Aluminum Foil Market Size, Share & Industry Analysis, By Application (Flexible Packaging & Laminates, Semi-rigid Containers, Pharma & Medical, Building & Industrial Insulation and Others), and Regional Forecast, 2026-2034

Aluminum Foil Market Overview

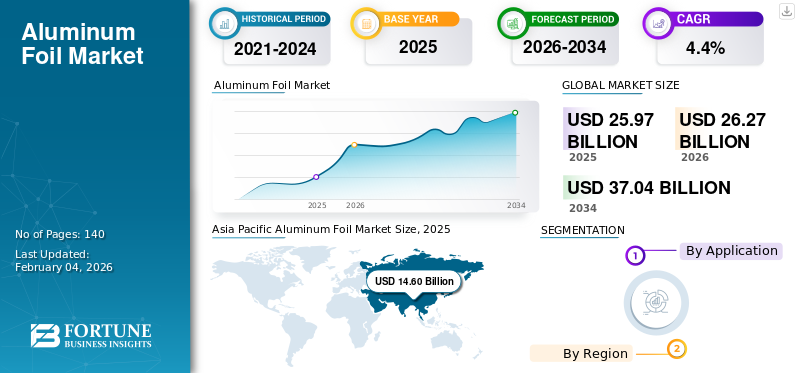

The global aluminum foil market size was valued at USD 25.97 billion in 2025. The market is projected to grow from USD 26.27 billion in 2026 to USD 37.04 billion by 2034, exhibiting a CAGR of 4.4% during the forecast period. Asia Pacific dominated the global aluminum foil market with a market share of 56.21% in 2025.

Aluminum foil pertains to rolled aluminum products with a thickness not exceeding 0.2 mm (excluding any backing). It is typically supplied in light-gauge converter foils for use in flexible packaging laminates, semi-rigid container foils, and technical foils designated for industrial, electrical, and energy applications. Aluminum foil is in demand due to its excellent barrier properties, including resistance to oxygen, moisture, and light, its formability, thermal conductivity, corrosion resistance (particularly when coated or laminated), and recyclability. The demand for aluminum foil is also driven by its applications in food and beverage packaging, household foil, pharmaceutical blister packs, insulation and HVAC facings, and a rapidly expanding energy sector, such as lithium-ion battery cathode current collectors.

Furthermore, the market is dominated by several major players, including Novelis, Hindalco, Assan Alüminyum, UACJ Foil, and Norsk Hydro, which are at the forefront. A broad portfolio, innovative product launches, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

ALUMINUM FOIL MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 25.97 billion

- 2026 Market Size: USD 26.27 billion

- 2034 Forecast Market Size: USD 37.04 billion

- CAGR: 4.40% from 2026–2034

- Asia Pacific dominated the global aluminum foil market with a market share of 56.21% in 2025.

- The flexible packaging & laminates segment is projected to expand at CAGR of 4.5% over the specified study period.

- The flexible packaging & laminates segment held the highest aluminum foil market share.

North America

The market in North America is projected to reach USD 3.40 billion in 2026.

Europe

European region is projected to grow at 3.4% and reach a valuation of USD 4.68 billion by 2026.

Asia Pacific

Asia Pacific held the dominant share in 2024, valued at USD 13.60 billion and also led in 2025, with USD 14.60 billion.

U.S.

Based on North America’s strong contribution the U.S. market can be analytically approximated at around USD 2.91 billion in 2026, accounting for roughly 11.1% of global sales.

Japan

The Japanese market in 2026 is estimated at around USD 1.25 billion, accounting for roughly 4.8% of global revenues.

Read More

ALUMINUM FOIL MARKET TRENDS

Recyclability-Driven Packaging Design and Rise of Higher-Performance Foils Are Emerging Market Trends

A significant trend is the movement toward packaging formats that can be collected, sorted, and recycled more efficiently, alongside increasing demand for barrier properties and shelf-life extension. In Europe, industry organizations emphasize aluminum's recyclability and have highlighted efforts to improve recycling performance, including small aluminum packaging formats. Meanwhile, regulatory authorities are enacting stricter packaging regulations through the EU Packaging and Packaging Waste Regulation (PPWR), adopted in late 2024 and set to come into force in August 2026. These developments are encouraging the redesign of lidding foils, coffee capsules, and composite structures to enhance recyclability and establish clearer end-of-life pathways.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Packaging Demand and Battery Electrification Increase Foil Consumption and Value Density

Packaging remains the primary end-use sector for aluminum foil, as it offers minimal oxygen and moisture permeability, along with lightweight properties and malleability, suitable for flexible laminates and semi-rigid containers. The growth in this sector is supported by proliferation of convenience food formats, extended distribution networks, and the increasing utilization of unit-dose packs in regulated products, where barrier performance and tamper evidence are essential.

Simultaneously, the electrification trend is driving higher demand for battery-grade cathode current-collector foil. The expansion of electric vehicles and stationary energy storage systems is necessitating greater volumes of thin-gauge, precisely tolerance foil with stringent surface-quality standards. Consequently, this elevates the value per ton compared to traditional commodity packaging grades. These factors collectively contribute to the aluminum foil market growth.

MARKET RESTRAINTS

Metal Price Volatility and High-Spec Yield Losses Restrains Market Growth

Foil pricing is anchored to aluminum metal benchmarks and regional delivery premiums. Rapid movements in metal prices and premiums can exert pressure on converter margins, complicate contract pass-through mechanisms, and introduce procurement volatility for brand owners and packagers. Furthermore, thin-gauge, high-performance foils, including blister and battery grades, require rigorous process control and specialized finishing capabilities. Yield losses, scrap generation, and bottlenecks in polishing and finishing processes can also increase costs and prolong lead times, particularly for products with stringent defect specifications and wide-format requirements.

MARKET OPPORTUNITIES

Circularity Policies and Recyclability-Driven Redesign Create Market Growth Opportunities

Packaging regulations and voluntary commitments are accelerating the redesign toward recyclable structures, higher recycled content and improved collection outcomes. This supports the demand for foil-based solutions where aluminum can facilitate mono-material concepts, enhance barrier performance at low gauges, and ensure robust recycling economics when properly collected.

Concurrently, the regionalization of supply chains for batteries and strategic applications is expanding investments outside China. New rolling and finishing lines dedicated to premium foil can increase local availability, shorten supply chains and support higher-value product mixes in Europe, North America and India.

MARKET CHALLENGES

Trade Remedies, Policy Shifts and Collection Constraints Can Create Flow Disruptions and Uncertainty

Trade actions and policy changes can swiftly redirect flows of goods, impacting availability and pricing across regions. Measures such as anti-dumping or countervailing duties, tariff modifications and sanctions may introduce volatility for markets reliant on imports and increase the qualification burdens when supply sources are altered.

Although aluminum is highly recyclable, challenges in collecting and sorting small-gauge and small-format items persist as practical obstacles. Without advancements in collection efficiency, sorting technology and consumer behavior, certain foil formats may encounter policy pressures or substitution risks within specific packaging industries.

Segmentation Analysis

By Application

To know how our report can help streamline your business, Speak to Analyst

Flexible Packaging & Laminates Segment Dominates due to its Higher Barrier Performance and Light-Weight

In terms of application, the market is categorized into flexible packaging & laminates, semi-rigid containers, pharma & medical, building & industrial insulation and others.

The flexible packaging & laminates segment held the highest aluminum foil market share. The segment accounts for the majority of foil consumption through flexible packaging laminates (food, beverage, tobacco and pet food) and semi-rigid containers (trays, lids, dairy and ready to eat meals packs). Foil is selected for its barrier performance, heat resistance, light-weighting and shelf-life extension, supported by convenience formats and premiumization in food and pharma-adjacent packaging. Additionally, this segment is projected to expand at CAGR of 4.5% over the specified study period.

The building & industrial insulation segment is experiencing significant growth. Foil is utilized for insulation facings, HVAC duct wrap, radiant barriers and harsh-environment shielding, where reflectivity, corrosion resistance and temperature tolerance are highly valued. Industrial applications also encompass heat exchangers, cable wraps and specialty laminates, with demand driven by building efficiency enhancements, industrial maintenance cycles and infrastructure investments.

Aluminum Foil Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America and Middle East & Africa.

Asia Pacific

Asia Pacific Aluminum Foil Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2024, valued at USD 13.60 billion and also led in 2025, with USD 14.60 billion. Asia Pacific remains the leading region in both production and consumption, driven by China’s extensive foil-rolling capacity and the concentration of supply chains in the packaging and electronics sectors. The demand in the Asia Pacific region is underpinned by substantial volumes in the food and beverage and electronics industries, as well as by the growing capacity of the battery manufacturing sector.

China Aluminum Foil Market

In 2026, the China market is estimated to reach USD 9.15 billion. China’s mass-market packaged food sector and the fast-growing “convenience” formats drive demand for converter foil (such as laminates, sachets, and wraps) and container foil (including trays and lids). Manufacturers such as Mingtai sea food, cigarettes and packaging act as key downstream sectors due to their foil products, highlighting the broad range of packaging usage.

To know how our report can help streamline your business, Speak to Analyst

Japan Aluminum Foil Market

The Japanese market in 2026 is estimated at around USD 1.25 billion, accounting for roughly 4.8% of global revenues.

India Aluminum Foil Market

The Indian market in 2026 is estimated at around USD 1.42 billion, accounting for roughly 5.4% of global revenues.

Europe

Europe is expected to experience substantial market growth in the coming years. Over the forecast period, the European region is projected to grow at 3.4% and reach a valuation of USD 4.68 billion by 2026. The foil industry in Europe demonstrated signs of recovery in 2024, with EAFA reporting total deliveries of 892,500 tons, a 7.3% year-on-year increase. Policy plays a significant role, as the EU PPWR (Regulation (EU) 2025/40), adopted in December 2024, is set to enter into force in August 2026 and will promote packaging redesign, recycled-content pathways and enhanced recycling outcomes.

U.K. Aluminum Foil Market

The U.K. market in 2026 is estimated at around USD 0.71 billion, accounting for roughly 2.7% of global revenues.

Germany Aluminum Foil Market

Germany’s market in 2026 is estimated at around USD 0.99 billion, accounting for roughly 3.8% of global revenues.

North America

The market in North America is projected to reach USD 3.40 billion in 2026. North America is a substantial market for foil and foil containers, primarily driven by sectors such as food service, retail packaging, and industrial applications. Recent trade measures enacted by the U.S. targeting specific downstream aluminum container products from China reflect increased regulatory scrutiny and could influence regional pricing and sourcing strategies.

U.S. Aluminum Foil Market

Based on North America’s strong contribution the U.S. market can be analytically approximated at around USD 2.91 billion in 2026, accounting for roughly 11.1% of global sales.

Latin America and Middle East & Africa

Over the forecast period, it is anticipated that the Latin America and Middle East & Africa regions will experience moderate growth within this market. The Latin America market is projected to reach USD 1.57 billion by 2026. Although Latin America and Middle East & Africa are relatively smaller markets, their growth is driven by increasing penetration of packaged foods and rising investments in the industrial and energy sectors. In the Middle East & Africa region, growing demand supported by packaging and infrastructure, is further reinforced by harsh environmental conditions, where insulation/HVAC facings and industrial foils are pertinent.

GCC Aluminum Foil Market

The GCC market in 2026 is estimated at USD 0.82 billion, accounting for approximately 3.1% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Rolling Capacity, Expertise in Thin-Gauge Materials, and Strategic Downstream Converting Partnerships Leads to Key Players Dominance

The market is characterized by intense competition and regional fragmentation, with major integrated rollers supplying foilstock and foil, complemented by specialized foil and packaging converters. Key differentiators encompass scale and cost efficiency in rolling processes, expertise in thin-gauge production and defect management, capacity for finishing and coating, qualification and traceability systems designed for pharmaceutical and battery applications, and offerings of recycled-content and low-carbon aluminum supported by recycling investments. Novelis, Hindalco, Assan Alüminyum, UACJ Foil, and Norsk Hydro are few key players in the market.

LIST OF KEY ALUMINUM FOIL COMPANIES PROFILED

- Novelis (U.S.)

- Assan Aluminium Industry and Trade Inc. (Turkey)

- Norsk Hydro ASA (U.S.)

- Hindalco Industries Ltd. (India)

- UACj Corporation (Japan)

- LOTTE Aluminium (South Korea)

- Reynolds Consumer Products (U.S.)

- Henan Mingtai Al. Industrial Co., Ltd. (China)

- Jiangsu Dingsheng New Energy Materials Co., Ltd. (China)

- Constellium (France)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Constellium inaugurates a new finishing line at the Singen plant. This milestone completes a USD 35 billion investment in partnership with Lotte Infracell to produce high-quality aluminium foil stock for battery applications in Europe. The new lines improve capacity to supply foil used in EV battery markets and other high-performance segments, featuring advanced edge trimming and packing capabilities, as well as sustainability enhancements such as onsite solar power.

- April 2025: Novelis opened a new Ulsan Aluminum Recycling Center in South Korea with an annual capacity of 100,000 tons of low-carbon aluminum, enhancing recycled aluminum feedstock. While the facility primarily targets beverage, automotive, and specialty products, increased availability of recycled aluminum supports Novelis’s ability to supply high-recycled-content thin foil and sheet products globally.

- July 2024: Novelis announced an investment to expand Used Beverage Can (UBC) recycling capacity at Latchford (U.K.), adding 85 kt/year of UBC recycling capacity, supporting higher recycled content in rolled products.

REPORT COVERAGE

The global aluminum foil market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, with market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.4% from 2026-2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Application and Region |

|

By Application |

· Flexible Packaging & Laminates · Semi-rigid Containers · Pharma & Medical · Building & Industrial Insulation · Others |

|

By Geography |

· North America (By Application and Country) o U.S. (By Application) o Canada (By Application) · Europe (By Application, and Country/Sub-region) o Germany (By Application) o U.K. (By Application) o France (By Application) o Italy (By Application) o Rest of Europe (By Application) · Asia Pacific (By Application, and Country/Sub-region) o China (By Application) o Japan (By Application) o India (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Application, and Country/Sub-region) o Brazil (By Application) o Mexico (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Application, and Country/Sub-region) o GCC (By Application) o South Africa (By Application) o Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 25.97 billion in 2025 and is projected to reach USD 37.04 billion by 2034.

The market is projected to grow at a CAGR of 4.4% during the forecast period of 2026-2034.

The flexible packaging & laminates application segment led in 2025.

Asia Pacific held the highest market share in 2025.

Food and pharma packaging demand, shelf-life requirements, and convenience formats are accelerating the adoption of aluminum foil.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us