AI in Power Utilities Market Size, Share & Industry Analysis, By Technology (Machine Learning, Optimization Algorithms, Deep Learning, NLP & Conversational AI, and Others), By Deployment (Cloud and On-Premise), By Application (Grid Optimization & Smart Grid, Energy Trading Optimization, Customer Analytics & Demand Response, Predictive Maintenance, Forecasting, and Others), and Regional Forecast, 2026-2034

AI in Power Utilities Market Size and Future Outlook

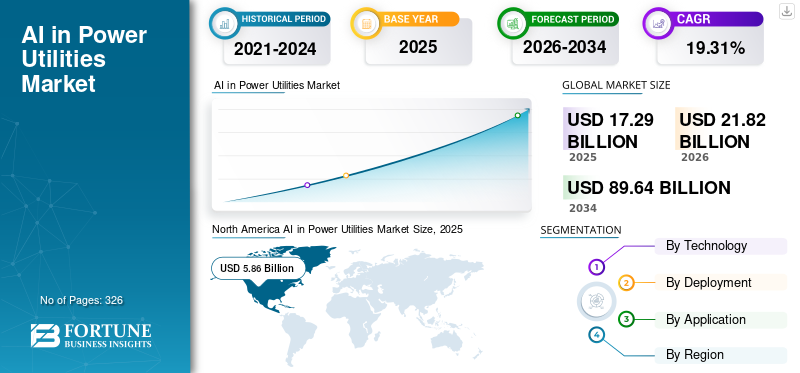

The global AI in Power Utilities market size was valued at USD 17.29 billion in 2025. The market is projected to grow from USD 21.82 billion in 2026 to USD 89.64 billion by 2034, exhibiting a CAGR of 19.31% during the forecast period. North America dominated the AI in power utilities market with a market share of 33.89% in 2025.

AI in Power Utilities refers to the application of artificial intelligence technologies to optimize the power generation, transmission, distribution, and energy consumption. It enables utilities to analyze large volumes of operational and customer data to improve grid reliability, forecast demand and renewable output, and enhance asset performance. AI-driven solutions support predictive maintenance, real-time grid management, energy trading optimization, and customer engagement. Overall, it helps utilities increase efficiency, reduce costs, and manage the growing complexity of modern, decentralized energy systems.

The growth of AI in power utilities is driven by the increasing integration of renewable energy sources, which requires advanced forecasting and grid optimization capabilities. Rising electricity demand, coupled with aging infrastructure, is pushing utilities to adopt predictive maintenance and efficiency-enhancing solutions. Additionally, the expansion of smart grids, smart meters, and distributed energy resources is generating large volumes of data, accelerating AI adoption. Regulatory pressures for grid reliability, decarbonization, and improving energy efficiency further support market growth, along with the need to enhance customer engagement and demand-side management.

Siemens AG, General Electric (GE Vernova), Schneider Electric, ABB Ltd., and IBM are among the leading players in the AI in power utilities market. These companies are actively developing and deploying AI-driven solutions for grid optimization, predictive maintenance, and energy management. They are investing in digital platforms, such as digital twins and advanced analytics, to enhance grid reliability and operational efficiency. Additionally, they collaborate with utilities and governments to modernize infrastructure, integrate renewable energy, and support smart grid initiatives. Overall, their efforts focus on improving efficiency, reducing downtime, and enabling a more resilient and sustainable power system.

Download Free sample to learn more about this report.

AI in Power Utilities Market Key Takeaways

- 2025 Market Size: USD 17.29 billion

- 2026 Market Size: USD 21.82 billion

- 2034 Forecast Market Size: USD 89.64 billion

- CAGR: 19.31% from 2026–2034

- North America dominated the AI in power utilities market with a 33.89% share in 2025.

- Machine learning held the largest technology segment share with 37.27% in 2025.

- On-premise deployment accounted for the leading share with 60.36% in 2025.

North America

North America led the market with USD 5.86 billion in revenue and approximately 33.92% of the global market in 2025.

Europe

Europe accounted for USD 3.03 billion, representing 17.54% of global revenue in 2025.

Asia Pacific

Asia Pacific generated USD 2.98 billion, accounting for 17.22% of the global market in 2025.

U.S.

Market reached USD 4.85 billion in 2025 and USD 6.13 billion in 2026.

Japan

Market reached USD 0.59 billion in 2025 and USD 0.75 billion in 2026.

Read More

AI in Power Utilities Market Trends

Increasing Integration of AI with Smart Grids and DERs are Amplifying Market Growth

A major trend in AI in power utilities is the rapid integration of AI with smart grids and distributed energy resources (DERs). As per the International Energy Agency (IEA), global renewable capacity additions exceeded 500 GW in 2023, significantly increasing grid complexity. Utilities are leveraging AI to manage bidirectional power flows, optimize voltage, and balance intermittent sources such as solar and wind. For instance, National Grid UK uses AI-driven forecasting tools to predict renewable output and maintain grid stability. Additionally, the rise of electric vehicles, expected to reach ~240 million globally by 2030 (IEA), is further driving the need for intelligent grid management systems. This trend is pushing utilities toward advanced AI-enabled platforms such as DERMS (Distributed Energy Resource Management Systems), making AI a core component of next-generation grid infrastructure.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Growing Need for Grid Reliability and Efficiency to Push Market Growth

One of the primary drivers of AI adoption in power utilities is the increasing need to improve grid reliability and operational efficiency. Aging infrastructure remains a major concern, particularly in developed markets—over 70% of transmission lines in the U.S. are more than 25 years old (U.S. DOE). AI-based predictive maintenance helps utilities detect faults early and reduce unplanned outages. For example, utilities deploying AI-driven asset monitoring have reported 10–20% reductions in maintenance costs and improved asset lifespans. Furthermore, rising electricity demand—projected to grow by ~3% annually through 2030 (IEA)—requires utilities to optimize existing infrastructure rather than rely solely on new investments. AI enables real-time monitoring, faster fault detection, and automated decision-making, making it a critical tool for enhancing grid performance and ensuring uninterrupted power supply.

Market Restraints

Data Silos and Legacy Infrastructure Limit AI Deployment to Limit the Market Growth

A key restraint in the adoption of AI in power utilities is the prevalence of legacy systems and fragmented data environments. Many utilities still rely on outdated SCADA and IT systems that are not designed to handle modern AI workloads. According to the World Bank and industry studies, digitalization levels in utilities remain relatively low, with IT spending often limited to 2–4% of total revenue. This creates challenges in integrating data across departments such as generation, transmission, and customer operations. For instance, utilities may struggle to combine real-time grid data with historical maintenance records, limiting the effectiveness of AI models. Additionally, upgrading legacy infrastructure requires significant capital investment and organizational change, slowing down AI adoption despite its proven benefits.

Market Opportunities

Expansion of AI in Renewable Energy Integration to Create New Growth Avenues

The transition toward renewable energy presents a significant opportunity for AI in power utilities. With renewables expected to account for over 50% of global electricity generation growth by 2030 (IEA), utilities face increasing variability in power supply. AI can enhance renewable forecasting accuracy by up to 20–30%, enabling better scheduling and grid balancing. For example, Google’s DeepMind has demonstrated AI models that improved wind power prediction accuracy by 20%, increasing the value of the wind energy sector. Additionally, emerging technologies such as energy storage and microgrids rely heavily on AI for optimal operation. As countries accelerate decarbonization efforts and invest in clean energy infrastructure, AI will play a crucial role in ensuring efficient integration and utilization of renewable resources, creating substantial growth opportunities.

Market Challenges

Cybersecurity Risks in AI-Driven Grid Systems to Limit Market Growth

As utilities increasingly adopt AI and digital technologies, cybersecurity has become a critical challenge. Power grids are classified as critical infrastructure, making them prime targets for cyberattacks. According to the International Energy Agency, cyberattacks on energy utilities have increased significantly in recent years, with incidents affecting grid operations and data integrity. AI systems, while enhancing efficiency, also expand the attack surface by introducing more connected devices and data flows. For instance, ransomware attacks on utilities have caused operational disruptions and financial losses in multiple regions. Ensuring the security of AI technologies models, data pipelines, and operational technology (OT) systems requires continuous investment in cybersecurity measures. Utilities must adopt AI-driven threat detection and adhere to stringent regulatory frameworks to mitigate risks, making cybersecurity a major operational challenge in the AI adoption journey.

Segmentation Analysis

By Technology

Utilization Across Multiple Utility Functions Led to Machine Learning Segment Growth

Based on technology, the market is segmented into machine learning, optimization algorithms, deep learning, NLP & conversational AI, and others.

Machine Learning (ML) represents the largest and most foundational technology segment within the market, accounting for approximately 37.27% of share in 2025. Its dominance is driven by its versatility across multiple utility functions, including predictive maintenance, demand forecasting, grid optimization, and fraud detection. ML algorithms, such as regression models, decision trees, and clustering techniques, are widely used to process large volumes of structured and unstructured data generated from smart meters, sensors, and SCADA systems.

NLP & conversational AI is the fastest growing segment in the market with a CAGR of 21.21% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Requirement of Low Latency and High Reliability to Boost On-Premise Segment Growth

Based on deployment, the market is segmented into cloud and on-premise.

The on-premise segment accounted for approximately 60.36% of the market share in 2025. The segment’s growth is particularly influenced by critical grid operations and regions with strict data sovereignty requirements. Utilities prefer on-premise solutions for core systems, such as SCADA, EMS, and grid control, due to the need for low latency, high reliability, and enhanced cybersecurity control. This model is especially prevalent in legacy infrastructure environments and in countries with stringent regulatory frameworks. While on-premise solutions offer greater control over data and system performance, they involve higher capital expenditure and longer deployment timelines. As a result, this segment is growing at a relatively moderate rate (CAGR ~12–16%), with many utilities gradually transitioning toward hybrid models that combine on-premise reliability with cloud-based analytics capabilities.

The cloud segment is expected to grow at a CAGR of 20.21% during the forecast period.

By Application

Increasing Grid Complexity Due to Renewable Energy Integration Propelled Grid Optimization & Smart Grid Segment Growth

Based on application, the market is segmented into grid optimization & smart grid, energy trading optimization, customer analytics & demand response, predictive maintenance, forecasting, and others.

The grid optimization & smart grid segment represented the largest share of around 28.94% in the market in 2025. This growth is driven by increasing grid complexity due to renewable energy integration and Distributed Energy Resources (DERs). AI enables real-time load balancing, voltage optimization, and fault detection, improving grid reliability and efficiency. Utilities are deploying advanced systems such as ADMS and DERMS to manage bi-directional power flows. With global renewable capacity additions exceeding 500 GW annually (IEA), the need for intelligent grid management is accelerating, making this segment a core investment area.

Energy trading optimization is the fastest-growing segment with a CAGR of 20.94% over the forecast period.

AI in Power Utilities Market Regional Outlook

By region, the AI in Power Utilities market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America AI in Power Utilities Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America is the dominant region, with a market valued at USD 5.86 billion in 2025, accounting for approximately 33.92% of the global market. North America is one of the most advanced markets driven by high digital maturity and a liberalized electricity market. Aging infrastructure, with more than 70% of transmission lines over 25 years old (DOE), is further accelerating AI adoption in predictive maintenance and grid reliability. Additionally, increasing renewable penetration and EV adoption are pushing utilities to invest in AI-driven grid optimization. Major utilities and ISOs (such as PJM and CAISO) actively use AI for forecasting and market operations, making North America a mature and innovation-driven region.

U.S. AI in Power Utilities Market

The U.S. market was valued at USD 4.85 billion in 2025 and is estimated to reach USD 6.13 billion in 2026. The U.S. is a mature market with strong AI adoption across grid optimization, energy trading, and customer analytics. Over 110 million smart meters enable advanced demand response and analytics (EIA). Liberalized markets such as PJM and CAISO drive high adoption of AI in trading and forecasting. Aging infrastructure is also accelerating predictive maintenance deployments.

Europe

Europe accounted for USD 3.03 billion in 2025, representing approximately 17.54% of global revenues. Europe is one of the most advanced markets for AI in power utilities, driven by ambitious decarbonization targets, rapid renewable energy integration, and large-scale grid modernization programs.

- According to the European Commission, renewable energy accounted for around 44% of the EU’s electricity generation in 2023, creating growing demand for AI-based forecasting, grid balancing, and energy management solutions. In addition, the EU plans to invest over EUR 584 billion (~USD 659.14 billion) in electricity grids by 2030, including substantial spending on digital and smart grid infrastructure, which is accelerating the deployment of AI-enabled monitoring and automation technologies.

The region’s interconnected electricity markets, including Nord Pool and EPEX SPOT, further support the adoption of AI for energy trading optimization and load forecasting. Moreover, widespread smart meter deployment across countries such as Italy, Spain, France, and the U.K. is enabling utilities to leverage AI for demand response, outage prediction, and customer analytics.

Germany AI in Power Utilities Market

Germany was valued at USD 0.28 billion in 2025 and is estimated to reach USD 0.36 billion in 2026. Germany is a leader in AI-driven grid optimization due to high renewable penetration, with renewables contributing over 50% of electricity generation at times (IEA). This creates strong demand for forecasting and grid balancing solutions. The country also benefits from advanced energy markets, supporting AI in trading and system optimization.

U.K. AI in Power Utilities Market

The U.K. market was valued at USD 0.56 billion in 2025 and is estimated to reach USD 0.70 billion in 2026. The country has a highly liberalized electricity market, driving strong adoption of AI in energy trading and demand response. Large-scale smart meter rollout (targeting ~53 million installations) supports customer analytics. High offshore wind capacity further increases reliance on AI for forecasting and grid stability.

Asia Pacific

Asia Pacific market is valued at USD 2.98 billion in 2025, accounting for approximately 17.22% of global revenues. Asia Pacific is the fastest-growing region in the AI in power utilities market, driven by rapid electrification, grid modernization, and rising renewable energy integration. China dominates the regional market through extensive investments in smart grids and transmission infrastructure. According to the International Energy Agency (IEA), China accounted for nearly 60% of global renewable capacity additions in 2024, highlighting the increasing requirement for AI-based grid balancing, renewable forecasting, and predictive maintenance solutions. Additionally, China’s State Grid announced investments exceeding CNY 520 billion (~USD 72 billion) in power grid infrastructure in 2024, including digital substations and intelligent transmission networks, further supporting AI deployment across utility operations.

India is also emerging as a major growth market due to rapid power sector digitalization and distribution reforms. According to the Ministry of Power, India achieved over 222 GW of installed renewable energy capacity by early 2025, significantly increasing grid complexity and the need for AI-enabled forecasting and energy management systems. Furthermore, under the Revamped Distribution Sector Scheme (RDSS), more than 120 million smart meters had already been sanctioned by 2025, enabling utilities to enhance demand response, outage detection, and customer analytics capabilities.

Japan and Australia are similarly increasing investments in AI-driven distributed energy resource management and virtual power plant optimization to support renewable-heavy grids. Rising electricity consumption, urbanization, and smart grid investments across the region continue to accelerate AI adoption in power utility operations.

China AI in Power Utilities Market

China remains the dominant contributor in Asia Pacific, valued at USD 0.98 billion in 2025, and is estimated to reach USD 1.25 billion in 2026. China leads in grid infrastructure investment and smart grid deployment, with extensive Ultra-High Voltage (UHV) networks. AI adoption is heavily focused on grid optimization and predictive maintenance. Limited market liberalization results in lower use of AI in energy trading compared to Western markets.

India AI in Power Utilities Market

The Indian market was valued at USD 0.37 billion in 2025 and is estimated to reach USD 0.48 billion in 2026. India is rapidly adopting AI, driven by large-scale digital initiatives such as the 250 million smart meter program. AI is widely used for loss reduction, customer analytics, and grid optimization. The growing electricity demand and renewable expansion are further accelerating adoption.

Japan AI in Power Utilities Market

Japan was valued at USD 0.59 billion in 2025 and is estimated to reach USD 0.75 billion in 2026. Japan focuses on AI for grid reliability, predictive maintenance, and renewable integration. Post-Fukushima energy restructuring has increased emphasis on efficiency and distributed energy systems. Moderate market liberalization supports gradual growth in trading-related AI applications.

Latin America

Latin America accounted for USD 1.69 billion in 2025, accounting for approximately 9.77% of global revenues. The region is an emerging market for AI in power utilities, with growth driven by the need to improve grid reliability and reduce losses. Countries such as Brazil and Mexico are investing in smart grid technologies and renewable energy, with Brazil having one of the largest renewable shares in its energy mix. Non-technical losses (electricity theft) remain high in several countries, often exceeding 15–20% in some regions, as per the World Bank estimates, further driving adoption of AI-based fraud detection and revenue protection solutions. Predictive maintenance is also a key focus due to aging infrastructure. While digital maturity is lower compared to North America and Europe, increasing investments and regulatory reforms are supporting gradual AI adoption.

Middle East & Africa

The Middle East & Africa region was valued at USD 3.73 billion in 2025. The region is in the early-to-growth stage of AI adoption in power utilities, with strong investments in grid modernization and energy diversification. GCC countries are leading the region, investing heavily in smart grid infrastructure and renewable projects under initiatives such as Saudi Vision 2030. For instance, large-scale solar projects in the UAE and Saudi Arabia are increasing the need for AI-based forecasting and grid optimization. In Africa, utilities face challenges such as unreliable grids and high technical losses, prompting the use of AI for predictive maintenance and fault detection. Additionally, cybersecurity is becoming a major focus due to increasing digitalization of critical infrastructure, further driving AI adoption in the region.

GCC AI in Power Utilities Market

The GCC market was valued at USD 2.78 billion in 2025 and is estimated to reach USD 3.50 billion in 2026. GCC countries are investing heavily in smart grids and renewable energy under national visions (e.g., Saudi Vision 2030). AI adoption is concentrated in grid optimization, predictive maintenance, and forecasting for large-scale solar projects. Limited electricity market liberalization keeps trading-related AI relatively low.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Investment in AI-Enabled Grid Management Platforms by Key Players are Boosting Market Share

Siemens AG, General Electric (GE Vernova), Schneider Electric, ABB Ltd., and IBM are among the most influential technology companies driving AI adoption in power utilities. These companies are operating with broadly aligned strategies centered on digitalization, grid intelligence, and operational optimization. These companies are investing heavily in AI-enabled grid management platforms, including Advanced Distribution Management Systems (ADMS), Energy Management Systems (EMS), and Distributed Energy Resource Management Systems (DERMS), to handle increasing renewable penetration and grid decentralization. For example, they are deploying AI models for real-time load balancing, congestion management, and voltage optimization to improve grid stability. One of the major focuses is on predictive maintenance and asset performance management, where AI is used to analyze sensor and historical data from turbines, transformers, and transmission assets. This helps utilities reduce unplanned outages and lower maintenance costs by 10–20%, while extending asset lifecycles.

List of Key AI in Power Utilities Companies Profiled

- Siemens AG (Germany)

- GE Vernova (U.S.)

- Schneider Electric (France)

- ABB Ltd. (Switzerland)

- Oracle Utilities (U.S.)

- SAP (Germany)

- IBM (U.S.)

- Microsoft (U.S.)

- Google (Alphabet) (U.S.)

- Amazon Web Services (AWS) (U.S.)

- AutoGrid Systems (U.S.)

- ai (U.S.)

- Uplight (U.S.)

- SparkCognition (U.S.)

- Bidgely (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Microsoft expanded Azure AI for Energy with new capabilities for digital twins and grid optimization. The update enables utilities to simulate grid behavior and improve forecasting accuracy using AI models. It reinforces Microsoft’s role as a key cloud and AI partner for utilities.

- January 2026: GE Vernova expanded its GridOS AI suite to include advanced predictive outage management and renewable forecasting capabilities. The platform integrates AI with grid operations to improve resilience and reduce downtime. This aligns with rising global demand for grid modernization and decarbonization.

- December 2025: ABB launched new AI-enabled features in its Ability™ Energy Management suite, targeting asset performance and grid reliability. The solution leverages machine learning for early fault detection and maintenance planning. This strengthens ABB’s digital offerings for utility-scale infrastructure.

- November 2025: Schneider Electric introduced enhanced AI-driven automation within its EcoStruxure Grid solutions, focusing on real-time monitoring and predictive analytics. The upgrade helps utilities optimize energy flows and reduce operational costs. It also supports integration of distributed energy resources.

- October 2025: Siemens enhanced its Gridscale X platform with advanced AI modules focused on DER orchestration and real-time grid analytics. The update enables utilities to manage increasing renewable penetration and EV load more efficiently. It also strengthens Siemens’ position in next-generation smart grid software.

REPORT COVERAGE

The report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 19.31% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Technology

|

|

By Deployment

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 17.29 billion in 2025 and is projected to reach USD 89.64 billion by 2034.

In 2025, the market value stood at USD 5.86 billion.

The market is expected to exhibit a CAGR of 19.31% during the forecast period.

By technology, the machine learning segment is expected to lead the market.

The growing need for grid reliability and efficiency are the key factors driving market expansion.

Siemens AG, GE Vernova, Schneider Electric, ABB Ltd., and IBM are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 326

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us