Adhesion Barrier Market Size, Share & Industry Analysis, By Product Type (Synthetic [Hyaluronic Acid, Regenerated Cellulose, and Others] and Natural), By Formulation (Film/Mesh, Gel, and Liquid), By Absorbability (Absorbable and Non-absorbable), By Application (General Surgery, Gynecological Surgery, Cardiovascular Surgery, Orthopedic Surgery, and Others), By End User (Hospitals & ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Adhesion Barrier Market Size and Future Outlook

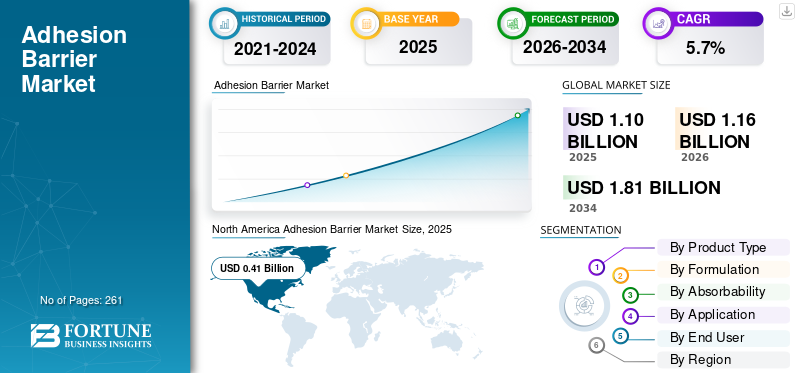

The global adhesion barrier market size was valued at USD 1.10 billion in 2025 and is projected to grow from USD 1.16 billion in 2026 to USD 1.81 billion by 2034, exhibiting a CAGR of 5.7% during the forecast period. North America dominated the adhesion barrier market with a market share of 37.27% in 2025.

Adhesion barriers are temporary biocompatible materials, including gels, films, or fabrics that are applied between tissue surfaces to prevent the formation of postoperative adhesions during surgical procedures among patients. They are typically composed of bioresorbable materials, including hyaluronic acid, carboxymethylcellulose, polyethylene glycol, and other polymeric compounds. The increasing prevalence of chronic disorders, rising surgical procedures, and the growing awareness about post-operative complications are resulting in an increasing adoption rate of these devices in the market. The aging population is further driving demand for surgical procedures, thereby increasing the adoption of these products in the market.

- For instance, according to the 2020 statistics published by the National Center for Biotechnology Information (NCBI), it was reported that approximately 310 million major surgical procedures are performed every year globally.

Additionally, the increasing integration of technological advancements in these products among the major companies, including Medtronic, Johnson & Johnson Services, Inc., among others, is further contributing to the demand for these devices in the market.

Download Free sample to learn more about this report.

ADHESION BARRIER MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.10 billion

- 2026 Market Size: USD 1.16 billion

- 2034 Forecast Market Size: USD 1.81 billion

- CAGR: 5.7% from 2026–2034

- North America dominated the adhesion barrier market with a 37.27% share in 2025.

- The absorbable segment held a 90.3% share in 2025.

- The film/mesh segment accounted for 51.0% share in 2025.

North America

North America reached USD 0.41 billion in 2025, supported by advanced surgical infrastructure and strong reimbursement policies.

Europe

The market is projected to reach USD 0.32 billion by 2026, driven by established healthcare systems and increasing adoption of adhesion barriers.

Asia Pacific

The market is projected to reach USD 0.30 billion by 2026, driven by rising surgical volumes and expanding healthcare infrastructure.

U.S.

The market is projected to reach USD 0.40 billion by 2026, fueled by high surgical volumes and advanced healthcare infrastructure.

Japan

The market is projected to reach USD 0.07 billion by 2026, supported by increasing surgical procedures and growing R&D activities.

Read More

Adhesion Barrier Market Trends

Rapid Technological Advancements in Adhesion Barrier Products to Fuel Demand

The rapid technological advancements in these products are significantly reshaping the market. The companies are focusing on the development and introduction of advanced bioresorbable polymers, biomaterials, and enhanced delivery products, including gels, films, and sprays, to improve product ease of application and effectiveness during surgery.

The modern products are designed to degrade naturally in the body after the prevention of tissue adhesion, which reduces the need for removal procedures, further minimizing complications among patients. Additionally, advancements, including synthetic products such as hyaluronic acid-based barriers, polyethylene glycol (PEG) hydrogels, and oxidized regenerated cellulose films, are enhancing biocompatibility, surgical handling, and adhesion prevention outcomes, thereby fueling the adoption rate of these products in the market.

- In March 2025, Fziomed, Inc., attended the 2025 IFSSH and IFSHT Triennial Global Hand Congress to highlight its Dynavisc Adhesion Barrier Gel, hosted by the American Society for Surgery of the Hand, American Society of Hand Therapists, and American Association for Hand Surgery.

Market Dynamics

Market Drivers

Download Free sample to learn more about this report.

Increasing Volume of Surgical Procedures to Boost Market Growth

The growing prevalence of chronic disorders, including cardiovascular disorders, neurological disorders, and others, is resulting in a growing number of surgical procedures among the patient population, subsequently fueling the demand for adhesion barrier products in the market.

- For instance, according to 2024 statistics published by the Centers for Disease Control & Prevention (CDC), about 1 in 20 adults has coronary artery disease in the U.S.

This, coupled with rising awareness among surgeons regarding the prevention of post‑operative adhesions and improvement in healthcare infrastructure, is boosting the adoption rate of these devices in the market. Therefore, the factors above, coupled with the growing emphasis of major players on introducing research and development activities to launch innovative devices, are further anticipated to drive their adoption rate, thereby supporting the global market size.

Other Prominent Drivers

- Growth in minimally invasive and laparoscopic surgical procedures is expected to drive market growth.

Market Restraints

High Cost Associated with Adhesion Barrier Products to Hamper Market Growth

The high cost of these products is one of the crucial factors hampering the growth of the global market. Adhesion barriers are mainly used as adjunct surgical devices, and their adoption depends on hospital budgets, reimbursement policies, and surgeon preference.

Furthermore, advanced products, including hyaluronic acid, polyethylene glycol (PEG), and oxidized regenerated cellulose, require complex manufacturing processes that increase device costs. The prioritization of essential surgical supplies over preventive products, among others, are some of the additional factors limiting the adoption rate of these products in the market.

- For instance, according to the data published by Synergy Surgical, the price of Baxter Genzyme Seprafilm Adhesion Barrier is around USD 2,999.0.

Market Opportunities

Growth of Ambulatory Surgical Centers (ASCs) Emerge as a Market Growth Opportunity

There is an increasing expansion of healthcare facilities in emerging nations, such as India, Mexico, and others. The increasing surgical procedures, expansion of healthcare infrastructure, and rising number of ambulatory surgical centers are consequently boosting the adoption of adhesion barrier products in healthcare settings. The preference for ambulatory surgical centers has increased for minimally invasive and elective surgical procedures due to their advantages, including lower procedural costs, shorter patient stays, faster turnover times, and reduced risk of hospital-acquired infections.

- According to 2025 statistics published by Definitive Healthcare, there are about 10,000 active ambulatory surgical centers in the U.S.

Market Challenges

Limited Healthcare Access in Developing Countries to Hamper Market Growth

There is a growing demand for elective and minimally invasive surgeries among the patient population. However, limited awareness about the adhesion barriers, shortage of advanced devices, limited healthcare spending, coupled with an insufficient reimbursement framework, especially in developing countries, is resulting in reduced access to healthcare facilities among the patient population.

Additionally, a limited number of healthcare settings and limited specialist surgeons, among others, are some of the crucial factors, resulting in the delayed surgical procedures among the patient population, especially in developing countries, including Mexico, and Brazil, among others.

- For instance, according to 2023 data published by The World Bank Group (WBG), about 4.5 billion people lack full access to essential health services globally.

Other Prominent Challenges

- Regulatory challenges for medical device approvals to hamper market growth.

SEGMENTATION ANALYSIS

By Product Type

Increasing Product Launches of Synthetic Products Led to Segment Dominance

Based on the product type, the market is classified into synthetic and natural. The synthetic segment is further divided into hyaluronic acid, regenerated cellulose, and others.

The synthetic segment held the largest revenue share in 2025. The growth is due to the increasing prevalence of chronic conditions among patients, resulting in a growing number of surgical procedures globally. This, along with the rising focus of key companies on launching synthetic products, is further anticipated to contribute to the global adhesion barrier market growth.

- For instance, according to 2024 data published by Science Direct, more than 1 million cardiac surgical procedures are estimated to occur yearly globally.

The natural segment is expected to grow at a CAGR of 5.0% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Formulation

Increasing Number of Film/Mesh Product Launches Led to Dominance of Segment

Based on formulation, the market is trifurcated into film/mesh, gel, and liquid.

The film/mesh segment dominated the global market in 2025 and accounted for 51.0% in 2025. The growth is owing to the increasing prevalence of hospital-acquired infections, resulting in a rising demand for film/mesh products, thereby contributing to the adoption rate of these devices in the market.

- For instance, in April 2025, Womed launched Womed Leaf, an intrauterine adhesion barrier film, to expand its product channel.

The segment of gel is set to flourish with a growth rate of 6.2% across the forecast period.

By Absorbability

Growing Product Introductions Led to Dominance of Absorbable Segment

Based on absorbability, the market is bifurcated into absorbable and non-absorbable.

The absorbable segment dominated the global market in 2025. By application, the absorbable segment held the share of 90.3% in 2025. The growth is owing to the rising prevalence of chronic conditions, including cardiovascular diseases, and gynecological diseases, among others. This is resulting in a rising number of surgical procedures globally, thereby contributing to the adoption rate of these devices in the market.

- For instance, in February 2022, Gunze Limited received approval to manufacture and sell TENALEAF, the sheet-type absorbable adhesion barrier made in Japan.

The segment of non-absorbable is set to flourish with a growth rate of 5.0% across the forecast period.

By Application

Growing Number of General Surgery Procedures Led to Dominance of Segment

Based on application, the market is segmented into general surgery, gynecological surgery, cardiovascular surgery, orthopedic surgery, and others.

The general surgery segment dominated the global market in 2025. By application, the general surgery segment accounted for 35.4% in 2025. The growth is due to the growing prevalence of chronic conditions such as cardiovascular diseases, neurovascular diseases, among others, resulting in an increasing volume of surgical procedures globally, thereby contributing to the adoption rate of these synthetic and natural adhesion barriers in the market.

- For instance, according to the 2020 data published by the National Center for Biotechnology Information (NCBI), about 18.3% procedures were for general surgery in 9,284 surgical procedures performed in 88,273 people in India.

The gynecological surgery segment is set to flourish with a growth rate of 6.2% across the forecast period.

By End User

Growing Number of Hospitals & ASCs Led to Segmental Dominance

Based on end user, the market is segmented into hospitals & ASCs, specialty clinics, and others.

The hospitals & ASCs segment dominated the market in 2025. The rising number of surgical procedures in hospitals, the development of healthcare infrastructure, the growing number of hospitals, among others, are some of the crucial factors contributing to the growth of the segment in the market. Furthermore, the segment is set to hold an 80.5% share in 2026.

- For instance, according to 2025 data published by Statistisches Bundesamt, there are approximately 1,874 hospitals in Germany.

In addition, specialty clinics’ end users are projected to grow at a 5.3% CAGR during the forecast period.

Adhesion Barrier Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Adhesion Barrier Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valued at USD 0.39 billion, and also took the leading share in 2025 with USD 0.41 billion. The advanced surgical infrastructure, adequate reimbursement policies, growing R&D activities, adoption of adhesion barriers, among others, are some of the factors supporting the growth of the segment in the market.

- For instance, according to 2024 data published by the Centers for Disease Control & Prevention (CDC), it was reported that the prevalence of inflammatory bowel disease (IBD) is estimated between 2.4 and 3.1 million among the patient population in the U.S.

U.S. Adhesion Barrier Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.40 billion in 2026, accounting for roughly 34.2% of global sales.

Europe

Europe is projected to record a growth rate of 5.0% in the coming years, which is the second highest among all regions, and reach a valuation of USD 0.32 billion by 2026. The strong adoption due to established healthcare systems is anticipated to support the market growth.

U.K. Adhesion Barrier Market

The U.K. market in 2026 is estimated at around USD 0.05 billion, representing roughly 3.9% of global revenues.

Germany Adhesion Barrier Market

Germany’s market is projected to reach approximately USD 0.05 billion in 2026, equivalent to around 4.7% of global sales.

Asia Pacific

The Asia Pacific market is estimated to reach USD 0.30 billion in 2026 and secure the position of the third-fastest growing region in the market. The rising surgical volumes in Asia Pacific countries, including China, South Korea, and others, are expected to support the growth of the market. In the region, India and China are both estimated to reach USD 0.05 billion and USD 0.10 billion, respectively, in 2026.

Japan Adhesion Barrier Market

The Japan market size in 2026 is estimated at around USD 0.07 billion, accounting for roughly 5.8% of global revenues. Japan has historically reported a relatively high volume of surgical procedures, with growing research and development activities among the key players in the industry.

China Adhesion Barrier Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.10 billion, representing roughly 9.0% of global sales.

India Adhesion Barrier Market

The Indian market size in 2026 is estimated at around USD 0.05 billion, accounting for roughly 4.0% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.06 billion in 2026. The growth is driven by increasing healthcare investments and surgical procedures in these regions. The Middle East & Africa are expected to grow due to expanding hospital infrastructure and growing surgical procedures in the region. In the Middle East & Africa, the GCC is set to reach a value of USD 0.02 billion in 2026.

South Africa Adhesion Barrier Market

The South Africa market is projected to reach around USD 0.01 billion in 2026, representing roughly 1.1% of global revenues.

Competitive Landscape

Key Industry Players

Growing Number of Collaborations to Support Key Player’s Dominance in Market

A broad and well-diversified product portfolio, combined with a strong focus on inorganic growth strategies such as partnerships and acquisitions, plays a crucial role in reinforcing the market leadership of major companies globally. These approaches continue to shape competitive dynamics within the market.

Companies such as Medtronic and Johnson & Johnson Services, Inc., are expected to remain prominent players in 2025. Their growing emphasis on strategic collaborations and acquisitions is expected to enhance their market position and expand their global footprint, ultimately boosting their adhesion barrier market share.

- For example, in March 2026, Medtronic partnered with GE Healthcare with an aim to enable healthcare providers to deliver smart and efficient care across hospital settings.

Additionally, other companies, including Baxter and several other emerging players, are gaining momentum. Their growth is largely driven by increased investments in research and development, enabling the introduction of innovative products and strengthening their presence in the competitive landscape.

List of Key Adhesion Barrier Companies Profiled

- Medtronic (U.S.)

- Baxter Corporation (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Womed (U.S.)

- Gunze Limited (Japan)

- Fziomed, Inc. (U.S.)

- Braun SE (Germany)

- SEIKAGAKU CORPORATION (Japan)

- Integra LifeSciences Corporation (U.S.)

- Terumo Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- December 2025: ARC Medical Inc., a player in surgical adhesion prevention innovation, announced the first deployment of IPCOAT liquid adhesion barrier product in a gynecologic surgery patient. This helped the company in strengthening its presence.

- September 2025: Womed received PMA approval for Womed Leaf Resorbable Adhesion Barrier for women suffering from moderate to severe intrauterine adhesions, a major cause for female infertility.

- July 2025: Fziomed, Inc., has granted De Novo classification and marketing authorization for Oxiplex gel, indicated for reducing postoperative leg pain and neurological symptoms in adult patients undergoing lumbar spine procedures.

- April 2025: Genewal and Hanmi Science held a press conference launching Guardix, the first domestically developed anti-adhesion barrier, with an aim to strengthen its product channel.

- October 2024: The American College of Surgeons gathered 100 experts across the world for its first Surgical Adhesions Improvement Project Summit, aimed to generate momentum in effective prevention, assessment, and treatment for surgical adhesions.

- July 2023: Seikagaku Corporation announced favorable results obtained in a pivotal study in Japan for SI-449, a surgical adhesion barrier, in the field of gastroenterological surgery.

- May 2020: Seikagaku Corporation announced the initiation of a pivotal study of SI-449, an adhesion barrier in Japan, with an aim to strengthen its product channel.

REPORT COVERAGE

The report provides a detailed global adhesion barrier market analysis and focuses on key aspects such as leading companies and market segmentation, including product type, formulation, absorbability, application, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Formulation, Absorbability, Application, End User, and Region |

| By Product Type |

|

| By Formulation |

|

| By Absorbability |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 1.10 billion in 2025 and is projected to reach USD 1.81 billion by 2034.

In 2025, North Americas market value stood at USD 0.41 billion.

Growing at a CAGR of 5.7%, the market will exhibit steady growth over the forecast period.

By product type, the synthetic segment is the leading segment in this market.

The introduction of novel adhesion barrier products is one of the major factors driving the markets growth.

Medtronic and Johnson & Johnson Services, Inc., are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of chronic disorders, the rising number of surgical procedures, among others, are some of the crucial factors anticipated to boost the adoption of these products worldwide.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us