Aerospace Accumulator Market Size, Share, and Industry Analysis, By Accumulator Type (Bladder, Piston, Diaphragm, and Metal Bellows), By Pressure Class (Less Than 3,000 Psi, 3,000 - 5,000 Psi, and More Than 5,000 Psi), By Application (Flight-control & Actuation, Landing Gear Emergency Extension, Braking Energy Reserve, Doors, Ramps & Cargo Systems, Thrust Reverser Actuation, and Others), By Capacity (< 1 L, 1–5 L, and > 5 L), By End Use (OEM and Aftermarket), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

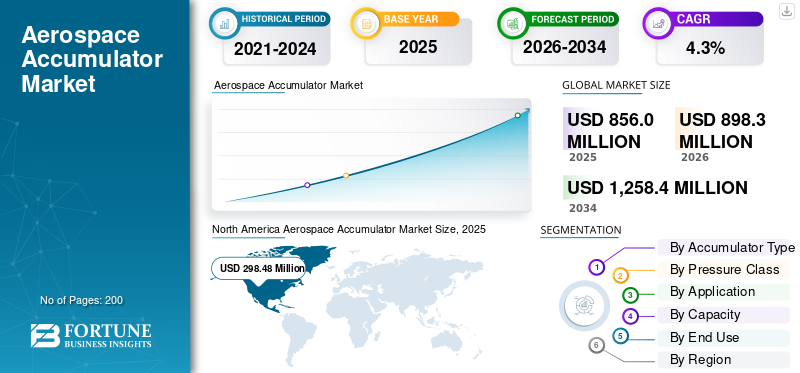

The global aerospace accumulator market size was valued at USD 856.0 million in 2025. The market is projected to grow from USD 898.3 million in 2026 to USD 1,258.4 million by 2034, exhibiting a CAGR of 4.3% during the forecast period. North America dominated the aerospace accumulator market with a market share of 34.86% in 2025.

The aerospace accumulator market is a critical segment of the aerospace industry, providing essential hydraulic energy storage solutions used in commercial, military, and space applications. Aerospace accumulators support vital functions such as flight control systems, landing gear operation, emergency power backups, and fuel systems, ensuring aircraft safety and operational efficiency. Market growth is driven by increasing demand for fuel-efficient and lightweight components, advancements in hydraulic technologies, and rising commercial and defense aircraft production globally. Innovations such as smart accumulators with real-time monitoring and predictive maintenance capabilities are also shaping future growth trajectories.

Expanding urban air mobility and UAV sectors contribute to demand for specialized accumulators designed for compact, high-performance applications. The market benefits from regulatory support focused on reducing carbon emissions and enhancing safety standards, spurring investment in advanced materials and design methodologies. Regions such as North America lead the market due to mature aerospace infrastructure and defense modernization initiatives, while the Asia Pacific region is experiencing rapid growth driven by expanding commercial aviation and indigenous aerospace manufacturing capabilities.

The aerospace accumulator market is dominated by a concentrated set of Tier-1 and specialist suppliers. Parker Aerospace (U.S.), Collins Aerospace (U.S.), and Eaton Aerospace (U.S.) lead with broad portfolios of hydraulic and pneumatic accumulators integrated into flight control, landing gear, and braking systems.

Download Free sample to learn more about this report.

AEROSPACE ACCUMULATOR MARKET Key Takeaways

- 2025 Market Size: USD 856.0 million

- 2026 Market Size: USD 898.3 million

- 2034 Forecast Market Size: USD 1,258.4 million

- CAGR: 4.3% from 2026–2034

- North America dominated the aerospace accumulator market with a market share of 34.86% in 2025.

- The bladder segment is expected to lead the market with a 46.03% share in 2026.

- The 3,000 - 5,000 psi segment is anticipated to dominate with a 56.15% share in 2026.

North America

North America generated USD 298.48 million in 2025, supported by strong commercial aircraft production, defense investments, and hydraulic system advancements.

Europe

Europe is projected to reach USD 264.6 million in 2026, driven by fuel-efficiency initiatives, green aviation programs, and extensive MRO activities.

Asia Pacific

Asia Pacific is estimated at USD 272.5 million in 2026 and is expected to witness the fastest growth due to expanding airline fleets and aerospace infrastructure investments.

U.S.

The market is expected to reach USD 283.0 million in 2026, supported by large-scale aircraft manufacturing and ongoing defense modernization programs.

Japan

Growth is supported by increasing investments in aerospace technologies, aircraft component manufacturing, and the adoption of advanced hydraulic systems across aviation applications.

Read More

AEROSPACE ACCUMULATOR MARKET TRENDS

Demand for Advanced & Sustainable Systems Driving Rapid Expansion

The aerospace accumulator market growth is marked by a transition toward sustainability, digitalization, and advanced lightweight engineering, reflecting the rapid evolution in how commercial and defense aircraft approach hydraulic system integration and environmental impact. There is a visible move away from conventional steel/aluminum designs to composites and titanium, reducing weight and improving fuel efficiency while also complying with tighter emission mandates. Smart technologies, such as onboard sensors and predictive maintenance algorithms, are integrated in modern accumulators, providing real-time system monitoring and minimizing downtime. Regional fleet modernization and the push for greener aviation have been fueling this trend, with Asia Pacific, in particular, accelerating adoption as its aviation sector rapidly expands and upgrades. As aerospace platforms diversify from UAVs and next-generation fighter jets to commercial airliners, the trend increasingly favors innovation and adaptability in accumulator manufacturing, with sustainability targets and operational reliability at the forefront.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Surging Aircraft Production and Digital Integration are Boosting Market Growth

The primary driver of the aerospace accumulator market is the surge in aircraft deliveries across commercial, military, and civil sectors, paired with digital upgrades in hydraulic and energy management systems. Advanced flight control, landing gear, braking, and redundancy mechanisms depend on accumulators for critical hydraulic pressure, making reliability non-negotiable in modern aerospace design. The rise in “more electric aircraft” concepts is intensifying demand for compact, integrated accumulators that support emergency energy needs and rapid actuation. Defense modernization programs, especially in North America, Europe, and fast-developing Asia Pacific markets, are compelling system makers to invest in state-of-the-art accumulators for both new and retrofitted fleets. Innovations in predictive maintenance, smart sensor integration, and real-time diagnostics ensure accumulators are central to achieving heightened safety standards, operational continuity, and cost efficiency within the industry.

Market Restraints

Cost, Compliance, and Sustainability Pressures to Hamper Market Growth

The aerospace accumulator sector faces critical restraints due to volatile material costs, regulatory complexities, and challenges in scaling sustainable manufacturing. The adoption of advanced composites and titanium, while essential for lightweighting, comes with higher price volatility and sourcing risks exacerbated by geopolitical tensions and global supply chain disruptions. Compliance with stringent aviation and environmental standards necessitates extensive and expensive R&D, testing, and certification protocols, which slow product cycles and put pressure on margins. The industry’s push for greener solutions, including recycling, low-waste manufacturing, and end-of-life recovery, further tightens operational leeway as regulatory frameworks expand across jurisdictions. As legacy aircraft remain in service longer, retrofitting with compliant accumulator systems introduces technical and cost barriers, constraining broad market adoption and innovation.

MARKET OPPORTUNITIES

Electrification and Need for Lightweight Aircraft Components to Accentuate Market Growth

Aerospace electrification and the push for lightweight aircraft components open compelling market opportunities for accumulator manufacturers and system integrators. Growth is expected from sectors such as electric and hybrid aircraft, urban air mobility vehicles, and high-performance UAVs that require compact, high-density energy solutions for actuation, braking, and emergency power backups. The transition to smart, energy-efficient hydraulics enables accumulators to play central roles in new system architectures, from fly-by-wire controls to active vibration suppression, each demanding new design standards and innovative materials. The evolution in space exploration and satellite launch vehicles further extends market potential for specialized, robust accumulators capable of withstanding extreme physical and operational stresses. Ecosystem shifts, including government investments in aerospace infrastructure, digitalization, and R&D for carbon-neutral aviation, make it a favorable environment for aerospace accumulator companies that can innovate and align product development with emerging aircraft concepts and efficiency mandates.

MARKET CHALLENGES

Technology, Legacy Integration, and Competitive Pressure are Major Challenges in Market

Integrating next-generation accumulator technologies into legacy aircraft fleets while maintaining performance, compliance, and cost-effectiveness remains a central challenge for the market. The influx of digital platforms and smart sensor networks complicates interoperability, especially in mixed fleets with diverse hydraulic architectures. Manufacturers must continually navigate certification complexity, where evolving standards and cross-border requirements demand flexible design plus robust documentation and testing. Rising competitive intensity, led by both traditional OEMs and agile technology startups, pushes incumbents to accelerate innovation pipelines while constraining profits. Achieving reliability in extreme environments (temperature, vibration, and pressure) complicates design and material selection. Additionally, the growing adoption of automation and AI-driven diagnostics, while boosting safety and efficiency, requires significant investments that may challenge smaller aerospace accumulator suppliers and new entrants.

SEGMENTATION ANALYSIS

By Accumulator Type

Bladder Accumulators Dominate Market Due to Their Reliable Hydraulic Performance and Low Maintenance Needs

By accumulator type, the market is segmented into bladder, piston, diaphragm, and metal bellows.

The bladder segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 46.03% share. Bladder accumulators dominate demand as they offer reliable hydraulic energy storage with simple maintenance, rapid response to pressure changes, and good compatibility with diverse aircraft hydraulic environments, making them cost-effective throughout the lifecycle.

The piston segment is expected to grow at a CAGR of 4.4% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Pressure Class

3,000–5,000 Psi Segment Led Market Due to Modern Aircraft Requiring Higher Hydraulic Pressure for Safety and Performance

By pressure class, the market is classified into less than 3,000 psi, 3,000 - 5,000 psi, and more than 5,000 psi.

The 3,000 - 5,000 psi segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 56.15% share. Rising demand for the 3,000–5,000 psi segment stems from the need for more robust, high-pressure hydraulic performance in new-generation aircraft and upgraded fleets, providing optimal actuation, safety, and operational reliability.

The more than 5,000 psi segment is expected to grow at a CAGR of 5.0% over the forecast period.

By Application

Flight-Control and Actuation Segment Dominated as Flight Safety and Control Precision Depend on Stable Hydraulic Power

By application, the market is classified into flight-control & actuation, landing gear emergency extension, braking energy reserve, doors, ramps & cargo systems, thrust reverser actuation, and others.

The flight-control & actuation segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 34.30% share. Actuation and flight-control applications drive this segment’s demand as modern aviation safety and maneuverability depend on accumulators for energy reserves, pressure stability, and rapid response in mission-critical controls.

The landing gear emergency extension segment is expected to grow at a CAGR of 4.5% over the forecast period.

By Capacity

Rise of UAVs and Urban Air Mobility Platforms Boosted Demand for 1–5 L Accumulators

By capacity, the market is classified into < 1 L, 1–5 L, and > 5 L.

The 1–5 L segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 56.19% share. Compact accumulators between 1–5 liters are in demand thanks to urban air mobility and UAV programs requiring precise energy storage for smaller, lightweight flight platforms and specialized subsystem integration.

The < 1 L segment is expected to grow at a CAGR of 4.8% over the forecast period.

By End Use

OEM Segment Commanded Since New Aircraft Designs Require Embedded Accumulators Meeting Strict Compliance and Innovation Standards

By end use, the market is classified into OEM and aftermarket.

The OEM segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 65.20% share. OEM demand is robust as accumulators are embedded into new aircraft designs, fulfilling compliance, reliability, and operational needs in next-generation commercial, military, and defense vehicle launches worldwide.

The aftermarket segment is expected to grow at a CAGR of 4.0% over the forecast period.

Aerospace Accumulator Market REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and Rest of the World.

North America

North America Aerospace Accumulator Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 289.37 million, and also took the leading share in 2025 with USD 298.48 million. Demand is strongest, driven by major commercial aircraft production, extensive defense programs, and leadership in hydraulic system digitalization and innovation. Fleet renewal and next-gen aircraft platforms amplify the need for advanced accumulators.

In 2026, the U.S. market is estimated to reach USD 283.0 million. The U.S. aerospace accumulator demand is driven by its large commercial aircraft production and extensive defense modernization programs. Despite supply chain challenges, steady deliveries of narrowbody and widebody aircraft sustain market needs. Innovation in fuel-efficient, lightweight systems and flight control technologies also bolsters demand, aligning with the growing aerospace manufacturing and modernization ecosystem domestically.

Europe

During the forecast period, the European region is projected to record a growth rate of 4.2% and touch the valuation of USD 264.6 million in 2026. Growth is sustained by fuel efficiency regulations, green aviation projects, and extensive MRO activities. Demand centers on lightweight and eco-friendly accumulator solutions for both civil and military applications.

Asia Pacific

The market in Asia Pacific is estimated to reach USD 272.5 million in 2026. Fastest growth region, propelled by expanding airline fleets, government-backed aerospace infrastructure, and aggressive commercial and defense aviation investments, with China and India leading adoption of advanced systems.

Rest of the World

The rest of the world market is set to record USD 48.7 million in its valuation by 2026. Markets in the Middle East, Africa, and Latin America are rising due to regional fleet expansion and defense procurement, though total volumes remain lower compared to established markets.

Competitive Landscape

KEY INDUSTRY PLAYERS

Growth Fueled by Innovation, Partnerships, and Urban Integration by Key Players

Key players such as Parker Aerospace, Collins Aerospace, Eaton Aerospace, Safran Landing Systems, Liebherr-Aerospace, Arkwin Industries, Triumph Group, Sargent Aerospace & Defense, Valcor Engineering, and PneuDraulics are instrumental in advancing this market. These companies contribute through continuous innovation in accumulator design, material science, and integration of digital technologies to enhance performance and reliability. They supply accumulators that meet stringent aerospace certification standards, enabling safer and more efficient aircraft operations. Many engage in R&D collaborations and strategic partnerships to develop lightweight, environmentally friendly solutions aligned with global sustainability goals. Their extensive global manufacturing and service networks ensure timely delivery and aftermarket support, vital for maintaining operational readiness in commercial and defense sectors. Collectively, these industry leaders drive technological advancements and broaden market reach, ensuring the aerospace accumulator market share remains resilient and adaptive to evolving aerospace trends.

LIST OF KEY AEROSPACE ACCUMULATOR COMPANIES PROFILED

- Parker Aerospace (U.S.)

- Collins Aerospace (U.S.)

- Eaton Aerospace (U.S.)

- Safran Landing Systems (France)

- Liebherr-Aerospace (France)

- Arkwin Industries (U.S.)

- Triumph Group (U.S.)

- Sargent Aerospace & Defense (U.S.)

- Valcor Engineering (U.S.)

- PneuDraulics (PDI) (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025 - Rolls-Royce signed an agreement with Bharat Forge to manufacture and supply fan blades for the Pearl 700 and Pearl 10X engines. Concluded at Rolls-Royce’s Dahlewitz site near Berlin, the pact deepens the companies’ collaboration and supports the plan to double Rolls-Royce’s India sourcing by 2030.

- July 2025 - FDH Hardware, a division of FDH Aero, signed a new supply agreement with MS Aerospace to provide fasteners to OEM and aftermarket customers worldwide. The deal covers critical applications across space, military, helicopter, commercial aircraft, missile, jet, and rocket engine platforms.

- July 2025 - HAECO and Liebherr-Aerospace entered a component maintenance agreement to support COMAC’s C909 and C919 programs. The partners will jointly deliver repair and overhaul services for hydraulic components, aiming to uphold safety and reliability as COMAC expands its fleet.

- May 2025 – GE Aerospace finalized a limited distribution agreement with United Aero Group, authorizing UAG to distribute CT7/T700 engine parts and spares. The arrangement broadens service access for CT7/T700 operators by adding another qualified channel for parts and maintenance solutions.

- May 2024 - Topcast reached a new cooperation agreement with Apollo Aerospace Components to expand joint activity in aerospace and defense hardware. Apollo will supply a wide range of U.S. and European specification items nuts, bolts, screws, rivets, bearings, seals, labels, and hydraulic fittings through the partnership.

REPORT COVERAGE

The aerospace accumulator market delivers a focused analysis of the key ecosystem players, including leading manufacturers, hydraulic system integrators, and service providers specializing in accumulator components such as bladders, pistons, charging, and control systems. The report explores core use cases spanning commercial aviation, military applications, and emerging sectors, including urban air mobility and regional air transport. It maps policy developments, regulatory milestones, and pilot programs fueling real-world deployments and infrastructure expansion globally. Key shifts in material technology, digital integration, and sustainability initiatives are highlighted as critical factors accelerating market growth.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.3% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation

|

By Accumulator Type · Bladder · Piston · Diaphragm · Metal Bellows |

|

By Pressure Class · Less Than 3,000 Psi · 3,000 - 5,000 Psi · More Than 5,000 Psi |

|

|

By Application · Flight-control & Actuation · Landing Gear Emergency Extension · Braking Energy Reserve · Doors, Ramps & Cargo Systems · Thrust Reverser Actuation · Others |

|

|

By Capacity · < 1 L · 1–5 L · > 5 L |

|

|

By End Use · OEM · Aftermarket |

|

|

By Region · North America (By Accumulator Type, Pressure Class, Application, Capacity, End Use, and Country) o U.S. (By End Use) o Canada (By End Use) · Europe (By Accumulator Type, Pressure Class, Application, Capacity, End Use, and Country) o U.K. (By End Use) o Germany (By End Use) o France (By End Use) o Russia (By End Use) o Rest of Europe (By End Use) · Asia Pacific (By Accumulator Type, Pressure Class, Application, Capacity, End Use, and Country) o China (By End Use) o Japan (By End Use) o India (By End Use) o Rest of Asia Pacific (By End Use) · Rest of the World (By Accumulator Type, Pressure Class, Application, Capacity, End Use, and Sub-Region) o Middle East and Africa (By End Use) o Latin America (By End Use) |

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 856.0 million in 2025 and is estimated to reach USD 1,258.4 million by 2034.

The market is growing at a CAGR of 4.3% during the projection period (2026-2034).

The bladder segment led the market.

By capacity, the 1–5 L segment dominated the global market.

Parker Aerospace, Collins Aerospace, Eaton Aerospace, Safran Landing Systems, Liebherr-Aerospace, and Arkwin Industries are some of the leading OEMs in the market.

North America held the largest market share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us