Specialty Papers Market Size, Share & Industry Analysis, By Material (Chemical Pulp, Mechanical & Semi-Chemical Pulp, Recycled Fiber, and Specialty Fibers), By Type (Packaging Specialty Papers, Release Liner Papers, Decor Papers, Thermal & Carbonless Papers, Industrial Specialty Papers, and Others), By End Use (Food & Beverages, Pharmaceuticals, Retail & Ecommerce, Building & Construction, and Others), and Regional Forecast, 2026-2034

Specialty Paper Market Size & Future Outlook

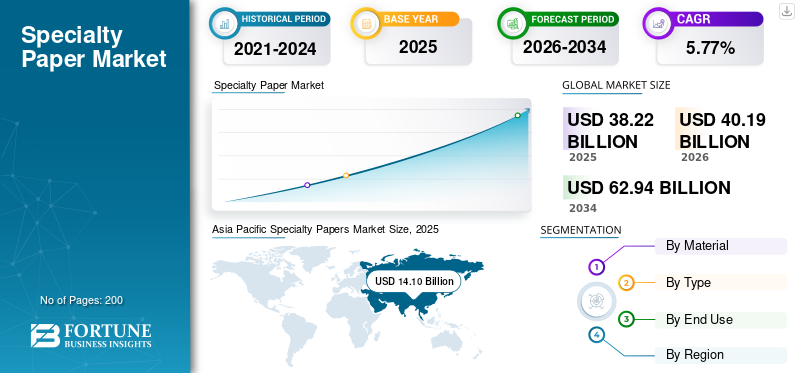

The global specialty papers market size was valued at USD 38.22 billion in 2025. The market is projected to grow from USD 40.19 billion in 2026 to USD 62.94 billion by 2034, exhibiting a CAGR of 5.77% during the forecast period. Asia Pacific dominated the specialty papers market with a market share of 36.89% in 2025.

The global specialty papers market encompasses the manufacturing and distribution of high-performance, value-added paper grades designed for particular functional uses, including packaging, labeling, insulation, filtration, décor, and security. The increasing demand for sustainable, recyclable packaging in the food, e-commerce, and consumer goods sectors is driving the adoption of specialty papers, as brands transition from plastics to environmentally friendly, high-performance paper-based alternatives that offer improved barrier and functional performance.

Furthermore, many key industry players, such as Stora Enso, UPM-Kymmene Corporation, and Mondi, operating in the market, are focusing on developing innovative products and conducting R&D.

Download Free sample to learn more about this report.

SPECIALTY PAPERS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 38.22 Billion

- 2026 Market Size: USD 40.19 Billion

- 2034 Forecast Market Size: USD 62.94 Billion

- CAGR: 5.77% from 2026–2034

- Asia Pacific dominated the specialty papers market with a 36.89% share in 2025.

- Chemical pulp was the leading material segment in 2025.

- Packaging specialty papers dominated the type segment in 2025.

North America

North America generated USD 6.47 billion in 2025, driven by sustainability initiatives and recyclable packaging adoption.

Europe

Europe reached USD 10.83 billion in 2025 and is projected to grow at a CAGR of 5.44% through 2034.

Asia Pacific

Asia Pacific led the market with USD 14.10 billion in 2025, supported by industrialization and packaging demand.

U.S.

The market was valued at USD 5.20 billion in 2025 and accounted for 13.60% of global sales.

Japan

The market reached USD 2.16 billion in 2025, representing 5.66% of global revenues.

Read More

SPECIALTY PAPERS MARKET TRENDS

Shift Toward Functional and Barrier-Enhanced Papers is a Prominent Trend Observed in the Market

A significant trend in the global market is the swift advancement of functional and barrier-enhanced paper solutions that serve as alternatives to plastic-based materials. Manufacturers are increasingly allocating resources toward coatings and treatments that offer resistance to moisture, grease, oxygen, and light, all while ensuring recyclability and composability. Moreover, progress in bio-based coatings and water-based barrier technologies is becoming more prominent, thereby decreasing dependence on fluorochemicals and polyethylene layers. The drive toward circular economy models are further stimulating innovation, resulting in the development of multi-functional specialty papers that integrate strength, printability, and environmental impact. The demand for specialty papers that are functional and barrier-enhanced thus emerges as a key trend.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Demand for Sustainable Packaging Solutions is Driving Market Growth

The primary driver for the specialty papers market growth is the global movement toward sustainable and environmentally friendly packaging options. Governments, brands, and consumers are progressively emphasizing materials that minimize environmental harm, resulting in a decrease in single-use plastics and an increase in paper-based alternatives. Sectors such as food & beverage, e-commerce, and personal care are swiftly embracing these materials to comply with regulatory requirements and meet consumer demands. This shift is additionally bolstered by corporate sustainability pledges and advancements in paper production process technologies that improve product efficacy.

MARKET RESTRAINTS

High Production Costs and Raw Material Volatility Hampers Market Expansion

A significant constraint in the market is the comparatively high production cost relative to traditional paper grades and certain plastic substitutes. Furthermore, variations in the prices of pulp, chemicals, and energy have a considerable effect on cost effectiveness & structures, leading to uncertainty for manufacturers. Disruptions in the supply chain and the restricted availability of premium-grade raw materials further intensify the problem. These financial challenges can hinder adoption, especially in price-sensitive markets, where end-users might be reluctant to transition from less expensive alternatives, even in light of the environmental and functional advantages provided by specialty papers.

MARKET OPPORTUNITIES

Expansion in Emerging Applications and End-Use Industries Offers Potential Growth Opportunities

A considerable opportunity exists in the growth of specialty papers within new applications and industries. In addition to their conventional uses, specialty papers are being progressively utilized in fields such as electronics, healthcare, construction, and automotive, owing to their customizable characteristics. For example, there is a consistent increase in the demand for electrical insulation papers, medical-grade papers, and décor papers used in laminates. Moreover, the incorporation of intelligent features such as anti-counterfeiting technologies and compatibility with digital printing creates fresh possibilities for innovation. These expanding applications offer manufacturers the chance to broaden their product ranges and explore high-growth market segments.

MARKET CHALLENGES

Performance Limitations Compared to Plastics Pose a Critical Challenge to Market Development

A significant challenge facing the market is closing the performance gap with conventional plastic materials. Although specialty papers provide sustainability benefits, they frequently fall short of plastics regarding durability, flexibility, and long-term barrier performance in extreme conditions. This limitation is especially crucial in applications that demand prolonged shelf life, high moisture resistance, or exposure to severe environments. While technological innovations are tackling some of these challenges, attaining similar performance without sacrificing recyclability continues to be a complex issue.

Segmentation Analysis

By Material

High Purity, Strength, and Process Versatility Drive the Dominance of the Chemical Pulp Segment

Based on the material, the market is divided into chemical pulp, mechanical & semi-chemical pulp, recycled fiber, and specialty fibers.

Chemical pulp is the leading material in the global market, attributed to its exceptional purity, strength, and versatility in high-performance applications. The enhanced quality of the fiber facilitates superior coating adhesion and uniform surface characteristics, rendering it suitable for value-added applications. Furthermore, chemical pulp allows for customization regarding fiber treatment and functional improvements, enabling manufacturers to fulfill particular end-use specifications. With the increasing demand for premium, high-specification papers, the dependability and performance benefits of chemical pulp persist in promoting its extensive use.

The mechanical & semi-chemical pulp segment is expected to grow at a CAGR of 5.89% over the forecast period.

By Type

Sustainability Demand, Functional Performance, and End-Use Expansion Drive the Dominance of the Packaging Specialty Papers Segment

Based on type, the market is segmented into packaging specialty papers, release liner papers, decor papers, thermal & carbonless papers, industrial specialty papers, and others.

In 2025, the packaging specialty papers segment dominated the global market, which plays a vital role in substituting plastic-based packaging while providing necessary performance characteristics. The rise in environmental regulations and the growing consumer inclination toward sustainable materials have expedited the transition to paper based packaging in the food, e-commerce, and retail industries. Moreover, the rapid increase in the consumption of packaged goods and the expansion of online retail have led to a significant rise in the demand for protective and flexible packaging solutions. Their capability to harmonize sustainability with performance, coupled with ongoing innovations in coatings and treatments, secures their prominent position in the market.

The release liner papers segment is projected to grow at a CAGR of 5.85% over the forecast period.

By End Use

To know how our report can help streamline your business, Speak to Analyst

High Consumption Volume and Sustainability Shift Drive the Dominance of the Food & Beverages Segment

Based on the end use, the market is segmented into food & beverages, pharmaceuticals, retail & ecommerce, building & construction, and others.

The food and beverages sector leads the global specialty papers market share, driven by substantial, steady demand for packaging materials for both staple and processed goods. The swift expansion of packaged and convenience foods, coupled with the growth of quick-service restaurants and e-commerce grocery platforms, further enhances this demand. Moreover, rising regulatory pressures to reduce plastic consumption have hastened the shift toward paper-based alternatives in food packaging. Specialty papers offer a combination of safety, performance, and sustainability, making them the favored option in this highly regulated, volume-oriented industry.

The pharmaceuticals segment is projected to grow at a CAGR of 4.95% over the forecast period.

Specialty Papers Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

Asia Pacific Specialty Papers Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the third-leading share in 2024, valued at USD 6.15 billion, and maintained its leading position in 2025, with a value of USD 6.47 billion. In North America, the market for specialty papers is propelled by strict environmental regulations and robust corporate sustainability initiatives. Companies are swiftly substituting plastics with recyclable paper alternatives, as the demand for premium, high-performance packaging in the food, healthcare, and e-commerce industries persists in driving innovation and adoption.

U.S Specialty Papers Market

Based on North America's strong contribution and the U.S. dominance within the region, the U.S. market was approximated at around USD 5.20 billion in 2025, accounting for roughly 13.60% of global sales. The U.S. market is driven by a significant uptake of innovative paper technologies and coatings that improve functionality and performance. The swift expansion of e-commerce and the consumption of packaged food are boosting the demand for durable, lightweight, and sustainable packaging solutions, bolstered by substantial investments in research and development as well as manufacturing capabilities.

Europe

Europe is projected to grow at 5.44% over the coming years, the second-highest among regions, and reached a valuation of USD 10.83 billion in 2025. The growth of the market in Europe is largely driven by stringent circular economy policies and ambitious objectives aimed at minimizing single-use plastics. Regulatory frameworks, along with heightened consumer awareness, are compelling manufacturers to shift toward biodegradable and recyclable specialty papers, particularly in food packaging, labeling, and industrial applications across the region.

U.K Specialty Papers Market

The U.K. market in 2025 was valued at USD 2.04 billion, representing approximately 5.33% of global revenues.

Germany Specialty Papers Market

Germany's market reached a value of USD 2.41 billion in 2025, equivalent to around 6.32% of global sales.

Asia Pacific

The Asia Pacific region reached a value of USD 14.10 billion in 2025 and secured the position of the dominating region in the market. The Asia Pacific region leads in growth driven by swift industrialization, urbanization, and an increase in the consumption of packaged goods. Nations such as China and India are experiencing a robust demand for economical and practical packaging materials, while a growing awareness of environmental issues is slowly changing preferences toward sustainable specialty paper options.

Japan Specialty Papers Market

The Japanese market in 2025 accounted for USD 2.16 billion, accounting for roughly 5.66% of global revenues. The market for specialty papers in Japan is propelled by the demand for high-quality, precision-engineered paper products utilized in the electronics, automotive, and premium packaging industry. A robust emphasis on innovation, cutting-edge manufacturing methods, and rigorous quality standards facilitates the creation of specialized, high-performance paper grades tailored for niche applications.

China Specialty Papers Market

China's market is projected to be one of the largest worldwide, with 2025 revenues at around USD 5.04 billion, representing roughly 13.18% of global sales.

India Specialty Papers Market

The Indian market in 2025 was valued at USD 3.59 billion, accounting for roughly 9.38% of global high-revenue markets.

Latin America

The Latin America region is expected to witness moderate growth in this market space during the forecast period. The Latin America market reached a valuation of USD 3.91 billion in 2025. In Latin America, the growth of the market is bolstered by the expanding food and beverage as well as consumer goods sectors. The rise in urbanization and the development of retail are driving the demand for packaging; however, cost sensitivity continues to be a significant consideration, prompting the adoption of economical specialty paper solutions that offer balanced performance attributes.

Middle East & Africa

In the Middle East & Africa, the South Africa region accounted for USD 0.76 billion in 2025. The Middle East and Africa region is experiencing growth attributed to the expansion of the retail, food processing, and logistics sectors. The increasing demand for packaged goods, coupled with enhancements in industrial infrastructure, is driving the necessity for specialty papers. Additionally, trends in sustainability are progressively impacting material selections in developed urban markets.

Saudi Arabia Specialty Papers Market

The Saudi Arabian market accounted for USD 1.04 billion in 2025, accounting for roughly 2.71% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Product Launch and Acquisitions by Key Players to Propel Market Progress

The global market has a semi-consolidated structure, with prominent players including Stora Enso, UPM-Kymmene Corporation, and Mondi. The significant market shares of these packaging companies are due to numerous strategic initiatives, including collaborations among operating entities to advance research.

- For instance, in February 2026, Stora Enso declared the expansion of its barrier-coated paper range for food packaging uses, unveiling advanced fiber-based materials intended to substitute multilayer plastics. This development aims to enhance grease and oxygen barriers while ensuring recyclability within current paper streams. Additionally, the company emphasized its investments in pilot-scale coating technologies throughout its European facilities, which will facilitate quicker commercialization.

Other notable players in the global market include ITC Limited, Oji Holdings Corporation, and Sappi Limited. These companies are expected to prioritize new product launches, strategic partnerships, and collaborations to increase their global market shares during the forecast period.

LIST OF KEY SPECIALTY PAPERS COMPANIES PROFILED

- Stora Enso (Finland)

- UPM-Kymmene Corporation (Finland)

- Mondi (U.K.)

- ITC Limited (India)

- Oji Holdings Corporation (Japan)

- Sappi Limited (South Africa)

- Nippon Paper Industries Co., Ltd. (Japan)

- Munksjö (Finland)

- Burgo Group S.p.A. (Italy)

- Ahlstrom (Finland)

- Fedrigoni S.p.A. (Italy)

- Felix Schoeller Group (Germany)

- Nordic Paper AS (Sweden)

- Twin Rivers Paper Company (U.S.)

- Domtar Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Mondi has introduced a new collection of high-performance specialty kraft papers as part of its sustainable packaging portfolio, aimed at e-commerce and food service applications. These products are designed with improved strength and printability, enabling brands to minimize material usage without compromising on durability. Additionally, Mondi has increased its production capacity in Central Europe to meet the rising regional demand.

- September 2025: Ahlstrom has launched a new range of sustainable filtration and food-grade specialty papers that feature bio-based coatings. These products are aimed at applications including coffee pods, tea bags, and industrial filtration, providing enhanced permeability and environmental performance. This introduction is a component of Ahlstrom's extensive innovation strategy to create high-value fiber solutions that minimize carbon emissions.

- June 2024: UPM-Kymmene Corporation has declared the launch of advanced barrier papers designed to substitute polyethylene-coated packaging materials. These papers offer resistance to moisture and oxygen, making them appropriate for packaging dry and frozen foods. The company utilized its knowledge in fiber processing and coating technologies to improve product functionality while maintaining recyclability.

- March 2024: Fedrigoni has finalized the acquisition of a business specializing in paper and self-adhesive materials to bolster its standing in the premium packaging and labeling sectors. This acquisition improves Fedrigoni's technological expertise and broadens its geographical reach, especially in Europe and North America. The company intends to incorporate advanced coating and converting technologies to create innovative, high-margin specialty papers.

- July 2023: Oji Holdings Corporation has declared the advancement of environmentally responsible and friendly packaging papers that feature improved water resistance and durability for food delivery purposes. The organization concentrated on minimizing plastic coatings while ensuring the preservation of product integrity throughout transportation. Additionally, Oji has broadened its production capabilities in Southeast Asia to cater to the increasing regional demand.

REPORT COVERAGE

The specialty papers market analysis includes a comprehensive study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments, as well as their prevalence by key regions. The global market research report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.77% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Material, Type, End Use, and Region |

| By Material |

|

| By Type |

|

| By End Use |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 38.22 billion in 2025 and is projected to reach USD 62.94 billion by 2034.

In 2025, the market value of Asia Pacific stood at USD 14.10 billion.

The market is expected to grow at a CAGR of 5.77% over the forecast period.

By material, the chemical pulp segment is expected to lead the market.

The growing demand for sustainable packaging solutions is driving market growth.

Stora Enso, UPM-Kymmene Corporation, and Mondi are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us