Affordable Luxury Fashion Market Size, Share & Industry Analysis, By Type (Apparel, Footwear, Accessories, and Beauty & Fragrance), By Price Positioning (Entry-Level, Upper Affordable, and Bridge-to Luxury), By Age Group [16-25 Years (Gen Z), 26–40 years (Millennials), 41–60 years (Gen X), and 60+ years (Boomers & Older)], By Gender (Women, Men, and Unisex), By Distribution Channel (Specialty Retailing Stores, Brand Stores, Online channels, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

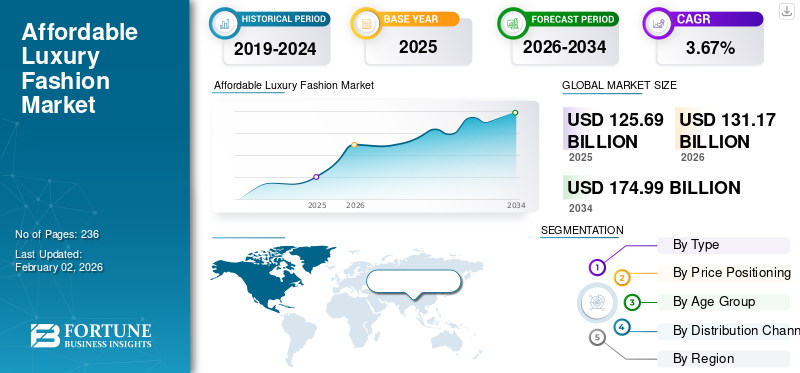

Affordable Luxury Fashion Market Size and Future Outlook

The global affordable luxury fashion market size was valued at USD 125.69 billion in 2025 and is projected to grow from USD 131.17 billion in 2026 to USD 174.99 billion by 2034, exhibiting a CAGR of 3.67% during the forecast period. North America dominated the affordable luxury fashion market with a market share of 35.27% in 2025.

The affordable luxury fashion goods market combines premium design and quality with affordable pricing, appealing to ambitious millennial and Gen Z consumers seeking status without paying full luxury rates. It is driven by rising middle-class affluence, digitalization, and shifting tastes among millennials and Generation Z, who value both style and brand legacy. Craftsmanship and storytelling are important for brands that leverage social media and e-commerce to drive interaction. As the market grows, it faces intense competition and pressure to preserve exclusivity. Sustainability, transparency, and tailored experiences are progressively influencing this market.

Tapestry, Inc., Ralph Lauren Corporation, Capri Holdings Limited, Estee Lauder Companies, Inc., and Tory Burch LLC. are the leading players in the worldwide market. These brands maintain their edge by emphasizing craftsmanship, expanding digital strategies, and appealing to younger demographic, style-conscious consumers seeking attainable prestige.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

AI-driven Personalization Technology Innovations to Improve Affordable Luxury Fashion Shopping Experience Fuel Market Growth

Innovation in retail technology, such as virtual try-ons and AI-driven personalization, is transforming the affordable luxury fashion shopping experience by allowing customers to witness products such as shoes, bags, and accessories on themselves virtually before buying. Leading luxury brands such as Gucci, Burberry, Chanel, and Louis Vuitton offer AR-based virtual try-on features that enable personalized and realistic product visualization, allowing customers to adjust size, color, and positioning for a tailored experience. AI and computer vision technologies underpin these tools by accurately mapping facial and body features, enhancing customer confidence, and reducing purchase hesitation. This technology also supports brand engagement through social media sharing and immersive campaigns, thus driving affordable luxury fashion market growth and customer satisfaction.

MARKET RESTRAINTS:

High Production Costs of Luxury Fashion Goods to Restrict Market Expansion

High production and material procurement costs of affordable luxury fashion goods pose challenges for key brands in maintaining business profitability. Affordable luxury brands differentiate themselves from fast fashion by offering higher-quality materials (e.g., top-grain leather, silk blends, and eco-friendly fabrics). Unlike fast fashion, they maintain fabric quality without undermining brand perception. These premium inputs are inherently more expensive, often subject to global commodity price fluctuations, restraining the global market expansion.

MARKET OPPORTUNITIES:

Emergence of Genderless Fashion to Create Newer Market Growth Opportunities

Genderless fashion refers to clothing and accessories designed without traditional gender distinctions, focusing on inclusive, versatile, and fluid styles. Brands target gender-biased upper-middle class and upper-income group of consumers that can afford luxury brands. It appeals especially to younger, progressive consumers who prioritize self-expression over gender norms. This creates an opportunity for affordable luxury brands to differentiate with minimalist, functional designs that resonate across demographics, expanding their addressable market while aligning with modern values of inclusivity and individuality.

AFFORDABLE LUXURY FASHION MARKET TRENDS:

Expansion of Omnichannel Retailing to Favor Market Growth

The expansion of omnichannel retailing in affordable luxury fashion blends online and offline channels to offer consumers a seamless, convenient, and personalized shopping experience. Retailers are integrating physical stores with e-commerce platforms, mobile apps, and social media to meet evolving consumer expectations for accessibility and immediacy. This approach enables consumers to interact with brands through multiple touchpoints, from in-store experiences to virtual shopping and direct digital engagement, enhancing customer loyalty and driving sales growth.

MARKET CHALLENGES:

Intense Competition from Fast Fashion Brands Offering Low-priced Alternatives to Challenge Key Players’ Business Expansion

Affordable luxury fashion brands face intense competition from fast fashion brands, which offer trendy designs at much lower prices, appealing to consumers seeking style and affordability without the premium cost. Fast fashion’s rapid production cycles and heavy social media presence allow it to quickly capitalize on trends, attracting younger, price-sensitive consumers who may prioritize immediacy over craftsmanship. While fast fashion replicates luxury aesthetics, it often sacrifices quality and sustainability, yet its affordability challenges luxury brands to justify their higher price points and exclusivity. This competitive pressure forces affordable luxury brands to emphasize their heritage, quality, and personalized experiences to maintain market share and customer loyalty.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

High Spending on Affordable Fashion Accessories to Boost Accessories Segment Growth

On the basis of type, the market is classified into apparel, footwear, accessories, and beauty & fragrance.

The accessories segment led the market accounting for 41.68% market share in 2026. The largest share of the accessories segment, which includes bags, hats, jewelry, and watches, is attributed to the significant consumer awareness and spending on affordable fashion accessories, including watches and jewelry. Accessories appeal widely across regions, driven by their role as a status symbol and a versatile fashion statement. They also benefit from high tourist demand in key markets and the rising trend toward personalization, making them a key growth driver within affordable luxury fashion. Leading brands continuously innovate within this segment to meet evolving consumer preferences and maintain competitiveness.

To know how our report can help streamline your business, Speak to Analyst

The beauty & fragrance segment is projected to grow at the fastest CAGR of 5.12% during the forecast period (2025-2032). This growth is driven by consumers' desire for authentic, artisanal products that emphasize craftsmanship and personal expression. Key trends include niche perfumes, sustainable formulations, and personalized scents, appealing particularly to younger generations seeking unique and meaningful olfactory experiences. Brands are blending tradition with innovation, using storytelling and digital engagement to deepen emotional connections with consumers.

By Price Positioning

High Middle-Income Consumers' Spending on Entry-Level Affordable Fashion Goods Led the Segment Growth

Based on price positioning, the market is categorized into entry-level, upper affordable, and bridge-to-luxury. The entry-level segment will account for 50.01% market share in 2026. The global demand for the entry-level affordable luxury fashion goods is mainly driven by the growing number of middle-class population seeking premium quality and brand prestige at accessible price points. This segment acts as a bridge between mass-market/ and affordable luxury brands, appealing especially to millennials and Gen Z who desire luxury experiences without exorbitant costs. Brands in this segment focus on offering aspirational designs with superior craftsmanship while leveraging digital channels and direct-to-consumer models. This pricing strategy enables wider market penetration and sustained growth, making entry-level affordable luxury the key driver of the market expansion.

The bridge-to-luxury segment is slated to grow at the fastest rate of 5.32% during the forecast period (2025-2032) as consumers seek premium quality and exclusivity at more attainable prices than traditional luxury. This segment benefits from rising demand for niche, artisanal fragrances and personalized beauty products that emphasize craftsmanship and unique identity. Brands leverage immersive retail experiences and digital innovation to deepen emotional connections, making this segment a key driver of market expansion in beauty and fragrance.

By Age Group

26–40 Years (Millennials) Segment Leads the Market Due to Their High Purchasing Power

Based on age group, the market is segmented into 16-25 years (Gen Z), 26–40 years (millennials), 41–60 years (Gen X), and 60+ years (boomers & older). The 26–40 years (millennials) segment is expected to account for 42.03% of the market in 2026, due to strong millennial consumers’ preferences for quality-based, affordable, and sustainably-made products. Millennials are highly engaged in online shopping, valuing seamless and secure digital experiences, and they prioritize ethical production and long-lasting, premium products. Their significant purchasing power and demand for authenticity make them the key consumer group driving segment growth.

The 16-25 years (Gen Z) segment is expected to witness the fastest growth at 4.90% during 2025-2032. Gen Z shoppers blend established luxury brands with trendy labels, influenced by social media and motivated by authenticity, sustainability, and individualized styles. They favor accessible luxury items and brands that engage them through digital innovation, influencer marketing, and inclusive, community-driven brand experiences.

By Gender

High Spending by Women Consumers on Premium-based Beauty Products Boosted the Segment Growth

Based on gender, the market is segmented into women, men, and unisex. The women's segment is anticipated to hold a dominant market share of 61.33% in 2026. Its largest share is due to the higher spending by women consumers on premium skincare, makeup, and fragrances. Women prioritize self-care, anti-aging, and innovative beauty solutions, fueling demand for high-quality, ethically produced products. The segment benefits from strong digital influence, celebrity endorsements, and expansion of e-commerce channels, driving continuous growth globally.

The unisex segment is slated to grow at the fastest rate of 5.77% during 2025-2032. The segment is gaining traction as brands introduce gender-neutral products such as bags, fragrances, and accessories that appeal to a broader and more inclusive consumer base. This segment resonates particularly well with younger generations, such as Gen Z, who value inclusivity and diversity in brand offerings. Luxury brands are expanding their unisex lines, leveraging digital engagement and personalized shopping experiences to attract new customers and drive growth within this evolving market category.

By Distribution Channel

Brand Stores Segment to Lead due to its Key Role in Maintaining Brand Exclusivity

Based on distribution channel, the market is segmented into specialty retailing stores, brand stores, online channels, and others. The brand stores segment is slated to exhibit a leading global market share of 41.57% in 2024. Brand stores play a pivotal role in maintaining brand exclusivity and delivering personalized, high-touch customer experiences. These stores serve as brand embassies, offering immersive retail environments, private appointments, and exclusive events that reinforce brand narratives and premium positioning. Luxury brands strategically use flagship and boutique stores to balance accessibility with prestige, ensuring that product presentation and customer service align with brand values. Integration with digital tools and experiential retail innovations further enhances engagement, driving both brand loyalty and sales growth.

The online channels segment is projected to grow at the fastest CAGR of 5.80% during the forecast period (2025-2032). The online channels segment is mainly driven by increasing digital literacy and smartphone penetration globally. Consumers, especially Millennials and Gen Z, prefer seamless, mobile-first shopping experiences enhanced by AI, augmented reality, and personalized services. Luxury brands are investing heavily in digital platforms, social commerce, and fast, white-glove delivery options to meet rising consumer expectations and expand their reach beyond traditional retail boundaries.

Affordable Luxury Fashion Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Affordable Luxury Fashion Market Size, 2025 (USD billion )

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America represented USD 44.33 billion, accounting for 35.27% of the worldwide market, and is projected to grow to USD 46.31 billion in 2026. The North American luxury market is robust, driven by a wealthy and fashion-conscious consumer base, including affluent millennials and Gen Z consumers. Social media, digital innovation, and the demand for sustainability and personalized experiences increasingly influence luxury purchases. Key cities such as New York, Los Angeles, and Toronto serve as luxury hubs with flagship stores and multimodal retail, while the online segment grows rapidly, catering to tech-savvy consumers. The market is expected to grow steadily, supported by rising disposable incomes and evolving luxury lifestyles focused on quality and exclusivity.

The U.S. affordable luxury fashion market size is expected to reach USD 41.69 billion by 2026. The U.S. market benefits from a high number of high-net-worth individuals and strong consumer demand for premium fashion, accessories, and experiential luxury. Digital innovation, social media influence, and sustainability are key growth drivers. The U.S. is also the largest online luxury market, generating significant e-commerce revenue driven by tech-savvy and younger affluent consumers.

Asia Pacific and Europe

Asia Pacific contributed 29.21% to the global market in 2025, with a valuation of USD 36.71 billion, and is projected to reach USD 38.55 billion in 2026. Other regions, such as the Asia Pacific and Europe, are anticipated to witness a notable growth in the coming years. During the forecast period, the market in the Asia Pacific region is projected to record a growth rate of 4.51%, which is the second highest amongst all the regions, and reach the valuation of USD 36.71 billion in 2025. Growth in this region is driven by rising middle-class affluence, especially in China, India, and Southeast Asia, coupled with strong e-commerce adoption and social media influence. Tourism and duty-free shopping significantly boost sales in key hubs such as Japan, Hong Kong, and Singapore. Brands focus on personalization, sustainability, and digital innovation to cater to evolving consumer preferences across this diverse and dynamic market. The Japan market is valued at USD 7.41 billion by 2026, the China market is valued at USD 21.41 billion by 2026, and the India market is valued at USD 3.93 billion by 2026.

Europe

The Europe market generated USD 33.45 billion in 2025, representing 26.61% of the global market landscape, and is expected to reach USD 34.82 billion in 2026. Europe remains a cornerstone of the global market, renowned for its iconic fashion houses and artisanal craftsmanship. The region is characterized by sophisticated consumers who value heritage, exclusivity, and superior quality. Digital adoption continues to grow, with luxury brands enhancing omnichannel experiences to engage discerning clientele. Additionally, the shift toward sustainable luxury and transparency in sourcing is shaping purchasing decisions, aligning with European consumers' ethical values and regulatory frameworks. The UK market is valued at USD 6.59 billion by 2026, while the Germany market is valued at USD 6.24 billion by 2026.

South America and Middle East & Africa

Over the forecast period, the market in South America and the Middle East & Africa would witness a moderate growth rate during 2026-2034. The market in South America in 2025 is set to record USD 6.01 billion in its valuation. The Middle East & Africa market was valued at USD 5.19 billion in 2025, capturing 4.13% of global revenue, and is estimated to reach USD 5.34 billion in 2026. The South America region captured 4.78% of the global market in 2025, generating USD 6.01 billion in revenue, and is projected to reach USD 6.14 billion in 2026.

South America

In South America, the market is expanding, with Brazil, Argentina, and Colombia driving growth as rising urbanization, greater fashion accessibility, and growing body-positivity movements boost demand for inclusive apparel. The South America luxury goods market is growing steadily, driven by rising middle-class incomes and urbanization, with Brazil leading in market share. E-commerce is rapidly expanding, catering to younger, digitally savvy consumers, while luxury brands invest in flagship stores and omnichannel strategies to capture diverse consumer demand across the region.

The Middle East & Africa (MEA) market is growing steadily, driven by affluent consumers in GCC countries such as Saudi Arabia and the UAE who value luxury as a status symbol. Rising tourism, expanding e-commerce, and strong brand presence in key cities support growth. International brands such as Gucci and Rolex are expanding retail footprints, while regional players contribute to market diversity. Sustainability and digital innovation are becoming important trends shaping consumer preferences in this vibrant region. In the Middle East & Africa, South Africa is set to attain the market value of USD 1.25 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players:

Portfolio Diversification and Global Distribution Help Key Players Maintain Leading Market Position

Key players operating in the market are Tapestry, Inc., Ralph Lauren Corporation, Capri Holdings Limited, Estee Lauder Companies, Inc., and Tory Burch LLC. These players maintain leadership through diverse brand portfolios, extensive global distribution, and strong heritage branding. The market is evolving with an increased focus on sustainability, personalized luxury experiences, and digital engagement to attract younger, affluent consumers. Despite macroeconomic headwinds, these companies continue to innovate and adapt to shifting consumer preferences to sustain growth. For instance, in July 2025, Tapestry, Inc., a parent company of luxury fashion brands Coach and Kate Spade, increased its equity stake in recycled leather maker Gen Phoenix to 9.9% via a USD 15 million financing round. The partnership includes a three-year supply agreement for Gen Phoenix’s recycled leather materials, enabling Tapestry brands (Coach and Kate Spade) to utilize leather waste materials in production at scale.

LIST OF KEY AFFORDABLE LUXURY FASHION COMPANIES PROFILED:

- Tapestry, Inc. (U.S.)

- Ralph Lauren Corporation (U.S.)

- Capri Holdings Limited (U.S.)

- Tory Burch LLC (U.S.)

- Coty, Inc. (U.S.)

- Guess, Inc. (U.S.)

- Longchamp (France)

- PVH Corp. (U.S.)

- SMCP Group (France)

- Furla S.p.A. (Italy)

KEY INDUSTRY DEVELOPMENTS:

- September 2025: NEXT partnered with Myntra to open its first Exclusive Brand Outlet (EBO) in Pune, India, ahead of the festive season 2025, expanding retail presence in the large emerging markets.

- September 2025: Gucci unveiled a sneak preview of its new artistic director, Demna’s debut collection, “La Famiglia,” ahead of Milan Fashion Week. The collection includes dramatic styles and handbags.

- February 2025: Coach launched its Spring 2025 campaign titled “On Your Own Time,” with global ambassadors Elle Fanning, Nazha, Kōki, and Youngji Lee. It promotes Coach’s Spring collection (bags, sneakers, and outerwear), aligned with the brand platform “The Courage to Be Real” and expressing urgency for authenticity over chasing pace.

- February 2025: Fashion house Jacquemus inked a beauty partnership with L’Oréal Groupe to launch a beauty line, exploring terrain beyond pure fashion into beauty/ fragrance under its branding.

- March 2025: Steve Madden (a U.S.-based footwear/accessories brand) acquired British brand Kurt Geiger from Cinven for USD 390.07 million. Kurt Geiger has been growing in the fashion/footwear premium segments.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The global affordable luxury fashion market analysis provides an in-depth study of market insights, size, and forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.67% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Price Positioning, Age Group, Gender, Distribution Channel, and Region |

| By Type |

|

| By Price Positioning |

|

| By Age Group |

|

| By Gender |

|

| By Distribution Channel |

|

| By Geography |

North America (By Type, Price Positioning, Age Group, Gender, Distribution Channel, and Country) o U.S. (By Type) o Canada (By Type) o Mexico (By Type) Europe (By Type, Price Positioning, Age Group, Gender, Distribution Channel, and Country) o Germany (By Type) o France (By Type) o Italy (By Type) o Spain (By Type) o U.K. (By Type) o Russia (By Type) o Rest of Europe (By Type) Asia Pacific (By Type, Price Positioning, Age Group, Gender, Distribution Channel, and Country) o China (By Type) o India (By Type) o Japan (By Type) o Australia (By Type) o Rest of Asia Pacific (By Type) South America (By Type, Price Positioning, Age Group, Gender, Distribution Channel, and Country) o Brazil (By Type) o Argentina (By Type) o Rest of South America (By Type) Middle East & Africa (By Type, Price Positioning, Age Group, Gender, Distribution Channel, and Country) o South Africa (By Type) o UAE (By Type) o Rest of the Middle East & Africa (By Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 131.17 billion in 2026 and is projected to reach USD 174.99 billion by 2034.

In 2025, the market value stood at USD 125.69 billion.

The market is expected to exhibit a CAGR of 3.67% during the forecast period (2026-2034).

The accessories segment is likely to lead the market by type.

The consistent AI-driven personalization technology innovations are a key factor driving market growth.

Tapestry, Inc., Ralph Lauren Corporation, Capri Holdings Limited, Estee Lauder Companies, Inc., and Tory Burch LLC. are some of the prominent players in the market.

North America dominated the market in 2026.

The growing expansion of omnichannel retailing to meet consumer needs is likely to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 236

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us