Dialysis Market Size, Share & Industry Analysis, By Type (Products {Equipment [Hemodialysis Machines (In-Center Hemodialysis Machines and Home Based Hemodialysis Machines) and Peritoneal Dialysis Equipment (Continuous Ambulatory Peritoneal Dialysis (CAPD) and Automated Peritoneal Dialysis (APD))] and Consumables [Dialyzers, Dialysate, Cyclers, Fluids, Access Products, and Others]} and Services), By Dialysis Type (Hemodialysis and Peritoneal Dialysis), By End User (Dialysis Centers & Hospitals and Home Care), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

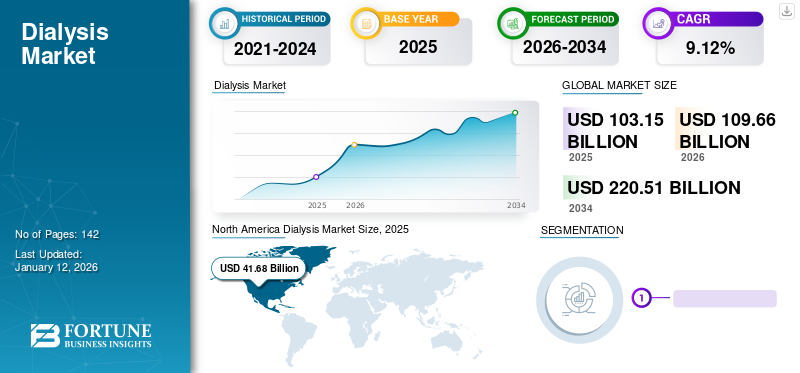

Dialysis Market Size and Future Outlook

The dialysis market size was valued at USD 103.15 billion in 2025. The market is projected to grow from USD 108.91 billion in 2026 to USD 170.19 billion by 2034, exhibiting a CAGR of 5.7% during the forecast period. North America dominated the dialysis market with a market share of 40.41% in 2025.

The prevalence of chronic kidney diseases is rising at a significant rate, which in turn, has increased patient visits to renal therapy clinics over the last decade. Rise in the number of patients opting for this treatment have increased the demand for products, such as dialysate and hemodialysis machines. As a result of this, key companies are launching new products in the market and expanding their services, thereby accelerating the market growth during the forecast period.

- For instance, in March 2023, Northwest Kidney Centers opened a new outpatient dialysis facility in the Panther Lake area of Kent. The center has 11 dialysis stations that can accommodate approximately 66 patients.

- In May 2022, Diaverum announced the acquisition of booknowmed.com, the world’s leading renal care booking website that allows patients to browse through over 400 dialysis clinics across 54 countries.

- Similarly, in September 2022, Terumo Corporation received approval from the National Medical Products Administration (NMPA), China for its peritoneal dialysis

Such new product launches and the rising prevalence of renal failure and other chronic diseases are expected to increase the patient population seeking this treatment, thereby spurring the market growth.

- For instance, as per the data published by the United States Renal Data System (USRDS) in its 2023 annual report, in 2021, the number of prevalent ESRD patients in the U.S., was 808,536.

Furthermore, Fresenius Medical Care AG, DaVita Inc., Vantive, and B. Braun SE, Ltd held the largest market share, driven by the limited market presence of other players and market consolidation.

Download Free sample to learn more about this report.

Dialysis Market Key Takeaways

- 2025 Market Size: USD 103.15 billion

- 2026 Market Size: USD 108.91 billion

- 2034 Forecast Market Size: USD 170.19 billion

- CAGR: 5.7% from 2026–2034

- North America dominated the market with a 40.41% share in 2025.

- Services accounted for the largest market share by type in 2025.

- Hemodialysis held the largest market share by dialysis type in 2025.

North America

The market reached USD 41.68 billion in 2025, driven by the high prevalence of CKD and ESRD and strong treatment adoption.

Asia Pacific

The market is projected to reach USD 24.89 billion in 2026, driven by expanding renal care infrastructure and improving treatment accessibility.

Europe

The market is projected to reach USD 28.21 billion in 2026, supported by the growing geriatric population and rising dialysis adoption.

U.S.

The market is projected to reach USD 40.32 billion in 2026.

Japan

The market is projected to reach USD 5.35 billion in 2026.

Read More

DIALYSIS MARKET TRENDS

Substantial Shift From In-Center Dialysis to Home Dialysis is Identified As Significant Market Trend

A substantial shift from in-center dialysis to home dialysis is emerging as a prominent trend in the global market. Healthcare systems, payers, and providers are increasingly encouraging treatment models that improve convenience, support patient-centered care, and reduce dependence on facility-based dialysis capacity. This trend is strengthening demand for home hemodialysis equipment, peritoneal dialysis cyclers, remote-monitoring tools, consumables, and related support services, making home-based therapy an increasingly important part of the dialysis care continuum. The trend is gaining momentum as home dialysis offers greater flexibility in treatment scheduling and can reduce the logistical burden associated with frequent travel to dialysis centers. It also aligns with broader care-delivery goals around decentralization, quality-of-life improvement, and more individualized therapy pathways. Moreover, this shift is contributing to the growing demand for home dialysis devices, installation services, patient training, digital support platforms, and recurring home-use consumables.

- For instance, according to data published by the U.S. Department of Health and Human Services (USDHHS), the percentage of incident dialysis patients performing home dialysis increased from 7.5% to 13.4% from 2011 to 2021.

The policy frameworks are increasingly designed to encourage home-based renal replacement therapy. In the U.S., CMS’s Kidney Care Choices model explicitly aims to incentivize home dialysis alongside better dialysis starts and greater transplant utilization. As reimbursement and value-based care structures evolve, home dialysis is becoming more commercially attractive for providers and more accessible for appropriately selected patients.

Additionally, ongoing product innovation and digital enablement are also likely to contribute to the penetration rate of these procedures in the market. Home dialysis pathways are increasingly supported by remote monitoring, connected treatment platforms, and improved patient support models, which make at-home therapy more manageable for both patients and care teams. This strengthens confidence in home treatment adoption and helps expand the addressable market beyond traditional in-center settings.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Prevalence of Chronic Conditions to Fuel Demand for Advanced Products

The rising burden of chronic kidney disease is a major driver for the global market. There is an increase in the number of patients requiring renal replacement therapy, especially hemodialysis or peritoneal dialysis, as CKD progresses to advanced stages and kidney function declines among patients. This directly supports demand for dialysis machines, dialyzers, bloodlines, concentrates, catheters, access products, and related consumables across hospital, clinic, and home-care settings.

- For instance, according to 2024 statistics published by Nature, it was reported that approximately 850 million people worldwide had kidney disease, most of whom live in low-income and lower-middle-income countries (LICs and LMICs), and a large proportion of these individuals lack access to kidney disease diagnosis, prevention, or treatment.

The key risk factors for these diseases are highly prevalent and persistent, resulting in growing demand for dialysis equipment in the market. Kidney disease is closely linked with diabetes and hypertension, two chronic conditions that continue to expand globally and drive progression toward end-stage kidney disease. CKD is often silent in early stages and is frequently diagnosed late, when patients are already closer to needing intensive intervention or kidney replacement therapy. Furthermore, the delayed diagnosis increases the probability of higher treatment intensity among patients, which strengthens recurring demand for chronic dialysis infrastructure, monitoring products, and replacement consumables. The growing prevalence is further supported by the improving survival of patients receiving long-term renal care, among others.

Moreover, dialysis is not a one-time intervention as it is a recurring and high-frequency therapy. As more patients remain on treatment for longer periods, the market benefits not only from new patient additions but also from sustained utilization of machines, disposables, vascular access products, and clinic capacity. Therefore, all the above-mentioned factors, along with rising research and development activities to launch technologically advanced dialysis systems, are anticipated to support the growing adoption rate of these devices in the market.

Improved Accessibility to Hemodialysis Centers to Drive Market Growth

The constantly growing number of patients requiring dialysis, especially in low and middle-income countries, has resulted in a high demand for efficient renal facilities with shorter waiting times. Different developed countries have an increasing number of nephrologists, which has, in turn, increased the number of renal care facilities. Moreover, to cater to the rising demand for renal care in emerging economies, investors are focusing more on increasing the network of renal treatment centers in countries, such as India, China, and Mexico. This is expected to increase the market’s revenue in the coming years. The delivery of affordable care in these countries is increasing the number of visits to these facilities.

- For instance, in May 2023, Life Healthcare announced that it had acquired the operations of renal dialysis clinics of Fresenius Medical Care in Southern Africa. Through this acquisition, the company gained operational rights to 51 renal dialysis clinics, thereby expanding its services in the region.

- Similarly, in July 2020, NIPRO CORPORATION acquired NIPRO RENAL CARE PRIVATE LIMITED, an Indian dialysis service provider. This strategic acquisition was made due to India's increasing population of 1.36 billion, with an estimated number of dialysis patients of 180,000 in 2019.

MARKET RESTRAINTS

Risks and Complications Associated with Procedures to Slow Down Market Growth

Even though the number of patients receiving this treatment is constantly increasing, there are a few factors that may restrain the market growth over the forecast period. One of them is the risks and complications associated with these procedures.

Several side effects and complications are associated with hemodialysis. Also, the creation of access for this therapy is a tedious process that requires accuracy and perfection. The complications associated with hemodialysis access may result in lower adoption. The imbalance of fluids and electrolytes in the body impacts the heart function and blood pressure, resulting in serious complications.

- For instance, according to a study published in BMC Nephrology in August 2020, risk factors for elderly hemodialysis patients include cardiovascular diseases, type of the access, therapy initiation time, and others. Presence of other chronic diseases in the body further increases the risk of mortality in hemodialysis patients.

Furthermore, according to the National Health Services (NHS), Peritonitis (bacterial infection), increased risk of developing a hernia, weight gain, and others are some of the side effects associated with peritoneal dialysis.

MARKET OPPORTUNITIES

Expansion of Healthcare Infrastructure is an Emerging Market Opportunity

Expansion of dialysis capacity across emerging markets represents a significant opportunity for the global market. Many low- and middle-income countries still face substantial under-penetration in dialysis infrastructure, despite a growing burden of chronic kidney disease and end-stage renal disease. There is an increasing demand for dialysis machines, dialyzers, blood tubing sets, concentrates, catheters, water-treatment systems, and other recurring consumables as governments, private providers, and public-private partnerships are expanding district-level dialysis services, setting up new treatment centers, and improving referral access. This opportunity is especially significant as market in many emerging countries are still constrained by capacity availability rather than by underlying disease need. The healthcare infrastructure is expanding, resulting in growing actual treatment volumes, creating a multiplier effect across center construction, equipment installation, and long-term consumables utilization.

This, along with installations of support systems including reverse osmosis water purification units, vascular access products, acute and chronic dialysis equipment, technical service support, and trained personnel, is contributing to demand across both capital equipment and high-frequency consumables, improving the long-term revenue visibility and driving the dialysis market growth.

- For instance, according to 2025 data published by the Government of India, there are about 1,704 operational dialysis centers in India.

The opportunity is also supported by the fact that several emerging economies are actively introducing or scaling national dialysis-access initiatives. These programs improve affordability and broaden treatment availability through district hospitals and partnership-based delivery models, thereby making dialysis access more geographically and financially feasible.

MARKET CHALLENGES

Poor Reimbursement and Management Policies for Dialysis Treatment in Emerging Countries to Restrict Market Growth

Poor reimbursement structures and weak management policies remain a major restraint in the market, especially across developing countries. Dialysis is a high-frequency, resource-intensive therapy that depends on sustained financing, stable procurement, trained personnel, and effective referral systems. When reimbursement is inadequate or irregular, the companies often face difficulty expanding capacity, maintaining infrastructure, and ensuring uninterrupted treatment delivery, which directly hampers market growth across equipment, consumables, and service segments. The dialysis demand does not translate into market expansion unless patients can consistently afford treatment or access publicly funded care. In many developing countries, kidney care remains heavily dependent on out-of-pocket spending, and reimbursement coverage for kidney replacement therapy is still limited. Moreover, this reduces treatment initiation, lowers adherence to recommended treatment frequency, and delays adoption of advanced dialysis technologies in cost-sensitive settings.

- For instance, according to 2023 data published by the International Society of Nephrology (ISN), in many countries where KRT is not publicly funded, the annual minimum wage is less than USD 2,000.0 while the annual cost of dialysis is more than USD 25,000.0.

Additionally, weak policy execution and fragmented care management are also limiting the adoption of dialysis procedures in the market. The inadequate planning around dialysis-unit distribution, referral pathways, workforce availability, and consumables supply can reduce treatment access among the patient population, resulting in a reduced number of patients receiving treatment, thereby weakening adoption for machines, dialyzers, tubing sets, concentrates, access products, and related support services. This, along with the increasing prevalence of kidney disease among economically vulnerable populations burdened by diabetes, hypertension, and other chronic conditions, is making long-term dialysis financially unsustainable for households. This not only restricts patient volumes but also affects provider economics, discouraging new center setup, technology upgrades, and private-sector participation in underpenetrated markets.

Dialysis Market Segmentation Analysis

By Type

Service Segment Gained Momentum Owing to Increasing Prevalence of Chronic Kidney Diseases

Based on type, the market is segmented into products and services. The product is further segmented into equipment and consumables. Moreover, equipment is further segmented into hemodialysis machines and peritoneal dialysis equipment, and consumables are further segmented into dialyzers, dialysate, cyclers, fluids, access products, and others.

To know how our report can help streamline your business, Speak to Analyst

The services segment accounted for the highest dialysis market share in 2025 due to the emergence of well-equipped renal care facilities for chronic and acute care across the globe and rising burden of kidney diseases. Due to these factors, the demand for chronic and acute-dialysis services has surged significantly.

- For instance, in August 2023, Innovative Renal Care opened a new state-of-art dialysis center, NCG Piedmont, at Covington to expand its dialysis service offering in the region.

- Moreover, according to the data published by the European Parliament in February 2022, around 100 million people in Europe were suffering from kidney diseases. Patients suffering from these ailments require dialysis to support their kidney health. The increasing prevalence of kidney diseases will increase awareness about the availability of dialysis services, thereby supporting the segment's growth.

Moreover, the products segment is expected to witness significant growth in the coming years owing to the rising number of local and regional market players to cater to the growing demand for advanced products and consumables. Additionally, the products segment is projected to grow at a CAGR of 6.7% during the forecast period.

By Dialysis Type

Hemodialysis to Gain Traction Owing to Higher Adoption of This Modality

By dialysis type, the global market is categorized into hemodialysis and peritoneal dialysis.

Hemodialysis segment generated the highest revenue in the market in 2025 and is expected to remain dominant in terms of revenue throughout the forecast period. Inadequate training provided for peritoneal treatment in developed as well as developing countries has reduced the preference for peritoneal dialysis. Moreover, the clinical benefits associated with hemodialysis, such as lesser time and adoption of Arteriovenous (AV) fistula are propelling the demand for this procedure. Additionally, the increasing incidence of severe CKD among the geriatric population is augmenting the number of patients requiring hemodialysis treatment.

- For instance, according to an article published in the Journal of Nephrology in September 2020, the incidence rate of stage IV CKD increases with age, hence the demand for hemodialysis treatment is growing.

The peritoneal dialysis segment is expected to witness strong growth over the forecast period. Increase in the preference for peritoneal dialysis over hemodialysis in developed countries is expected to drive the segment's growth during the forecast period. Additionally, demand for at-home peritoneal dialysis treatment is expected to increase in the coming years, thereby accelerating the segment’s growth. In addition, the peritoneal dialysis segment is projected to grow at a CAGR of 7.6% during the forecast period.

By End User

Dialysis Centers & Hospitals to Increase Product Use Owing to Rising Number of Patients Requiring Renal Care

Based on end-user, the market is segmented into dialysis centers & hospitals and home care.

The dialysis center & hospital segment accounted for the largest market share in 2025. This is due to factors, such as favorable reimbursements provided by renal facilities & hospitals for renal therapies, rising number of patients suffering from CKD & ESRD, and increasing healthcare expenditure by the population. The segment is also expected to dominate the market throughout the forecast period.

- For instance, in January 2023, six dialysis centers in the UAE’s Al Dhafra region upgraded their services by installing the latest medical equipment and hiring professionally trained medical staff. These factors will increase the number of patients served by the dialysis centers, further driving the segment’s growth.

Homecare is anticipated to be the fastest-growing segment during the forecast period, recording a considerable CAGR. The growth of this segment is attributed to the fact that homecare dialysis is a cost-effective therapy to treat End-Stage Kidney Disease (ESKD). Similarly, the launch of next-generation products for home dialysis will further augment the segment’s growth during the forecast period. In addition, the homecare segment is projected to grow at a CAGR of 9.3% during the forecast period.

Dialysis Market Regional Outlook

On the basis of region, the global market is divided into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Dialysis Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, at USD 39.66 billion, reached USD 41.68 billion in 2025. The region is projected to dominate the market during the forecast period as well. High prevalence of CKD and ESRD in the U.S. and Canada and a higher treatment rate in these countries are the key factors estimated to boost the expansion of the regional market during the forecast period.

- For instance, according to the 2023 statistics published by the U.S. Department of Health and Human Services (USDHHS), about 831,192 people are living with end-stage kidney disease in the U.S.

U.S. Dialysis Market

In 2026, the U.S. market is forecasted to represent USD 40.32 billion, capturing 37.0% of total global revenue.

Europe

Europe is expected to achieve a 5.1% growth rate in the coming years, the second-highest globally, reaching USD 28.21 billion by 2026. Europe is expected to emerge as the second-largest region in this market in terms of size, recording moderate growth in the long run. The region’s robust growth is due to the increasing percentage of the geriatric population suffering from renal disorders. Additionally, the number of patients receiving any form of dialysis therapy has increased over time throughout the region.

- According to data published by the NCBI in November 2022, an estimated 46,813 patients were on dialysis treatment in Italy. Both hemodialysis (HD) and Peritoneal Dialysis (PD) therapies provided by renal care units in public hospitals/structures are free of cost to Italian citizens.

U.K. Dialysis Market

The U.K. market is projected to reach USD 3.37 billion by 2026, accounting for 3.1% of the global market revenue.

Germany Dialysis Market

Germany's market is forecasted to reach about USD 5.06 billion by 2026, representing roughly 4.6% of global revenue.

Asia Pacific

In 2026, the Asia Pacific market is predicted to be valued at USD 24.89 billion, ranking as the third-largest globally. Asia Pacific is expected to witness relatively higher growth in the global market. Funding by public organizations to improve the accessibility of renal care is likely to augment the regional market’s expansion during the forecast period. Also, the increasing accessibility of dialysis services in various regions including remote areas of Asia Pacific countries will further propel the market growth.

- For instance, in March 2022, the Sathyalok free dialysis center was launched with the installation of 10 dialysis machines. The launch was funded by the Rotary Club of Chennai. This facility offered free dialysis to 18,000 people in 2022.

Japan Dialysis Market

Japan is projected to generate approximately USD 5.35 billion in revenue by 2026, contributing nearly 4.9% to the global market.

China Dialysis Market

China's market is forecasted to reach approximately USD 7.05 billion by 2026, contributing about 6.5% to global revenues.

India Dialysis Market

India is forecasted to contribute approximately USD 2.56 billion to the market by 2026, corresponding to about 2.4% of global revenues.

Latin America and Middle East & Africa

Furthermore, Latin America is expected to witness strong growth over the forecast period, with Latin America expected to reach around USD 6.45 billion by 2026. In Brazil, the rising incidence of CKD among the elderly population is boosting the adoption of dialysis products and services.

- For instance, the number of patients on dialysis in Brazil was 148,363 as per the Brazilian Dialysis Survey published in July 2021. This number was higher by 2.5% as compared to that in July 2020.

The Middle East & Africa is estimated to reflect significant growth during the forecast period due to the delayed diagnosis of chronic CKD and ESRD, and the growing presence of key players in this region to offer innovative products and services.

- For instance, in May 2023, Rockwell Medical, Inc. collaborated with Global Medical Supply Chain LLC for the distribution of Rockwell's hemodialysis concentrate products in the UAE.

Saudi Arabia Dialysis Market

By 2026, Saudi Arabia is expected to generate approximately USD 0.82 billion in the market, accounting for nearly 0.8% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Diligent Efforts by Leading Companies to Introduce Novel Products Strengthened Their Market Position

The market’s competitive landscape is semi-consolidated, with key players, such as Fresenius Medical Care, DaVita Inc., and Baxter capturing a significant share in 2025. These companies are adopting various strategies, such as focus on getting regulatory approvals and expansion of geographic presence through partnerships & collaborations to expand their customer base.

- For instance, in April 2023, Fresenius Medical Care AG & Co. KGaA expanded its collaboration with DocGo, Inc., with an aim to gain data insights from DocGo, Inc.’s chronic condition management solution.

- Additionally, in April 2022, Fresenius Medical Care North America received the U.S. FDA 510(k) clearance for its VersiPD Cycler System, which is a portable automated peritoneal dialysis system.

Apart from these players, other prominent companies, such as B. Braun SE, Medtronic, Asahi Kasei Medical Co., Ltd., and others are also undertaking various strategic initiatives, such as launch of new & innovative products and increasing R&D expenditure to strengthen their market presence.

- For instance, in June 2023, B. Braun SE partnered with Rockwell Medical for a three-year co-promotion of hemodialysis products to expand customer reach. This strengthened the reach of company’s products in the market.

LIST OF KEY DIALYSIS COMPANIES PROFILED

- B Braun SE (Germany)

- Fresenius Medical Care AG (Germany)

- Mozarc Medical Holding LLC. (U.S.)

- DaVita Inc. (U.S.)

- NIPRO (Japan)

- Asahi Kasei Medical Co., Ltd. (Japan)

- Diaverum (Sweden)

- Kimal (U.K.)

- BD (U.S.)

- Vantive (U.S.)

- WEIGAO GROUP (China)

- BAIN MEDICAL EQUIPMENT(GUANGZHOU) CO.,LTD (China)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Mozarc Medical partnered with DK Medical Technology (Suzhou) Co., Ltd. (DK Medtech) with an aim to strengthen PTA balloon technology in the U.S. AV access market.

- July 2025: Fresenius SE & Co. KGaA’s CRO Frenova announced a genomics collaboration with Nephronomics and GENEWIZ by Azenta Life Sciences to advance precision kidney disease care. This expanded the company’s market position.

- June 2025: Fresenius SE & Co. KGaA announced broader U.S. commercialization of the 5008X CAREsystem, with updated FDA clearance and the rollout of high-volume hemodiafiltration in the U.S. clinic network. This initiative improved the company’s reputation in the North America market.

- October 2023: Northeast Georgia Health Ventures (NGHV) and Dialyze Direct signed a strategic collaboration to provide home dialysis services to skilled nursing facilities (SNFs) in Georgia.

- August 2023: Fresenius Medical Care partnered with Sarah Bush Lincoln, a regional health system in Illinois, to provide dialysis services to rural patients. Through this partnership, an on-site dialysis program was launched.

REPORT COVERAGE

The market report offers qualitative and quantitative insights on the products and services offered and a detailed analysis of the market’s size & growth rate for all possible segments. Along with this, the report provides an elaborative analysis of the market’s dynamics, emerging trends, and competitive landscape. Key insights offered in the report include the prevalence of CKD & ESRD in key countries, recent industry developments, such as partnerships, mergers & acquisitions, new product launches, reimbursement policies, regulatory scenario, and key industry trends.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.7% from 2026-2034 |

| Unit | Value (USD billion) |

| Segmentation | By Type, Dialysis Type, End User, and Region |

| By Type |

|

| By Dialysis Type |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 103.15 billion in 2025 and is projected to reach USD 170.19 billion by 2034.

In 2025, the North America market value stood at USD 41.68 billion.

The market will exhibit steady growth at a CAGR of 5.7% during the forecast period of 2026-2034.

Currently, the services segment was leading the market by type.

Growing prevalence of chronic kidney diseases and government initiatives offering increased access to dialysis are the key drivers of the market.

Fresenius Medical Care, Baxter, and DaVita Inc. are the major players operating in the market.

North America dominated the market.

Surge in the demand for effective treatment of chronic kidney diseases and a large patient population base are expected to drive the adoption of these products.

- 2021-2034

- 2025

- 2021-2024

- 235

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us