Aerobridge Market Size, Share, and Industry Analysis, By Industry Verticals (Airline and Others), By Type (Apron Drive Bridge, Nose Loader Bridge, T-bridge, Commuter Bridge, Dual-boarding Bridge, and Others), By Wall Structural Material (Glass-walled and Steel-walled), By Elevation System (Electromechanical Elevation System and Hydraulic Elevation System), By Location (Fixed and Movable), and Regional Forecast, 2026-2034

AEROBRIDGE MARKET SIZE AND FUTURE OUTLOOK

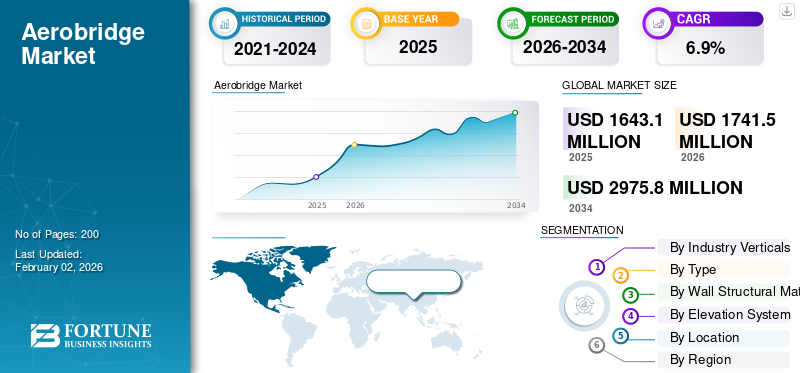

The global aerobridge market size was valued at USD 1,643.1 million in 2025. The market is projected to grow from USD 1,741.5 million in 2026 to USD 2,975.8 million by 2034, exhibiting a CAGR of 6.9% during the forecast period. Asia Pacific dominated the global aerobridge market with a market share of 35.15% in 2025.

The aerobridge market has evolved from a niche hardware line item into a strategic piece of airport infrastructure. Long-term air passenger expansion, terminal capacity constraints, and rising expectations around accessibility and passenger experience underpin the growth of this market. Airports are transitioning from basic steel structures to glass-walled, electromechanical bridges with smarter docking, integrated ground power, and pre-conditioned air, in support of decarbonization and operational resilience. The strongest demand comes from Asia Pacific, the Middle East, and selected African and Latin American hubs, where greenfield airports and expansions are still underway, while North America and Europe are entering a sizeable replacement and retrofit cycle. Movable apron-drive and dual-boarding configurations are dominating new projects as airports seek to increase gate utilization and flexibility for mixed fleets. Overall, aerobridges are increasingly viewed as critical to on-time performance, brand perception, and regulatory compliance rather than a discretionary comfort upgrade.

The competitive landscape is concentrated around a handful of global OEMs and strong regional champions. Key players actively participating in the market include CIMC Tianda Holdings (China), TK Airport Solutions S.A. (Spain), ADELTE Group S.L. (Spain), ShinMaywa Industries, Ltd. (Japan), Oshkosh AeroTech (U.S.), Mitsubishi Heavy Industries, Ltd. (Japan), PT Bukaka Teknik Utama Tbk (Indonesia), HÜBNER GmbH & Co. KG (Germany), UBS Airport Systems (Turkey), and Dabico Airport Solutions (U.S.). These companies supply a broad range of passenger boarding bridges and related systems to airports worldwide across new-build, expansion, and retrofit projects.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Passenger Growth, Efficiency Needs, and Regulatory Pressure to Boost Market Growth

The core demand is driven by three forces: passenger growth, efficiency imperatives, and rising regulatory pressure. Long-term air traffic growth as well as the recovery and expansion of international routes force airports to process an increasing number of passengers through their finite terminal footprints. Aerobridges directly support shorter turnarounds, more predictable boarding, and fewer weather-related disruptions compared with stairs and buses, which in turn improve on-time performance and airline economics. At the same time, safety and accessibility regulators are tightening expectations regarding passenger handling, particularly for people individuals with reduced mobility, prompting airports to adopt enclosed, level-access walkways. Environmental and ESG agendas add another layer. electromechanical bridges with PCA and ground power help reduce apron emissions by limiting auxiliary power unit usage. Together, these drivers make aerobridges a “nice-to-have” comfort feature, as well as a core operational asset tied to slot throughput, regulatory compliance, airline service-level agreements, and passenger satisfaction metrics, giving airport management a strong business case to invest in or upgrade.

MARKET RESTRAINTS

High Upfront CAPEX and Long Procurement Cycles to Hamper Market Growth

Despite healthy fundamentals, the aerobridge market share faces significant restraints. The most visible is the high upfront capital cost. This product requires significant investment in steel, glass, drive systems, and controls, as well as structural interface work with the terminal façade. For many mid-sized or financially constrained airports, this competes with runways, security, baggage systems, and airfield projects that appear more critical. Procurement and decision cycles tend to be lengthy, politicized, and vulnerable to delays when passenger forecasts or funding assumptions are revised. In some regions, airport operators still view stairs and buses as “good enough,” especially for low-cost carriers, limiting the pace of conversion. Currency volatility, import duties, and local-content requirements can further increase prices and complicate tenders. Finally, where concessions or privatization models place heavy financial risk on the operator, management may defer aerobridge projects in favor of less asset-intensive measures, restraining short-term order volumes even when technical need exists.

AEROBRIDGE MARKET TRENDS

Smart, Sustainable and Passenger-Centric Aerobridge Upgrades to Drive Market Expansion

The primary trend in the aerobridge market growth is a shift from basic metal walkways to smart, sustainable, and passenger-centric boarding systems. Airports are specifying glass-walled, electromechanical bridges with integrated sensors, automated docking, and compatibility with pre-conditioned air and ground power to support decarbonization targets. Design is moving toward modular, upgradeable platforms that can be digitally monitored, remotely diagnosed and more easily refurbished rather than fully replaced. At the same time, terminal planners are prioritizing flexible, apron-drive, and dual-boarding configurations to cope with mixed fleets and growing swings between widebody and narrowbody aircraft on the same gates. Passenger experience is another clear trend. Brighter, more spacious bridges, better lighting, branding surfaces, and accessibility features are becoming standard in new projects. The aerobridges are increasingly procured as part of integrated apron packages alongside GSE, power, PCA, safety markings, and IT systems, creating more bundled, long-term contracts and tighter collaboration between OEMs, airport operators, and airlines.

Download Free sample to learn more about this report.

MARKET OPPORTUNITIES

Emerging Hubs, Secondary Airports, and Retrofit Waves to Accentuate Market Growth

The biggest opportunities lie in emerging hubs, high-growth secondary airports, and the upcoming retrofit wave at aging terminals. Many airports in Asia, the Middle East, Africa, and Latin America are transitioning from bus boarding and stairs to aerobridges, resulting in first-time installation boom. As traffic increases and airlines reposition more premium capacity into these markets, boards are under pressure to modernize passenger handling and accessibility, which naturally favors product deployment. In parallel, a large installed base in North America and Europe is reaching the end of its technical or aesthetic life, opening multi-year retrofit cycles where operators can swap to glass-walled, electromechanical, digitally enabled models. There is also a niche but growing opportunity in “bridge-as-a-service” models, long-term O&M contracts, and performance-based agreements where OEMs manage uptime, safety, and energy performance for a fee. Vendors that can combine product, lifecycle services, and integration with airport IT and safety systems are well positioned to capture higher-margin opportunities.

MARKET CHALLENGES

Design Complexity, Lifecycle Support and Integration Risks are Major Challenges for Market Growth

Key challenges center on technical complexity, lifecycle support, and integration risks. Aerobridges must be precisely engineered to interface with diverse aircraft types, variable stand geometries, and evolving safety rules, which can lead to design changes, site delays, and cost overruns. Once installed, bridges must operate reliably in harsh climates, heat, corrosion, ice, and wind, requiring robust maintenance practices that some airports lack. OEMs are expected to provide rapid parts availability, remote diagnostics, and on-the-ground service across widely dispersed geographies, which puts smaller players at a disadvantage. Integration with airport IT, docking guidance systems, ground power, PCA, and safety interlocks adds further complexity and cybersecurity exposure. Any failure or collision event is highly visible and can damage both the airport and the vendor’s reputation. In price-sensitive markets, pressure to cut capex can lead to under-specification, resulting in increased total cost of ownership and potential dissatisfaction later. Balancing customization for each terminal with standardized, maintainable designs remains a structural challenge for the industry.

SEGMENTATION ANALYSIS

By Industry Verticals

Rising Focus on Quicker Turnarounds and Premium Service Standards Drives Airline Segment Growth

By industry verticals, the market is segmented into airline and others.

The airline segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 65.28% share. The demand from airlines is strong, as carriers push airports to achieve faster turnarounds, better on-time performance, and an improved passenger experience. Aerobridges support premium branding, reduce weather exposure and safety-associated incidents, and simplify boarding for widebody and narrowbody fleets, making them a critical element in airline–airport service level agreements and negotiations.

The others segment is expected to grow at a CAGR of 6.6% over the forecast period.

By Type

Versatile Aircraft Compatibility and Flexible Stand Configurations Pushes Apron Drive Bridge Segment Expansion

By type, the market is classified into apron drive bridge, nose loader bridge, T-bridge, commuter bridge, dual-boarding bridge, and others.

The apron drive bridge segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 50.71% share. Apron drive bridges are in the highest demand due to their wide range of aircraft types and stand configurations, from narrow bodies to some wide bodies. Their maneuverability helps airports maximize gate utilization, handle irregular operations, and adapt to changing fleet mixes without requiring extensive redesign of terminal facades or parking layouts.

The dual-boarding bridge segment is expected to grow at a CAGR of 9.2% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Wall Structural Material

Enhanced Aesthetics and Improved Passenger Experience Fuels Glass-walled Segment Growth

By wall structural material, the market is bifurcated into glass-walled and steel-walled.

The glass-walled segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 61.18% share. Glass-walled aerobridges are increasingly preferred as airports compete on aesthetics, comfort, and perceived safety. They let in natural light, improve wayfinding, and create a more premium feel, which supports non-aero revenue and airport branding. Visibility also helps security and operations teams monitor flows and incidents more easily than enclosed steel structures.

The steel-walled segment is expected to grow at a CAGR of 6.5% over the forecast period.

By Elevation System

Shift toward Reliable, Energy-efficient Systems Boosts Electromechanical Elevation System Segment Growth

By elevation system, the market is classified into electromechanical elevation system and hydraulic elevation system.

The electromechanical elevation system segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 54.28% share. Electromechanical elevation systems are in demand due to their lower lifecycle maintenance, better energy efficiency, and cleaner operation than traditional hydraulic systems. Airports seeking to reduce fluid leakage risks, meet environmental targets, and improve reliability are standardizing on electromechanical designs, especially for new terminals and major refurbishment programs.

The hydraulic elevation system segment is expected to grow at a CAGR of 6.6% over the forecast period.

By Location

Flexible Gate Operations and Mixed-fleet Adaptability Drives Movable Segment Growth

By location, the market is bifurcated into fixed and movable.

The movable segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 70.04% share. Movable aerobridges witness strong demand as airports need flexible infrastructure to handle diverse aircraft sizes on the same stand. Adjustable, movable units enable dynamic gate allocation, support mixed-fleet operations, and help squeeze more movements out of constrained terminal footprints. This directly improves the capacity, connectivity, and airline slot economics without new buildings.

The fixed segment is expected to grow at a CAGR of 7.1% over the forecast period.

AEROBRIDGE MARKET REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Aerobridge Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific held the dominant share in 2024, valued at USD 546.02 million, and also took the leading share in 2025, with USD 577.55 million. This region shows the strongest structural demand as China, India, Southeast Asia, and Australia expand and upgrade terminals. New greenfield airports and additional concourses at existing hubs need large batches of aerobridges, while older facilities accelerate replacement of obsolete units to reduce turnaround times and handle fast-growing regional and international traffic.

In 2026, the Chinese market is estimated to reach USD 214.3 million. It remains a major demand center as large hub expansions, regional airport upgrades, and new airports continue under long-term aviation plans. Authorities emphasize standardized, modern aerobridges to improve safety, boarding efficiency, and passenger comfort, driving bulk procurement of apron-drive and glass-walled bridges across both Tier-1 and fast-growing regional airports.

North America

The market in North America is estimated to reach USD 432.0 million in 2026. Demand for the product in this region is driven by terminal modernization at major hubs, growing traffic at secondary airports, and strict accessibility standards. The U.S. and Canadian airports are replacing aging steel bridges with glass, integrating smarter docking and safety systems, and adding extra gates to support rising domestic and transborder volumes.

Europe

During the forecast period, European region is projected to record the growth rate of 6.8% and touch the valuation of USD 513.0 million in 2026. In this region, the demand is heavily tied to refurbishment and replacement cycles at mature hubs plus selective greenfield expansions in Eastern Europe. Airports are prioritizing energy-efficient, glass-walled, and electromechanical bridges that align with EU sustainability goals, while also reconfiguring gates for higher aircraft utilization and improving passenger experiences and accessibility.

Rest of the World

The rest of the world market is set to record USD 182.0 million in 2026 as its valuation. In the Middle East, Africa, and Latin America, demand is supported by tourism growth, emerging hub strategies, and government-backed airport investment. Gulf and key African hubs are installing advanced bridges to match premium service ambitions, while Latin American airports steadily replace stairs and buses with modern boarding bridges for flagship routes.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Growth Fueled by Innovation, Partnerships, and Urban Integration by Key Players

A concentrated group of specialized OEMs and system integrators dominates the market. CIMC Tianda Holdings (China) leads global supply with large-scale manufacturing and broad international footprints, while TK Airport Solutions S.A. (Spain) and ADELTE Group S.L. (Spain) are strong in Europe, Latin America, and selective Asian hubs. In Asia, ShinMaywa Industries, Ltd. (Japan) and Mitsubishi Heavy Industries, Ltd. (Japan) leverage wider airport-systems portfolios to bundle bridges into turnkey projects. Oshkosh AeroTech (U.S.) and Dabico Airport Solutions (U.S.) add strength in North America and the Middle East through integrated apron solutions. Regional champions such as PT Bukaka Teknik Utama Tbk (Indonesia), HÜBNER GmbH & Co. KG (Germany), and UBS Airport Systems (Turkey) compete aggressively on cost, localization, and customization, increasingly winning projects in secondary and fast-growing airports, particularly where governments prioritize domestic industrial participation.

LIST OF KEY AEROBRIDGE COMPANIES PROFILED:

- CIMC Tianda Holdings (China)

- TK Airport Solutions S.A. (Spain)

- ADELTE Group S.L. (Spain)

- ShinMaywa Industries, Ltd. (Japan)

- Oshkosh AeroTech (U.S.)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- PT Bukaka Teknik Utama Tbk (Indonesia)

- HÜBNER GmbH & Co. KG (Germany)

- UBS Airport Systems (Turkey)

- Dabico Airport Solutions (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- June 2025 - Fiji Airports installed the first of six new aerobridges at Nadi International Airport. The bridge incorporates advanced features such as automated aircraft docking, compatibility with pre-conditioned air, and integrated ground power. It also offers upgraded passenger safety and improved weather protection to better handle growing passenger volumes.

- April 2025 - Newcastle Airport in Australia installed its first aerobridge a 20 m long, 31-tonne unit, marking a key step as it gears up for international services. The new bridge improves accessibility for all travelers, especially those with reduced mobility, while helping speed up boarding and disembarkation to boost overall operational efficiency.

REPORT COVERAGE

This report delivers a targeted deep dive into the aerobridge ecosystem, profiling the leading manufacturers and airport infrastructure operators, the key bridge types (apron-drive, nose-loader, T-bridge, commuter, and dual-boarding units), and the main applications across narrowbody, widebody, and regional operations. It tracks current terminal expansion programs, retrofit cycles, and automation upgrades, and pinpoints the shifts shaping the next generation of boarding solutions. Together, these insights explain the recent surge in investments and the forces set to drive the next phase of market growth.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.9% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Industry Verticals

By Type

By Wall Structural Material

By Elevation System

By Location

|

|

By Region |

By Geography

|

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 1,643.1 million in 2025 and is estimated to reach USD 2,975.8 million by 2034.

The market is anticipated to grow at a CAGR of 6.9% during the projection period (2026-2034).

The airline segment dominated the market by industry verticals in 2025.

The electromechanical elevation system segment led the market in 2025.

CIMC Tianda Holdings (China), TK Airport Solutions S.A. (Spain), ADELTE Group S.L. (Spain), ShinMaywa Industries, Ltd. (Japan), Oshkosh Corporation (U.S.), Mitsubishi Heavy Industries, Ltd. (Japan) are some of the leading OEMs in the market.

Asia Pacific was the largest shareholder in the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us