan data, and repair workflows, enabling collision repair shops to improve accuracy, documentation, and compliance with OEM diagnostic and calibration requirements.

Combined calibration is the fastest-growing segment, expanding at an 11.4% CAGR during the forecast period, as advanced ADAS systems increasingly require both workshop-based and on-road validation. Growing sensor fusion, tighter OEM tolerances, and real-world performance verification drive adoption rates.

By Vehicle Type

High ADAS Penetration and Frequent Repair Incidence to Propel Passenger Cars Segmental Dominance

Based on vehicle type, the market is segmented into passenger cars, LCVs, and HCVs.

The passenger cars segment dominates the market due to the large global passenger vehicle parc and high penetration of camera- and radar-based safety systems. Frequent windshield replacements, minor collisions, suspension repairs, and wheel alignments regularly trigger calibration needs. Urban driving conditions, dense traffic, and widespread personal vehicle ownership further increase recalibration frequency, ensuring consistent service demand across authorized dealerships and independent workshops.

- According to OICA data, global passenger car sales reached approximately 56.9 million units in 2024, increasing from about 55.6 million units recorded in 2023.

The LCVs segment is the fastest growing, registering a CAGR of 11.0% during the forecast period, driven by expanding e-commerce, last-mile delivery, and fleet electrification. Fleet operators prioritize ADAS uptime, boosting demand for frequent, precise sensor recalibration to ensure safety, compliance, and operational continuity.

By Service Provider Type

Broad Repair Footprint and High Post-Collision Volumes to Sustain Independent Workshop Market

By service provider type, the market is divided into authorized OEM dealerships, independent workshops & collision repair centers, and specialized ADAS calibration centers.

Independent workshops & collision repair centers segment dominates the market. This is due to their extensive global footprint and high exposure to post-accident repairs. These facilities routinely handle windshield replacements, body repairs, suspension work, and alignments that trigger mandatory ADAS recalibration. Competitive pricing, faster turnaround times, and growing investments in multi-brand calibration equipment reinforce their dominant share across mature and emerging automotive markets.

- In August 2025, Revv introduced an AI-powered solution that helps collision repairers instantly identify all required ADAS calibration procedures through VIN-specific reports and OEM documentation, streamlining workflow, reducing missed calibrations, and improving repair accuracy in the collision repair industry.

Specialized ADAS calibration centers segment is the fastest-growing, expanding at a CAGR of 11.7% over the forecast period, driven by complex sensor architectures, OEM certification programs, and insurer-backed quality standards. Their focus on accuracy, controlled environments, and advanced automation supports widespread adoption.

By ADAS Sensor Type

Widespread Front-View Deployment and Cost-Effective Integration to Drive Camera Sensor Segment Growth

By ADAS sensor type, the market is categorized into camera sensors, radar sensors, LIDAR sensors, and ultrasonic sensors.

Camera sensors dominate through the ADAS calibration services market forecast period. The growth is due to their widespread deployment in features such as lane keeping assist, lane departure warning, automatic emergency braking, traffic sign recognition, and assistance and adaptive cruise control. Cameras are highly sensitive to windshield replacements, minor impacts, and alignment changes, leading to frequent recalibration needs. Their cost-effective integration across mass-market vehicles ensures consistently high service volumes across dealerships and independent repair facilities.

- In May 2024, Morpho, Inc. launched the Morpho Visual Calibrator, an AI-based driving calibration technology that uses in-vehicle video to infer camera positional relationships, streamlining camera calibration, reducing factory facility requirements, and boosting development efficiency for next-generation vehicle imaging systems.

LiDAR sensors represent the fastest-growing segment, expanding at a CAGR of 12.7% during the forecast period, driven by their increasing adoption in premium vehicles, autonomous testing fleets, and advanced driver assistance systems requiring high-precision environmental mapping and calibration accuracy.

By End-use

To know how our report can help streamline your business, Speak to Analyst

High Post-Accident Recalibration Frequency to Augment Collision Repair Segment Growth

By end-use, the market is segmented into collision repair & body shop services, windshield replacement & glass repair, suspension, wheel alignment & chassis repairs, and routine diagnostics & software updates.

Collision repair & body shop services segment holds the largest ADAS calibration services market share, as even low-speed impacts, panel replacements, and structural repairs can disrupt sensor alignment. OEM repair procedures and insurer mandates increasingly require mandatory recalibration after collision repairs. High accident rates, growing ADAS penetration, and insurance-driven quality standards ensure consistent calibration demand from body shops across both passenger and commercial vehicle segments.

- In December 2025, Karl Malone’s Body & Paint expanded its collision repair services to include ADAS recalibration and safety system checks, enhancing vehicle safety by ensuring proper sensor alignment after body repairs and windshield replacements. This upgrade aims to improve repair quality and customer confidence in advanced driver assistance systems.

Routine diagnostics & software updates are the fastest-growing end-use segment in the market, expanding at a CAGR of 13.8% during the forecast period, driven by software-defined vehicles, over-the-air updates, and proactive sensor health checks aimed at maintaining ADAS accuracy and compliance.

ADAS Calibration Services Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific ADAS Calibration Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates and is the fastest-growing ADAS calibration services market, driven by high vehicle production volumes, rapid ADAS penetration, and expanding middle-class vehicle ownership. Rising accident rates in dense urban traffic, growing collision repair infrastructure, and increasing regulatory focus on vehicle safety are accelerating recalibration demand. Strong growth in China, Japan, South Korea, and India, alongside expanding independent workshops and OEM service networks, supports sustained regional expansion at the highest CAGR.

- In October 2025, ZF and Horizon Robotics announced plans to jointly launch Level 3 ADAS solutions in China, combining ZF’s vehicle control and sensing expertise with Horizon’s AI chips to enable scalable, cost-efficient advanced driving functions for Chinese automakers.

China ADAS Calibration Services Market

The China market in 2026 is estimated at around USD 1.87 billion, accounting for roughly 32.4% of global revenues. China dominates the Asia Pacific region. The demand in the country is driven by rapid ADAS penetration, high accident repair volumes, expanding EV parc, mandatory calibration regulations, and aggressive investments by OEM-authorized workshops and independent service networks nationwide.

Japan ADAS Calibration Services Market:

The Japan market in 2026 is estimated at around USD 0.48 billion, accounting for roughly 8.3% of global revenues. The country growth remains steady due to advanced vehicle safety adoption, strict inspection standards, aging vehicle fleet, strong OEM influence, and high demand for precision calibration services within certified dealer workshops.

India ADAS Calibration Services Market:

The India market in 2026 is estimated at around USD 0.37 billion, accounting for roughly 6.3% of global revenues. India’s market growth is supported by rising ADAS-equipped vehicle sales, urban accident rates, expanding organized aftermarket, improving insurance penetration, and increasing awareness of sensor recalibration following post-collision repairs.

Europe

Europe represents the second-largest market, growing at a CAGR of 10.2% during the forecast period, supported by stringent safety regulations and widespread adoption of advanced driver assistance systems. Mandatory calibration requirements following windshield replacement and collision repairs drive steady demand. A mature network of OEM dealerships, certified body shops, and insurer-backed repair standards ensures consistent service volumes. High penetration of premium vehicles with complex ADAS architectures further reinforces calibration intensity across the region.

- In May 2024, LeddarTech unveiled its LeddarNavigator demo car and European roadshow, showcasing AI-based sensor fusion and perception software for ADAS and autonomous driving, enabling scalable deployment across camera, radar, and LiDAR systems for OEMs and Tier-1 suppliers.

Germany ADAS Calibration Services Market

The Germany market in 2026 is estimated at around USD 0.29 billion, accounting for roughly 4.9% of global revenues. Premium vehicle dominance, stringent safety regulations, high ADAS content per vehicle, a strong collision repair ecosystem, and continuous technological upgrades across independent and OEM workshops fuel market growth in the country.

U.K. ADAS Calibration Services Market

The U.K. market in 2026 is estimated at around USD 0.06 billion, accounting for roughly 1.1% of global revenues. Market expansion in the U.K. is supported by insurance-driven repairs, increasing ADAS penetration, regulatory compliance needs, and growing reliance on specialized calibration centers amid rising vehicle complexity.

North America

North America is the third-largest market in ADAS calibration services, driven by a high concentration of ADAS equipped vehicles, elevated repair costs, and strong insurance involvement in post-collision recalibration. Strict OEM repair procedures, widespread windshield replacements, and increasing sensor complexity sustain calibration demand.

- In July 2024, SEMA announced the introduction of a landmark ADAS bill in the U.S. Congress aimed at protecting consumer demand for advanced safety features, and independent repair access by ensuring transparency, standardized calibration procedures, and fair access to ADAS diagnostic and calibration data for aftermarket service providers.

U.S. ADAS Calibration Services Market

The U.S. market in 2026 is estimated at around USD 0.72 billion, accounting for roughly 12.4% of global revenues. The U.S. dominates the North American market due to high ADAS penetration, strong insurance-driven repair compliance, frequent windshield replacements, and the widespread presence of certified collision repair centers and advanced diagnostic infrastructure.

Rest of the World

The rest of the world market is driven by gradual ADAS adoption, improving road safety regulations, and expanding aftermarket repair infrastructure across Latin America, the Middle East, and Africa. Rising vehicle parc, increasing urbanization, and growing awareness of calibration requirements support steady regional market growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Automation, Software Accuracy, and Certified Service Expansion Define Competitive Intensity

The ADAS calibration services market is moderately fragmented, with competition spread across diagnostic equipment manufacturers, calibration solution providers, and specialized service operators. Key players, including Bosch, Continental, Hunter Engineering, and Hella Gutmann, compete through high-precision calibration systems, software accuracy, OEM coverage, and multi-sensor compatibility. Competitive differentiation increasingly focuses on automation, cloud-enabled diagnostics, mobile calibration units, and OEM certification.

- In June 2024, Lexus approved the Tru-Point ADAS Calibration System for service use across the U.S., enabling certified collision repair facilities to perform OEM-compliant camera and radar calibrations, supporting repair accuracy, safety assurance, and standardized ADAS recalibration procedures nationwide.

LIST OF KEY ADAS CALIBRATION SERVICES COMPANIES PROFILED

- Bosch Automotive Service Solutions (Germany)

- Continental Automotive Services (Germany)

- ZF Aftermarket (ZF Friedrichshafen AG) (Germany)

- DENSO Corporation (Japan)

- Valeo Service (France)

- Magneti Marelli (Marelli Aftermarket) (Italy)

- Hunter Engineering Company (U.S.)

- Snap-on Incorporated (U.S.)

- HELLA Gutmann Solutions (Forvia HELLA) (Germany)

- AVL List GmbH (Austria)

- HORIBA Automotive Test Systems (Japan)

- Belron International (U.K.)

- SGS Automotive Services (Switzerland)

- TÜV SÜD Automotive Service (Germany)

- Autel (China)

KEY INDUSTRY DEVELOPMENTS

- January 2026: ZF announced that its ProAI automotive supercomputer, combined with Qualcomm’s Snapdragon Ride platform, forms a flexible foundation for next-generation ADAS systems, enabling scalable AI processing, sensor fusion, and software-defined vehicle architectures across multiple automation levels.

- December 2025: ETAS collaborated with Microsoft to bring its flagship automotive calibration tools, ETAS Calibration Suite, Data Operator, EATB, and ETAS ASCMO, to the Microsoft Azure Marketplace, enabling cloud-based workflows that accelerate automotive software development and early validation.

- October 2025: Valeo partnered with Capgemini to develop an integrated ADAS system testing framework, combining Valeo’s sensing technologies with Capgemini’s digital engineering expertise to accelerate validation, simulation, and deployment of advanced driver assistance functions for automakers.

- October 2025: Valeo’s LiDAR technology received two industry awards recognizing its precision, reliability, and contribution to advanced ADAS and automated driving, including improved sensor accuracy and calibration robustness essential for consistent performance across diverse driving and environmental conditions.

- September 2025: Bosch Diagnostics released ADS X software updates, versions 6.15 and 7.0, enhancing diagnostic speed, ADAS calibration workflows, vehicle coverage, and cloud connectivity, enabling automotive technicians to improve repair accuracy, efficiency, and compatibility with newer software-defined and ADAS-equipped vehicles.

- September 2025: DENSO and onsemi strengthened their long-term partnership to secure advanced power semiconductor supply for automotive applications, supporting ADAS, electrification, and software-defined vehicles through improved chip availability, performance optimization, and resilient supply chains.

- September 2025: Hunter Engineering partnered with GreatAmerica Financial Services to offer flexible financing for its ADAS alignment and calibration systems, helping repair shops lower upfront costs, accelerate adoption of advanced calibration equipment, and meet growing OEM and insurer requirements for ADAS-equipped vehicles.

- January 2025: Rivian’s Certified Collision Network approved the Autel IA900 ADAS Calibration System, enabling certified repair centers to perform OEM-compliant camera, radar, and sensor calibrations, supporting accurate repairs, safety assurance, and standardized ADAS service procedures for Rivian electric vehicles.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, By Calibration Type, By Service Provider Type, By ADAS Sensor Type, By End-use, and By Region |

| By Vehicle Type |

|

| By Calibration Type |

|

| By Service Provider Type |

|

| By ADAS Sensor Type |

|

| By End-use |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.24 billion in 2025 and is projected to reach USD 12.85 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 2.89 billion.

The market is expected to exhibit a CAGR of 10.5% during the forecast period.

The passenger cars segment leads the market in terms of vehicle type.

Rising penetration of ADAS-equipped vehicles is the key factor driving the market.

Key players in the market include Bosch, Continental, Hunter Engineering, and Hella Gutmann, among others.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us