AI In Cancer Diagnostics Market Size, Share & Industry Analysis, By Component (Software & Services), By Technology (Computer Vision, Machine Learning & Deep Learning, Natural Language Processing, & Others), By Modality (Liquid Biopsies, Imaging Diagnostics, Digital Pathology AI, Genomics and Biomarker Discovery, & Others), By Application (Screening support, Triage & Prioritization, Staging Support, & Others), By Deployment (Cloud-Based, On Premise, & Hybrid), By Cancer Type (Breast Cancer, Lung Cancer, Colorectal Cancer, Prostate Cancer, & Others), By End User, and Regional Forecast, 2026-2034

AI in Cancer Diagnostics Market Size and Future Outlook

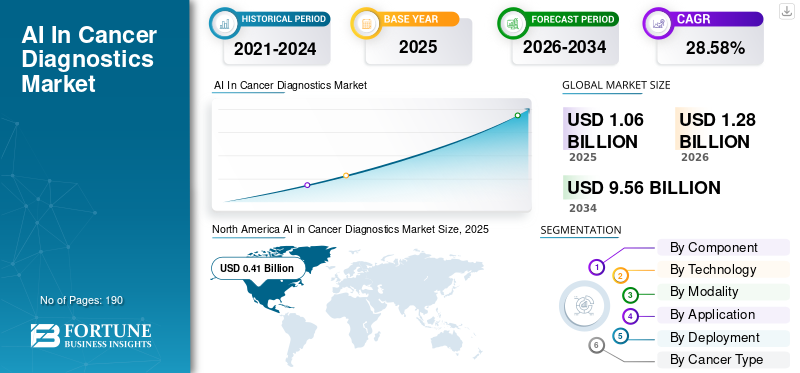

The global AI in cancer diagnostics market size was valued at USD 1.06 billion in 2025. The market is projected to grow from USD 1.28 billion in 2026 to USD 9.56 billion by 2034, exhibiting a CAGR of 28.58% during the forecast period. North America dominated the AI in cancer diagnostics market with a market share of 38.67% in 2025.

The global AI in cancer diagnostics market is projected to grow significantly in the coming years, driven by the rising prevalence of cancer and the increasing demand for scalable diagnostic tools. These solutions help healthcare providers and labs to detect, triage, and characterize cancer using data from imaging, digital pathology, genomics, and related diagnostic workflows at large volumes. With an increasing focus on improving early detection and treatment and reducing turnaround times by healthcare providers, the market is projected to grow. As hospitals and labs digitize workflows and connect data systems, AI solutions are increasingly used to support more consistent reads, faster prioritization of high-risk cases, and more standardized reporting across sites, with varied applications that further support growth in the global market.

Key companies operating in the market are increasingly focusing on new product launches to capitalize on the market's growth potential and on incorporating AI capabilities into their diagnostic solutions.

- For instance, in September 2024, F. Hoffmann-La Roche Ltd announced the expansion of its digital pathology open environment by integrating more than 20 advanced artificial intelligence (AI) algorithms. These collaborations aimed to support pathologists and scientists in cancer research and diagnosis by leveraging cutting-edge AI technology to help clinicians improve patient outcomes and expand personalized healthcare. Such innovative product launches are anticipated to boost overall market growth.

Leading players in the industry, such as Aidoc Medical, Ltd, Lunit Inc., Paige.AI, Inc., and Ibex Medical Analytics Ltd., are focusing on expanding their offerings and strengthening their market positions.

Download Free sample to learn more about this report.

AI In Cancer Diagnostics Market Key Takeaways

- 2025 Market Size: USD 1.06 billion

- 2026 Market Size: USD 1.28 billion

- 2034 Forecast Market Size: USD 9.56 billion

- CAGR: 28.58% from 2026–2034

- North America dominated the AI in cancer diagnostics market with a 38.67% share in 2025.

- The digital pathology AI segment is projected to grow at a CAGR of 32.08% during the study period.

- The triage & prioritization segment is projected to grow at a CAGR of 31.39% during the study period.

North America

Valued at USD 0.49 billion in 2025, leading the market through AI commercialization and expanded screening workflows.

Europe

Projected to reach USD 0.33 billion in 2026, driven by screening expansion and diagnostic IT investments.

Asia Pacific

Expected to reach USD 0.32 billion in 2026, supported by rising cancer burden and imaging AI adoption.

U.S

Projected to reach USD 0.45 billion in 2026, supported by regional leadership and strong market share.

Japan

Projected to reach USD 0.08 billion in 2026, accounting for 6.14% of the global market.

Read More

AI IN CANCER DIAGNOSTICS MARKET TRENDS

Rising Adoption of Quantification and Biomarker Scoring in Pathology is a Significant Market Trend

Some of the prominent market trends are the increased applications for quantification and biomarker scoring by healthcare providers. As biomarker testing expands in oncology, pathologists need to score markers such as HER2 and other IHC results more reliably and efficiently. These factors create a significant need for AI tools that can help to standardize scoring, reduce variability, and speed up reporting. These features are especially helpful when case volumes rise and turnaround times are closely tracked. As diagnostic laboratories move toward digital workflows, it becomes easier to run AI in the background on routine slides, further increasing adoption.

Key companies are entering into strategic partnerships and collaborations to enhance their offerings and strengthen their market position.

- For instance, in March 2025, Koninklijke Philips N.V. expanded its partnership with Ibex Medical Analytics to enhance AI-enabled pathology workflows using the company's IntelliSite Pathology Solution for cancers such as prostate, breast, and gastric. The development aimed to support more efficient and interoperable digital pathology workflows that can include quantitative analysis and decision support.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Cancer Incidence to Drive Market Growth

The major factor driving the growth of the market is the rising cancer incidence. As the number of patients entering diagnostic pathways increases, radiology and pathology capacity experience increased workload pressure. These factors encourage providers to increasingly seek scalable diagnostic tools that can help them triage large caseloads, flag suspicious findings earlier, and standardize reads across sites. As screening volumes grow, AI becomes more valuable as it can support faster prioritization and more consistent interpretation without needing a proportional increase in specialist headcount. Major operating companies are increasingly adopting these solutions to manage large-scale patient volumes, further reinforcing AI in cancer diagnostics market growth.

- For instance, in February 2025, the U.K. government announced a world-leading trial where nearly 700,000 women would take part to test how AI tools can help detect cancer earlier through NHS screening. Such development showcases how growing screening programs are driving real-world deployment at scale.

MARKET RESTRAINTS

Regulatory Complexity and Slow Update Cycles to Limit Market Growth

Regulatory complexity in the cancer diagnostic market is a major restraint on market growth. AI models need regular updates to stay accurate across new scanners, new protocols, and changing clinical data practices; however, regulated healthcare software cannot be updated as easily as consumer software. Additionally, every model change triggers additional documentation, testing, and submission requirements, leading to longer release cycles and higher compliance costs. These factors can delay hospital rollouts and slow the transition from pilot programs to enterprise-wide deployment. As a result, when clinical value is proven, adoption may stall due to challenges related to audit readiness and performance drifts.

- For instance, in August 2024, Health Policy and Technology published an article titled 'Defining change: Exploring expert views about the regulatory challenges in adaptive artificial intelligence for healthcare, highlighting how AI systems create coordination and governance for regulators.

MARKET OPPORTUNITIES

Growing AI Adoption in Emerging Markets with Improving Diagnostic Infrastructure to Offer Several Growth Opportunities

As diagnostic infrastructure improves in emerging markets, more hospitals and diagnostic laboratories are moving from manual and fragmented workflows to connected digital systems for imaging, pathology, and lab data. This directly increases use cases for AI, as AI these tools perform best when integrated into standardized workflows, consistent data formats, and repeatable reporting processes. This creates a clear growth opportunity for AI vendors as AI can help prioritize high-risk cases, reduce turnaround times, and improve consistency across distributed facilities. Over time, as adoption expands beyond Tier-1 hospitals into regional centers and emerging markets, deployments can shift from pilots to multi-site rollouts, driving faster and more sustained revenue growth.

- For instance, in January 2025, NEC Corporation and Biomy, Inc. announced a joint marketing partnership to develop and expand AI/deep learning-based analytical platforms in digital pathology to promote precision medicine for cancer. Such developments demonstrate the market's growth potential and support AI-enabled cancer diagnostics.

MARKET CHALLENGES

Unclear Reimbursement and Coverage Pathways for AI-Enabled Cancer Diagnostics Pose a Challenge for Market Growth

A key challenge faced by the market is reimbursement uncertainty and complex coverage pathways. Many hospitals and diagnostic laboratories hesitate to invest in large-scale AI purchases unless they can clearly recover costs through payer coverage. When payment rules are unclear, buyers treat AI as an additional expense rather than a standard-of-care tool, slowing procurement approvals. This also complicates budgeting across regions, as the same AI solution may be reimbursed in one country but treated as a non-billable expense in another. As a result, vendors face longer sales cycles and are pressured to discount or bundle AI into broader software contracts, limiting standalone revenue growth. Over time, this slows market penetration even when clinical performance is strong, as financial incentives are not consistently aligned with adoption.

- For instance, in November 2025, JACR published an article titled 'Reimbursement for Artificial Intelligence Software as a Medical Device in Radiology' that reported adoption of U.S. FDA-cleared AI tools remains limited due to nascent reimbursement policies, highlighting how reimbursement uncertainty constrains market growth potential.

Segmentation Analysis

By Component

Software Segment Led the Market owing to Rising Investments by Key Players in Developing Software Solutions

Based on component, the market is categorized into software and services.

The software segment accounted for the largest share of the global market. The segment dominated as most buyers pay first for the core AI engine and the platform layer that integrates into PACS, pathology viewers, or diagnostic workflows. These software products are scaled across more studies, users, and sites at relatively low incremental cost, making it easier for hospitals and networks to justify larger budgets for software subscriptions. As providers push for repeatable, enterprise-wide rollouts, software becomes the main revenue driver, while services are increasingly bundled, standardized, or limited to implementation and support. Additionally, they account for revenue share, encouraging key players to invest in developing software solutions and new product launches to monetize their growth.

- For instance, in February 2025, DeepHealth introduced AI-powered radiology informatics and population screening solutions enabled by its cloud-native DeepHealth OS, reinforcing how platform software is becoming the central purchase point for scalable cancer screening workflows.

The services segment is expected to grow at a CAGR of 22.75% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Increasing Application of Computer Vision in Imaging Boosted Segment Growth

Based on technology, the market is segmented into computer vision, machine learning & deep learning, natural language processing, and others.

In 2025, the computer vision segment accounted for the largest market share. Computer vision dominates, as the most immediate diagnostic AI use cases in oncology are built around imaging-based interpretation. AI models can detect, segment, and quantify suspicious findings directly from scans or pathology slides. These features create tangible operational value by offering faster reads, more consistent interpretation, and earlier flagging of high-risk cases, which are especially useful in high-volume settings. As a result, most commercialized cancer diagnostic AI solutions are fundamentally computer-vision-led, with other technologies supporting adjacent workflow steps.

Key companies are focusing on technologically advanced offerings and the regulatory approvals that accompany them to strengthen their market position.

- For instance, in July 2025, SimBioSys received 510(k) clearance from the U.S. FDA for TumorSight Viz, highlighting the continued commercialization of imaging-based computer vision AI tools in breast cancer care.

The natural language processing segment is projected to grow at a CAGR of 32.25% during the forecast period.

By Modality

Increasing Adoption of AI in Liquid Biopsies to Lead Growth in the Segment

Based on modality, the market is segmented into liquid biopsies, imaging diagnostics, digital pathology AI, genomics and biomarker discovery, and others.

In 2025, the liquid biopsies dominated the market, as healthcare systems prioritize scalable, minimally invasive testing and need tools that can interpret complex molecular signals from blood-based assays. As liquid biopsy adoption grows for treatment selection and monitoring, AI becomes critical for quickly and consistently converting raw sequencing signals into clinically actionable outputs. These factors collectively drive demand for global market from biopharmaceutical companies and advanced clinical labs, particularly as tests are deployed across multiple institutions and require standardized interpretation. Additionally, key companies in the market are focusing on strategic collaboration, underscoring their high importance.

- For instance, in April 2025, SOPHiA GENETICS expanded its collaboration with AstraZeneca to accelerate MSK-ACCESS. This is powered by SOPHiA DDM, a liquid biopsy testing application designed to detect actionable alterations from a blood draw, supporting broader deployment across institutions.

The digital pathology AI segment is projected to grow at a CAGR of 32.08% during the study period.

By Application

Increasing Screening Volumes Boosted Segment Growth

Based on application, the market is segmented into screening support, triage & prioritization, staging support, quantification & biomarker scoring, clinical decision support, and others.

Screening support accounted for the largest global AI in cancer diagnostics market share during the forecast period. Screening programs generate very high volumes, and even small improvements in sensitivity, consistency, and prioritization can translate into meaningful operational impact. As screening volumes rise, providers face pressure to maintain turnaround times and reduce missed findings without expanding specialist headcount at the same pace. These factors have led to the increasing adoption of AI screening tools to improve reading efficiency and standardize outcomes across sites. These advantages make screening support one of the most commercially attractive application areas, encouraging key companies to innovate their offerings through strategic collaborations.

- For instance, in October 2024, Lunit announced a partnership with VIDI Group to deploy Lunit INSIGHT MMG across France's largest radiology network. This collaboration aimed to improve breast cancer screening efficiency and quality at scale. Such development highlights how screening programs are increasingly adopting AI as a scalable support layer.

The triage & prioritization segment is projected to grow at a CAGR of 31.39% during the study period.

By Deployment

Scalability Opportunity offered by Cloud-Based Deployments Led Segment Growth.

Based on deployment, the market is segmented into cloud-based, on-premises, and hybrid.

In 2025, the cloud-based deployment accounted for the largest share. These deployments reduce the time and complexity required to roll out AI across multiple sites, simplify updates and monitoring, and make it easier to scale capacity as volumes increase. For large screening and imaging networks, the cloud supports centralized governance, consistent version control, and faster onboarding of new tools. As a result, buyers increasingly favor cloud or cloud-enabled architectures when they want AI to move beyond pilot programs into repeatable, enterprise-scale deployments.

- For instance, in September 2025, the U.K. government announced a new cloud computing system that would allow AI tools to be tested at an unprecedented scale across NHS screening, reflecting the shift toward cloud infrastructure to operationalize screening AI.

The hybrid segment is projected to grow at a CAGR of 27.62% over the study period.

By Cancer Type

Breast Cancer Segment Leads As Integration Of AI Helps Standardize Reads And Prioritize Suspicious Cases

Based on cancer type, the market is segmented into breast cancer, lung cancer, colorectal cancer, prostate cancer, brain & nervous system cancers, and others.

The breast cancer segment accounted for a significant market share in 2025. Breast cancer is one of the high-volume screening pathways. This creates high demand for tools that can scale mammogram reading capacity without adding specialist headcount. As mammography programs expand, providers face higher workload and tighter turnaround targets to reduce missed findings. These factors result in the integration of AI to standardize reads and prioritize suspicious cases. The segment also benefits from mature datasets, validation evidence, and established clinical workflows. These factors collectively reinforce the segment dominance. Expanding product portfolio of key companies through strategic collaborations and partnerships further reinforces the segment's dominance.

- For instance, in May 2025, RamSoft announced a commercial partnership to integrate Therapixel's MammoScreen AI breast imaging software into RamSoft's PowerServer and OmegaAI platforms, showing how breast cancer screening AI is being scaled through workflow-integrated, enterprise deployments.

The lung cancer segment is projected to grow at a CAGR of 31.24% over the study period.

By End User

Increasing Investment in Improving Operational Efficiency Encouraged Hospitals and ASCs Segment Growth

Based on end user, the market is segmented into hospitals & ASCs, diagnostic laboratories, research & academic institutes, and others.

Hospitals and ASCs dominated the market as they control the largest share of diagnostic decision-making across imaging, pathology coordination, and multidisciplinary care pathways. They also face the greatest pressure on turnaround times, capacity, and patient throughput, making them more likely to invest in AI solutions that improve operational efficiency and reduce diagnostic delays. As hospitals standardize diagnostic workflows across networks, they tend to purchase enterprise licenses and invest in integration of AI platforms, driving the largest revenue contribution among end users. Strategic collaborations between AI solution providers and hospitals are further supporting the segment's growth.

- For instance, in May 2025, NTT DATA and The Royal Marsden launched a large-scale AI radiology platform to improve cancer detection and treatment, illustrating how major hospital settings are leading AI deployment and spending.

The diagnostic laboratories segment is projected to grow at a CAGR of 30.80% over the study period.

AI in Cancer Diagnostics Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America AI in Cancer Diagnostics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 0.35 billion and maintained its leading position in 2025 at USD 0.49 billion. The market in the region is expected to grow significantly over the forecast period, driven by faster commercialization of clinically validated AI, strong hospital purchasing power, and scaling screening workflows to manage high imaging volumes and specialist shortages.

U.S. AI in Cancer Diagnostics Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 0.45 billion by 2026, accounting for roughly 35.35% of global sales.

Europe

Europe is projected to grow at 26.40% over the coming years, the second-highest among all regions, and reach a valuation of USD 0.33 billion by 2026. The region is expected to grow due to rising adoption as national health systems expand standardized screening and invest heavily in interoperable diagnostic IT.

U.K. AI in Cancer Diagnostics Market

The U.K.'s market is estimated at around USD 0.05 billion by 2026, representing roughly 4.06% of the global market.

Germany AI In Cancer Diagnostics Market

Germany's market is projected to reach approximately USD 0.09 billion by 2026, equivalent to around 6.78% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 0.32 billion by 2026 and secure the position of the third-largest region in the market. The market is growing rapidly as the rising cancer burden and expanding diagnostic infrastructure are driving demand for scalable tools and accelerating digital pathology and imaging AI deployments.

Japan AI in Cancer Diagnostics Market

The Japanese market in 2026 is estimated at around USD 0.08 billion, accounting for approximately 6.14% of the global market.

China AI in Cancer Diagnostics Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.11 billion, representing approximately 8.52% of global sales.

India AI in Cancer Diagnostics Market

The market in 2026 is estimated at around USD 0.03 billion, accounting for roughly 2.08% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The market is set to reach a valuation of USD 0.06 billion by 2026. The region is experiencing market growth supported by the expansion of private diagnostics and imaging networks that use AI to improve throughput and consistency. In the Middle East & Africa, the GCC is set to reach USD 0.06 billion by 2026.

South Africa AI in Cancer Diagnostics Market

The South African market is projected to reach approximately USD 0.01 billion by 2026, accounting for roughly 0.77% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Strategic Collaborations to Enhance Back-Office Software Automation

The global AI in cancer diagnostics market is highly consolidated, with companies such as Aidoc Medical, Ltd., Lunit Inc., Paige.AI, Inc., Ibex Medical Analytics Ltd., iCAD, Inc., and ScreenPoint Medical B.V. holding significant market share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector drive these companies' market share gains.

- For instance, in June 2023, Lunit Inc., a leading provider of AI-powered cancer diagnostics, collaborated with Thales, a global leader in software monetization and licensing, to accelerate the profitability of its software, protect its core technology, and enhance back-office software automation.

Other notable players in the global market include Proscia Inc, SOPHiA GENETICS SA, and Tempus AI, Inc. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions during the forecast period.

LIST OF KEY AI IN CANCER DIAGNOSTICS COMPANIES PROFILED

- Aidoc Medical, Ltd (Israel)

- Lunit Inc (South Korea)

- AI, Inc. (U.S.)

- Ibex Medical Analytics Ltd (Israel)

- iCAD, Inc. (U.S.)

- ScreenPoint Medical B.V. (The Netherlands)

- Proscia Inc. (U.S.)

- SOPHiA GENETICS SA (Switzerland)

- Tempus AI, Inc. (U.S.)

- Medtronic plc. (Ireland)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Lord's Mark Industries Limited collaborated with the Centre for Materials for Electronic Technology (CMET) and signed a Technology Transfer Agreement to manufacture an AI-powered, radiation-free Breast Screening Wearable Device for early detection of breast cancer.

- March 2026: Perimeter Medical Imaging AI, Inc. received premarket approval from the U.S. FDA for Claire, the first AI-enabled imaging device approved in the U.S. for intraoperative breast cancer margin assessment. The technology received Breakthrough Device designation from the FDA and is designed to enhance surgeons' ability to detect difficult-to-see cancer during breast-conserving surgery and potentially reduce the need for re-operations.

- August 2025: PathAI collaborated with Moffitt Cancer Center to deploy its digital pathology platform, AISight Dx, across Moffitt's pathology programs to transform cancer detection and innovation.

- February 2025: Aiforia Technologies Plc obtained the In Vitro Diagnostic Regulation (IVDR) certification and launched three CE-IVD-marked AI models for breast and prostate cancer diagnostics. BSI Group granted the certification, enabling the company to bring an expanded portfolio of AI models to the European market.

- October 2024: DeepHealth acquired Kheiron Medical Technologies Limited, a U.K.-based AI cancer diagnostic company focused on developing deep learning solutions to support radiologists in improving breast cancer detection. The development provided access to Kheiron's Mia (Mammography Intelligent Assessment) suite of AI solutions for a breast cancer screening portfolio roadmap aimed at large-scale diagnostic and screening programs.

REPORT COVERAGE

The global AI in cancer diagnostics market analysis includes a comprehensive study of market size & forecast across all market segments covered in the report. It contains details on the market dynamics and trends expected to drive the global market. It provides information on key aspects, including technological advancements and new product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments. The global market research report also provides a detailed competitive landscape and profiles of major operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 28.58% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Technology, Modality, Application, Deployment, Cancer Type, End User, and Region |

| By Component |

|

| By Technology |

|

| By Modality |

|

| By Application |

|

| By Deployment |

|

| By Cancer Type |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.06 billion in 2025 and is projected to reach USD 9.56 billion by 2034.

In 2025, the market value stood at USD 0.41 billion.

The market is expected to grow at a CAGR of 28.58% over the forecast period.

By component, the software segment is expected to lead the market.

Rising cancer incidence and the expansion of screening programs are driving the market.

Aidoc Medical, Ltd, Lunit Inc., Paige.AI, Inc., Ibex Medical Analytics Ltd., and iCAD, Inc are the top players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us