AI in Medical Billing Market Size, Share & Industry Analysis, By Component (Software and Services), By Deployment (Cloud-Based, On-Premise, and Hybrid), By Technology (LLMs & Natural Language Processing, Machine Learning & Deep Learning, and Others), By Product Type (Claims Automation Tools, Denial Management Tools, Eligibility & Prior Authorization Tools, and Others), By Application (Claims Submission, Denial Prediction & Appeals, Prior Authorization Support, and Others), By End User (Hospitals & Health Systems, Physician Groups/Clinics, and Others), and Regional Forecast, 2026-2034

AI in Medical Billing Market Size and Future Outlook

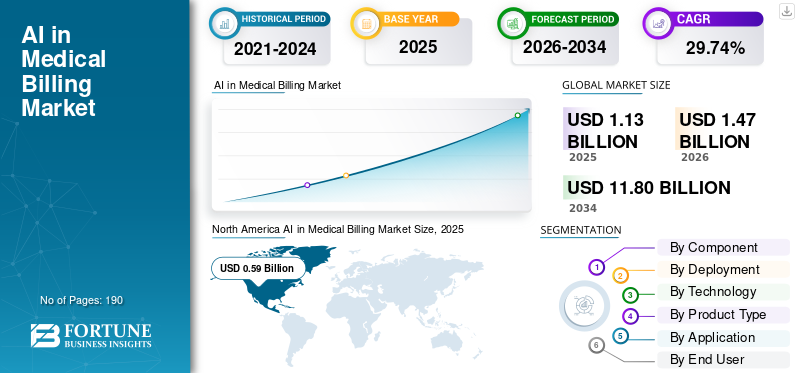

The global AI in medical billing market size was valued at USD 1.13 billion in 2025. The market is projected to grow from USD 1.47 billion in 2026 to USD 11.80 billion by 2034, exhibiting a CAGR of 29.74% during the forecast period. North America dominated the AI in medical billing market with a market share of 52.21% in 2025.

The global AI in medical billing solutions comprises of AI-enabled revenue cycle platforms, automated medical coding tools, claim management systems, denial prediction solutions, and billing workflow automation software. The demand for these solutions is elevating as healthcare providers face rising claim volumes, payer-specific documentation rules, and pressure to reduce revenue leakage. As a result, AI is being used by hospitals, physician groups, billing companies, and healthcare payers to automate repetitive billing tasks, improve coding accuracy, identify missing information before claim submission, reduce denials, and speed up reimbursement. Key companies are collaborating to deliver faster, more accurate, and lower-cost billing operations.

- For instance, in April 2025, AKASA Inc. collaborated with the Cleveland Clinic to deploy generative AI tools for revenue cycle operations. The partnership focused on improving medical coding and documentation accuracy during the mid-revenue cycle, where clinical records are reviewed and translated into billing codes.

Furthermore, major players, such as Waystar, Optum Inc., R1, and AKASA Inc., are streamlining their resources toward technological advancement, investment initiatives, and new product launches to strengthen their market presence.

Download Free sample to learn more about this report.

AI in Medical Billing Market Key Takeaways

- 2025 Market Size: USD 1.13 billion

- 2026 Market Size: USD 1.47 billion

- 2034 Forecast Market Size: USD 11.80 billion

- CAGR: 29.74% from 2026–2034

- North America dominated the market with a 52.21% share in 2025.

- Software segment held the largest market share in 2025.

- Cloud-based segment held the largest market share in 2025.

North America

The market reached USD 0.59 billion in 2025, driven by healthcare IT adoption and AI-enabled billing.

Asia Pacific

The market is projected to reach USD 0.31 billion by 2026, driven by healthcare digitization and rising insurance penetration.

Europe

The market is projected to reach USD 0.31 billion by 2026, supported by revenue cycle modernization and AI adoption.

U.S.

The market is projected to reach USD 0.69 billion by 2026, driven by AI-powered medical billing solutions.

Japan

The market is projected to reach USD 0.08 billion by 2026, supported by healthcare digitalization and AI adoption.

Read More

AI IN MEDICAL BILLING MARKET TRENDS

Growing Adoption of AI-Powered Medical Coding Automation is an Emerging Trend Observed

The global market trend observed is shift toward the increased adoption of AI-powered medical coding automation. As healthcare providers are consistently under pressure to process claims faster, reduce coding errors, and improve reimbursement accuracy, these automation tools have gained traction over recent years. Medical coding is time-consuming, as coders must review large volumes of clinical notes, discharge summaries, lab reports, and payer-specific documentation before claims can be submitted. As patient volumes rise and coding rules become more complex, manual coding increases the risk of claim delays, denials, and revenue leakage. This is encouraging hospitals and health systems to adopt AI-based coding platforms, significantly improving billing speed and staff productivity.

- For instance, in June 2025, CodaMetrix launched its first contextual coding automation platform and a new Emergency Department (ED) solution, while expanding its executive leadership team with deep healthcare and AI expertise.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Pressure to Lower Administrative Costs in Healthcare Billing is Driving Market Growth

A key factor driving the global market is the rising need to reduce administrative costs across healthcare billing and revenue cycle operations. Hospitals and physician groups spend significant time and resources on manual coding review, claim checks, prior authorization, payer follow-ups, denial handling, and payment reconciliation. As billing rules become more complex and staffing pressure increases, these manual workflows raise operating costs and slow down reimbursement. These factors are driving global market demand that automates repetitive tasks, identify errors before claim submission, reduce rework, and support faster payment cycles. Key companies are also directing their resources toward new product launches to meet this increasing demand.

- For instance, in April 2025, Waystar launched new generative AI and advanced automation capabilities across its healthcare payment software platform. These generative AI capabilities and advanced automation aim to eliminate more than USD 440.0 billion in administrative waste across the U.S. healthcare system. Such AI-enabled automation reduces manual billing effort, improves revenue cycle efficiency, and helps providers’ lower administrative costs.

MARKET RESTRAINTS

Data Privacy and Compliance Concerns in AI-Based Billing Workflows Hampers Market Growth

Data privacy and compliance concerns are among the prominent factors restraining the global AI in medical billing market growth. Billing platforms must process highly sensitive patient, insurance, clinical, and claims information. Since AI tools often need large datasets to automate coding, claim review, denial prediction, and revenue cycle decisions, healthcare providers remain cautious about how patient data is collected, stored, shared, and monitored. Any weakness in HIPAA compliance, cybersecurity controls, vendor governance, or auditability can expose providers to regulatory risk, reputational damage, and financial penalties. As a result, hospitals and billing companies may delay full-scale adoption of AI billing tools.

- For instance, in January 2026, Experian Health published an article titled ‘AI in healthcare RCM: 2026 opportunities and insights’ stating that while nearly two-thirds of healthcare providers are using AI in billing processes, providers remain cautious about using AI for critical decision-making. The article specifically highlighted data privacy, data security, accuracy, and cost as the biggest barriers to AI adoption.

MARKET OPPORTUNITIES

Opportunity to Address Medical Coder Shortages Through Automation to Offer Growth

The global market offers significant growth opportunities to address the shortage of skilled medical coders through automation. Medical coding requires trained professionals to review clinical notes, match services with accurate codes, check documentation gaps, and ensure payer compliance before claims are submitted. As patient volumes increase and coding rules become more complex, the available coding workforce often struggles to keep pace. AI-powered coding tools can help address this gap by reading clinical documentation, suggesting accurate codes, prioritizing complex cases for human review, and automating routine coding tasks. As a result, healthcare providers can improve productivity without depending only on expanding manual coding teams, creating a clear opportunity for AI vendors offering autonomous coding and revenue cycle automation solutions.

- For instance, in January 2026, R1 RCM launched Phare Audit, an AI-native solution for coding and clinical documentation integrity designed to capture full reimbursement, reduce revenue leakage, and improve quality. The solution used agentic AI to enhance pre-bill auditability and reimbursement optimization, directly supporting the market opportunity by enabling providers to reduce manual coding review, identify billing gaps before claim submission, and improve reimbursement accuracy.

MARKET CHALLENGES

Ensuring Accuracy and Compliance Across Changing Payer Rules Remains a Prominent Challenge

Ensuring accuracy and compliance with changing payer rules is a major challenge for AI in the medical billing market, as billing decisions depend on correct coding, complete documentation, payer-specific policies, and frequent regulatory updates. Even when AI tools can automate coding and claims review, providers still need to verify that the recommended codes match clinical documentation and comply with payer rules. If the AI system misses a modifier, applies an outdated rule, or misinterprets documentation, it can result in claim denials, underpayments, overpayments, audits, or compliance penalties. These factors create challenges among hospitals and billing companies, as they may not fully rely on automated billing decisions without human review, transparent audit trails, and continuous model updates. As a result, maintaining coding accuracy and compliance across complex reimbursement environments remains a key challenge for wider market adoption.

- For instance, the 2025 MDaudit Benchmark Report highlighted that healthcare providers are facing rising denials, payer audits, and outpatient coding challenges. The report noted that coding accuracy and continuous risk monitoring are becoming more important as billing errors can directly affect reimbursement, compliance, and audit exposure.

Segmentation Analysis

By Component

Ease of Integration for Software with EHR to Drive Segmental Growth

Based on component, the market is categorized into software and services.

By component, software dominated the market. The segment dominated the value in AI for medical billing, with value delivered primarily through coding engines, claim scrubbers, denial management platforms, eligibility tools, and revenue cycle automation systems. Healthcare organizations prefer software-led solutions as they can be integrated with EHRs, billing systems, and practice management platforms without requiring major physical infrastructure. As billing teams face rising claim volumes and increasingly complex payer rules, software helps automate repetitive tasks, improve coding accuracy, and speed up reimbursements. Highlighting these key features, major companies’ operations in the market are focusing on new product launches.

- For instance, in October 2025, athenahealth launched AI-native athenaOne practice and revenue cycle management capabilities designed to reduce administrative work by more than 50%, including automated insurance selection and AI agents for prior authorization and claims processing. Such development involves vendors embedding AI directly into RCM software platforms used by practices and health systems.

The services segment is expected to grow at a CAGR of 25.28% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Faster Implementation and Scalability Offered by Cloud-based Segment Led to its Dominance

Based on deployment, the market is segmented into cloud-based, on-premise, and hybrid.

In 2025, cloud-based deployment dominated the AI in medical billing market share. The high share is allocated to the segment as AI medical billing tools require scalable computing power, frequent model updates, secure data exchange, and easy integration across multiple provider locations. Cloud deployment enables hospitals and billing teams to access AI coding, claims, and denial management tools without a heavy on-premises infrastructure investment. As healthcare organizations increasingly prefer flexible and subscription-based digital platforms, cloud-based AI billing solutions are becoming the preferred deployment model. Innovative product launches and strategic collaborations by key companies further strengthen dominance.

- For instance, in November 2025, PwC collaborated with Amazon Web Services (AWS) to transform healthcare revenue cycle management using AI, cloud, and automation. The partnership focused on improving financial performance and patient outcomes through cloud-enabled revenue cycle modernization, supporting the dominance of cloud-based deployment in AI medical billing.

The hybrid segment is projected to grow at a 28.08% CAGR during the forecast period.

By Technology

Heavy Reliance on Reading and Interpreting Led to Dominance of LLMs & Natural Language Processing Segment

Based on technology, the market is segmented into LLMs & natural language processing, machine learning & deep learning, rules/RPA-based automation, and others.

In 2025, LLMs & natural language processing segment dominated the market as medical billing depends heavily on reading and interpreting clinical documentation, physician notes, discharge summaries, lab reports, and payer requirements. These technologies help convert unstructured clinical text into billing-ready insights, support code selection, identify missing documentation, and improve claim accuracy. As billing errors often begin with incomplete or misread documentation, NLP and LLM-based tools are being launched and increasingly adopted to bridge the gap between clinical records and revenue cycle workflows.

- For instance, in May 2025, Optum launched Optum Integrity One, an integrated revenue cycle platform powered by Optum Clinical Language Intelligence to reduce administrative burden for health systems.

The machine learning & deep learning segment is projected to grow at a CAGR of 28.53% during the forecast period.

By Product Type

Increasing Efficiency in Time Management Due to Claims Automation Tools Facilitates Segmental Growth

Based on product type, the market is segmented into claims automation tools, denial management tools, eligibility & prior authorization tools, payment posting & reconciliation tools, patient billing & collections tools, and others.

Based on product type, claims automation tools segment held a dominant market share as it is one of the most time-consuming and error-prone areas of medical billing. Providers must verify coverage, check coding accuracy, apply payer rules, submit claims, follow up on rejections, and manage denials, which creates a heavy administrative workload. AI-based claims automation helps detect claim errors before submission, reduce manual review, improve first-pass claim acceptance, and accelerate payment cycles. As providers continue to face pressure from rising denials and delayed reimbursements, automated claims solutions are becoming a core product category in AI medical billing platforms.

- For instance, in May 2025, Smarter Technologies launched an AI-powered revenue management automation and insights platform that helps hospitals and health systems optimize administrative workflows and strengthen financial performance.

The denial management tools segment is projected to grow at a CAGR of 32.38% during the forecast period.

By Application

Widespread Utilization of AI in Claims Submission Led to Dominance of Segment

Based on application, the market is segmented into claims submission, denial prediction & appeals, prior authorization support, payment integrity & underpayment detection, patient billing automation, and others.

In 2025, claims submission segment dominated the market as it is the central step where billing accuracy directly affects provider reimbursement. If claims are submitted with coding errors, missing documentation, incorrect eligibility details, or payer rule mismatches, providers face rejections, denials, delayed payments, and revenue leakage. AI tools are therefore widely used before and during claim submission to validate codes, identify documentation gaps, check payer-specific rules, and improve clean-claim rates. Since every healthcare provider depends on timely, accurate claim submission for cash flow, this application has the highest adoption across AI medical billing workflows.

- For instance, in September 2025, Oracle Health announced plans to launch a comprehensive suite of AI-powered applications to increase automation in prior authorizations, reduce claims denials, and enhance care coordination between payers and providers. These applications and AI agents aim to significantly reduce administrative costs and improve value-based care initiatives to maximize care quality while optimizing resource allocation.

The prior authorization support segment is projected to grow at a CAGR of 31.72% over the projected period.

By End User

Strategic Collaboration with Hospitals to Expand Access Led to Dominance of Hospital & Health Systems Segment

Based on end user, the market is segmented into hospitals & health systems, physician groups/clinics, RCM vendors & BPOs, payers, and others.

By end user, hospitals & health systems segment dominated the market. They generate large volumes of complex claims and manage multiple payers, high-value claims, and significant denial risk, making billing automation a financial priority. AI medical billing solutions help hospitals improve charge capture, coding accuracy, claims throughput, denial prevention, and cash collections at scale. Since hospitals have larger IT budgets, greater billing complexity, and stronger incentives to reduce revenue leakage, they are the leading end users of AI-enabled medical billing platforms.

- For instance, in November 2025, Conifer Health Solutions collaborated with Google Cloud to embed advanced AI across its end-to-end RCM platform, aiming to strengthen financial performance, improve cash collections, and elevate the patient experience for healthcare organizations.

The physician groups/clinics segment is projected to grow at a CAGR of 31.60% over the forecast period.

AI in Medical Billing Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America AI in Medical Billing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 0.47 billion and also maintained its leading position in 2025 at USD 0.59 billion. The market is growing in North America due to high healthcare IT adoption, complex reimbursement systems, and strong pressure to reduce claim denials. Hospitals and physician groups are adopting AI billing tools to improve coding accuracy, automate claims workflows, and reduce administrative costs.

U.S. AI in Medical Billing Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 0.69 billion in 2026, accounting for roughly 47.20% of the global market.

Europe

Europe is projected to grow at 29.03% over the coming years, the second-highest among all regions, and reach a valuation of USD 0.31 billion by 2026. Europe is witnessing growth as healthcare providers modernize revenue cycle processes and improve digital health infrastructure. The rising focus on billing transparency, compliance, and operational efficiency is driving demand for AI-enabled claims and coding automation.

U.K. AI in Medical Billing Market

The U.K. market is estimated to be valued at around USD 0.05 billion in 2026, representing roughly 3.43% of the global market.

Germany AI in Medical Billing Market

Germany's market is projected to reach approximately USD 0.06 billion in 2026, equivalent to around 4.13% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 0.31 billion in 2026 and secure the position of the third-largest region in the market. Asia Pacific is growing due to rapid healthcare digitization, expanding private hospital networks, and increasing insurance penetration. As patient volumes rise, providers are using AI billing solutions to manage claims faster and reduce manual administrative workload.

Japan AI in Medical Billing Market

The Japanese market is estimated at around USD 0.08 billion in 2026, accounting for approximately 5.69% of the global market.

China AI in Medical Billing Market

China's market is projected to be among the largest globally, with 2026 revenues estimated at around USD 0.10 billion, accounting for approximately 6.51% of global sales.

India AI in Medical Billing Market

The Indian market is estimated at around USD 0.04 billion in 2026, accounting for roughly 3.05% of global revenue.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness a steady growth in this market during the forecast period. The market in Latin America is estimated to reach a valuation of USD 0.08 billion in 2026. The region is witnessing growth as hospitals and payers adopt digital billing systems to improve reimbursement efficiency. The need to reduce billing errors, accelerate payment cycles, and support expanding healthcare coverage is driving AI adoption.

GCC AI in Medical Billing Market

The GCC market is set to reach USD 0.01 billion in 2026.

South Africa AI in Medical Billing Market

The South African market is projected to reach approximately USD 0.01 billion by 2026, accounting for roughly 0.37% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Increasing Focus of RCM Vendors Toward AI-Enabled Billing Automation to Improve Revenue Cycle to Propel Market Progress

The global AI in medical billing market is moderately fragmented, with companies such as Waystar, Optum, Oracle Health, R1 RCM, athenahealth, and Experian Health, operating across the market. These companies hold strong positions due to their established revenue cycle platforms, AI-powered coding tools, claims automation capabilities, and denial management solutions, among others. Ongoing product launches, partnerships, acquisitions, and AI platform upgrades are further helping these companies strengthen their market presence and expand their role in automating healthcare billing workflows.

- For instance, in April 2025, Waystar launched new generative AI and advanced automation capabilities across its healthcare payment software platform to reduce administrative waste and improve revenue cycle performance. The development supports the market growth as leading vendors are embedding AI into claims, denials, payments, and billing workflows to improve efficiency and reduce manual effort.

Other notable participants in the global market include AKASA, CodaMetrix, Fathom, Nym, Infinx, Veradigm, TruBridge, and ModMed. These companies are expected to focus on autonomous medical coding, generative AI-based revenue cycle tools, improved claim accuracy, denial prevention, and specialty-specific billing automation during the forecast period. The rest of the market remains fragmented among emerging AI billing start-ups, regional RCM service providers, healthcare IT vendors, and niche automation companies serving hospitals, physician groups, and billing organizations.

LIST OF KEY AI IN MEDICAL BILLING COMPANIES PROFILED IN REPORT

- Waystar (U.S.)

- Optum Inc. (U.S.)

- R1 (U.S.)

- AKASA Inc. (U.S.)

- CodaMetrix (U.S.)

- Oracle (U.S.)

- Athenahealth (U.S.)

- Experian Health (Ireland)

- Fathom (U.S.)

- Infinx Healthcare (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Cedar expanded its Cedar Intelligence, its AI-powered decision engine, with new capabilities embedded across its product suite. The release is designed to help providers personalize billing journeys at scale, improve collections, reduce cost-to-collect, and make it easier for patients to resolve medical bills.

- January 2026: Veradigm launched a new AI-enabled application for Veradigm Revenue Cycle Services (RCS) clients, designed to deliver faster, deeper revenue cycle insights and strengthen the value of ongoing performance reviews for independent practices.

- January 2026: R1 launched Phare Audit, an AI-native solution for both coding and clinical documentation integrity. The solution was designed to transform mid-revenue-cycle performance by improving accuracy and quality before a bill is generated, so providers capture full reimbursement for the care delivered, with evidence-based recommendations and complete auditability.

- October 2025: Tebra launched AI Review Replies and AI Review Insights, two artificial intelligence features integrated natively into its EHR+ Patient Experience package.

- June 2025: Amperos Health launched Amanda, an AI biller specifically designed for healthcare providers to reduce denials and recover outstanding claims, supporting revenue cycle management (RCM) teams.

REPORT COVERAGE

The report provides a comprehensive global AI in medical billing market analysis. It covers detailed market assessment across component, deployment, technology, product type, application, and end user, while examining the role of AI-enabled billing tools in claims automation, denial management, eligibility verification, payment posting, patient billing, and revenue cycle optimization. The study also evaluates major market drivers, restraints, challenges, and growth opportunities influencing adoption across healthcare providers, physician groups, RCM vendors, and payers. It highlights how rising claim denials, administrative cost pressure, payer complexity, coder shortages, data privacy concerns, and integration challenges are shaping market growth. The report further provides regional insights across key geographies, a competitive landscape analysis, company profiling, and recent developments, including product launches, partnerships, collaborations, and strategic initiatives. Overall, it assesses the major factors driving, restraining, and creating future opportunities in the market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 29.74% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Technology, Product Type, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Technology |

|

| By Product Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.13 billion in 2025 and is projected to reach USD 11.80 billion by 2034.

In 2025, North Americas market value stood at USD 0.59 billion.

The market is expected to grow at a CAGR of 29.74% over the forecast period of 2026-2034.

The software segment is expected to lead the market.

Growing pressure to lower administrative costs in healthcare billing is driving market growth.

Waystar, Optum Inc., R1, and AKASA Inc. are the top players in the global market.

North America held the largest share of the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us