Cyber Weapons Market Size, Share & Russia-Ukraine War Impact Analysis, By Weapon Type (Data Extortion Tools, Destructive Malware, Surveillance Malware, Zero-Day Delivery Tools, & OT Attack Tools), By Application (Cyber Espionage, Critical Infrastructure Disruption, Defense Cyber Operations, Industrial Sabotage, Cybercrime Operations, & Others), By End User (Defense Organizations, Intelligence Agencies, Homeland Security, Specialized Cyber Units, & State Cyber Commands), By Target Environment (Defense / Military Systems, Industrial Control Systems, & Others), and Regional Forecast, 2026-2034

Cyber Weapons Market Size and Future Outlook

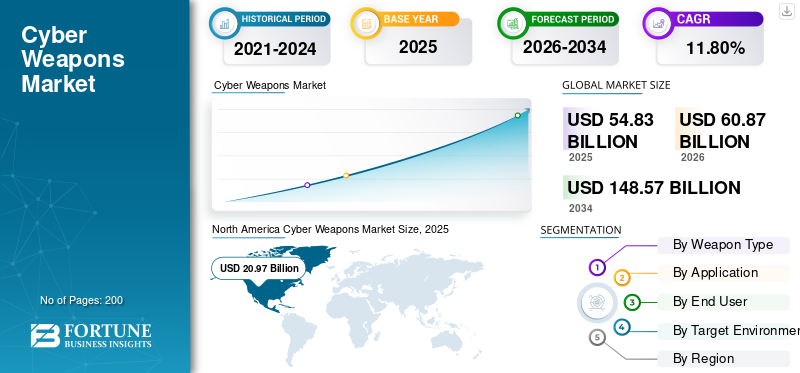

The global cyber weapons market size was valued at USD 54.83 billion in 2025 and is projected to grow from USD 60.87 billion in 2026 to USD 148.57 billion by 2034, exhibiting a CAGR of 11.80% during the forecast period. North America dominated the cyber weapons market with a market share of 38.24% in 2025.

Cyber weapons consist of malware, exploits, and code designed by states for offensive military or intelligence operations, such as sabotage, espionage, or disruption equivalent to physical attacks. Examples include Stuxnet for industrial sabotage, DDoS floods, data wipers, and spyware targeting critical infrastructure such as power grids, nuclear facilities, or financial networks. These weapons are used mainly in cyberwarfare by militaries and agencies for non-kinetic strikes amid rising geopolitical tensions. State-sponsored hacks, AI-enhanced threats, surging defense spending, and needs for asymmetric advantages over rivals are some of the driving factors pushing the market’s growth. Among the key players, there are few leading companies such as Raytheon which develops cyber defense platforms, Northrop Grumman: delivering offensive cyber integration, Lockheed Martin: handles cyber ops contracts, Booz Allen: advises on strategies, and BAE Systems: engineers advanced tools.

Download Free sample to learn more about this report.

Cyber Weapons Market Key Takeaways

- 2025 Market Size: USD 54.83 billion

- 2026 Market Size: USD 60.87 billion

- 2034 Forecast Market Size: USD 148.57 billion

- CAGR: 11.80% from 2026-2034

- North America dominated the cyber weapons market with a 38.24% share in 2025.

- The exploit kits/zero-day delivery tools segment is projected to grow at a CAGR of 12.35%.

- The critical infrastructure disruption segment is projected to grow at a CAGR of 12.35%.

North America

North America reached USD 20.97 billion in 2025 and maintained its leading market position.

Europe

Europe is projected to reach USD 14.10 billion in 2026, supported by steady cybersecurity investments.

Asia Pacific

Asia Pacific is estimated to reach USD 13.52 billion in 2026 and is expected to register the fastest regional growth.

U.S.

The market is estimated to reach USD 14.06 billion in 2026, driven by increasing cyber defense spending.

Japan

The market is projected to reach USD 2.64 billion in 2026, exhibiting a CAGR of 12.30% during the forecast period.

Read More

CYBER WEAPONS MARKET TRENDS

AI-Driven Weaponization is a Leading Trend in the Global Market

AI-driven weaponization accelerates cyber weapons through autonomous agents that autonomously scan networks, generate exploits, and launch adaptive attacks without human oversight. Open-source frameworks such as CyberStrikeAI integrate over 100 offensive tools, reducing weaponization timelines from months to weeks as threat actors deploy them operationally. State-sponsored groups leverage generative AI for real-time evasion, deepfake disinformation, and vulnerability chaining in critical infrastructure strikes. This shift industrializes attacks, enabling hybrid warfare where AI swarms overwhelm defenses faster than countermeasures evolve. Defenders counter with ML detection, however attackers maintain asymmetry in speed and scale.

Download Free sample to learn more about this report.

Russia Ukraine War Impact

The Russia-Ukraine war has accelerated cyber weapons market growth by demonstrating hybrid warfare's effectiveness, spurring global militaries to procure advanced tools. Russia's NotPetya and wiper attacks, alongside Ukraine's drone-embedded malware, showcased persistent implants and infrastructure sabotage, prompting NATO nations to boost offensive capabilities.

- In March 2026, Polish officials detected a cyberattack on their solar grid that they believe was carried out by Center 16, a cell under Russia's Federal Security Bureau that has a reputation for breaching extremely secure industrial systems.

MARKET DYNAMICS

MARKET DRIVERS

Escalating Geopolitical Tensions is anticipated to Drive Market Growth

Escalating geopolitical tensions drive cyber weapons market growth through intensified state rivalries that prioritize cyber-crimes. Conflicts such as Russia's Ukraine campaign, U.S.-China decoupling, and Iran-Israel exchanges push nations to stockpile tools for infrastructure disruption and espionage. Furthermore, heightened threats from groups such as PLA hackers, APT28, and Lazarus Group compel accelerated investments in cyber capabilities amid hybrid warfare doctrines. Additionally, proliferation of commercial exploits lowers barriers, enabling even smaller entities to compete while defense allocations surge to counter persistent network intrusions.

- In March 2026, since the beginning of the Iran War, credential harvesting attempts and automated reconnaissance traffic targeting banks and other vital enterprises have increased cybercrime by 245%, according to Akamai. Additionally, the company noticed a significant increase in credential harvesting attempts (45%), broad scanning of infrastructure and exposed services (52%), and reconnaissance prior to distributed denial of service (DDoS) attacks (38%).

MARKET RESTRAINTS

Government Budget limitations Acts as a Significant Market Restraint

Government budget strains impede cyber weapons market growth as nations oversee priorities such as drones, missiles, and personnel amid fiscal pressures. India's 2026 defense allocation faces tight limits despite cyber needs, forcing trade-offs against conventional arms and infrastructure. Taiwan's 6.6% spending cut in 2025 slashed cyber platforms, weakening readiness against China's AI threats. Furthermore, global agencies prioritize immediate services over high-cost offensive tools, with legacy procurement slowing innovation.

MARKET OPPORTUNITIES

Space-cyber integration Create New Market Opportunities

Space-cyber integration creates cyber weapons markets by targeting satellite weak spots such as jamming, spoofing, and ground hacks for military gain. Nations develop orbital malware to blind enemy ISR satellites or hijack communication channels in conflicts. Moreover, leaked military data from hacked payloads shows real risks, driving demand for advanced cyber tools against Starlink-scale networks. This orbital arms fuels contracts for persistent, deniable attacks blending cyber with space doctrines.

- In April 2026, "Gonets," a Russian low-orbit satellite communications technology advertised as Moscow's Starlink substitute, was attacked by Ukrainian cyber experts. Over the course of a multi-year intelligence operation, experts have obtained highly confidential internal documents. The "Ukrainian Militant" analytical group, 256th Cyber Assault Division, carried out the joint CYBINT (Cyber Intelligence) operation.

MARKET CHALLENGES

Legal uncertainties Present a Major Market Challenge

Legal uncertainties create major challenges by complicating development, sales, and deployment under international law. Existing international laws, crafted for physical conflicts, fail to address digital operations clearly, leaving developers unsure if their products violate sovereignty rules or proportionality standards. This ambiguity sparks endless internal reviews and legal consultations, inflating costs and timelines. For instance, there is no standard or global treaty that defines cyber weapons or bans specific malware such as Stuxnet, leaving gaps in “jus ad bellum” and “jus in bello” rules from the Tallinn Manual which provides 95 rules interpreting international law for cyber warfare.

Segmentation Analysis

By Weapon Type

High Profitability and Scalability Boost Ransomware / Data Extortion Tools’ Growth

Based on weapon type, the market is segmented into ransomware / data extortion tools, wiper / destructive malware, spyware / surveillance malware, exploit kits / zero-day delivery tools, and ICS / OT attack tools.

The ransomware / data extortion tools segment is anticipated to account for the largest market share due to their proven profitability and scalability in Ransomware-as-a-Service (RaaS) models. These subsystems generate recurring revenue through affiliate networks, outpacing one-off exploits and among others.

The exploit kits / zero-day delivery tools segment is anticipated to rise with a high CAGR of 12.35% over the forecast period.

By Application

Low Risk Nature Boosts Cyber Espionage & Intelligence Gathering’s Dominance

Based on application, the market is segmented into cyber espionage & intelligence gathering, critical infrastructure disruption, military / defense cyber operations, industrial & economic sabotage, financial extortion & cybercrime operations, and others.

In 2025, the cyber espionage & intelligence gathering segment dominated the global market. Low-risk nature boosts cyber espionage & intelligence gathering segment growth as these operations evade detection through stealthy persistence, avoiding kinetic retaliation or public backlash tied to destructive attacks.

The critical infrastructure disruption segment is projected to grow at a high CAGR of 12.35% over the forecast period.

By End User

High Budgets of Defense Organizations Makes them the Leading End User

Based on end user, the market is segmented into defense organizations, intelligence agencies, homeland security / internal security agencies, law enforcement / specialized cyber units, and state cyber commands.

The defense organizations segment is anticipated to witness a dominating cyber weapons market share over the forecast period. Defense organizations dominate as the leading end-user subsystem due to their massive budgets and strategic imperatives for offensive capabilities.

The intelligence agencies segment is projected to grow at a high CAGR of 12.37% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Target Environment

Rise in Critical Strategic Value Boosts the Defense / Military Systems Segment

Based on target environment, the market is segmented into defense / military systems, Industrial Control Systems (ICS) / OT, communication networks, transportation systems, smart grid / power systems, and others.

The defense / military systems segment dominated the market share owing to their critical strategic value in modern warfare, housing command-control networks and weapons platforms that yield outsized tactical gains.

In addition, the communication networks are projected to grow at a high CAGR of 12.36% during the study period.

Cyber Weapons Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America Cyber Weapons Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 18.92 billion, and also maintained the leading share in 2025, with USD 20.97 billion. North America commands the market through unparalleled defense spending and technological superiority, with the U.S. DoD allocating USD 30 billion annually for offensive cyber capabilities.

U.S Cyber Weapons Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 14.06 billion in 2026, accounting for roughly 12.00% CAGR over the projected timeframe. The U.S. holds absolute dominance via USCYBERCOM's global strike missions and a USD 25 billion IT/cybersecurity budget emphasizing autonomous malware and quantum-resistant tools.

Europe

Europe is projected to record a steady growth rate of 11.84%during the forecast period, which is the second highest among all regions, and reach USD 14.10 billion in 2026. Europe advances collective cyber deterrence through NATO's CCDCOE and national commands, balancing offense with Tallinn Manual compliance. France's ANSSI and Poland's cyber units procure shared exploits against Russian hybrid threats post-Ukraine.

U.K Cyber Weapons Market

In 2026, the U.K. market is estimated for USD 4.63 billion and register a 12.35% CAGR during the study period. The U.K. invests USD 1.28 billion in Strategic Defence Review's Digital Targeting Web, fusing cyber with kinetic fires under new Cyber Command.

Germany Cyber Weapons Market

Germany is projected to reach approximately USD 4.02 billion in 2026. The country’s cyber weapons growth stems from urgent NATO frontline needs against Russian hybrid threats post-Ukraine invasion. Bundeswehr modernization prioritizes persistent implants for A2/AD penetration and electromagnetic dominance in Baltic scenarios.

Asia Pacific

Asia Pacific is estimated to reach USD 13.52 billion in 2026 and become the third-largest region, while also registering fastest growth. The region’s rapid growth arises from intensifying U.S.-China maritime rivalries demanding sovereign cyber forces. Regional militaries develop modular exploits targeting carrier groups and hypersonic defenses amid Taiwan contingencies.

Japan Cyber Weapons Market

In 2026, Japan is estimated to reach USD 2.64 billion and depict a 12.30% CAGR during the forecast period. The country accelerates cyber weapons via 2025 Defense Buildup responding to PLA gray-zone coercion around Senkakus. SDF prioritizes island chain implants and submarine network attacks through NEC/Fujitsu R&D.

China Cyber Weapons Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 4.58 billion. China expands cyber weapons through military-civil fusion, mobilizing private tech for state espionage and sabotage. PLA doctrine weaponizes supply chains for pre-conflict network access against U.S. Pacific bases.

India Cyber Weapons Market

India will reach USD 3.69 billion in 2026 driven by border cyber intrusions from China/Pakistan, necessitating indigenous Defence Cyber Agency capabilities.

Rest of the World

The rest of the world includes the Middle East & Africa and Latin America. Latin America is heavily targeted by ransomware gangs, such as LockBit and RansomHub, and financial criminals, particularly in Brazil, Mexico, and Argentina which increases the demand for cyber weapons. The Middle East & Africa region escalates due to the rising Threat of State-Sponsored Attacks. In 2026, the Middle East & Africa and Latin America market is set to reach a valuation of USD 6.16 billion and USD 3.84 billion respectively.

COMPETITIVE LANDSCAPE

Key Industry Players

Government-Industry Partnerships Fuel Cyber Weapons Market Expansion

The cyber weapons market remains fragmented, featuring defense primes, cybersecurity specialists, and niche exploit developers across offensive, espionage, and infrastructure disruption niches, with key players such as Raytheon, Northrop Grumman, BAE Systems, Booz Allen Hamilton, and Israel's NSO Group among others.

Government-industry partnerships drive the competitive landscape as defense contractors collaborate with AI developers, zero-day marketplaces, and command-control specialists to engineer autonomous malware, persistent backdoors, and adaptive wipers featuring real-time evasion tactics. Raytheon and similar companies partner with national cyber commands and chip manufacturers to embed modular exploits within unified military architectures, while NSO Group works with intelligence services and regional defense forces to deliver tailored surveillance platforms and ransomware deployment systems.

LIST OF KEY CYBER WEAPONS COMPANIES PROFILED

- Raytheon Technologies (U.S.)

- Northrop Grumman (U.S.)

- Lockheed Martin (U.S.)

- BAE Systems (U.K.)

- Booz Allen Hamilton (U.S.)

- NSO Group (Israel)

- Thales Group (France)

- L3Harris Technologies (U.S.)

- Leidos (U.S.)

- Palo Alto Networks (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: In order to further their collaboration in cyber defense, Indra Group and Leonardo signed a Memorandum of Understanding (MoU) with the goal of collaboratively identifying and growing their global reach throughout Europe, NATO, and other high-potential markets.

- January 2026: Seekr announced that it has been given a contract by the U.S. Army to use agentic AI to find "cyber, system and mission vulnerabilities" in weapon systems at the Army Combat Capabilities Development Command Aviation & Missile Center (DEVCOM AvMC). There was no disclosure of the contract value.

- November 2025: The VENIN Full-Spectrum Cyber Digital Accelerator was introduced by General Dynamics Information Technology (GDIT), a division of General Dynamics. The company will quickly provide tools, technologies, and solutions to meet the changing cyber risks that government organizations must deal with.

- May 2025: As a crucial component of the People's Liberation Army's (PLA) overarching military doctrine, China's strategy for cyberwarfare extends into space. In order to interfere with enemy space-based assets, the PLA's Strategic Support Force (PLASSF) is in charge of combining space, cyber, and electronic warfare capabilities.

- October 2024: In order to support clients' defense and national security missions in the fields of artificial intelligence and autonomous systems, networking, C5ISR, electronic warfare, and cyber defense and operations, Peraton Labs has been awarded contracts totaling almost USD 100 million for advanced technology, research, development, and engineering services.

REPORT COVERAGE

The global cyber weapons market research report includes a comprehensive study of the market size & forecast by all the segments included. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements the regulatory environment, Porter’s five forces analysis, company profiles, key mergers and acquisitions and retrofitting program. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments. The report also provides an in-depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.80% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Weapon Type, Application, End User, Target Environment, and Region |

| By Weapon Type |

|

| By Application |

|

| By End User |

|

| By Target Environment |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 54.83 billion in 2025 and is projected to reach USD 148.57 billion by 2034.

In 2025, North Americas market value stood at USD 20.97 billion.

The market is expected to exhibit a CAGR of 11.80% during the forecast period of 2026-2034.

By weapon type, the ransomware / data extortion tools segment is expected to dominate the market.

Escalating geopolitical tensions is anticipated to drive market growth.

Raytheon, Northrop Grumman, BAE Systems, Booz Allen Hamilton, and Israel's NSO Group are few key players in the global market.

North America dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us