Hemostats Market Size, Share & Industry Analysis, By Product (Active Hemostats, Passive Hemostats, Combination Hemostats, and Others), By Application (Trauma, Cardiovascular Surgery, General Surgery, Plastic Surgery, Orthopedic Surgery, Neurosurgery and Others), By End-User (Hospitals & ASCs, Tactical Combat Casualty Care Centers, and Others), and Regional Forecast, 2026-2034

Hemostats Market Size and Industry Overview

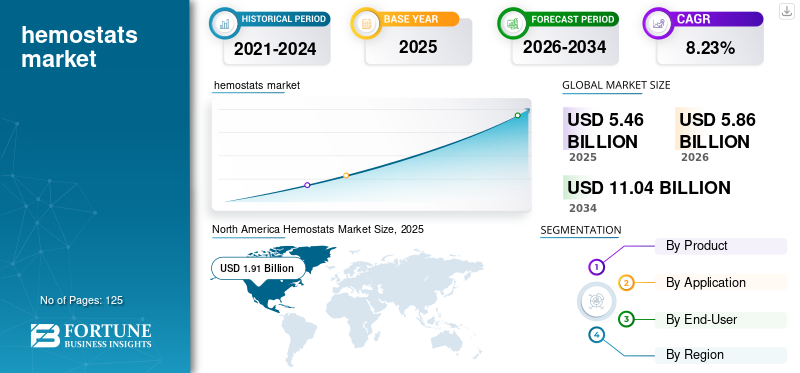

The global hemostats market size was valued at USD 5.46 billion in 2025 and is projected to grow from USD 5.86 billion in 2026 to USD 11.04 billion by 2034, exhibiting a CAGR of 8.23% during the forecast period (2026-2034). North America dominated the hemostats market with a market share of 34.96% in 2025.

The modern healthcare scenario is witnessing a trend of increasing incidence of several types of chronic diseases, such as cardiovascular disease, cancer, and occurrences of trauma and accidents. This has led to a substantial surge in the number of surgical procedures and medical specialties for the treatment and management of several diseases across the globe. A surgical procedure is complex and may lead to several complications, such as bleeding. A hemostat proves to be effective in controlling such bleeding in the surgical theater.

Additionally, the increasing focus on operating in developing and introducing new, innovative products and the increasing number of product approvals by the regulatory bodies further support the market’s growth.

- For instance, in March 2023, Axio Biosolutions received the U.S. FDA 510(k) clearance for its Ax-Surgi Surgical Hemostat. It is a chitosan-based hemostat that can be used to control severe surgical bleeding.

Additionally, increasing occurrence of accidents and trauma cases requiring surgical interventions will also supplement the market growth. For instance, an article published in January 2023 stated that in 2020, a total of 35,766 fatal car accidents occurred in the U.S. Hence, high number of such cases will result in a growing demand for effective blood loss management products.

Cancellation of elective procedures amid the COVID-19 pandemic negatively impacted the market in 2020. Consequently, the postponement of various surgeries resulted in a substantial decline in non-essential surgical rates during the initial phases of the pandemic. However, with the increase in surgical procedure volumes in 2021 and 2022, the market witnessed a substantial growth. From 2023 onwards, the market is estimated to witness a considerable growth.

Download Free sample to learn more about this report.

Hemostats Market Key Takeaways

- 2025 Market Size: USD 5.46 Billion

- 2026 Market Size: USD 5.86 Billion

- 2034 Forecast Market Size: USD 11.04 Billion

- CAGR: 8.23% from 2026–2034

- North America dominated the hemostats market with a 34.96% share in 2025.

- The passive hemostats segment is projected to lead the market with a 48.21% share in 2026.

- The general surgery segment accounted for the largest market share of 21.91% in 2026.

North America

North America led the global market, reaching USD 1.91 billion in 2025 and projected to grow to USD 2.04 billion in 2026.

Europe

Europe represented a significant share of the global market and is expected to reach USD 1.55 billion in 2026.

Asia Pacific

Asia Pacific continues to expand steadily and is projected to reach USD 1.47 billion in 2026.

U.S.

The market is projected to reach USD 1.90 billion by 2026.

Japan

The market is projected to reach USD 0.23 billion by 2026.

Read More

Hemostats Market Trends

Increasing Number of Hospitals and Surgical Centers to Boost the Demand

A key trend currently prevailing in the global market is the constant addition in the number of medical institutions catering to the need of the patient’s surgical demands. Therefore, there is an increasing and sustained need for a wide range of efficient product offerings with strong efficacies for managing bleeding complications in a wide range of surgical procedures. According to a report by the American Hospital Association, in 2022, the number of hospitals in the U.S. increased to 6,120, and this trend of rapid expansion is expected to persist during the forecast period. Furthermore, according to a report published by American Heart Association in July 2020, the annual number of Coronary Artery Bypass Graft (CABG) surgeries is around 240,000 in the U.S. All these trends are expected to increase demand for hemostatic agents during the forecast period.

Download Free sample to learn more about this report.

Hemostats Market Growth Factors

Increasing Number of Surgical Procedures Globally to Fuel Market Growth

A critical driving factor of the global market is the surge in the number of surgical procedures conducted worldwide, providing an impetus to boost the rising incidence of bleeding complications during surgeries.

- For instance, according to Eurostat data updated in July 2022, at least 1.12 million cesarean sections were performed in the European Union in 2020. The two most commonly performed surgical procedures were cesarean sections and cataract surgery.

- According to an article published by the National Library of Medicine (NLM) in July 2020, around 310 million major surgeries are performed each year globally, with around 40 to 50 million of the procedures occurring in the U.S. and 20 million in Europe.

In the current scenario, a wide range of medical instruments are available for the management and significant improvement in achieving hemostasis in surgical procedures.

- For instance, recent estimates published by the National Center for Biotechnology Information (NCBI) state that about 60-70% of all transfused red blood cells are utilized in a surgical setting, as bleeding during surgeries is one of the most feared complications to occur in these procedures.

This has led to a substantial demand for the product offerings in the global market, as many surgeons opt for administering these products in surgical procedures with minimal risk of bleeding complications.

Increasing Technological Developments in the Product to Drive Market Growth

During the forecast period, another key factor anticipated to drive market growth is the increasing number of product launches with technologically advanced features. Some advantages associated with advanced products are their efficiency in achieving hemostasis. Besides, other advantages, such as the reduced risk of infections and lower costs, are owing to the advancements in the R&D of the product. This has led to the development and manufacturing of technologically advanced product offerings with several improved features. Furthermore, it has resulted in widening the application areas of these product offerings in terms of the surgical procedures covered.

- For instance, in April 2023, Olympus introduced EndoClot Polysaccharide Hemostatic Spray (PHS) in Europe and the Middle East and Africa (EMEA) region. This product is based on EndoClot Absorbable Modified Polymer (AMP) technology.

- Similarly, TISSEEL, a product offered by Baxter, is considered among the most technologically advanced products in the fibrin sealants category. Moreover, increasing the adoption of this product is expected to drive market growth during the forecast period.

RESTRAINING FACTORS

Clinical and Other Limitations Associated with the Product to Hinder Market Growth

One of the notable restraining factors impeding the hemostats market share is the presence of clinical limitations. For instance, in cases of uncontrolled bleeding, the potential for these products to be adopted is restricted. Despite the demonstrated effectiveness in managing bleeding complications during surgical procedures and a notable reduction in infection risks, the high costs associated with these products have curtailed their widespread adoption. Additionally, specific surgical procedures face challenges due to clinical limitations associated with certain instruments. Despite significant advancements in technology and the advantages offered, these clinical limitations act as a barrier, severely constraining the broader adoption of these products.

Hemostats Market Segmentation Analysis

By Product Analysis

Passive Hemostats Dominance Supported by Increasing Number of Product Approvals

Based on product, the market is segmented into active hemostats, passive hemostats, combination hemostats, and other hemostats. The active segment can be further sub-segmented into thrombin based hemostats and fibrin sealants. The passive segment can be further sub-segmented into the plant-based hemostats, animal-based hemostats, and other segments.

The passive hemostats segment accounted for the largest market share in 2023 owing to the presence of a large number of product offerings and especially the increased adoption of technologically advanced products.

- The Passive Hemostats segment is projected to lead the market with a 48.21%% share in 2026.

- For instance, in February 2022, Futura Surgicare Pvt Ltd. introduced Hemostax (Oxidised Regenerated Cellulose). It is an absorbable hemostat that can be used for efficient bleeding control by surgeons.

Additionally, introduction of new products by key operating players also supplemented the market growth.

- For instance, in July 2023, Baxter introduced PERCLOT Absorbable Hemostatic Powder for ready to use application. This passive hemostatic powder can be used for patients with intact coagulation to address mild bleeding.

The combination hemostats segment is anticipated to register the highest CAGR in the market during the forecast period owing to the increasing launch of cutting-edge products such as Baxter’s Floseal.

To know how our report can help streamline your business, Speak to Analyst

By Application Analysis

General Surgery Segment is anticipated to Dominate due to High Number of Surgical Procedures in 2022

Based on the application, the market is segmented into trauma, cardiovascular surgery, general surgery, plastic surgery, orthopedic surgery, neurosurgery, and others. The general surgery segment accounted for the largest share of 21.91% in 2026, owing to an increasing number of several types of surgical procedures. Additionally, an increasing number of general surgeons is also supporting the increasing number of general surgery procedures.

- For instance, according to a study published in March 2021, general surgery procedures accounted for 21.4% of inpatient procedures in small rural and isolated rural hospital settings in the U.S.

The cardiovascular surgery segment is anticipated to register the highest CAGR in the market during the forecast period. This is ascribable to factors such as the increasing prevalence of cardiovascular diseases necessitating surgical intervention globally.

The growth of the orthopedic surgery, plastic surgery, and neurosurgery segments are expected to be driven by the increased prevalence of chronic diseases. The higher demand for aesthetic procedures, the substantial improvement in healthcare infrastructure, and increasing expenditure worldwide resulted in a surge in surgical procedures.

- For instance, according to the American Joint Replacement Registry 2022 Annual Report, the number of Knee Arthroplasty Procedures between 2012 and 2021 has reached 1,306,719.

By End-User Analysis

Wide-Scale Surgical Procedures Fuel Hemostats Usage, Cementing Hospitals & ASCs Segment

In terms of end-user, the market is segmented into hospitals & ASCs, tactical combat casualty care centers, and others. The critical reason for the dominance of the hospitals & ASCs segment is attributed to the majority of the surgical procedures conducted at hospitals in most developed and developing countries, owing to the availability of requirements for such complex surgical procedures. Hospitals & ASCs segment is projected to lead the market with a 89.38% in 2026.

Increasing instances of military conflict necessitating the need for combat activities are driving the tactical combat casualty care center segment. The tactical combat casualty care centers segment is expected to account for a considerable share of the global market during the forecast period. The others segment includes other medical institutions that conduct surgical procedures and is expected to register a comparatively lower CAGR in the forecast period.

REGIONAL INSIGHTS

North America

North America Hemostats Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America recorded a market size of USD 1.91 billion in 2025, capturing 34.96% of the global market share, and is projected to reach USD 2.04 billion in 2026. Some of the factors resulting in the dominance include the adoption of technologically advanced products and the strong surgical procedures volumes resulting in a higher demand for the product. Additionally, the increasing number of product approvals by the U.S. FDA further supports the region's dominance in the global market. The U.S. market is projected to reach USD 1.9 billion by 2026.

- For instance, in January 2023, Medcura, Inc.’s LifeGel Absorbable Surgical Hemostat received the U.S. FDA’s Breakthrough Device Designation. This is the only product that has received this designation and can be used in surgical procedures where swelling is tolerated.

Europe

In 2025, Europe represented USD 1.47 billion, accounting for 26.93% of the worldwide market, and is projected to grow to USD 1.55 billion in 2026 and the region’s growth is attributable to factors such as a strong healthcare expenditure that leads to a demand for technologically advanced products owing to the strong surgeries volume. The UK market is projected to reach USD 0.2 billion by 2026, and the Germany market is projected to reach USD 0.23 billion by 2026.

Asia Pacific

The Asia Pacific market generated USD 1.34 billion in 2025, representing 24.50% of the global market landscape, and is expected to reach USD 1.47 billion in 2026, a substantial increase in surgical procedures, and increasing product launches. The Japan market is projected to reach USD 0.23 billion by 2026, the China market is projected to reach USD 0.56 billion by 2026, and the India market is projected to reach USD 0.18 billion by 2026.

- For instance, according to an article published in NCBI in June 2022, the number of metabolic/bariatric surgeries in Asia Pacific has rapidly grown in the last decade. In 2010, surgeons in IFSO-APC societies performed 18,280 bariatric/metabolic surgeries. This number reached 49,553 in 2020.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are anticipated to account for comparatively lower market share and growth rate. This is ascribable to factors such as major improvements in healthcare expenditure and infrastructure. Furthermore, a strong potential patient population owing to an increasing number of surgical procedures is expected to aid market growth during the forecast period. Middle East & Africa accounted for USD 0.29 billion in 2025, representing 5.33% of the global market share, and is projected to reach USD 0.31 billion in 2026. In 2025, Latin America held 8.28% of the global market, reaching a valuation of USD 0.45 billion, and is projected to grow to USD 0.49 billion in 2026.

List of Key Companies in Hemostats Market

Strong and Diversified Product Portfolio of Leading Players to Aid Market Dominance

The competitive landscape scenario depicts a monopolistic competition structure with the presence of several established and emerging companies. However, this market is mainly dominated by three established players: Baxter, Ethicon, and BD (Becton, Dickinson, and Company). This is ascribable to factors such as a strong product portfolio, which has been in the market for a significant amount of time, coupled with innovative product offerings.

Moreover, these companies undertake various strategic initiatives such as mergers, acquisitions, and collaborations to strengthen their market presence.

- For instance, in July 2021, Baxter International Inc. completed the acquisition of CryoLife Inc.’s PerClot Polysaccharide Hemostatic System. This acquisition expanded the company’s advanced surgery portfolio.

Some emerging players include CryoLife, Inc., and Biom'up, which are expected to emerge as strong market players during the forecast period owing to their increased regulatory approvals, which results in new product launches.

LIST OF KEY COMPANIES PROFILED:

- Baxter (U.S.)

- Integra LifeSciences (U.S.)

- Stryker (U.S)

- Artivion, Inc. (U.S.)

- Biom'up (U.S.)

- BD (Becton, Dickinson and Company) (U.S.)

- Medtronic (Ireland)

- Johnson & Johnson Services, Inc. (U.S.)

- Pfizer Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- November 2023 - Ethicon, a part of the Johnson & Johnson Medical Devices Companies, announced that its ETHIZIA Hemostatic Sealing Patch had received the CE Mark approval. This product is expected to be launched in the EMEA region in the first quarter of 2024.

- April 2023 – Baxter introduced Floseal + Recothrom flowable hemostat at the Association of periOperative Registered Nurses (AORN) Global Surgical Conference & Expo 2023.

- December 2021 – BD completed the acquisition of Tissuemed – a developer of self-adhesive surgical sealant film. The acquired company’s key product Tissuepatch is used to prevent leaks from surgical incisions or control internal bleeding. This acquisition expanded BD’s product offerings.

- October 2020 - Teleflex Incorporated announced that it had signed a definitive agreement to acquire privately-held Z-Medica, LLC., which is a manufacturer of hemostatic products.

- March 2020 – Ethicon, a part of the Johnson & Johnson Medical Devices Companies, announced the strategic regional launch of SURGICEL POWDER ABSORBABLE HEMOSTAT in the key territories of Australia, New Zealand, and Thailand.

REPORT COVERAGE

The global hemostats market research report provides a detailed analysis of the market. It focuses on key aspects such as epidemiology of disease - for key countries/key regions, and key industry developments - mergers, acquisitions, partnerships, and technological advancements. Moreover, the report offers insights into the market trends and highlights other key industry-related developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over the recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.23% from 2026-2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Product

|

|

By Application

|

|

|

By End-User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 5.46 billion in 2025 and is projected to reach USD 11.04 billion by 2034.

In 2025, the North America market value stood at USD 1.91 billion.

Recording a CAGR of 8.23%, the market will exhibit steady growth during the forecast period of 2026-2034.

By product, the passive hemostats segment is expected to be the leading segment in this market during the forecast period.

The anticipated introduction of more advanced hemostats in the market, coupled with significant unmet clinical needs, is fueling the demand for the market.

Johnson & Johnson Services, Inc., Baxter, and BD (Becton, Dickinson and Company) are the leading players in the global market.

North America dominated the hemostats market with a market share of 34.96% in 2025.

Growing R&D and clinical trials by market players are leading to the development of advanced and efficient hemostats, coupled with the increase in the number of surgical procedures are expected to drive the global market.

- 2021-2034

- 2025

- 2021-2024

- 125

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us