AI in Computer Vision Market Size, Share & Industry Analysis, By Component (Hardware, Software, and Services), By Function (Training and Inference), By Technology (Deep Learning and Generative AI), By Application (Predictive Maintenance, Quality Assurance and Inspection, Positioning and Guidance, and Others (Identification and Measurement, etc.)), By Industry (Consumer Electronics, Automotive, Retail, Healthcare, Manufacturing, and Others (Security & Surveillance, Transportation, etc.)), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

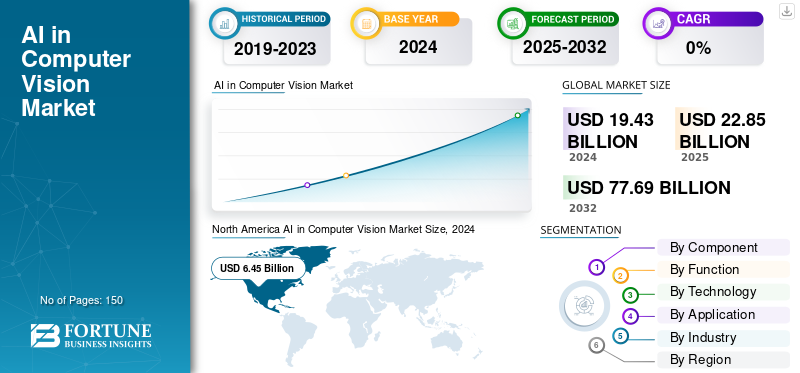

The global AI in computer vision market size was valued at USD 22.85 billion in 2025. The market is projected to grow from USD 27.01 billion in 2026 to USD 100.78 billion by 2034, exhibiting a CAGR of 17.89% during the forecast period. North America dominated the global AI in computer vision market with a market share of 32.47% in 2025.

AI in computer vision is a field of artificial intelligence that uses machine learning and deep learning, allowing computers to understand and analyze visual data such as images or videos. The technology enables machines to "see" and grasp their environment, allowing them to carry out functions such as object recognition, image classification, and scene understanding, which in turn helps them to make decisions based on the visual data. The major applications cover autonomous vehicles, medical image analysis, and content moderation.

Market expansion is largely influenced by demand for automation, technological innovations, and the proliferation of AI in different industries such as automotive, healthcare, and security. Besides the necessity for greater operational efficiency and quality control in the manufacturing industry, improvements in hardware, such as GPUs and edge devices, and the growing use of cloud computing for scalable infrastructure also contribute substantially to market growth.

The top firms in the industry are NVIDIA Corporation, Microsoft Corporation, Intel Corporation, Alphabet, Inc., Amazon.com, Inc. and Sony Corporation.

Download Free sample to learn more about this report.

AI in Computer Vision Market Key Takeaways

- 2025 Market Size: USD 22.85 billion

- 2026 Market Size: USD 27.01 billion

- 2034 Forecast Market Size: USD 100.78 billion

- CAGR: 17.89% from 2026–2034

- North America dominated the AI in computer vision market with a 32.47% share in 2025.

- The hardware segment is projected to lead the market with a 57.71% share in 2026.

- The inference segment is expected to account for 66.20% of the global market in 2026.

North America

North America reached USD 7.42 billion in 2025 and is projected to grow to USD 8.56 billion in 2026, supported by strong investments in AI technologies and digital transformation initiatives.

Europe

Europe generated USD 4.31 billion in 2025 and is anticipated to expand further in 2026, benefiting from increasing deployment of AI-powered computer vision solutions across industries.

Asia Pacific

Asia Pacific accounted for USD 8.10 billion in 2025 and is expected to reach USD 9.88 billion in 2026, driven by expanding AI adoption across manufacturing, automotive, and healthcare sectors.

U.S.

The market is estimated to reach USD 5.85 billion by 2026, supported by rapid innovation in AI infrastructure, autonomous systems, and enterprise AI applications.

Japan

The market is projected to reach USD 1.95 billion by 2026, driven by growing adoption of AI-enabled vision systems in manufacturing, robotics, and smart automation.

Read More

Impact of Gen AI

Gen AI Speeds Model Development and Enhances Computer Vision Innovation

Generative AI is a major factor in transforming the computer vision environment by improving the system’s intelligence, flexibility, and creativity. For example, it allows models to generate synthetic data, visually reconstruct missing parts, and even simulate scenarios that improve algorithm training and accuracy. Consequently, the need for large labeled datasets is greatly reduced, and the model development cycles are fast-tracked. With advanced deep learning architectures, generative AI supports applications such as image restoration, object detection, and autonomous navigation. The healthcare, automotive, and retail industries, among others, are using these propellers to improve diagnostics, automate visual inspections, and deliver personalized experiences, thus fueling innovation across AI in computer vision market.

Impact of Reciprocal Tariff

Reciprocal Tariff Disrupt AI Hardware Supply Chain, Delaying Development and Slowing Innovation

The global supply chain has been disrupted by the imposition of reciprocal tariffs between the major economies, leading to uncertainty in both the availability and the pricing of hardware components necessary for AI and computer vision systems. The prices of key components such as GPUs, sensors, and semiconductor chips are subject to fluctuations, and the lead times are becoming longer. These products cause product development and large-scale deployment of AI-powered visual systems to be delayed, the effect being most pronounced in the manufacturing and automotive sectors. Additionally, the imposition of trade barriers hinders the advancement of international collaborations and technology transfer, thereby slowing the pace of innovation.

MARKET DYNAMICS

Market Drivers

Increased Availability of Visual Data Drives Market Growth

With the worldwide adoption of digital imaging technologies, such as smartphones, drones, CCTV systems, and IoT-enabled devices, visual data has increased in volume. Such a rise in the mainstay for deploying sophisticated computer vision applications, as AI models are very dependent on large and varied datasets for their training. Better image quality and more extensive data availability enhance model performance, precision, and flexibility across various industries. The technologies have brought vast benefits that can be seen in almost every industry, such as facial recognition, autonomous systems, retail analytics, healthcare diagnostics, and many more. Consequently, the increased availability of visual content is one of the primary factors driving the expansion of AI in computer vision market.

Market Restraints

High Infrastructure and Integration Costs Hinder Growth

One of the major challenges for AI in computer vision market growth that still persists alongside the booming demand for AI-powered visual intelligence is the high expense related to infrastructure and integration. To deploy computer vision solutions, a powerful computational resource is necessary such as top-of-the-line GPUs, storage systems, and dedicated servers. In addition to this, organizations are required to spend in software development, cloud integration, and skilled labor to achieve a successful implementation. Such capital-intensive requirements can cause small and medium enterprises with limited budgets to slow down the adoption process. Furthermore, integrating AI-based visual analytics into existing processes without disrupting operations requires considerable and technical expertise. Therefore, the high upfront and maintenance costs still remain the main reasons for the limited large-scale spread of AI in computer vision market.

Market Opportunities

Government Initiatives and Investments Open Up Growth Prospects

Governments worldwide are placing greater emphasis on AI development enhance technological competitiveness and digital innovation. National AI strategies, public private partnerships, and funding initiatives are creating a comprehensive ecosystem for startups, research institutes and enterprises to engage in computer vision. Besides that, a majority of nations are heavily investing in AI infrastructure, cloud computing, and technologies to speed up the deployment of visual intelligence in smart cities, security, healthcare, and agriculture sectors. Also, the implementation of regulations allowing the use of ethical AI is promoting a trustworthy ecosystem for businesses and citizens. Such efforts stimulate locals and global markets as well as open up new opportunities for regional innovation hubs and cross-vector collaboration in computer vision.

AI IN COMPUTER VISION MARKET TRENDS

Advancements in AI Hardware Emerges as a Major Market Trend

As AI hardware rapidly evolves, the technologies supporting computer vision models must be reconsidered from scratch. Essentially, the new hardware accelerators, such as GPUs and TPUs, as well as AI-specific chips, are making computations more efficient and less energy-consuming to a significant extent. These developments fuel the technologies for real time image processing, edge computing, and enhanced inference capabilities, which thus provide tuned vision applications that address the issues of speed and scalability. Through hardware optimization, enterprises can integrate small devices with complex AI algorithms that can revolutionize the areas of the co-driver system, surveillance, and industrial automation. Hence, hardware technology continues to evolve and remains a key factor in the performance optimization of AI-driven computer vision systems.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Component

High-Performance Processing for AI Workloads Boosts Hardware Segment Growth

Based on the component, the market is segmented into hardware, software, and services.

Hardware occupied the largest market share of USD 10.05 billion in the global market in 2024. The increased growth of this segment is due to its ability to allow for high performance processing for AI workloads, particularly in edge devices and specialized accelerators such as GPUs and NPUs. The Hardware segment is projecteed to dominate the market with a share of 57.71% in 2026.

Software segment captures the maximum CAGR of 23.28% in the global market. The segment's growth is attributable to the growing demand for advanced AI algorithms, vision models, and cloud-based platforms that enable scalable and flexible computer vision applications across industries.

By Function

Inference Segment Leads Market Owing to Its Role in Real-Time Decision-Making

Based on the function, the market is segmented into training and inference.

The inference segment leads with a market share of USD 11.56 billion. The increased growth of this segment can be attributed to its ability to allow for real-time decision-making in applications such as autonomous vehicles, surveillance, and industrial automation that necessitate fast, on-device processing. The inference segment is expected to lead the market, contributing 66.20% globally in 2026.

Training captures the maximum CAGR of 21.49% in the market. The segment’s growth is mainly owing to the increasing need for advanced model development and the growing availability of large, labeled datasets to improve the accuracy and performance of AI-powered computer vision systems.

By Technology

Ability to Extract Features and Learn Complex Patterns Augments the Deep Learning Segment Growth

Based on the technology, the market is segmented into deep learning and generative AI.

The deep learning segment accounted for the largest AI in computer vision market share at USD 13.12 billion in 2024. The growth can be attributed to its ability to automatically extract features and learn complex patterns from large datasets, making it the foundation for most advanced computer vision applications. The deep learning segment is projecteed to dominate the market with a share of 37.59% in 2026.

Generative AI represent the largest CAGR at 21.40% in the global market. The growth is due to its ability to create synthetic data, enhance model training, and enable new applications in content generation, design, and data augmentation within computer vision.

By Application

Defect Detection and Process Optimization Augments the Quality Assurance and Inspection Segment Growth

Based on the application, the market is segmented into predictive maintenance, quality assurance and inspection, positioning and guidance, and others (identification and measurement, etc.).

The quality assurance and inspection segment accounted for the largest share at USD 7.63 billion in 2024. The segment’s growth is due to the increased adoption of AI-powered automation for defect detection, process optimization, and ensuring high-quality standards in manufacturing and production lines.

Positioning and guidance represent the largest CAGR at 23.10% in the global market. The segment’s growth is attributable to the increasing demand for autonomous systems, robotics, and navigation solutions in logistics, automotive, and aerospace industries.

To know how our report can help streamline your business, Speak to Analyst

By Industry

Rapid Adoption in ADAS and Autonomous Vehicles Augments the Automotive Segment Growth

Based on the industry, the market is segmented into consumer electronics, automotive, retail, healthcare, manufacturing, and others (security & surveillance, transportation, etc.).

The automotive sector represented the largest market share in 2024, at USD 5.80 billion. The growth in this segment is attributable to the fast adoption of AI-powered computer vision technologies in advanced driver-assistance systems (ADAS) and autonomous vehicles, contributing to the substantial demand for these technologies. The automotive segment is expected to lead the market, contributing 29.60% globally in 2026.

Manufacturing constituted to a maximum CAGR at 21.34% in the market. The sector's growth is attributable to the increasing adoption of AI-driven automation, quality control, and predictive maintenance solutions to improve operational efficiencies and reduce costs in production environments.

AI IN COMPUTER VISION MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

North America AI in Computer Vision Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America held 32.47% of the global market share, reaching a valuation of USD 7.42 Billion, and is projected to grow to USD 8.56 Billion in 2026. The region’s growth is attributable to strong presence of key technology companies, early adoption of AI solutions, and significant investments in AI research and development across various industries.

The U.S. is at the forefront of the North American market, with expected revenue of USD 5.11 billion in 2025. The expansion is a result of strong adoption in industries such as healthcare, automotive, and security, which is further strengthened by a robust tech ecosystem, research infrastructure, and government funding. The U.S. market is estimated to reach USD 5.85 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

Europe

The market in Europe reached USD 4.31 Billion in 2025, representing 18.86% of total market revenue, and is projected to reach USD 5. Billion in 2026. This growth is due to the increasing demand for automation, government investments in digital transformation, growing adoption across key industries such as automotive and healthcare, and the rise of smart devices.

The UK market is estimated to reach USD 0.95 billion by 2026, and the Germany market is estimated to reach USD 0.93 billion by 2026.

Asia Pacific

Asia Pacific contributed approximately USD 8.1 Billion to the global market in 2025, accounting for 35.40% share, and is expected to reach USD 9.88 Billion in 2026. The region’s growth is attributable to rapid technological advancements, increased investments in AI infrastructure, and the growing adoption of AI-powered solutions across industries such as manufacturing, automotive, and healthcare in countries such as China, Japan, and South Korea.

The Japan market is estimated to reach USD 1.95 billion by 2026, the China market is estimated to reach USD 1.99 billion by 2026, and the India market is estimated to reach USD 1.41 billion by 2026.

South America and Middle East & Africa

The Middle East & Africa region captured 18.86% of the global market in 2025, generating USD 1.89 Billion in revenue, and is projected to reach USD 2.24 Billion in 2026. The growth is due to growing demand for automation and operational efficiency, government-backed digital transformation initiatives, and rising application in industries such as manufacturing, automotive, and surveillance.

GCC countries are predicted to have a market share of USD 0.60 billion by 2025.

Latin America

In 2025, Latin America generated USD 1.13 Billion, contributing 4.95% to global market revenue, and is projected to grow to USD 1.32 Billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Firms Expand Their Product Offerings to Stay Ahead of Competition

The leading firms in the industry are NVIDIA Corporation, Microsoft Corporation, Intel Corporation, Alphabet, Inc., Amazon.com, Inc. and Sony Corporation. The firms employ strategies such as research and development, partnerships and acquisitions, expansion of product portfolio, and hardware advancements. They are also developing cutting-edge hardware and software solutions for various sectors such as automotive, healthcare, and manufacturing to stay ahead of competition.

LIST OF KEY AI IN COMPUTER VISION COMPANIES PROFILED:

- NVIDIA Corporation (U.S.)

- Microsoft Corporation (U.S.)

- Intel Corporation (U.S.)

- Alphabet, Inc. (U.S.)

- com, Inc. (U.S.)

- Sony Corporation (Japan)

- OMRON Corporation (Japan)

- KEYENCE Corporation (Japan)

- SICK AG (Germany)

- Basler AG (Germany)

- Hailo Technologies Ltd. (Israel)

- Teledyne Technologies (U.S.)

- Cognex Corporation (U.S.)

- Qualcomm Technologies, Inc. (U.S.)

- Texas Instruments Incorporated (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- October 2025- RealSense, which develops AI-powered camera vision technology, announced it has spun out of Intel and garnered a USD 50 million Series A funding round alongside a strategic partnership with NVIDIA to speed up the adoption of physical AI in humanoids and autonomous mobile robots.

- June 2025- Cognex Corporation, the global technology leader in industrial machine vision, announced the launch of OneVision™, a cloud-based platform that will transform how manufacturers build, train, and scale AI-powered vision applications.

- June 2025- NVIDIA and Deutsche Telekom have joined forces to launch Europe’s first sovereign industrial AI cloud, an initiative anchored in one of AI’s most transformative domains: vision-based intelligence. With an initial deployment of 10,000 NVIDIA Blackwell GPUs, scaling to 100,000 GPUs by 2027, the platform will serve as a digital backbone for AI-powered inspection, robotics, simulation, and visual analytics establishing Germany as the European epicentre of machine vision innovation.

- May 2025- Amniscient, a B2B SaaS company revolutionizing computer vision AI, announced the launch of AmniSphere, a computer vision AI platform designed to help businesses harness the power of AI without complexity. It provides companies of all sizes and various industries a platform to create and deploy custom computer vision models in days and with 99.9% accuracy in visual intelligence, enhancing production and efficiencies.

- January 2025- NVIDIA unveiled the most advanced consumer GPUs for gamers, creators and developers, the GeForce RTX™ 50 Series Desktop and Laptop GPUs. Powered by the NVIDIA Blackwell architecture, fifth-generation Tensor Cores and fourth-generation RT Cores, the GeForce RTX 50 Series delivers breakthroughs in AI-driven rendering, including neural shaders, digital human technologies, geometry and lighting.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Growth Rate |

CAGR of 17.89% from 2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component, Function,Technology, Application, Industry, and Region |

|

By Component |

· Hardware · Software · Services |

|

By Function |

· Training · Inference |

|

By Technology |

· Deep Learning · Generative A |

|

By Application |

· Predictive Maintenance · Quality Assurance and Inspection · Positioning and Guidance · Others (Identification and Measurement, etc.) |

|

By Industry |

· Consumer Electronics · Automotive · Retail · Healthcare · Manufacturing · Others (Security & Surveillance, Transportation, etc.) |

|

By Region |

· North America (By Component, Function, Technology, Application, Industry and Country/Sub-region) o U.S. (By Application) o Canada (By Application) o Mexico (By Application) · Europe (By Component, Function, Technology, Application, Industry and Country/Sub-region) o U.K. (By Application) o Germany (By Application) o France (By Application) o Italy (By Application) o Spain (By Application) o Russia (By Application) o Benelux (By Application) o Nordics (By Application) o Rest of Europe · Asia Pacific (By Component, Function, Technology, Application, Industry and Country/Sub-region) o China (By Application) o Japan (By Application) o India (By Application) o South Korea (By Application) o ASEAN (By Application) o Oceania (By Application) o Rest of Asia Pacific · South America (By Component, Function, Technology, Application, Industry and Country/Sub-region) o Argentina (By Application) o Brazil (By Application) o Rest of South America · Middle East & Africa (By Component, Function, Technology, Application, Industry and Country/Sub-region) o GCC (By Application) o South Africa (By Application) o Turkey (By Application) o Israel (By Application) o North Africa (By Application) o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 22.85 billion in 2025 and is projected to reach USD 100.78 billion by 2034.

The market is expected to exhibit steady growth at a CAGR of 17.89% during the forecast period.

Increased availability of visual data is speeding up the market growth.

NVIDIA Corporation, Microsoft Corporation, Intel Corporation, Alphabet, Inc., Amazon.com, Inc. and Sony Corporation are some of the top players in the market.

The North America region held the largest market share.

North America was valued at USD 7.42 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us