The Asia Pacific market generated USD 1.26 billion in 2025, representing 23.13% of the global market landscape, and is expected to reach USD 1.37 billion in 2026, with the Japan market is projected to reach USD 0.29 billion by 2026, the China market is projected to reach USD 0.53 billion by 2026, and the India market is projected to reach USD 0.19 billion by 2026. In the Asia-Pacific, countries including China, India, South Korea, and Japan, the governments of these countries are promoting local forging ecosystems to support domestic aircraft and UAV programs.

Aerospace Cold Forgings Market Size, Share & Industry Analysis, By Material Type (Aluminum Alloys, Titanium Alloys, Stainless Steel, Nickel-Based Superalloys, and Carbon & Alloy Steel), By Component Type (Shafts & Spindles, Landing Gear Components, Engine & Turbine Discs, Structural Fittings, Fasteners & Bolts, Rings & Flanges, and Others), By Aircraft Type (Commercial Narrow-Body Aircraft, Wide-Body & Long-Range Aircraft, Military Fighters & Rotorcraft, Transport Aircraft & UAVs, and Business Jets), By Application and By End User, and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

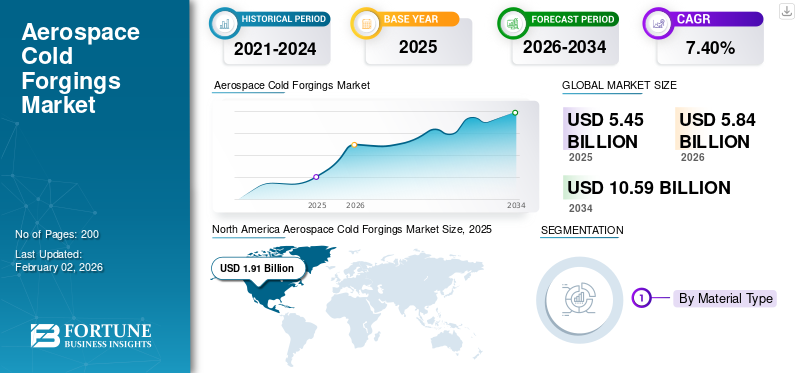

The global aerospace cold forgings market size was valued at USD 5.45 billion in 2025 and is projected to grow from USD 5.84 billion in 2026 to USD 10.59 billion by 2034, exhibiting a CAGR of 7.40% during the forecast period. North America dominated the aerospace cold forgings market with a market share of 35.06% in 2025.

Aerospace cold forgings are strong, precision-shaped metal parts created at or near room temperature for aircraft, spacecraft, and defense systems. This process improves fatigue resistance, dimensional accuracy, and surface quality while maintaining lightweight components. These characteristics make cold forgings ideal for engines, landing gear, and airframes. As global aviation moves toward fuel efficiency and advancing materials, cold forging has become crucial for producing lighter, stronger, and longer-lasting aircraft. The market is growing due to increased aircraft production, defense modernization, and the use of titanium and nickel-based alloys, as well as the adoption of digitally controlled forging technologies.

Leading companies, including Precision Castparts Corp., Otto Fuchs, Arconic, Bharat Forge, and VSMPO-AVISMA, are driving this market through innovation and global integration. They are developing closed-die, CNC-controlled, and hybrid cold forging methods to improve precision, cut waste, and localize supply chains. These players are transforming aerospace manufacturing processes, making cold forging the foundation of a smarter, cleaner, and more sustainable next-generation aerospace sector.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Constant Lightweight-Material Demand Spurs Aerospace Cold Forgings Market Growth

One of the primary factors driving the aerospace cold forgings market growth is the need for lighter and stronger aerospace parts. Airlines aim to reduce fuel consumption, and manufacturers must meet stricter emissions and efficiency standards. Cold-forged components made from advanced materials such as titanium and high-strength-to-weight ratio alloys are becoming increasingly essential. These precise forgings enable aircraft builders to replace heavy, machined parts for forged components that are strong, consistent, and lighter. This shift is growing demand for aerospace parts used in engine systems, landing gear, and structural assemblies.

- For example, in July 2024, industry reports mentioned that Boeing’s plans to increase production, expecting nearly 44,000 new airplanes in commercial aviation over the next 20 years, are driving a rise in demand for lighter and high-performance forging components.

MARKET RESTRAINTS

Supply Chain Fragmentation and Alloy Shortages Restrain the Market Development

A significant challenge for the aerospace cold forgings market today is its heavy reliance on a fragile global supply chain for specialty metals and aerospace-grade alloys. The precise nature of cold forging requires very pure grades of titanium, nickel, and stainless steel. These materials often come from a limited number of global suppliers. Disruptions from geopolitical tensions, export restrictions, or energy shortages can easily disrupt the system, causing production delays of several months. Many Tier-2 and Tier-3 forging houses lack backup sourcing or local melting capabilities, rendering the industry susceptible to unexpected material shortages.

- In February 2025, GE Aerospace publicly noted ongoing delays in delivering forged engine components due to nickel alloy shortages and supplier capacity issues in its U.S. and European plants. Likewise, Airbus experienced periodic part delays in late 2024 when sub-tier forging suppliers struggled with raw material lead times that exceeded 40 weeks. This highlights how metallurgical bottlenecks continue to impact aerospace manufacturing processes.

MARKET OPPORTUNITIES

Rising Localization and Next-Gen Alloy Adoption Create Growth Opportunities

The aerospace cold forgings market is entering a new phase of opportunity as countries and OEMs work to localize aerospace manufacturing and adopt next-generation alloys for lightweight, high-stress components. Nations such as India, Brazil, Japan, and the UAE are heavily investing in local forging, heat treatment, and precision machining facilities to reduce reliance on imports. At the same time, the introduction of hybrid and super-plastic alloys, including advanced titanium and nickel blends, provides new options for weight reduction and longer part life in both civil and defense aircraft. These changes are attracting smaller, tech-focused forging companies into global supply chains, resulting in a broader and more resilient manufacturing network.

- In January 2025, India opened the world’s largest aerospace-grade titanium and super alloy forging facility in Lucknow, aimed at supporting HAL, ISRO, and global OEM programs.

AEROSPACE COLD FORGINGS MARKET TRENDS

Automation and Digital Forging Are Shaping Aerospace Production Efficiency Trends

The aerospace cold forgings market is experiencing a rapid shift toward automation, digital simulation, and closed-loop process control. Forging plants are adopting CNC-integrated systems, robotic handling arms, and AI-driven quality monitoring. These improvements drastically enhance precision and reduce scrap rates. The integration of digital twins enables engineers to simulate metal flow and die stress before physical forging. This shortens development cycles and ensures tighter tolerances. This change is turning a traditionally manual industry into one that is data-driven and predictive. It enables higher repeatability and real-time defect detection. As aircraft programs become increasingly complex and production volumes increase, digitalization is emerging as the most significant trend shaping the future of aerospace forging.

- In September 2024, Airbus and Siemens Digital Industries partnered to implement digital twin forging systems across several European aerospace sector suppliers. This partnership enables them to simulate and optimize titanium and aluminum cold forging processes in real-time.

MARKET CHALLENGES

High Certification Barriers and Costly Qualifications Slow Industry Expansion

One of the biggest challenges in the aerospace cold forgings market is the complex and lengthy certification process required to qualify forging materials, dies, and production lines for flight use. Every component must meet stringent standards, including AS9100, NADCAP, and OEM-specific metallurgy tests. This makes it very hard for new companies or smaller suppliers to grow quickly. Even after receiving technical approval, the costs for maintaining documentation, inspection tools, and traceability systems remain quite high. This slows down the adoption of new ideas and limits capacity expansion, especially in emerging regions where infrastructure and testing labs are still in development. In short, aerospace forging isn’t just a materials issue; it’s a certification marathon that only a few global companies can currently handle.

- For example, in October 2024, HAL’s Aerospace Division in India confirmed that its new titanium forging line in Bengaluru was still waiting for NADCAP accreditation. This has delayed initial deliveries to Airbus for A320 family landing-gear parts by nearly eight months.

Russia-Ukraine War Impact

Geopolitical Disruptions Reshape Titanium Supply Chains and Forging Production Dynamics

The Russia-Ukraine conflict has had a significant and lasting impact on the aerospace cold forgings industry. This impact stems not only from sanctions and trade disruptions but also from significant changes in the global supply chain for titanium, nickel, and specialty steel. Russia, through VSMPO-AVISMA, has been one of the world’s largest suppliers of aerospace-grade titanium. This titanium is vital for companies including Airbus, Boeing, Safran, Rolls-Royce, and many Tier-1 forging suppliers. When the conflict began, sanctions, export restrictions, and logistics issues dramatically reduced the availability of these materials. This situation forced original equipment manufacturers (OEMs) and forgers to quickly look for new suppliers in Japan, Kazakhstan, China, and India. The immediate result was a rise in alloy prices, longer lead times, and even production halts at several Western forging companies that depended heavily on Russian materials.

The war also caused a shift in where aerospace manufacturing takes place. European forgers and OEMs began to invest more in building capacity in their own countries or allied nations. This created new opportunities for plants in France, Germany, and Eastern Europe. It also sped up efforts in India, Japan, and the U.S. to set up local titanium melting and forging operations. Demand for defense materials surged across NATO member countries, resulting in increased orders for missile casings, aircraft structures, and UAV components, all of which require cold-forged materials. Many smaller suppliers found it hard to meet the growing demands of both sectors, which resulted in ongoing material shortages and a rise in subcontracting to Tier-2 and Tier-3 partners in the Asia-Pacific region.

For example, in May 2024, Airbus announced it had decreased its reliance on Russian titanium to less than 10% of its total sourcing. This change followed an increase in contracts with Toho Titanium in Japan and UKTMP in Kazakhstan. Around the same time, VSMPO-AVISMA revealed plans to boost its domestic forging output to support military programs for Sukhoi and Irkut, highlighting the split in the global supply chain.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material Type

Lightweight Efficiency and Cost Versatility of Aluminum Alloys Surges Segment’s Growth

In terms of material type, the market is categorized into aluminum alloys, titanium alloys, stainless steel, nickel-based super alloys, and carbon & alloy steel.

The aluminum alloys segment is projected to dominate the aerospace cold forgings market by material, accounting for 31.34% of the global market share in 2026. Aluminum alloys lead the market by holding the largest aerospace cold forgings market share, due to their providing a high strength-to-weight ratio at the lowest cost. No other alloy type has matched this combination. Their lightweight helps save fuel and improves payload efficiency, making them essential for aircraft structures, wing spars, and fuselage fittings. Aluminum is also easier to cold-forge and machine, resulting in high production rates with little need for extra processing. Additionally, its wide availability and established global supply chain make it a safe choice for both OEMs and Tier-1 suppliers. While titanium and nickel alloys are making progress in high-performance areas, aluminum continues to be the main material driving the aerospace forging industry.

For example, in August 2024, Airbus renewed its long-term contract with Constellium SE (France) to provide aluminum-lithium alloy forgings for the A320 and A321XLR programs. This agreement highlights aluminum’s ongoing dominance, as the alloy offers up to 20% weight savings while ensuring the necessary fatigue and corrosion resistance for high-volume commercial aircraft production.

The titanium alloys segment is expected to grow at the fastest CAGR of 9.3% during the forecast period.

By Component Type

High-Strength Requirements and Precision Tolerances Propel Landing Gear Components as the Dominant Segment

On the basis of component type, the market is classified into shafts & spindles, landing gear components, engine & turbine discs, structural fittings, fasteners & bolts, rings & flanges, and others (brackets, rods, and bushings).

Landing gear components are the leading segment in the aerospace cold forgings market, holding around 18.42% market share. The dominance is attributed to as the Landing gear needs very high structural strength, fatigue resistance, and impact durability. These qualities are best obtained through precision cold forging. These parts endure extreme loads during take-off, landing, and taxiing, making forgings the preferred method over casting or machining. Materials, including titanium and alloy steels, are forged into struts, pistons, and trunnions with micron-level precision to ensure strength and reliability. As aircraft programs increasingly focus on weight reduction and safety, manufacturers such as Boeing, Airbus, and Embraer prioritize cold-forged landing gear assemblies due to their better performance-to-weight ratio and reliable history in long-haul and defense platforms.

For instance, in May 2024, Safran Landing Systems opened an expanded forging and heat-treatment line at its Bidos facility in France. This line is dedicated to making titanium landing gear components for the A350 and B787 programs.

The engine & turbine discs segment is expected to grow at the fastest CAGR of 9.2% over the forecast period.

By Aircraft Type

Increasing Demand for Fleet Replacement and High Production Volume Leads the Commercial Narrow-Body Aircraft Segment

Based on aircraft type, the market is segmented into commercial narrow-body aircraft, wide-body & long-range aircraft, military fighters & rotorcraft, transport aircraft & UAVS, and business jets.

Commercial narrow-body segment is expected to lead by aircraft type, contributing 34.42% globally in 2026 due to this segment accounting for the largest share of global aircraft production and fleet renewals. Programs, including the Airbus A320neo, Boeing 737 MAX, and COMAC C919, depend heavily on forged parts for landing gear, structural fittings, engine mounts, and control linkages. These components require precision cold forging for strength, fatigue resistance, and reduced weight. The aircraft's short-to-medium-haul operations lead to frequent take-offs and landings, which increase wear on forged parts and drive ongoing aftermarket demand.

- In April 2024, Airbus announced it would increase production of its A320neo family to 75 aircraft per month by 2026. This historic rate directly boosts the need for high-volume forged aluminum and titanium components across its global supply chain.

The segment of military fighters & rotorcraft is growing at a CAGR of 8.2% growth across the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Critical Performance Demands and Material Complexity Make Engine Systems the Dominant Segment

Based on application, the market is segmented into engine systems, landing gear systems, airframe structures, control systems, auxiliary systems, and others.

Engine systems dominate the aerospace cold forgings market in 2024 because they require the highest mechanical strength, heat resistance, and metallurgical precision of any aircraft subsystem. Components such as turbine discs, shafts, compressor rings, and bearing housings work under extreme stress and temperature conditions, where even tiny flaws can jeopardize engine safety and efficiency. Cold forging offers the necessary grain alignment and dimensional control to meet the required fatigue life and material integrity in titanium and nickel-based superalloys. As new-generation engines aim for higher bypass ratios and lower emissions, the demand for lightweight high-strength components continues to grow. The landing gear components segment held a 17.29% market share in 2026.

For instance, in March 2025, Rolls-Royce expanded its precision forging and superalloy disc production facility in Derby, U.K., to support its UltraFan engine program, the world’s most fuel-efficient turbofan.

The segment of auxiliary systems is set to grow at a CAGR of 8.5% growth across the forecast period.

By Forging Technology

Precision, Efficiency, and Material Optimization Lead the Closed Die Forging Segment’s Growth

Based on forging technology, the market is segmented into conventional cold forging, closed die/impression forging, open die forging, roll & upset forging, and others (precision / CNC-controlled forging, hybrid (cold + warm) forging).

Closed die (impression) forging leads the aerospace cold forgings market, is projected to reach around 34.36% market share. The dominance is attributed to the segment's ability to provide the highest dimensional accuracy, repeatability, and material efficiency. These factors are essential for parts used in aerospace applications. The process allows manufacturers to create complex shapes, such as turbine discs, landing gear joints, and actuator housings, with little need for post-machining and consistent grain flow. Its ability to produce near-net-shape parts decreases both material waste and cycle time. This is especially important when working with expensive alloys such as titanium and nickel super alloys, resulting in closed die (impression) segments' dominance.

For example, in February 2025, Arconic Corporation (U.S.) started a new closed-die titanium forging line in Cleveland, Ohio. This line focuses on producing structural and engine components for Airbus and Boeing programs.

The other segment consists of precision / CNC-controlled forging, and hybrid (Cold + Warm) forging is set to grow at a rate of 8.3% growth during the forecast period.

By End User

High Production Integration and Direct Design Authority Leads OEMs as the Dominant End User

In terms of end user, the market is segmented into OEMs, Tier-1 & Tier-2 Suppliers, MRO service providers, and defense & government procurement agencies.

Original Equipment Manufacturers (OEMs) dominate the aerospace cold forgings market because they are at the center of the production chain. They hold both the design authority and procurement control over critical forged components. OEMs, including Airbus, Boeing, Embraer, and Lockheed Martin, directly source precision-forged parts for airframes, landing gear, and propulsion systems. They often set material specifications and supplier standards. Additionally, OEM-led efforts for sustainability and efficiency are speeding up the move toward lightweight alloys and digital forging technologies, resulting in further dominance of the segment throughout the forecast period.

For instance, in November 2024, Boeing awarded multi-year forging supply contracts to PCC (Precision Castparts Corporation) and Arconic for high-performance titanium and nickel-alloy components used in the 737 MAX and 787 programs.

The segment of Tier-1 & Tier-2 Suppliers is set to grow at a CAGR of 8.1% growth across the forecast period.

Aerospace Cold Forgings Market Regional Outlook

North America Dominates the Market, Driven by U.S. Defense Modernization and High Military Spending

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World (Middle East & Africa, and Latin America).

North America

North America Aerospace Cold Forgings Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America recorded a market size of USD 1.91 billion in 2025, capturing 35.06% of the global market share, and is projected to reach USD 2.04 billion in 2026, led primarily by the United States, which alone contributed over 89.43% share in 2024 of the regional share. U.S. deep industrial integration led by Boeing, Lockheed Martin, GE Aerospace, Honeywell, and Raytheon Technologies supports full in-house control of design, material testing, and production. With a strong presence of companies including PCC, Arconic, ATI, and Howmet Aerospace, North America maintains unmatched expertise in titanium, nickel, and advanced aluminum alloy forging. The U.S. market is projected to reach USD 1.71 billion by 2026.

Other regions such as Asia-Pacific, Europe, and the Middle East are expected to see significant growth in the Aerospace Cold Forgings Market in the coming years.

Europe

In 2025, Europe represented USD 1.5 billion, accounting for 2.38% of the worldwide market, and is projected to grow to USD 1.6 billion in 2026. During the forecast period, the European region is projected to have a growth rate of 7.1%. The market in Europe is estimated to be USD 1.50 billion in 2025, making it the second-largest region in the market. The UK market is projected to reach USD 0.27 billion by 2026 and the Germany market is projected to reach USD 0.29 billion by 2026.

Asia Pacific

Rest of the World

The market in Rest of the World reached USD 0.77 billion in 2025, representing 14.12% of total market revenue, and is projected to reach USD 0.82 billion in 2026. Meanwhile, the rest of the world (Africa and Latin America) collectively contributes approximately 14.28% in 2024, with Brazil’s Embraer and South Africa’s Denel expanding regional forging capabilities through international collaborations.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Integration and Regional Expansion Reshape Aerospace Forging Leadership

The aerospace cold forgings market features a mix of global forging companies, specialized Tier-1 suppliers, and emerging regional players, all forming a closely connected supply network. Leading firms such as Precision Castparts Corporation (PCC), Arconic, Howmet Aerospace, Otto Fuchs, and VSMPO-AVISMA dominate the industry by controlling every stage from alloy melting to final machining. Their long-term partnerships with major OEMs such as Boeing, Airbus, and Lockheed Martin provide them with an advantage in securing multi-year contracts for high-value parts such as turbine discs, landing gear, and structural assemblies. These companies continuously invest in automation, isothermal forging, and digital process monitoring to maintain consistency and meet certification standards for critical aerospace systems.

Meanwhile, a new group of regional and mid-sized competitors is changing the global market. Companies, namely Bharat Forge (India), Kobe Steel (Japan), Safran (France), and IHI Group (Japan), are quickly increasing their aerospace forging capacity to serve local and export markets. Their focus on closed-die, hybrid cold-warm forging and lightweight alloy processing makes them flexible alternatives to traditional Western suppliers. This shift is creating a more balanced, multi-regional industry where technology leadership remains in the West, but growth is increasingly moving toward Asia-Pacific and selective defense hubs in Europe and the Middle East.

LIST OF KEY AEROSPACE COLD FORGINGS COMPANIES PROFILED

- Precision Castparts Corporation (PCC) (U.S.)

- Arconic Corporation (U.S.)

- Howmet Aerospace Inc. (U.S.)

- Otto Fuchs KG (Germany)

- VSMPO-AVISMA Corporation (Russia)

- Bharat Forge Ltd. (India)

- Kobe Steel Ltd. (Japan)

- Safran S.A. (Safran Landing Systems) (France)

- IHI Corporation (Japan)

- Allegheny Technologies Incorporated (U.S.)

- Aerosud Aviation (Denel Group) (South Africa)

- Sumitomo Metal Industries, Ltd. (Japan)

- LISI Aerospace (France)

- Magellan Aerospace Corporation (Canada)

- Doncasters Group Ltd. (U.K.)

- MTU Aero Engines AG (Germany)

- GKN Aerospace (Melrose Industries) (U.K.)

- RTI International Metals (U.S.)

- Aichi Steel Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- In February 2025, Arconic Corporation (U.S.) expanded its closed-die forging facility in Cleveland, Ohio. The company added new titanium and nickel alloy forging lines to support high-precision components for the next-generation aircraft programs of Airbus and Boeing.

- In October 2024, Safran Landing Systems and Bharat Forge (India) set up a joint aerospace forging center in Hyderabad. This center focuses on producing landing gear and engine mount forgings using hybrid cold-warm processes for both civil and defense applications.

- In June 2024, Howmet Aerospace (U.S.) implemented AI-driven forging and inspection systems at its manufacturing site. These systems improve precision and reduce defects in titanium and aluminum components used in GE and Pratt & Whitney engine assemblies.

- In May 2024, Airbus (Europe) successfully reduced its reliance on Russian titanium to below 10%. This was achieved after securing long-term supply contracts with Toho Titanium (Japan) and UKTMP (Kazakhstan) to strengthen its material resilience strategy.

- In December 2024, Otto Fuchs KG (Germany) modernized its forging plant in Meinerzhagen with energy-efficient hydraulic presses and digital simulation controls. This change reduced production energy use by nearly 15%, in line with EU sustainability standards.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.40% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material Type · Aluminum Alloys · Titanium Alloys · Stainless Steel · Nickel-Based Superalloys · Carbon & Alloy Steel |

|

By Component Type · Shafts & Spindles · Landing Gear Components · Engine & Turbine Discs · Structural Fittings · Fasteners & Bolts · Rings & Flanges · Others (Brackets, Rods, Bushings) |

|

|

By Aircraft Type · Commercial Narrow-Body Aircraft · Wide-Body & Long-Range Aircraft · Military Fighters & Rotorcraft · Transport Aircraft & UAVs · Business Jets |

|

|

By Application · Engine Systems · Landing Gear Systems · Airframe Structures · Control Systems · Auxiliary Systems · Others |

|

|

By Forging Technology · Conventional Cold Forging · Closed Die / Impression Forging · Open Die Forging · Roll & Upset Forging · Others (Precision / CNC-Controlled Forging, Hybrid (Cold + Warm) Forging) |

|

|

By End User · OEMs · Tier-1 & Tier-2 Suppliers · MRO Service Providers · Defense & Government Procurement Agencies |

|

|

By Region · North America (By Material Type, By Component Type, By Aircraft Type, By Application, By Forging Technology, By End User, and By Country) o U.S. (By Material Type) o Canada (By Material Type) · Europe (By Material Type, By Component Type, By Aircraft Type, By Application, By Forging Technology, By End User, and By Country) o U.K. (By Material Type) o Germany (By Material Type) o France (By Material Type) o Italy (By Material Type) o Russia (By Material Type) o Rest of Europe (By Material Type) · Asia-Pacific (By Material Type, By Component Type, By Aircraft Type, By Application, By Forging Technology, By End User, and By Country) o China (By Material Type) o India (By Material Type) o Japan (By Material Type) o South Korea (By Material Type) o Singapore (By Material Type) o Rest of Asia-Pacific (By Material Type) · Rest of the World (By Material Type, By Component Type, By Aircraft Type, By Application, By Forging Technology, By End User, and By Country) o Latin America (By Material Type) o Middle East & Africa (By Material Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market size is projected to grow from USD 5.84 billion in 2026 to USD 10.59 billion by 2034

In 2025, the market value stood at USD 1.91 billion.

The market is expected to exhibit a CAGR of 7.40% during the forecast period of 2026-2034.

The aluminum alloys segment led the market by material type.

Lightweight-material demand spurs aerospace cold forgings market growth.

Precision Castparts Corporation (PCC) (U.S.), Arconic Corporation (U.S.), Howmet Aerospace Inc. (U.S.), Otto Fuchs KG (Germany), VSMPO-AVISMA Corporation (Russia), Bharat Forge Ltd. (India), Kobe Steel Ltd. (Japan), Safran S.A. (Safran Landing Systems) (France), IHI Corporation (Japan), Allegheny Technologies Incorporated (U.S.), and Aerosud Aviation (Denel Group) (South Africa) are the top companies in the Aerospace Cold Forgings market.

North America dominated the market in 2024.

Seeking Comprehensive Intelligence on Different Markets?Get in Touch with Our Experts

Speak to an Expert

- 2021-2034

- 2025

- 2021-2024

- 200

Download Free Sample

Jump to Content

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Aerospace & Defense

Clients

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us