Aerospace Valves Market Size, Share & Industry Analysis, By Type (Butterfly Valves, Ball Valves, Rotary Valves, Gate Valves, Other), By Aircraft Type (Commercial Aircraft, General Aviation Aircraft, Business Aircraft, Military Aircraft, Helicopter), By Application (Fuel System, Hydraulic System, Pneumatic System, Lubrication System, Others), By End Use (OEM and Aftermarket) and Regional Forecast, 2026-2034

Aerospace Valves Market Size & Industry Analysis

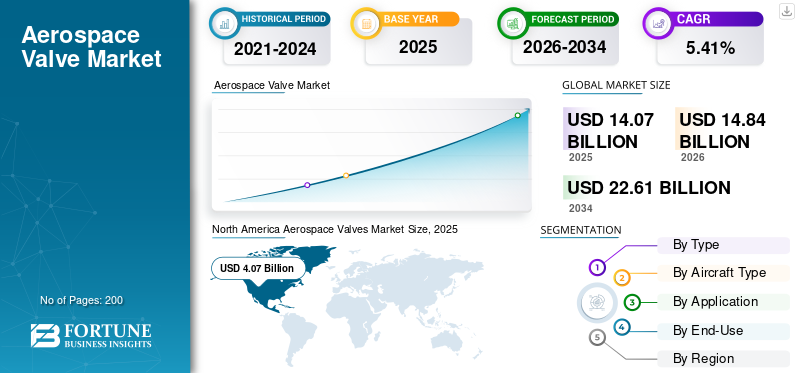

The global aerospace valve market size was valued at USD 14.07 billion in 2025. The market is projected to grow from USD 14.84 billion in 2026 to USD 22.61 billion by 2034, exhibiting a CAGR of 5.41% during the forecast period. North America dominated the aerospace valve market with a market share of 39.06% in 2025.

The aerospace valve is an important part of the aviation system as it controls the flow of gases or fluids by opening and shutting a path. Different types of valves are used in an airplane, depending upon application and pressure requirements. The global market has been driven by factors such as a rise in aircraft fleet size, frequent need for replacement of valves, and others.

Download Free sample to learn more about this report.

Aerospace Valve Market KEY TAKEAWAYS

- 2025 Market Size: USD 14.07 Billion

- 2026 Market Size: USD 14.84 Billion

- 2034 Forecast Market Size: USD 22.61 Billion

- CAGR: 5.41% from 2026–2034

- North America dominated the aerospace valve market with a 39.06% share in 2025.

- The butterfly valves segment is anticipated to grow at the highest CAGR.

- The commercial aircraft segment is expected to hold a 29.3% market share.

North America

Growth is driven by a large aircraft fleet, leading OEMs, and the presence of major aerospace valve manufacturers.

Europe

Growth is supported by aircraft fleet modernization, increasing air travel, and strong aerospace manufacturing capabilities.

Asia Pacific

Rapid growth is driven by rising aviation investments, increasing aircraft orders, and expanding passenger traffic.

U.S.

The market is driven by a large commercial and defense aircraft fleet, strong OEM presence, and continuous aircraft production.

Japan

The market is supported by increasing aviation investments, fleet expansion, and growing demand for advanced aerospace components.

Read More

Aerospace Valve Market Trends

Integration of Internet of Things (IOT) with Aerospace Valves to Bolster Market Outlook

The aviation sector is integrating advanced technologies such as Internet of things (IoT) into valves to enable smarter operations. IoT helps to enhance the efficiency of control valves and cut maintenance costs over the lifecycle of valves. The technology provides numerous benefits to airliners by enabling regular valve health monitoring and downtime prevention through timely fault warnings. The data received from the IoT-powered valves helps make smarter decisions in addition to basic functionality such as opening, closing, and flow modulation. Thus, the integration of IoT into valves could create massive opportunities for manufacturers in the forthcoming years.

Download Free sample to learn more about this report.

Aerospace Valve Market Growth Factors

Surge in the Acquisition of New Aircraft Triggered by the Increasing Demand for Air Travel to Fuel Growth

Robust economic development and increased travel is leading to rising air passenger traffic.

The growing number of air passengers has widely driven the procurement of new aircraft. Aircraft manufacturing companies have increased their production owing to increased aircraft orders. OEMs such as the Boeing Company and Airbus are anticipating substantial recovery of aerospace sector post-COVID-19 pandemic.

Airbus aims to increase the manufacturing of A320 family of aircraft to 45 aircraft per month by 2021 end. Moreover, the company aims to ramp up production to 64 aircraft per month by June 2023, and 70 aircraft per month by 2024.

The International Air Transport Association (IATA) reports that the number of air travelers could double to hit 8.2 billion by 2037.

The rising demand for air travel has led airline companies to expand their aircraft fleet, which is expected to augment the market growth during the forecast period.

Regular Replacement of Valves Due to the Increased Flight Hours to Fuel Market Growth

Due to rising air travel, aircraft flight hours have increased substantially, leading to wear & tear of valves. The life cycle of valves depends on the number of calendar days and flight hours. The average MTBUR (Mean Time Between Unscheduled Removal) of valves is between 9,000 and 100,000 cycles. Since valves cannot be refurbished, they need to be replaced at the end of their lifecycle. These factors indicate a lucrative opportunity for aerospace OEMs.

RESTRAINING FACTOR

Frequent Alterations in Raw Material Prices Hampers the Market Growth

The volatility in prices of raw materials such as steel, iron, alloys, and others is due to an imbalance in its supply and demand. Thus, the fluctuations in the prices of raw materials are anticipated to restrain the growth of the market.

Aerospace Valve Market Segmentation Analysis

By Type Analysis

Butterfly Valve Segment to Grow at Faster Rate Owing to its Extensive Use in Fuel and Pneumatic Systems

By type, the aerospace valves market share is divided into butterfly valve, ball valve, rotary valve, gate valve, and others.

The butterfly valves segment is anticipated to grow at higher CAGR through the projection period owing to the extensive usage of butterfly valves in various applications such as fuel systems and pneumatic systems of an aircraft. The ease of use, compact size, and fewer space requirements of butterfly valves is the reason for their higher adoption.

The ball valve segment is anticipated to showcase significant growth in the market owing to its adoption in aircraft turbines to maximize the efficiency of the turbines.

By Aircraft Type Analysis

To know how our report can help streamline your business, Speak to Analyst

Commercial Aircraft Segment to Lead the Market Due to Increasing Number of Aircraft Deliveries

Based on the aircraft type, the market is classified into commercial aircraft, business aircraft, military aircraft, general aviation aircraft, and helicopters.

The commercial aircraft segment is estimated to lead the market by aircraft type owing to the rising number of commercial aircraft deliveries. Airbus delivered 127 commercial jets in the third quarter of 2021.

- The commercial aircraft segment is expected to hold a 29.3% share in 2020.

The military aircraft segment is anticipated to showcase substantial growth through the forecast period owing to the growing spending by the governments of various countries to strengthen their air defense capabilities.

By Application Analysis

Pneumatic System Segment to Witness Highest Growth Owing to Replacement of Hydraulic Systems with Pneumatic Systems

Based on application, the market is segmented into the fuel system, hydraulic system, pneumatic system, lubrication system, and others.

The hydraulic system segment was expected to hold highest market share in 2020. The growth of the segment in the market can be attributed to the extensive use of valves in hydraulic systems in various components of aircraft such as landing gear, brakes, flaps, and others.

The pneumatic system segment is projected to grow at the highest CAGR during 2021-2028. The increasing need for replacing hydraulic systems with pneumatic systems to avoid oil leakage is expected to fuel the segment growth. Moreover, the rising demand to increase the efficiency of aircraft by decreasing fuel consumption is anticipated to aid the growth of the market.

By End-Use Analysis

OEM Segment Expected to Dominate Due to Rising Commercial Aircraft Deliveries

Based on the end-user, the market is bifurcated into OEM and aftermarket.

The OEM segment dominated the market in 2020 and will record the highest CAGR over 2021-2028. Aircraft valves are mainly installed by OEMs during the assembly stage, post which they are delivered to aircraft makers. A notable uptick in aircraft demand across regions is expected to fuel the segment growth.

The aftermarket segment is expected to grow significantly owing to the rise in the retrofit of technologically advanced aerospace valves into conventional aircraft.

In May 2021, Triumph Group was awarded a contract extension by the Boeing Company to supply critical system components for the 787 Dreamliner. The contract focuses on the provision of a high-valve system, geared solution, and MRO

REGIONAL INSIGHTS

The global market is segmented, based on region, into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Aerospace Valves Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America is anticipated to hold the largest market share in the global aerospace valve market during the projection period owing to the presence of a large aircraft fleet in the U.S. The market in North America stood at USD 4.07 billion in 2020. Moreover, the existence of dominant aircraft producers such as the Boeing Company and others, along with the presence of key market players such as Moog, Inc., Triumph Group, Parker Hannifin Corp., and others drives the growth of market in North America.

Asia Pacific

In Asia Pacific (APAC), the market is predicted to showcase exceptional growth through the projection period. The growth is attributed to the growing funding in the aviation industry by emerging countries such as China, Japan, India, and others. The rising orders of new aircraft to increase fleets to meet the rising air passenger traffic is predicted to augment the growth of the market in APAC.

Europe

The market in Europe is expected grow significantly owing to the increase in demand for modernization of aircraft fleet, rise in travel and tourism, and advanced technology. Moreover, countries such as France, Russia, and Germany have large aircraft fleets which are expected to support the market growth.

rest of the world

In rest of the world, the aerospace valve market is expected to witness a moderate growth owing to the rise in travel and business opportunities, new aircraft purchase plans in countries such as Israel, Saudi Arabia, Turkey, and others.

KEY INDUSTRY PLAYERS

Key Players Are Investing in New Technologies such as Internet of Things (IoT) to Improve Valve Operations and Decision Making

Major players are dedicated to introduce innovative technologies such as IoT, Augmented Reality, and others to increase efficiency of the valve, thus increasing efficiency of the aircraft. Manufacturers are implementing growth strategies such as partnerships, mergers, and acquisitions with aircraft OEMs.

List of Top Aerospace Valve Companies:

- Eaton Corporation PLC (Ireland)

- Safran SE (France)

- Woodward Inc. (U.S.)

- Triumph Group (U.S.)

- Parker Hannifin Corporation (U.S.)

- Moog Inc. (U.S.)

- Crissair Inc. (U.S.)

- Liebherr (Germany)

- Porvair PLC (U.K.)

KEY INDUSTRY DEVELOPMENTS

- June 2021 – Triumph group was awarded a contract by Lockheed Martin Corporation to provide its hydraulic utility actuation valves (HUAVs) to support F-35 fleet readiness at Marine Corps Air Station (MCAS) Cherry Point.

- May 2021 – Valcor Engineering Corporation launched a Modulating Control Valves (MCV) which can perform flow control in systems such as pneumatic, avionics cooling systems, and hydraulic systems. These valves can also be used for controlling aviation fuel flow and Polyalphaolefin (PAO) control

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The global aerospace valves market report provides a detailed analysis of the market and focuses on key aspects, such as key players, valve types, Aircraft Types, and application of aerospace valves in an aircraft. Moreover, the research report offers insights on market trends, competitive landscape, market competition, product pricing, market status, and highlights key industry developments. In addition to the factors mentioned above, the market report encompasses several direct and indirect factors that have contributed to the sizing of the global market over recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

Type; Aircraft Type; Application, End Use, and Geography |

|

By Type

|

|

|

By Aircraft Type

|

|

|

|

By Application

|

|

|

By End-Use

|

|

By Geography

|

|

Frequently Asked Questions

According to Fortune Business Insights, the global aerospace valves market size was USD 14.07 billion in 2025 and is projected to grow from USD 14.84 billion in 2026 to USD 22.61 billion by 2034, exhibiting a CAGR of 5.41% during 2026–2034.

Registering a CAGR of 5.41%, the market will exhibit moderate growth in the forecast period (2026-2034).

Growth is driven by rising aircraft fleet sizes, increasing air passenger traffic, frequent valve replacements due to high flight hours, and technological advancements such as IoT-enabled valves for real-time monitoring and predictive maintenance.

North America held the largest share at 39.06% in 2025, supported by major OEMs like Boeing and key suppliers such as Parker Hannifin, Moog, and Triumph Group. This dominance is attributed to a large commercial and military aircraft fleet and strong manufacturing infrastructure.

Major valve types include butterfly valves, ball valves, rotary valves, and gate valves. Butterfly valves are expected to grow fastest due to their lightweight design, compact size, and extensive use in fuel and pneumatic systems.

Commercial aircraft lead the market due to rising deliveries from manufacturers like Airbus and Boeing, followed by military aircraft and helicopters driven by defense modernization programs.

Valves are used in fuel systems, hydraulic systems, pneumatic systems, and lubrication systems. The shift from hydraulic to pneumatic systems is a notable trend to reduce leakage risks and enhance fuel efficiency.

Key players include Eaton Corporation, Safran, Woodward Inc., Triumph Group, Parker Hannifin, Moog Inc., Crissair, Liebherr, and Porvair PLC, focusing on innovations like IoT-integrated and lightweight valve designs.

Trends include integration of IoT for predictive maintenance, development of lightweight composite valves, and rising demand from emerging aviation markets such as China and India due to growing passenger traffic.

The market is set to grow steadily as global air travel increases, aircraft fleets expand, and airlines replace aging components with advanced, efficient valves. Asia-Pacific is expected to record the fastest growth due to expanding aviation infrastructure.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us