AI Data Center Market Size, Share & Industry Analysis, By Component (Hardware, Software, and Services), By Data Center Type (Hyperscale Data Center, Colocation Data Center, Edge Data Center, and Others), By Industry (Healthcare, Retail, IT and Telecom, BFSI, Automotive, Media & Entertainment, Manufacturing, and Others), and Regional Forecast, 2026-2034

AI DATA CENTER MARKET SIZE AND FUTURE OUTLOOK

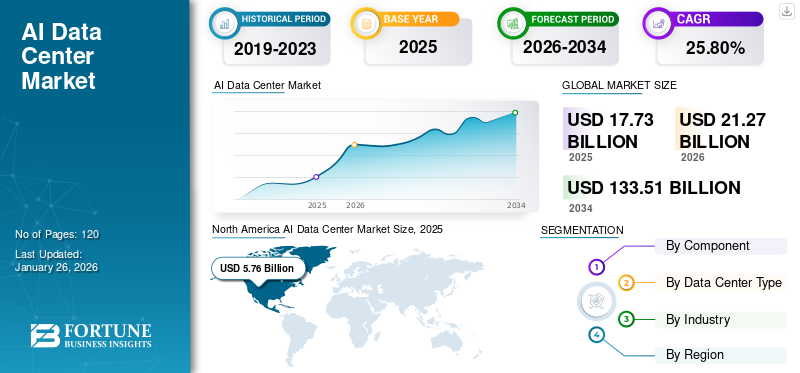

The global AI data center market size was valued at USD 17.73 billion in 2025 and is projected to grow from USD 21.27 billion in 2026 to USD 133.51 billion by 2034, exhibiting a CAGR of 25.80% during the forecast period. North America dominated the market with a share of 32.50% in 2025.

AI (Artificial Intelligence) data center is a facility designed to cope with the enormous power, storage, and cooling requirements of AI technology.

Several key players including Amazon, Equinix, Microsoft, HPE and others are making major investments with the aim of expanding their data center presence across emerging markets. The key players adopt this strategy to tap into the untapped potential for rising demand for digital infrastructure and AI-driven technologies.

During the forecast period, the market is expected to showcase a significant focus on the optimization of data center infrastructure with AI for enhanced performance, energy efficiencies, and scalability. In addition, as AI-based environmental concerns grow, data centers are increasingly integrating AI technology to optimize energy consumption and reduce their carbon footprint. The key market trends include AI-driven innovation, edge AI expansion, and the adoption of hybrid cloud environments.

The COVID-19 pandemic significantly boosted the adoption of AI technologies and digital transformation, thus influencing the market positively. This boost led to a higher need for data centers equipped with AI expertise to manage growing workloads. However, supply chain disruptions slowed the market growth. Despite these hurdles, the pandemic highlighted the importance of AI-based data centers in supporting critical infrastructure and driving long-term growth and innovation in the sector.

Download Free sample to learn more about this report.

AI Data Center Market KEY TAKEAWAYS

- 2025 Market Size: USD 17.73 billion

- 2026 Market Size: USD 21.27 billion

- 2034 Forecast Market Size: USD 133.51 billion

- CAGR: 25.80% from 2026–2034

- North America dominated the AI data center market with a 32.50% share in 2025.

- The hardware segment is projected to hold a 61.81% share in 2026.

- The colocation data center segment captured the largest market share in 2026.

North America

North America accounted for 32.50% of the global market in 2025, reaching USD 5.76 billion and projected to grow to USD 6.69 billion in 2026.

Europe

Europe generated USD 5.3 billion in 2025, contributing 29.90% of global revenue, and is expected to reach USD 6.3 billion in 2026.

Asia Pacific

Asia Pacific represented 26.80% of the global market in 2025, valued at USD 4.75 billion and forecast to reach USD 5.96 billion in 2026.

U.S.

U.S. The AI data center market is expected to reach USD 5.24 billion in 2026.

Japan

Japan The market stood at USD 1.1 billion in 2026, driven by increasing adoption of AI technologies and expansion of advanced data center facilities.

Read More

INVESTMENT ANALYSIS AND OPPORTUNITIES

The market has been witnessing a surge in investments related to the data center powered by the AI ecosystem. This rise is driven by the increasing adoption of artificial intelligence across several industries. Significant future opportunities lie in sectors such as confidential computing, generative AI, and others, with sustainability and energy efficiency becoming integral parts of investment strategies. In addition, several investments highlight the market players aiming to expand their data center expansion. For instance,

- September 2024: The U.S. private equity firm Blackstone announced a USD 13.3 billion investment to establish one of Europe's largest AI data centers in Northumberland, U.K.

- August 2024: The U.K. Government, with the support of the Coal Authority, started building the largest AI data center in Cambois, North East England.

- October 2024: Microsoft unveiled a USD 4.46 billion initiative to expand its hyper-scale cloud and AI data center infrastructure in Italy over the next two years. This plan includes providing digital skills training to over one million Italians by the end of 2025.

- July 2024: CyrusOne raised around USD 7.9 billion in funding with the aim of developing more data centers to meet the demand from the AI boom. This investment will be used to fund future and existing development projects in the U.S.

- July 2023: QTS Realty Trust, LLC and Blackstone, in tandem, spent over USD 8 billion to develop new data centers to prepare for the AI boom.

AI DATA CENTER MARKET TRENDS

Hybrid and Multi-Cloud Deployments Emerge as a Prominent Market Trend

Several businesses are using hybrid and multi-cloud strategies, combining on-premise data centers with public cloud services. As AI models evolve, the need for varying computing, storage, and networking requirements grows. Hybrid and multi-cloud setups offer dynamic environments to meet these demands. In addition, AI generates and processes large volumes of data. Hybrid and multi-cloud solutions allow businesses to manage this data efficiently across different environments.

- As per industry experts, a survey reported that a significant percentage of firms (76%) have been using two or more public clouds, with the average of them having 2.3 clouds in use. It was observed that large enterprises showcased even higher percentages of multi-cloud use. The revenue figures were more than USD 1 billion in revenue, which is twice as likely to be using three or more clouds as compared to smaller companies.

- As per a global survey by industry experts, over 86% of businesses have adopted a multi-cloud strategy owing to shifting business priorities. (Survey participants: 727 cloud technology decision-makers at businesses with more than 1,000 employees)

Thus, with businesses shifting toward hybrid and multi-cloud strategies, there is a growing need for hybrid and multi-cloud solutions in AI-based data centers due to their flexibility, scalability, and cost-effectiveness in handling vast amounts of data for AI workloads.

MARKET DYNAMICS

Market Drivers

Rising Demand for AI-powered Applications and Growth in Cloud Computing to Drive the Market

In recent years, there has been a surge in the use of cutting-edge AI technologies such as deep learning, advanced machine learning, and automated language processing across several sectors. These technologies are applied in various industries, including financial analysis, medical research, and smart production, among others. These applications often require immediate data processing and sophisticated computations, which demands high-performance data centers designed for such workloads. This growing need for AI-specific data centers equipped with advanced hardware and software helps businesses manage large datasets and execute complex algorithms.

- As per a recent article published by Acropolium in January 2024, over 42% of businesses that were surveyed reported AI integration into their operations. In addition, out of the early adopters, 59% of businesses have plans to speed up and expand their investments in AI technology.

Moreover, as companies shift toward cloud-based solutions, the demand for high-performance data center operations capable of processing large amounts of information continues to grow.

- As per Edge Delta Insights (2024), around 90% of businesses around the world already use cloud services—such as Google, Microsoft, and AWS. The insights also indicated that the number of cloud computing users is expected to grow exponentially over the coming years.

Thus, the rising demand for AI-powered applications and growth in cloud computing are driving the market in recent years.

Market Restraints

High Implementation Costs and Maintenance Associated with AI Data Centers Hinder Market Growth

One of the significant challenges slowing the growth of the AI-based data center industry is the high costs involved in setting them up and running efficiently. These data centers require specialized hardware and consume much power to maintain their peak performance. Integrating AI systems into existing infrastructures is also a complex task, particularly for companies that may not have the technical expertise or financial resources to manage such upgrades.

Data security is another issue slowing the market’s growth. As AI systems handle sensitive information, concerns about privacy breaches and adherence to strict regulations such as GDPR make businesses hesitant to adopt these technologies. Additionally, running AI workloads requires experts with niche skills, and the shortage of qualified professionals is a limiting factor.

The high costs of implementation and maintenance associated with AI-based data centers, the need for robust data privacy and security measures, and the shortage of skilled professionals hamper the AI data center market growth.

Market Opportunities

Increasing Demand for Hyperscale Data Center Services Creates Lucrative Opportunities for Market Players

Hyperscale data centers are becoming increasingly prevalent due to their significant role in supporting AI-driven use cases. These types of data centers are in demand due to the increasing need for power generation. AI technologies need immense computing power, and hyperscale data centers, along with their massive infrastructure and advanced technology, are perfectly positioned to meet this need.

With the increasing demand for AI, the demand for these data centers grows. In addition, cost-effectiveness, scalability, and flexibility are a few advantages of hyperscale data centers. These features make such data centers a viable solution for companies looking to invest in AI while keeping their costs in check.

The above chart highlights data center demand ownerships in Europe by hyperscalers and colocation providers. At present, data center growth in Europe is fueled by hyperscalers, driving up to 70% of the anticipated demand by 2028. The ownership model of data centers plays a crucial role in shaping the market. Hyperscalers drive large-scale, cutting-edge AI infrastructure deployment, while colocation providers offer flexibility and scalability for businesses of all sizes. Enterprise-owned data centers tend to offer more control but may lag in terms of scalability and innovation compared to the other models.

Thus, the increasing demand for hyper-scale data center services creates lucrative opportunities for market players, further accelerating market growth over the coming years.

SEGMENTATION ANALYSIS

By Component

Hardware Component Dominated the Market Owing to Its Growing Usage to Speed up Complex Tasks and Model Training

By component, the market is divided into hardware (servers, storage, networking equipment, and others), software (AI/ML frameworks, data management solutions, and others), and services (managed services, professional services, and others).

The hardware segment is projected to dominate the market with a share of 61.81% in 2026 and is expected to showcase the highest CAGR during the forecast period. Hardware forms the basis for creating dependable, high-performance infrastructure to accommodate modern computing requirements, which encompass a wide range from conventional enterprise applications to cutting-edge technologies such as big data analytics. Besides, there is a growing trend of specialized hardware used to speed up complex tasks and model training. The demand for hardware is also increasing due to the need to manage a huge amount of data, as well as its processing and storage.

The software segment is anticipated to foresee substantial growth over the forecast period. Software, ranging from operating systems to application-level solutions, plays a crucial role in the management of data flows, the analysis of performance metrics, and the assurance of security and compliance.

By Data Center Type

Rising Demand Higher Scalability Options Boosted Colocation Data Center Segment Growth

By data center type, the market is classified into hyperscale data centers, colocation data centers, edge data centers, and others (enterprise, hybrid).

The colocation data center segment captured the largest AI data center market share in 2026. Colocation facilities provide adaptable scalability choices, enabling users to adjust their IT infrastructure rapidly and effortlessly in response to evolving business requirements. Furthermore, the benefits of scaling empower colocation providers to furnish cost-efficient security and connectivity solutions and reduces the operational costs for leaseholders. Besides, colocation facilities are able to handle large volumes of data, enable predictive maintenance, and provide integration with other solutions.

The hyperscale data center segment is expected to lead the market, contributing 36.60% globally in 2026 and expected to grow at the highest CAGR during the forecast period, as it is designed to scale rapidly and efficiently to support massive amounts of data and workloads.

The edge data center segment is expected to grow at the highest CAGR of 28.16% during the forecast period.

By Industry

Popularity of Mobile Payments Bolstered BFSI Segment Growth

Based on industry, the market is divided into healthcare, retail, IT and telecom, BFSI, automotive, media & entertainment, manufacturing, and others.

The BFSI segment will account for 24.60% market share in 2026. Data center plays crucial role in facilitating fast transactions. The increasing popularity of mobile payment systems and online banking is driving the need for data centers with AI capabilities as huge amount of data is created and to handle and store this data demand for data center is expected to increase. In 2025, the BFSI market holds 24% of the market share.

The healthcare segment is estimated to showcase the highest CAGR of 32.93% during the forecast period as it deals with sensitive financial and personal data, making security and compliance paramount. Data centers provide secure environments equipped with robust physical and cybersecurity measures to protect against data breaches.

IT & telecom is estimated to grow significantly in coming years. IT & telecom companies are undergoing digital transformation by adopting initiatives to modernize their infrastructure, applications, and services. Data centers play an important role in supporting these initiatives by providing the computing power, storage capacity, and networking capabilities needed to deploy new technologies and deliver innovative digital services. The deployment of advanced software and applications in the IT sector is increasing. Additionally, the surge in internet users, 5G, and IoT is also creating a massive demand for data storage due to substantial data volume. These factors are driving AI-based data center demand in the IT & telecom sector.

To know how our report can help streamline your business, Speak to Analyst

AI DATA CENTER MARKET REGIONAL OUTLOOK

Geographically, the market is studied across North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

North America

North America AI Data Center Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America maintained a strong presence in the global market, reaching USD 5.76 billion in 2025, accounting for 32.50% share, and is expected to reach USD 6.69 billion in 2026. This is attributed to the early acceptance of data centers, driven by the growing need for big data, data processing, storage, and analysis. The rising demand for advanced AI and cloud computing-based platforms and the rapid adoption of AI technology across North American countries are driving the regional market. According to Accenture report, companies in North America have devoted 31% of their total technology budgets in AI.

Download Free sample to learn more about this report.

The U.S. market accounts for USD 5.24 billion in 2026 and is currently a prime location for investments in data centers. According to a report by industry experts, the demand for data centers in the U.S. is expected to increase by 10% annually until 2030. The country represents approximately 40% of the global demand, with Germany, Britain, and China following closely behind. Currently, Northern Virginia has the largest data center market globally, with over 275 facilities. Furthermore, substantial construction is underway in Dallas/Ft. Worth, Chicago, and Silicon Valley are anticipated to drive market growth in the U.S.

Asia Pacific

The Asia Pacific market accounted for USD 4.75 billion in 2025, representing 26.80% of the global industry, and is expected to reach USD 5.96 billion in 2026. The convergence of cloud computing and artificial intelligence is reshaping industries, and the region stands at the forefront of this transformation. As businesses strive to stay competitive and meet the demands of an increasingly connected world, the demand for robust data center infrastructure has surged.

- In 2023, according to the London Stock Exchange, the region’s data center deals hit a record of USD 3.45 billion. Asia Pacific is experiencing an unprecedented need for data center infrastructure due to the rapid increase in digital data, driven by the widespread use of connected devices, IoT sensors, and new technologies.

- According to a 2024 report by industry experts, the demand for AI and data center storage capacity is projected to increase from 10.1 zettabytes (ZB) in 2023 to 21.0 ZB in 2027, representing a five-year CAGR of 18.5%.

China’s market is estimated to hit USD 1.53 billion, while the market in India accounts for USD 0.66 billion, and the Japan market stood at USD 1.1 billion in 2026.

South America

South America is anticipated to hit USD 1.09 billion in 2025 and expected to showcase a notable CAGR over the forecast period. Rising investments in digital transformation across South American countries such as Brazil and Argentina majorly drive this growth. In addition, the countries tend to have lower environmental regulations than the U.S. and Europe. Therefore, high-tech companies looking for chip factory and data center locations are targeting South America. AI-based data centers are gaining popularity in the region as the volume of data processed in the region has doubled since 2020. As per CBRE, processing volume is expected to grow more than 9% between 2024 and 2029.

Europe

In 2025, Europe generated USD 5.3 billion, contributing 29.90% to global market revenue, and is projected to grow to USD 6.3 billion in 2026. This regional growth is attributed to the rise in machine learning and AI investments, along with the extensive utilization of high-performance computing in sectors such as healthcare and automotive. In addition, data center expansions in major European cities such as London, Dublin, Frankfurt, Amsterdam, and Paris has increased by 15%-20% compared to 2023. Despite power sourcing availability challenges, significant development and major project deliveries are anticipated in 2025. The U.K. market is estimated to hit USD 1.21 billion in 2026, while the market in France accounts for USD 0.65 billion in 2025, and the Germany market stood at USD 1.43 billion in 2026.

Middle East & Africa

In 2025, Middle East & Africa represented USD 0.83 billion, accounting for 4.70% of the worldwide market, and is projected to grow to USD 1.01 billion in 2026. In addition, the UAE is a top location for data centers in the region due to its strong and competitive digital economy. Furthermore, in Africa, the data center sector is attracting the attention of hyperscalers and investors, catalyzed by significant market opportunities in countries including Kenya, Egypt, Nigeria, South Africa, and Morocco. Thus, increasing investment in data centers is estimated to boost the market growth in the region. The GCC country is showing remarkable market size of value USD 0.20 billion in 2025.

Latin America

Latin America contributed 6.20% to the global market in 2025, with a valuation of USD 1.09 billion, and is projected to reach USD 1.31 billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Strategic Alliances and Investments Pave the Way for Growing Business Trajectories

The market comprises several key players that offer specialized hardware, software, and integrated solutions precisely developed to handle the demanding AI workloads. These players enter into relevant acquisitions and collaborations, which pave the way for their growing business trajectories. In addition, the market players are making major investments to expand their data center presence across emerging markets. Furthermore, the players are also investing in developing their product expertise, especially the AI hardware expertise. This strategy helps market players cater to the end user’s evolving requirements.

Major Players in the AI Data Center Market

To know how our report can help streamline your business, Speak to Analyst

The top 5 players captured around 53% - 56% market share owing to their cloud infrastructure dominance, rich data center networks, colocation services expertise, and AI hardware specialization. In addition, these players invest heavily in R&D activities for AI technologies. This strategy helps them stay ahead of their competitors. The global market comprises the top 5 large-scale players, accounting for around 54% of the market share.

List of Key AI Data Center Companies Profiled:

- Amazon.com, Inc. (U.S.)

- Microsoft Corporation (U.S.)

- Alphabet Inc. (U.S.)

- Equinix, Inc. (U.S.)

- Digital Realty Trust, Inc. (U.S.)

- Intel Corporation (U.S.)

- NVIDIA Corporation (U.S.)

- Stack Infrastructure (U.S.)

- CyrusOne (U.S.)

- QTS Realty Trust, LLC (S.)

- OVHcloud (France)

- Alibaba Cloud (China)

- NTT Communications (Japan)

- G42 (UAE)

- Etisalat Group (UAE)

- STC Solutions (Saudi Arabia)

- Atos (France)

- Cerebras (U.S.)

- Ampere Computing LLC (U.S.)

- Graphcore (U.K.)

….and more

KEY INDUSTRY DEVELOPMENTS:

- January 2025: CoreWeave announced the operationality of two of its initial data centers in London Docklands and Crawley. These sites would host some of NVIDIA AI platform utilizations empowered by NVIDIA H200 GPUs mounted with NVIDIA Quantum-2 InfiniBand networking, pursuing the enhancement of high-performance computing capability in the U.K.

- June 2024: HPE completed its strategic partnership with Nvidia with the aim of offering turnkey AI private cloud solutions that would help businesses deploy gen AI use cases at speed.

- April 2024: Google invested over USD 640.62 million in a data center in the Dutch city of Groningen. With this investment, the company expects to create over 125 new job opportunities for the public. The company even reported prioritizing sustainability and a positive impact on the local community while building the new data center.

- March 2024: Schneider Electric completed its strategic collaboration with NVIDIA with the aim of enhancing data center infrastructure. The company, Schneider, is expected to use its data center infrastructure capabilities and NVIDIA's enhanced AI technologies to launch data center reference designs. The designs are expected to transform the benchmarks for AI deployment and operation within the data center landscape.

- January 2024: Stack Infrastructure reported expanding its data center expertise with high-density racks with the aim of supporting the increasing demand for ML workloads. The company would support high-density workloads through a closed-loop water cooling system.

- August 2023: CyrusOne introduced Intelliscale, an AI workload-specific data center solution particularly designed to meet the increased demand for AI applications and services.

REPORT COVERAGE

The report offers a detailed overview of the market and focuses on crucial aspects such as key players, their product types, and their use cases in the market. In addition, the report provides insights into the market trends and highlights recent market-related developments. Besides, the report also includes several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 25.80% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component

By Data Center Type

By Industry

By Region

|

|

Companies Profiled in the Report |

Amazon.com, Inc. (U.S.), Microsoft Corporation (U.S.), Alphabet Inc. (U.S.), Equinix, Inc. (U.S.), Digital Realty Trust Inc. (U.S.), Intel Corporation (U.S.), NVIDIA Corporation (U.S.), Stack Infrastructure (U.S.), CyrusOne (U.S.), and QTS Realty Trust, LLC (U.S.) |

Frequently Asked Questions

According to Fortune Business Insights, the Market is projected to reach USD 133.51 billion by 2034.

In 2025, the global market was valued at USD 17.73 billion.

The market is projected to grow at a CAGR of 25.80% during the forecast period.

By component, the hardware segment led the market in 2026.

The rising demand for AI-powered applications and growth in cloud computing are the key factors driving the market expansion.

Amazon.com, Inc., Microsoft Corporation, Alphabet Inc., Equinix, Inc., Digital Realty Trust, Inc., Intel Corporation, NVIDIA Corporation, Stack Infrastructure, CyrusOne, and QTS Realty Trust, LLC are the top players in the market.

North America dominated the market with a share of 32.50% in 2025.

By industry, the healthcare segment is expected to grow at the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us