Aerospace Titanium Market Size, Share & Industry Analysis, By Alloy Grade (Ti-6Al-4V, Ti-3Al-2.5V, Ti-5Al-2.5Fe, Ti-7Al-4Mo, and Others), By Type (Plate, Sheets, Bars, Rods, Tubes, and Pipes), By Technology (Casting , Forging, Powdering, Rolling, and Others), By Application (Aircraft Structures, Aircraft Engines, Spacecraft, Missiles, and Industrial Application), By Platform (Commercial Aviation, Military Aviation , Space Systems, and General Aviation), By End User (OEMs, Tier 1 Suppliers, MROs & Aftermarket, and Defense & Space Contractors), and Regional Forecast, 2026-2034

Aerospace Titanium Market Size and Future Outlook

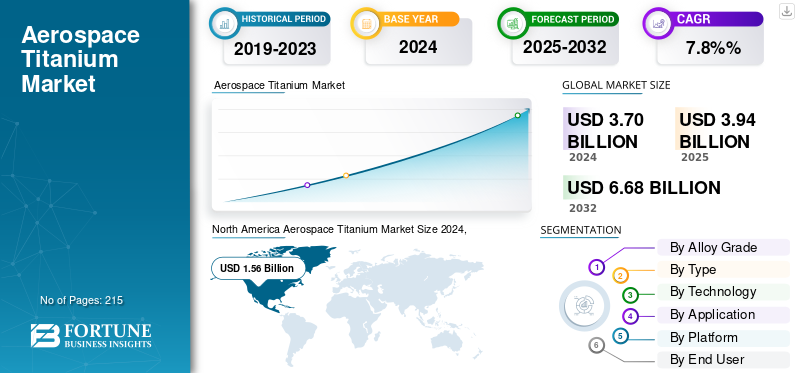

The global aerospace titanium market size was valued at USD 3944.4 million in 2025. The market is projected to grow from USD 4218.6 million in 2026 to USD 7,562.60 million by 2034, exhibiting a CAGR of 7.60% during the forecast period.

The aerospace titanium market encompasses the production and utilization of titanium and its alloys for critical applications across aircraft, spacecraft, and defense platforms. Owing to its exceptional strength-to-weight ratio, corrosion resistance, and high-temperature stability, titanium serves as a fundamental structural and engine material in both commercial and military aviation. It is extensively used in airframes, landing gear components, compressor blades, fasteners, and high-pressure hydraulic systems, where durability and fatigue resistance are essential under demanding operational conditions.

Government and defense agencies, including the Federal Aviation Administration (FAA), the European Union Aviation Safety Agency (EASA), and the U.S. Department of Defense (DoD), regulate the qualification and certification of aerospace-grade titanium alloys under rigorous standards such as AMS, ASTM, and MIL-SPEC. These frameworks ensure metallurgical consistency, traceability, and performance compliance for critical flight hardware.

Leading industry participants such as Timet (Precision Castparts Corporation), VSMPO-Avisma, ATI Inc., Toho Titanium Co., Kobe Steel Ltd., and Arconic Corporation are major suppliers of titanium sponge, billet, and forging for aerospace OEMs. Downstream, Airbus, Boeing, Lockheed Martin, and GE Aerospace integrate titanium into advanced airframes and propulsion systems to achieve weight reduction, improved fuel efficiency, and thermal performance. Emerging manufacturing technologies especially additive manufacturing (AM) and near-net-shape forging are revolutionizing titanium utilization by minimizing material waste and enabling complex geometries for next-generation aircraft and reusable launch systems.

Download Free sample to learn more about this report.

AEROSPACE TITANIUM MARKET Key Takeaways

- 2025 Market Size: USD 3,944.4 Million

- 2026 Market Size: USD 4,218.6 Million

- 2034 Forecast Market Size: USD 7,562.6 Million

- CAGR: 7.60% from 2026–2034

- North America dominated the aerospace titanium market with a 42.00% share, generating USD 1,660.8 million in 2025.

- The Ti-6Al-4V segment is projected to account for 58.42% of the market share in 2026.

- The aircraft engines segment is expected to hold a 40.51% market share in 2026.

North America

North America generated USD 1,660.8 million in 2025 and is projected to reach USD 1,772.4 million in 2026.

Europe

Europe accounted for USD 1,198.1 million in 2025 and is expected to reach USD 1,285.2 million in 2026.

Asia Pacific

Asia Pacific generated USD 700.8 million in 2025 and is projected to reach USD 757.3 million in 2026.

U.S.

The aerospace titanium market is projected to reach USD 1,526.2 million in 2026.

Japan

The aerospace titanium market is projected to reach USD 114.8 million in 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing Aircraft Production and Inclination Toward Sustainable Materials to Propel Titanium Adoption

The continuous expansion in global commercial and defense aircraft production is a key driver fueling the aerospace titanium market. Commercial OEMs such as Airbus and Boeing are scaling up monthly build rates for next-generation models, such as the A320neo, A350, 737 MAX, and 787 Dreamliner, all of which incorporate significant titanium content to optimize strength and reduce weight.

- For instance, in October 2025, the U.S. Federal Aviation Administration approved Boeing to raise its 737 MAX production rate from 38 to 42 aircraft per month, reflecting about a 10.5% increase in output.

Titanium’s high strength-to-weight ratio, fatigue resistance, and compatibility with composite structures help improve fuel efficiency and achieve targets demanded by modern aviation programs. Moreover, the rising fleet replacement cycle and increasing use of widebody aircraft for long-haul operations are intensifying titanium demand in both airframe and engine applications. The push toward net-zero aviation and sustainable materials further amplify titanium’s relevance over aluminum and steel alternatives.

MARKET RESTRAINTS

High Cost and Energy-Intensive Processing to Limit Market Expansion

Aerospace titanium market faces significant restraints due to the high cost and complexity of titanium extraction and processing. The Kroll process, the industry’s primary production route, is highly energy-intensive and produces limited yield, resulting in elevated sponge and billet costs compared to aluminum or steel alloys. Moreover, machining titanium components involves substantial tool wear, long cycle times, and high scrap generation, further inflating production costs. The volatility of raw material prices particularly due to dependence on a limited number of global producers supports, also heightens procurement risk for OEMs and Tier-1 suppliers. All such factors are expected to hamper the aerospace titanium market growth during the forecast period.

MARKET OPPORTUNITIES

Rising Investment into Hypersonic and Reusable Launch Systems Provides Significant Opportunities Market

The accelerating global investment in hypersonic vehicles, reusable launch systems, and deep-space platforms presents a compelling growth opportunity for the aerospace titanium market. Titanium alloys offer exceptional performance in extreme environments such as high temperatures, high stresses, and rapid dynamic loading, which makes them highly suited for next-generation space- and defense-platform materials. For instance, the push toward reusable rocket stages drive demand for lightweight, high strength materials, and high strength-to-weight and thermal stability fit provided by titanium. Moreover, space launch and hypersonic programs are increasingly transitioning from legacy aluminum or nickel-based alloys to titanium and advanced titanium alloys to achieve performance gains, thereby driving market growth.

AEROSPACE TITANIUM MARKET TRENDS

Integration of Titanium Alloys with Composite Airframes in Next-Generation Aircraft

A prominent trend shaping the aerospace titanium market is the growing integration of titanium alloys with advanced composite materials in modern airframe and engine design. As manufacturers pursue lighter, stronger, and more fuel-efficient aircraft, titanium has emerged as the preferred metal for structural interfaces adjoining carbon-fiber-reinforced polymer (CFRP) components. Its exceptional corrosion resistance, thermal compatibility, and non-galvanic interaction with composites make it ideal for hybrid structures such as fuselage frames, engine pylons, and landing gear fittings. Aircraft models such as the Boeing 787 Dreamliner and Airbus A350 exemplify this design evolution, incorporating up to 15% titanium by weight to complement extensive composite use. This material pairing reduces overall aircraft weight and also enhances fatigue life and maintenance reliability.

MARKET CHALLENGES

Persistent Supply Constraints and Extended Lead Times Impacting Production Efficiency

The aerospace titanium industry continues to face structural challenges related to limited raw material availability and prolonged supply lead times. The global supply of aerospace-grade titanium sponge and forged products is concentrated among a small number of qualified producers, creating vulnerability to geopolitical and logistical disruptions. The reduction of exports from Russia historically one of the largest titanium suppliers has exacerbated this imbalance, placing sustained pressure on downstream manufacturing capacity. Certification of new suppliers under FAA, EASA, and OEM material standards requires multi-year qualification cycles, preventing rapid adjustments to evolving demand. As a result, lead times for titanium billets and forgings have increased considerably, influencing component delivery schedules and overall aircraft production timelines.

Download Free sample to learn more about this report.

Segmentation Analysis

By Alloy Grade

Broad Utilization Across Engine Structures Boosted Ti-6Al-4AV Segment Growth

On the basis of alloy grade, the market is classified into Ti-6Al-4V, Ti-3Al-2.5V, Ti-5Al-2.5Fe, Ti-7Al-4Mo, and others.

The Ti-6Al-4V segment will accounting for the largest share of 58.42% in 2026, attributed to its extensive utilization across both airframe and engine structures in commercial and defense aircraft. The superior strength-to-weight ratio, corrosion resistance, and fatigue performance make this alloy grade the standard material for compressor blades, fasteners, landing gear, and critical load-bearing components. It is also preferred for composite-to-metal interfaces in advanced aircraft such as the Boeing 787 Dreamliner, Airbus A350, and F-35 Lightning II, due to its thermal and galvanic compatibility.

The Ti-3Al-2.5V alloy is witnessing steady growth in the aerospace titanium market due to its superior strength-to-weight ratio and excellent formability, making it ideal for aircraft hydraulic tubing and structural components. Its strong resistance to corrosion and fatigue extends service life in harsh flight environments.

By Type

Rising Demand for High-Strength Titanium Plates Supported Segment Growth

Based on type, the market is segmented into plates, sheets, bars, rods, tubes, and pipes.

The plate segment will accounting for the largest share of 29.53% in 2026, owing to its extensive use in airframe and engine structures requiring high tensile strength and fatigue resistance. Plates are used for manufacturing fuselage skins, wing spars, and bulkheads due to their dimensional stability and machinability.

- For instance, in May 2025, ATI Inc. signed a multi-year contract with Airbus to supply titanium plate, sheet, and billet, significantly increasing ATI’s previous support and positioning it as a key supplier for Airbus’s aircraft production ramp-up.

The bars segment is projected to record significant growth, driven by increasing demand for precision-machined components such as landing gear parts, actuator housings, and engine pylons. Bars offer superior mechanical uniformity and are suitable for both structural and engine-grade titanium applications.

By Technology

High Strength and Fatigue Resistant Characteristics Encouraged Forging Segment Growth

Based on technology, the market is segmented into casting, forging, powdering, rolling, and others.

The forging segment will capture the largest share of 29.48% in 2026, supported by its ability to deliver high-strength, fatigue-resistant components with superior grain flow. Forged titanium parts are extensively used in landing gears, discs, and compressor blades for next-generation aircraft. Numerous aircraft manufacturers source forged titanium parts from suppliers for aerospace applications.

- For example, Boeing and Airbus source titanium sheets and forged parts from numerous sources such as ATI, Inc. and others.

The powdering segment is expected to grow at the fastest CAGR, driven by rapid adoption of additive manufacturing and near-net-shape part production. Titanium powder metallurgy is being used for weight reduction, material savings, and customization of complex geometries for aerospace and space systems.

- For instance, in July 2025, Tekna received a USD 1.14 million order for high-performance Ti64 titanium powder from a Tier-1 U.S. aerospace and defense supplier, marking a fivefold increase in monthly delivery volume for the second half of 2025 due to rising demand for Laser Powder Bed Fusion (LPBF) additive manufacturing.

By Application

Expanding Airframe Production and Structural Weight Optimization Drive Titanium Utilization

Based on application, the market is segmented into aircraft structures, aircraft engines, spacecraft, missiles, and industrial application. Aircraft structures includes fuselages, landing gear, and fasteners. The aircraft engine is further divided into compressor blades, casings, and discs. Titanium used in titanium for frames, tanks, and propulsion parts. Missiles comprises of airframes, fins & control surfaces, nose cones, propellant casings, and guidance section housings.

Moreover, industrial application is classified into tooling & fixtures, additive manufacturing feedstock, support structures for test rig, and ground support hardware.

The aircraft structures segment held the largest aerospace titanium market share in 2024, driven by extensive titanium use in fuselages, landing gears, and fasteners due to its high strength-to-weight ratio and corrosion resistance. Continuous efforts by OEMs to reduce structural weight and enhance airframe longevity are sustaining titanium adoption. The increase in use of titanium fasteners in aircraft assembly due to its high strength-to-weight ratio and high-temperature performance, is further supporting segment growth.

- For instance, in May 2024, IperionX and Vegas Fastener partnered to co-produce titanium alloy fasteners and precision components for the U.S. Army’s Ground Vehicle Systems Center, using IperionX’s advanced titanium technologies.

The aircraft engines segment will anticipating to record the highest market share with 40.51% in 2026, propelled by increasing production of high-bypass turbofan engines and a higher number of titanium components in compressor and turbine assemblies. The thermal and oxidation resistance enables reliable operation under extreme temperature and pressure cycles, driving demand for titanium in the manufacturing of aircraft engine components.

To know how our report can help streamline your business, Speak to Analyst

By Platform

Commercial Aircraft Segment Led, Driven by Robust Demand For Narrow- and Wide-Body Aircraft

Based on platform, the market is segmented into commercial aviation, military aviation, space systems, and general aviation.

The commercial aviation segment dominated the market in 2024, supported by robust demand for narrow- and wide-body aircraft amid passenger traffic recovery. Titanium is extensively used in airframes, engines, and fastening systems to reduce fuel burn and extend maintenance intervals. The surge in aircraft orders directly drives higher demand for titanium in the manufacturing of critical components such as airframes, engines, landing gear, and other structural parts.

- For instance, in September 2025, WestJet ordered 67 additional Boeing aircraft, including 60 737-10s and seven 787-9 Dreamliners, effectively doubling its Dreamliner fleet and expanding its total order book to 123 airplanes.

The space systems segment is anticipated to witness notable growth, propelled by expanding satellite constellations and reusable launch vehicle programs. Several countries are focusing on the production of high-quality titanium components needed for aviation and space exploration, which highlights its increased demand for high-quality components.

- For instance, in February 2025, IperionX received a contract worth up to USD 47.1 million from the U.S. Department of Defense to help build a strong, affordable titanium supply chain in the U.S., marking a combined investment of over USD 70 million for this effort.

By End User

OEM Segment Dominated due to Rising Engine Production

Based on end user, the market is segmented into OEMs, Tier 1 suppliers, MROs & aftermarket, and defense & space contractors.

The OEM segment accounted for the largest share in 2024, attributed to rising aircraft and engine production. OEMs are securing long-term titanium supply contracts to mitigate price volatility and ensure material continuity across assembly lines, thereby stimulating segment growth.

• For instance, in July 2025, ATI Inc. extended and expanded its long-term titanium supply agreement with Boeing, reinforcing its position as a key supplier of high-performance titanium materials for Boeing’s full range of commercial aircraft, including narrowbody and widebody programs.

The MROs & aftermarket segment is expected to grow at the fastest pace, driven by increased fleet utilization and part replacement cycles. MRO and aftermarket demand for titanium components is accelerating as airlines extend aircraft service lives and utilization rates, leading to shop visits for titanium-rich engines and airframe structures.

Aerospace Titanium Market Regional Outlook

By region, the market is divided into North America, Latin America, Asia Pacific, Europe, and the Middle East & Africa.

North America

North America holds the largest share of the aerospace titanium market and is expected to maintain its lead throughout the forecast period. The market in North America reached USD 1660.8 Million in 2025, representing 42.00% of total market revenue, and is projected to reach USD 1772.4 Million in 2026. The region benefits from the highest concentration of airframe and engine OEMs, extensive defense procurement (fighters, rotorcraft, missiles), and the world’s largest MRO footprint, all of which are titanium-intensive. The presence of titanium providers in U.S. such as TIMET, ATI Inc., is expected to drive the aerospace titanium market demand. Moreover, these companies are focused on increasing their production capacity to supply high-quality titanium for the aerospace sector. The U.S. market is projected to reach USD 1526.2 million by 2026.

North America Aerospace Titanium Market Size 2025, (USD Million)

To get more information on the regional analysis of this market, Download Free sample

• For instance, in June 2025, ATI Inc. opened a state-of-the-art titanium alloy sheet production facility in Pageland, South Carolina, which produces ultra-thin, high-quality titanium sheets critical for aerospace aerostructures.

Europe

Europe contributed approximately USD 1198.1 Million to the global market in 2025, accounting for 30.40% share, and is expected to reach USD 1285.2 Million in 2026. Europe is projected to witness substantial growth, supported by Airbus and leading engine primes, robust defense modernization, and coordinated supply-chain resiliency initiatives. European stakeholders are investing in circular titanium (scrap recovery and revert programs) and additive-enabled near-net shaping to reduce buy-to-fly ratios and material waste. Moreover, there is surge in demand for high-performance titanium components used in military and defense applications. The UK market is projected to reach USD 283.08 million by 2026, while the Germany market is projected to reach USD 271.19 million by 2026.

• For instance, BAE Systems secured a USD 162 million contract to produce major titanium structures for the U.S. Army’s M777 lightweight howitzer, with production scheduled to start in 2026 at new facilities in the U.K. and the U.S.

Asia Pacific

In 2025, the Asia Pacific market stood at USD 700.8 Million, representing 17.80% of global demand, and is projected to grow to USD 757.3 Million in 2026. The Asia Pacific region is anticipated to be the fastest-growing market during the forecast period. Rising air traffic, expanding final-assembly and aerostructures work, and the maturation of regional engine MRO hubs are key drivers of the aerospace titanium market. In addition, countries such as China and India are leading this growth due to rising demand for lightweight, fuel-efficient aircraft, supportive government initiatives, and the presence of major titanium producers and fabricators. Countries in the region are also increasing its self-reliance in high-performance aerospace titanium and superalloy production, making the region a key hub for titanium consumption and production in aerospace. The Japan market is projected to reach USD 114.8 million by 2026, the China market is projected to reach USD 305.23 million by 2026, and the India market is projected to reach USD 112.79 million by 2026.

- For instance, in July 2025, PTC Industries, located in the Uttar Pradesh Defence Industrial Corridor in India, invested nearly USD 113.8 million to establish four manufacturing plants dedicated to producing titanium and superalloy materials for both domestic and global defense needs.

Latin America

The Latin America market accounted for USD 162.93 Million in 2025, representing 4.13% of the global industry, and is expected to reach USD 169.83 Million in 2026. Latin America is experiencing gradual but steady growth, led by commercial and defense programs, the expansion of aerostructures manufacturing, and the rise of engine and component MRO centers serving the region. As fleets modernize and utilization rises, titanium usage grows in landing gear, fasteners, nacelles, and engine components, with cost-efficient repair capabilities gaining traction. Partnerships with North American and European suppliers are helping qualify local manufacturers qualify for certified titanium machining and restoration processes.

Middle East & Africa

The Middle East & Africa (MEA) region is poised for notable growth, driven by large commercial fleet expansions, defense procurement, and the emergence of advanced manufacturing and MRO hubs. Middle East & Africa maintained a strong presence in the global market, reaching USD 221.72 Million in 2025, accounting for 5.62% share, and is expected to reach USD 233.86 Million in 2026. Investments in modernizing military aircraft and boosting commercial aviation infrastructure fuel demand for lightweight, corrosion-resistant titanium materials, driving growth of the Middle East Africa aerospace titanium market.

COMPETITIVE LANDSCAPE

Key Industry Players

Titanium Innovation, Integrated Supply Chains, and Emerging Regional Players Drive Leadership in the Aerospace Titanium Market

The aerospace titanium market is highly competitive with, established global leaders such as ATI, Timet, and VSMPO-AVISMA leveraging advanced titanium alloy technologies, integrated supply chains, and long-term contracts with major OEMs such as Boeing and Airbus. These companies maintain strong innovation pipelines, expanding production capacities, and sustainability initiatives, enabling them to maintain technological leadership and respond to increasing demand from commercial and defense sectors.

Additionally, emerging players from Asia Pacific and other regions are gaining traction through cost-competitive manufacturing capabilities and localized market expertise, thereby intensifying competition. The market is also evolving with technological advancements such as additive manufacturing, powder metallurgy, and advanced coatings, which are expanding application of titanium in new aerospace segments such as hybrid and electric propulsion.

LIST OF KEY AEROSPACE TITANIUM COMPANIES PROFILED

- VSMPO-AVISMA Corporation (Russia)

- ATI Inc. (U.S.)

- Timet (Titanium Metals Corporation) (U.S.)

- Plymouth Tube Company (U.S.)

- Precision Castparts Corporation (U.S.)

- Toho Titanium Co., Ltd. (Japan)

- Osaka Titanium Technologies Co., Ltd. (Japan)

- Carpenter Technology Corporation (U.S.)

- Allegheny Technologies (U.S.)

- BaoTi Group Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- May 2025, ATI Inc. signed a multi-year agreement with Airbus SE to supply titanium plate, sheet, and billet, supporting the ramp-up in production of narrow- and wide-body aircraft.

- April 2025, Airbus signed a USD 666.5 million deal to source titanium from Saudi Arabia, as part of a broader agreement involving the Kingdom’s national airline, Saudia, which ordered 20 A330neo aircraft.

-

April 2024, Airbus Aerostructures and Norsk Titanium signed a master supply agreement for the delivery of titanium parts, aimed at reducing Airbus’ dependency on Russian titanium raw materials.

- April 2024: Norsk Titanium entered a long-term Master Supply Agreement with Airbus Aerostructures GmbH for recurring production of titanium parts for the A350 aircraft program.

- September 2023: AMG Critical Materials N.V. and Titanium Metals Corporation (TIMET) announced a partnership to establish a new multi-hundred million-dollar titanium melt facility in Ravenswood, West Virginia, dedicated to supplying aerospace-grade titanium products.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size and forecast by all market segments included in the report. It includes details on the market dynamics, and market trends expected to drive the market in the forecast period. The market report includes porter’s five forces analysis which illustrates the potency of buyers suppliers in the market. The market forecast offers information on the technological advancements, new product launches, key trends, major industry developments, and details on partnerships, and mergers & acquisitions. The market analysis also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attributes | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.60% from 2026-2034 |

| Unit | Value (USD million) |

| Segmentation | By Alloy Grade, By Type, By Technology, By Application, By Platform, By End User, and Region |

| By Alloy Grade |

|

| By Type |

|

| By Technology |

|

| By Application |

|

| By Platform |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3944.4 million in 2025 and is projected to reach USD 7,562.60 million by 2034.

In 2025, the market value stood at USD 1660.8 million.

The market is growing at a CAGR of 7.60% during the forecast period (2026-2034).

The aircraft structures segment led the market by application.

The key factor driving the growth of market is increasing aircraft production

VSMPO-AVISMA Corporation (Russia), ATI Inc. (U.S.), TIMET (U.S.) are some of the prominent players in the market.

North America dominate the market.

- 2021-2034

- 2025

- 2021-2024

- 215

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us