AI-enabled Medical Devices Market Size, Share & Industry Analysis, By Component (Software, Hardware & Devices, and Services), By Technology (Machine Learning & Deep Learning, Natural Language Processing, Computer Vision, and Others), By Specialty (Radiology, Cardiology, Ophthalmology, Neurology, Orthopaedics, Gastroenterology, Pathology, and Others) By Application (Screening and Early Detection, Diagnosis and Interpretation, Monitoring and Alerting, Therapy Planning/Treatment Support, & Others), By End User (Hospitals & ASCs, Specialty Clinics, & Others), and Regional Forecast, 2026-2034

AI-enabled Medical Devices Market Size and Future Outlook

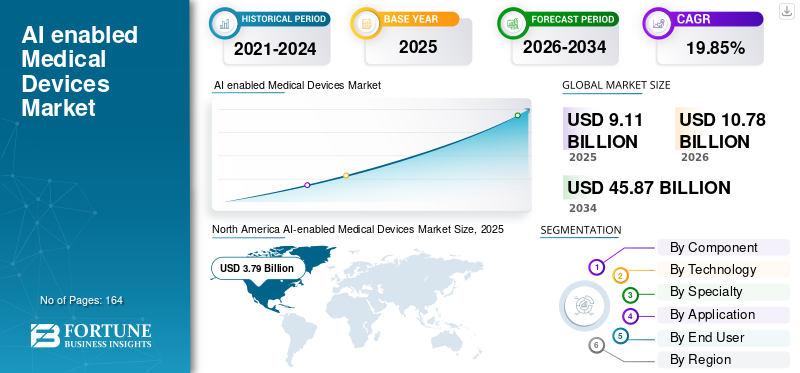

The global AI-enabled medical devices market size was valued at USD 9.11 billion in 2025. The market is projected to grow from USD 10.78 billion in 2026 to USD 45.87 billion by 2034, exhibiting a CAGR of 19.85% during the forecast period. North America dominated the AI enabled medical devices market with a market share of 41.6% in 2025.

Artificial intelligence in AI-enabled medical devices involves embedding various technologies into regulated medical products to support screening, image analysis, diagnosis, monitoring, workflow prioritization, and treatment support. The market expansion is being driven by the rising number of AI-enabled devices authorized for clinical use, the strong concentration of innovation in imaging-led specialties, and the growing use of predictive AI in hospitals to improve care quality, speed, and productivity.

Key participants in the global market include Medtronic, Siemens Healthineers AG, and Koninklijke Philips N.V., among others. These companies are competing across AI-enhanced ultrasound and imaging, radiology workflow automation, robotic-assisted intervention, GI endoscopy, connected health monitoring, portable imaging, and autonomous diagnostics.

Download Free sample to learn more about this report.

AI-ENABLED MEDICAL DEVICES MARKET TRENDS

Expansion of Wearable Devices & Remote Monitoring is a Significant Trend Observed in Global Market

The growth of wearable technology and remote monitoring is emerging as a key market trend in AI-driven medical devices, as healthcare providers are progressively transferring care from hospitals to home settings and outpatient environments. Wearable devices and remote monitoring systems assist healthcare providers in continuously monitoring patient conditions, identifying declines sooner, and easing the strain on hospital resources. This trend is further reinforced by the increasing significance of monitoring and alerting applications in chronic illness management, post-acute care, and hospital-at-home approaches. Firms are currently integrating sensors, connectivity, and AI-driven analytics to produce more practical insights instead of merely gathering raw data. This enhances the market worth of connected devices in cardiology, diabetes management, and overall patient monitoring. The trend is particularly robust as providers seek tools that enable ongoing monitoring, quicker responses, and improved workforce efficiency. In general, this is driving the market from occasional device usage to more subscription- and service-oriented monitoring systems. These factors are supporting the overall global AI-enabled medical devices market growth.

- For instance, in June 2025, Medtronic partnered with Corsano Health to expand its acute care and monitoring portfolio in Europe through distribution of a multi-parameter wearable for continuous monitoring in both hospitals and hospital-at-home settings.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Need for Faster and More Accurate Diagnostic Solutions is Propelling Market Growth

The increasing demand for quicker and more precise diagnostic solutions significantly fuels the AI-powered medical devices market, as healthcare professionals face pressure to manage higher imaging volumes, workforce shortages, and greater case complexity without postponing clinical decisions. Devices powered by AI expedite the duration from scan or test to interpretation through automated image analysis, prioritization of urgent cases, and lessening the manual review load. They further enhance consistency by aiding clinicians with more uniform detection, assessment, and decision-making assistance. This is particularly crucial in radiology, cardiology, oncology, and emergency medicine, where quicker diagnoses can significantly enhance treatment timing and patient results. The driver is gaining strength as hospitals emphasize both workflow efficiency and diagnostic confidence concurrently. Healthcare systems are being encouraged to invest in devices that integrate speed, automation, and improved accuracy instead of depending solely on traditional equipment. In general, the need for quicker and more dependable diagnoses is hastening the use of AI-powered imaging, monitoring, and clinical assistance systems. All these factors cumulatively drive the overall market growth.

- For instance, in July 2025, GE Healthcare announced increasing R&D investment in AI-enabled medical devices designed to improve productivity, efficiency, and diagnostic confidence for healthcare professionals.

MARKET RESTRAINTS

Requirement of Rigorous Clinical Validation to Limit Market Growth

Requirement of rigorous clinical validation is a key restraint for the market as these products must prove safety, accuracy, reproducibility, and real-world clinical benefit before they can scale widely. Unlike conventional software, AI-enabled devices often need strong validation across different patient populations, care settings, and data environments to show that performance remains reliable. This makes development timelines longer and increases costs for clinical studies, regulatory submissions, post-market monitoring, and quality-system compliance. The challenge becomes even greater when algorithms are updated or deployed across new geographies, as additional evidence may be needed to support consistent use. It also slows procurement, as hospitals and providers increasingly ask for stronger clinical and workflow evidence before adoption. As a result, some products face delays in commercialization even when the underlying technology seems promising. Overall, rigorous validation requirements are necessary for patient safety, but they can restrain near-term market growth by raising the time and cost needed to bring AI-enabled devices to market.

MARKET OPPORTUNITIES

Rapid Expansion of Telemedicine to Offer Market Growth Opportunities

The swift growth of telemedicine is generating a significant market opportunity for AI-driven medical devices since virtual care is more effective when healthcare providers get ongoing, device-produced patient data away from the hospital. HHS indicates that remote patient monitoring is a type of telehealth that utilizes digital devices to gather and transmit patient health data for provider assessment, whereas CMS will uphold Medicare telehealth and remote-monitoring options in 2025. This is increasing the demand for AI-integrated wearables, connected monitoring technologies, intelligent sensors, and device-connected analytics that can facilitate virtual consultations with more prompt and applicable clinical insights. It also raises the need for devices that assist providers in identifying deterioration sooner, oversee chronic conditions from a distance, and minimize unnecessary in-person appointments. With the increasing integration of telemedicine in standard healthcare, AI-powered medical devices derive worth not just from hardware sales but also from ongoing software, alerting, and connected-care services. This creates a significant opportunity for vendors who can integrate device data, AI-powered analysis, and remote clinical processes into a single solution. All these factors would drive the market growth in the coming years.

- For instance, in July 2025, Samsung Electronics acquired Xealth to combine Xealth’s digital health integration platform with Samsung’s wearable technology. This was aimed to advance a connected care platform spanning more than 500 hospitals and 70+ digital health solutions.

MARKET CHALLENGES

Complex System Integration Pose a Prominent Challenge to Market Growth

Integrating complex systems poses a significant obstacle in the market for AI-powered medical devices, as these solutions need to function seamlessly with hospital IT infrastructures, imaging platforms, monitoring equipment, EHRs, and clinical workflows simultaneously. Even if the AI operates effectively, deployment may lag if data formats, device connections, and interoperability are not consistent among departments. This lengthens implementation time, boosts integration expenses, and may postpone the complete clinical benefits of the device. The issue is particularly significant in major hospitals, where radiology, monitoring, therapy planning, and reporting systems frequently originate from various vendors. This also complicates scaling within multi-site health systems, as each location might possess varying infrastructures and workflow configurations. Consequently, vendors must invest not just in the AI model, but also in interoperability, workflow development, and enterprise integration assistance. In summary, integrating complex systems continues to pose a market challenge since their adoption relies on the compatibility of AI-enabled devices with actual clinical settings, and not solely on the effectiveness of the algorithms. All the factors cumulatively affect the market growth.

Segmentation Analysis

By Component

Rising Launch of AI-Integrated Clinical Systems Led to Dominance of Hardware & Devices Segment

In terms of component, the market is divided into software, hardware & devices, and services.

The hardware & devices sector led the market share for AI-enabled medical devices in 2025. This is driven by key factors such as high commercial demand for AI-integrated imaging systems, monitoring tools, endoscopy platforms, and various capital equipment utilized directly in clinical environments. This superiority is further reinforced by the reality that hospitals and diagnostic facilities typically incur greater initial expenses on physical systems compared to software or support services in the early adoption phase. Furthermore, numerous AI functionalities in this market continue to be monetized via device-embedded platforms such as ultrasound, MRI, robotic systems, and patient monitoring devices, resulting in a substantial contribution from hardware revenue. With providers persistently investing in cutting-edge diagnostic and intervention-ready tools to enhance speed, precision, and workflow efficiency, the hardware and devices segment is expected to uphold a dominant role in the market.

- For instance, in August 2025, Philips launched Transcend Plus for its EPIQ CVx and Affiniti CVx cardiovascular ultrasound systems, featuring FDA-cleared AI enhancements and intelligent automation for faster and more confident cardiac assessment,

The services segment is anticipated to rise with a CAGR of 21.52% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Wider Use of Pattern-Recognition Algorithms Supported the Dominance of Machine Learning & Deep Learning Segment

Based on technology, the market is classified into natural language processing, computer vision, machine learning & deep learning, and others.

The machine learning & deep learning segment captured the leading position in the global market in 2025. Key factors including its broad use across imaging, patient monitoring, predictive alerting, and clinical decision-support functions are supporting the dominance of the segment. This technology is widely used as it can learn from large clinical datasets, identify patterns quickly, and improve device performance in tasks such as detection, classification, and risk prediction. In addition, medical device manufacturers continue to use AI/ML technologies to improve diagnostic speed, workflow efficiency, and clinical accuracy, which is supporting stronger adoption of this segment in routine care settings. As the volume of healthcare data continues to rise, the machine learning & deep learning segment is anticipated to maintain its leading position in the market. Furthermore, the segment is set to hold 41.4% share in 2026.

- For instance, in March 2025, Philips expanded its partnership with Ibex Medical Analytics and introduced a new release of Philips IntelliSite Pathology Solution to strengthen AI-enabled digital pathology workflows for cancer diagnosis.

The natural language processing segment is anticipated to rise with a CAGR of 21.77% over the forecast period.

By Specialty

Rising Use of AI in Medical Imaging Supported Radiology Segment Dominance

Based on specialty, the market is classified into radiology, cardiology, ophthalmology, neurology, orthopedics, gastroenterology, pathology, and others.

The radiology segment dominated the AI-enabled medical devices market share in 2025 due to factors including the high use of AI in X-ray, CT, MRI, mammography, and ultrasound workflows. This segment leads as radiology departments handle large imaging volumes every day and need faster image reading, better prioritization of urgent cases, and more consistent results. AI-enabled devices are being widely adopted in radiology to improve detection, support interpretation, reduce manual workload, and help radiologists manage growing case pressure. In addition, the U.S. FDA’s AI-enabled medical device landscape remains heavily concentrated in radiology-related products, which further supports the strong revenue contribution of this segment. As healthcare providers continue to invest in imaging speed, diagnostic confidence, and workflow efficiency, the radiology segment is expected to maintain its leading position in the market. Furthermore, the segment is set to hold 44.0% share in 2026.

- For instance, in March 2025, GE HealthCare announced a collaboration with NVIDIA Corporation to develop autonomous X-ray and ultrasound solutions designed to reduce pressure on radiology teams and support faster imaging workflows.

The pathology segment is anticipated to rise with a CAGR of 24.39% over the forecast period.

By Application

Growing Need for Faster and More Confident Clinical Reading Led to Dominance of Diagnosis and Interpretation Segment

On the basis of application, the market is divided into screening and early detection, diagnosis and interpretation, monitoring and alerting, therapy planning/treatment support, workflow automation and care coordination, and others.

In 2025, the market share was primarily led by the diagnosis and interpretation segment, influenced by the significant adoption of AI systems in radiology, cardiology, pathology, and other clinical workflows based on images or signals. This area is prioritized as healthcare professionals require tools that assist in quicker analysis of scans and test results, enhance diagnostic accuracy, and minimize inconsistencies in interpretation. AI-driven medical devices are being increasingly utilized in this field to assist with detection, measurement, case prioritization, and to enhance consistency in clinical decision-making. Moreover, a significant portion of marketable AI-driven medical devices continues to emphasize interpretation-intensive applications, maintaining the highest revenue contribution in this category. As providers prioritize speed, precision, and efficiency in diagnosis, the diagnosis and interpretation segment is expected to sustain its dominant position in the market. Furthermore, the segment is set to hold 32.6% share in 2026.

- For instance, in November 2025, Philips launched Verida, described as the world’s first detector-based spectral CT powered by AI to advance diagnostic precision.

The workflow automation and care coordination segment is anticipated to rise with a CAGR of 22.23% over the forecast period.

By End User

Higher Adoption of Advanced AI Systems in Acute Care Settings Led to Dominance of Hospitals & ASCs Segment

Based on end user, the market is segmented into hospitals & ASCs, specialty clinics, diagnostic imaging centers, homecare settings, and others.

The hospitals & ASCs segment dominated the market share in 2025 due to factors including the high volume of patients, strong demand for faster diagnosis, and greater use of advanced imaging, monitoring, and procedural systems in these settings. This segment leads as hospitals and ASCs have better access to capital budgets, specialist staff, and digital infrastructure needed to deploy AI-enabled medical devices at scale. They also handle more complex and urgent cases, which increases the need for AI-supported tools that improve speed, accuracy, and workflow efficiency. In addition, many leading artificial intelligence enabled medical devices are first introduced in hospital-based radiology, surgery, and patient-monitoring environments, which keeps revenue contribution highest in this segment. Furthermore, the segment is set to hold 50.8% share in 2026.

- For instance, in May 2025, Mass General Brigham and Koninklijke Philips N.V. collaborated to improve patient care with live AI-powered insights from medical device data. The partnership is aimed at helping clinicians in hospital settings use real-time device information more effectively.

In addition, homecare settings are projected to witness 25.34% growth rate during the forecast period.

AI-enabled Medical Devices Market Regional Outlook

By region, the market is divided into Asia Pacific, Europe, Latin America, North America, and the Middle East & Africa.

North America

North America AI-enabled Medical Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America devices market size attained USD 3.24 billion in 2024 and topped the worldwide market. In 2025, the area maintained its top spot, with USD 3.79 billion. North America led the worldwide market due to its advanced healthcare infrastructure, high adoption of digital health technologies, and the presence of significant medical device and technology firms.

U.S. AI-enabled Medical Devices Market

The U.S. market led the North American sector and is projected to be approximately USD 4.10 billion in 2026, representing about 38.0% of the global market.

Europe

Europe market size is anticipated to grow at 18.28% CAGR during the forecast period. Europe’s growth is mainly supported by its rapidly ageing population, rising chronic disease burden, and increasing effort to integrate AI into health systems.

U.K. AI-enabled Medical Devices Market

The U.K. market in 2026 is estimated at around USD 0.58 billion, representing roughly 5.4% of global revenues.

Germany AI-enabled Medical Devices Market

Germany devices market size is projected to reach approximately USD 0.65 billion in 2026, equivalent to around 6.1% of global sales.

Asia Pacific

The Asia Pacific market size is expected to reach a valuation of USD 2.55 billion by 2026. Asia Pacific is expected to grow rapidly due to a very large patient base with rapid healthcare infrastructure expansion, growing digitalization, and a sharp rise in elderly population. The region is also witnessing stronger demand for AI-enabled imaging, ophthalmology, cardiology, remote monitoring, and screening tools due to high chronic disease burden and uneven specialist access.

Japan AI-enabled Medical Devices Market

The Japan market in 2026 is estimated at around USD 0.68 billion, accounting for roughly 6.3% of global revenues.

China AI-enabled Medical Devices Market

China’s market is projected to reach revenues of around USD 0.52 billion in 2026, representing roughly 4.8% of global sales.

India AI-enabled Medical Devices Market

The India market in 2026 is estimated at around USD 0.27 billion, accounting for roughly 2.5% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to experience slower growth throughout the forecast period. The market growth in these regions is being supported by the expansion of telehealth, digital health programs, and improving access to specialist services in remote and underserved areas.

In the Middle East and Africa region, the GCC market is projected to reach approximately USD 0.22 billion by 2026, representing about 2.0% of worldwide revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Focusing on AI-Integrated Product Innovation to Strengthen Market Position

The global market is moderately fragmented, with major players such as GE HealthCare, Siemens Healthineers AG, Koninklijke Philips N.V., and Medtronic accounting for a notable share of market revenue. These companies are focusing on improving diagnostic speed, workflow efficiency, and clinical confidence to strengthen their market presence. The market is also witnessing rising emphasis on software-linked recurring value, strategic collaborations, and expansion across multiple care settings.

- For instance, in February 2026, Koninklijke Philips N.V. announced new AI-enabled systems, intelligent software, and imaging cloud services at ECR 2025 to streamline radiology workflows and improve clinical insights.

Other significant participants include Intuitive Surgical Operations, Inc., Aidoc, and iRhythm Technologies, among others. These companies are expected to prioritize new product innovation, collaborations & partnerships, and scalable data-platform development to improve their competitive positions over the forecast period.

LIST OF KEY AI-ENABLED MEDICAL DEVICES COMPANIES PROFILED

- Medtronic (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- ai, Inc. (U.S.)

- Intuitive Surgical Operations, Inc. (U.S.)

- General Electric Company (U.S.)

- Aidoc (Israel)

- Digital Diagnostics Inc. (U.S.)

- TEMPUS (U.S.)

- iRhythm Technologies, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: GE HealthCare announced a collaboration with Diagnoly to advance AI-enabled fetal ultrasound offerings. This is relevant as it expands AI use in obstetric imaging and supports device-linked ultrasound workflow enhancement.

- November 2025: Siemens Healthineers introduced Optiq AI for its latest interventional systems portfolio. The company said the AI-powered imaging chain is designed to deliver higher-quality low-dose images for image-guided procedures across interventional radiology, cardiology, and minimally invasive surgery.

- November 2025: Butterfly Network launched Compass AI, an AI-powered enterprise platform for POCUS program management.

- October 2025: Intuitive announced the U.S. FDA-cleared software advancements for its Ion endoluminal system, expanding AI and advanced imaging integration for lung biopsy procedures.

- June 2025: Hyperfine announced FDA clearance for its next-generation Swoop portable MRI system powered by Optive AI software.

REPORT COVERAGE

The global market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market throughout the forecast period. It provides understanding of essential factors, including technological progress, product innovations, the regulatory environment, and the launch of new products. Additionally, it details partnerships, mergers & acquisitions, as well as key developments in the industry within the market. The global AI-enabled medical devices market forecast report also provides an in-depth competitive landscape, including information on market share and profiles of key active players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 19.85% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Technology, Specialty, Application, End User, and Region |

| By Component |

|

| By Technology |

|

| By Specialty |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 9.11 billion in 2025 and is projected to reach USD 45.87 billion by 2034.

In 2025, the market value stood at USD 3.79 billion.

The market is expected to exhibit a CAGR of 19.85% during the forecast period.

By component, the hardware & devices segment is expected to lead the market.

The growing need for faster and more accurate diagnostic solutions coupled with increasing number of medical imaging procedures are primarily driving market expansion.

Medtronic, Siemens Healthineers AG, and Koninklijke Philips N.V. are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 164

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us